| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 191.8 Million |

| Market Size (2030) | USD 250.6 Million |

| CAGR (2025 - 2030) | 5.49 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Middle East Commercial Aircraft In-Flight Entertainment System Market Analysis

The Middle East Commercial Aircraft In-Flight Entertainment System Market size is estimated at 191.8 million USD in 2025, and is expected to reach 250.6 million USD by 2030, growing at a CAGR of 5.49% during the forecast period (2025-2030).

The Middle East commercial aircraft in-flight entertainment system (IFES) industry is undergoing a significant technological transformation, driven by airlines' focus on enhancing passenger experience through advanced digital solutions. Airlines across the region are increasingly adopting next-generation airline entertainment systems featuring 4K OLED displays, Bluetooth connectivity, and high-power USB charging capabilities. This technological advancement is particularly evident in the economy and premium economy segments, which accounted for approximately 90% of all IFE system installations in narrowbody aircraft during 2022. The integration of these advanced systems reflects the industry's commitment to providing enhanced entertainment options across all cabin classes.

The regional aviation landscape is witnessing unprecedented fleet modernization initiatives, with major carriers implementing comprehensive aircraft renewal programs. According to recent industry data, leading Middle Eastern carriers including Air Arabia, Emirates, and Etihad have collectively placed orders for 804 new aircraft, comprising 391 narrowbody and 413 widebody planes. This substantial fleet expansion is particularly concentrated in the UAE, where the three major carriers - Emirates, Etihad, and Flydubai - have ordered 361 new aircraft, demonstrating their commitment to maintaining modern, efficient fleets equipped with state-of-the-art aircraft entertainment systems.

Manufacturing and supply chain dynamics in the IFES sector are evolving, with major system providers focusing on developing lighter, more energy-efficient solutions. Industry leaders are introducing innovative products such as 4K screens with High Dynamic Range (HDR) capabilities and advanced seat-end entertainment solutions, specifically designed for both narrowbody and widebody aircraft. The industry is witnessing a significant transformation in product development, with manufacturers emphasizing solutions that are up to 30% lighter than conventional systems while offering superior performance and reliability.

Looking ahead, the industry is positioned for substantial growth, supported by Boeing's forecast that the Middle East will require approximately 3,400 new aircraft over the next two decades to meet rising passenger demands. This expansion is complemented by confirmed delivery schedules for 944 new aircraft in the region between 2023 and 2030, comprising 543 narrowbody and 401 widebody aircraft. These deliveries will primarily serve major markets including Saudi Arabia, Qatar, and the United Arab Emirates, reflecting the region's position as a global aviation hub and its airlines' commitment to providing superior passenger entertainment systems experiences.

Middle East Commercial Aircraft In-Flight Entertainment System Market Trends

The main reasons for market growth are the expansion of the fleet and the increased demand for passenger air travel in Middle Eastern countries

- The aviation industry in the Middle East recovered from the COVID-19 pandemic faster and stronger than the rest of the world. In 2021, air passenger traffic in the Middle East reached 302 million, a growth of 249% compared to 2020 and 25% compared to 2019. The increase in air passenger traffic may eventually drive new aircraft procurements, boosting the cabin interior market in the region. Major airlines have adopted fleet expansion strategies.

- A total of 498 new aircraft were delivered in the region between 2017 and 2022. During 2023-2030, around 1,058 new aircraft are expected to be delivered in the region. During the forecast period, the majority of aircraft are expected to be narrowbody. In addition, the popularity of small and economical aircraft, the success of low-cost carriers, and the advent of narrowbodies with long ranges have contributed to this trend. Saudi Arabia and the United Arab Emirates are the major countries accounting for a significant number of aircraft deliveries.

- New aircraft deliveries and backlogs are expected to generate demand for cabin interiors, as various airlines in the region are opting for advanced aircraft systems and components such as LED cabin lights, wireless lightweight IFES, comfortable, lightweight seats, and other cabin products. As of November 2022, major airlines, such as Emirates, Qatar Airways, Saudia Arabia Airlines, Etihad Airways, and FlyDubai Airlines, together had a backlog of over 1,013 aircraft, of which 589 were expected to be narrowbody jets. Factors such as these are expected to drive the cabin interior market positively during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Consistent growth in air travel is the driving factor for air passenger traffic in the Middle East

- The Middle East, a popular connection point for international travelers and trade, is also growing as a starting point and destination for business and leisure passengers. In 2020, air passenger traffic in the Middle East dropped by 64% due to travel restrictions caused by the COVID-19 pandemic. However, in 2022, due to the rising vaccination rates and strong demand over the holiday season, air passenger traffic in the region reached 349.5 million, a growth of 16% compared to 2021, while the growth was at 45% compared to 2019. Major countries, such as the United Arab Emirates and Saudi Arabia, accounted for 42% of the total air passenger traffic, generating higher demand for new aircraft compared to other Middle Eastern countries.

- In 2022, passenger capacity increased by 73.8%, and passenger load factor grew by 24.6% to 75.8% compared to 2021. Air travel recovery in the region continues to gather momentum, and air passenger traffic is expected to double within the next 20 years. Many major Middle Eastern international route areas in Bahrain, Kuwait, Oman, Saudi Arabia, the United Arab Emirates, Iraq, Iran, Jordan, Yemen, and Qatar are already exceeding pre-COVID-19 levels. Such factors indicate that air travel has recovered and continues to gather momentum. Many major international routes, even within the Middle East, are already exceeding pre-COVID-19 levels. Tourism and the high willingness to travel continue to foster the industry’s recovery in the Middle East & Africa. The air passenger traffic levels are expected to grow by 34% in 2030 compared to 2022.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Saudi Arabia records the highest GDP per capita in the region

- Major original equipment manufacturers (OEMs) in the sector, Boeing and Airbus, are expected to increase their production between 2023 and 2030, resulting in a balanced aircraft supply chain

- Saudi Arabia and UAE emphasized airport development and expansion projects in the region

- The primary source of revenue for aircraft manufacturers is derived from commercial aircraft orders placed with major airlines

- The aviation industry's growth is driven by the rising air travel and the high volume of aircraft orders placed by various airlines

- Airlines planning to reduce aircraft fuel consumption by opting for innovative lightweight cabin interior products is a driving factor

Segment Analysis: Aircraft Type

Widebody Segment in Middle East Commercial Aircraft IFE System Market

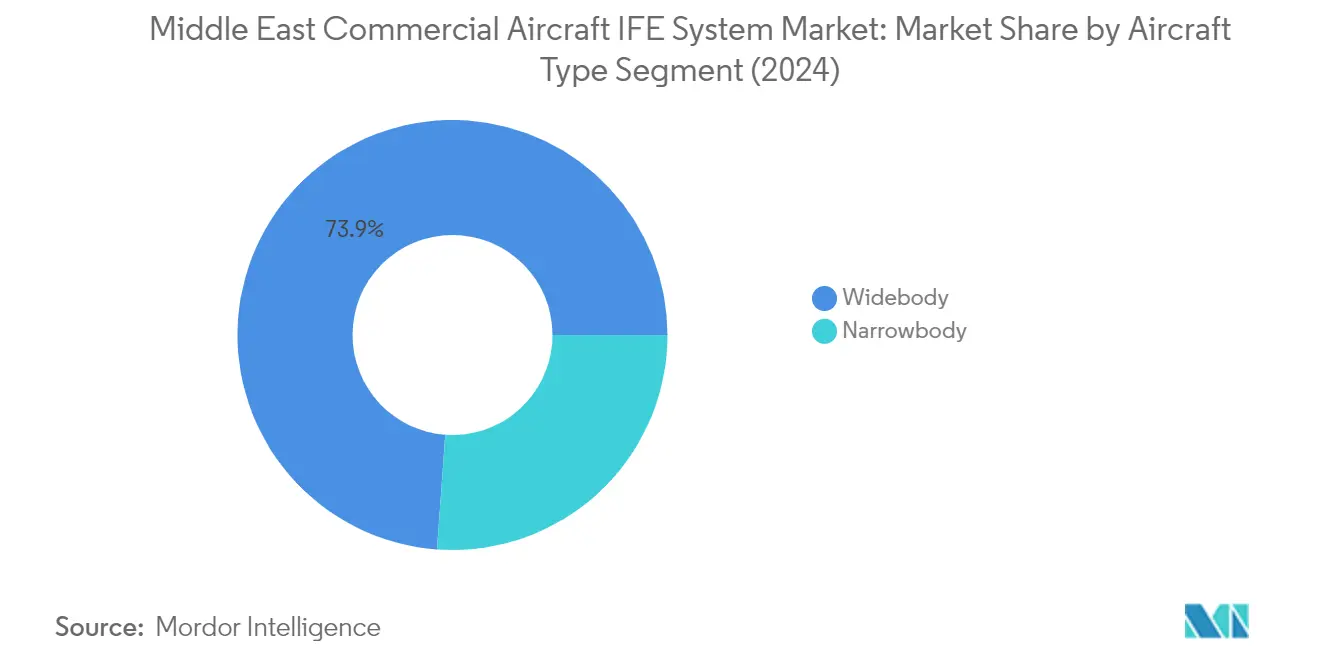

The widebody segment dominates the Middle East Commercial Aircraft In-Flight Entertainment (IFE) System market, commanding approximately 74% market share in 2024. This significant market position is primarily driven by the segment's extensive use in long-haul flights, where aircraft entertainment system plays a crucial role in enhancing the passenger experience. Major airlines in the region, including Emirates, Qatar Airways, and Etihad Airways, are heavily investing in widebody aircraft equipped with advanced IFE systems. The segment is also experiencing robust growth, projected to expand at around 6% from 2024 to 2029, making it the fastest-growing segment in the market. This growth is fueled by increasing fleet expansion programs of major Middle Eastern carriers and their focus on improving passenger amenities, particularly on long-haul routes exceeding 7 hours. Airlines are increasingly seeking ways to enhance customer experience by providing individual seatback screens with advanced features like 4K OLED displays and Bluetooth connectivity, particularly in their widebody fleets.

Narrowbody Segment in Middle East Commercial Aircraft IFE System Market

The narrowbody segment plays a vital role in the Middle East Commercial Aircraft IFE System market, particularly in serving regional and short-haul routes. This segment has gained significant traction with the rising popularity of low-cost carriers and the increasing deployment of narrowbody aircraft on medium-haul routes. Airlines are focusing on improving passenger comfort by providing advanced onboard entertainment systems even in narrowbody aircraft, with features like 4K screens and Bluetooth audio capabilities. The trend of using narrowbody aircraft on longer routes of 6-7 hours has also prompted airlines to enhance their passenger entertainment systems offerings in this segment, making it an important component of the overall market landscape.

Middle East Commercial Aircraft In-Flight Entertainment System Market Geography Segment Analysis

Middle East Commercial Aircraft In-Flight Entertainment System Market in United Arab Emirates

The United Arab Emirates dominates the Middle East commercial aircraft in-flight airline entertainment system market, accounting for approximately 50% of the total market value in 2024. The country's aviation sector significantly contributes to its economy, representing about 13.3% of the UAE's GDP. Major airlines in the UAE are actively investing in advanced IFE systems to enhance passenger experience. For instance, Flydubai has implemented Safran's RAVE Ultra IFE system across its new B737 Max fleet, featuring full HD 11.6-inch screens in economy class and 15.6-inch displays in business class. Similarly, Etihad Airways has focused on providing superior entertainment options with 18.5-inch screens in business class and 13.3-inch screens in economy class for its A350-1000 aircraft. The UAE's position as a global aviation hub and its airlines' commitment to passenger comfort continue to drive the demand for sophisticated passenger entertainment systems.

Middle East Commercial Aircraft In-Flight Entertainment System Market in Saudi Arabia

Saudi Arabia's commercial aircraft in-flight cabin entertainment system market is projected to grow at approximately 9% annually from 2024 to 2029. The kingdom's aviation sector has embarked on an ambitious transformation journey as part of its Vision 2030 initiative. The country's national carrier, Saudi Arabian Airlines, has been at the forefront of implementing cutting-edge IFE technologies, particularly focusing on 4K and Bluetooth audio innovations. The airline's commitment to passenger experience is evident in its aircraft configurations, with business class cabins featuring a full 4K experience on 16-inch screens and economy class equipped with 12-inch 4K screens. The establishment of new airlines and the expansion of existing carriers in the kingdom have created additional opportunities for IFE system providers. The government's focus on developing the aviation sector as a key economic driver continues to attract investments in advanced aircraft technologies, including state-of-the-art entertainment systems.

Middle East Commercial Aircraft In-Flight Entertainment System Market in Other Middle Eastern Countries

The commercial aircraft in-flight entertainment system market in other Middle Eastern countries encompasses several emerging aviation markets, including Qatar, Bahrain, Kuwait, Oman, and Iran. These countries have demonstrated varying levels of investment in aviation infrastructure and fleet modernization. Qatar, in particular, has shown significant commitment to enhancing its aviation capabilities with advanced IFE systems. The region's airlines are increasingly focusing on providing premium passenger experiences through sophisticated entertainment options. The growing emphasis on regional connectivity and tourism development has prompted airlines to invest in modern aircraft equipped with advanced IFE systems. Despite challenges such as market volatility and regional competition, these countries continue to prioritize passenger comfort and experience through investments in modern aircraft interiors and entertainment systems. The diverse nature of these markets, combined with their unique aviation development strategies, contributes to the overall dynamism of the Middle East's commercial aircraft IFE system market.

Get Analysis on Important Geographic Markets

Download PDF

Middle East Commercial Aircraft In-Flight Entertainment System Industry Overview

Top Companies in Middle East Commercial Aircraft In-Flight Entertainment System Market

The Middle Eastern commercial aircraft entertainment system market is characterized by continuous product innovation, with companies focusing on developing advanced IFE solutions featuring 4K displays, OLED technology, and enhanced connectivity options. Major players are demonstrating operational agility through partnerships with airlines and seat manufacturers to create integrated entertainment solutions. Strategic moves in the region primarily revolve around securing long-term agreements with prominent carriers like Emirates, Qatar Airways, and Etihad Airways. Companies are expanding their presence through regional offices and service centers, particularly in aviation hubs like Dubai and Abu Dhabi. The emphasis on lightweight systems and improved passenger experience drives technological advancement, while the integration of Bluetooth connectivity and personalized content delivery showcases the industry's adaptation to changing consumer preferences.

Consolidated Market Led By Global Players

The market structure is highly consolidated with global technology conglomerates dominating the landscape, particularly in the widebody aircraft segment. The top three players account for a significant majority of the market share, leveraging their established relationships with aircraft manufacturers and airlines. These dominant players maintain their position through extensive research and development capabilities, comprehensive product portfolios, and strong after-sales support networks. The market shows limited participation from local players, with most competition coming from established international aviation technology providers.

The industry exhibits minimal merger and acquisition activity, with companies preferring strategic partnerships and joint development agreements over outright acquisitions. Market leaders focus on organic growth through product development and service expansion rather than inorganic growth strategies. The competitive dynamics are shaped by long-term supply agreements and the high barriers to entry created by certification requirements and established airline relationships. Regional presence and local support capabilities have become crucial differentiators in securing new contracts and maintaining existing relationships.

Innovation and Customer Relations Drive Success

For incumbent players to maintain and expand their market share, focus needs to be placed on developing lighter, more energy-efficient systems while maintaining high reliability and performance standards. Success factors include the ability to offer customized solutions for different aircraft types and airline requirements, strong local support infrastructure, and seamless integration capabilities with other aircraft systems. Companies must also invest in next-generation technologies while maintaining backward compatibility with existing aircraft fleets to ensure long-term market relevance.

New entrants and challenger companies need to focus on developing niche capabilities or specialized solutions that address specific market gaps or emerging needs. Building relationships with regional airlines, particularly low-cost carriers expanding their fleets, presents opportunities for market entry. The regulatory environment favors companies with established safety certifications and compliance records, making strategic partnerships with certified providers a viable entry strategy. Success in this market increasingly depends on the ability to offer comprehensive solutions that combine hardware, content, and connectivity services while maintaining cost competitiveness and operational efficiency. The integration of passenger entertainment system solutions that enhance the overall travel experience is becoming a critical factor for success.

Middle East Commercial Aircraft In-Flight Entertainment System Market Leaders

-

Burrana

-

IMAGIK International Corp.

-

Latecoere

-

Panasonic Avionics Corporation

-

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Middle East Commercial Aircraft In-Flight Entertainment System Market News

- September 2022: Emirates has selected Thales’ AVANT Up, the next generation inflight entertainment system for their new fleet of Airbus A350s.

- June 2022: Qatar Airways Signs Deal With Panasonic Avionics To Provide Astrova for Boeing 777x Fleet.

- June 2022: Recaro Aircraft Seating partnered with Panasonic Avionics Corporation (Panasonic Avionics) to unveil a new in-flight entertainment seat-end solution installed on the CL3810 economy class seat.

Free With This Report

We provide a complimentary and exhaustive set of data points on global and regional metrics that present the fundamental structure of the industry. Presented in the form of 35+ free charts, the section covers data on commercial aircraft deliveries by manufacturer, number of flights performed by global airline industry, fuel costs of airlines as a percentage of expenditure, fuel consumption of commercial airlines, average price of brent crude oil, inflation, commercial aircraft cabin seating volume share by region and commercial aircraft windows by region.

Middle East Commercial Aircraft In-Flight Entertainment System Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

-

5.2 Country

- 5.2.1 Saudi Arabia

- 5.2.2 United Arab Emirates

- 5.2.3 Rest of Middle East

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles

- 6.4.1 Burrana

- 6.4.2 IMAGIK International Corp.

- 6.4.3 Latecoere

- 6.4.4 Panasonic Avionics Corporation

- 6.4.5 Thales Group

- *List Not Exhaustive

7. KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- AIR PASSENGER TRAFFIC, BY COUNTRY, NUMBER OF PASSENGERS TRAVELLED, MIDDLE EAST, 2017 - 2030

- Figure 2:

- NEW AIRCRAFT DELIVERIES, NUMBER OF AIRCRAFTS DELIVERED, MIDDLE EAST, 2017 - 2030

- Figure 3:

- GDP PER CAPITA (CURRENT PRICE), BY COUNTRY, USD, MIDDLE EAST, 2017 - 2030

- Figure 4:

- REVENUE OF AIRCRAFT MANUFACTURERS, USD, MIDDLE EAST, 2017 - 2022

- Figure 5:

- AIRCRAFT BACKLOG BY MANUFACTURER, NUMBER OF AIRCRAFT, MIDDLE EAST, 2017 - 2023

- Figure 6:

- GROSS ORDERS, BY MANUFACTURER, NUMBER OF AIRCRAFT, MIDDLE EAST, 2017 - 2022

- Figure 7:

- EXPENDITURE ON AIRPORT CONSTRUCTION PROJECTS (ONGOING), % SHARE, MIDDLE EAST VS OTHERS ,2022

- Figure 8:

- EXPENDITURE OF AIRLINES ON FUEL, % SHARE, MIDDLE EAST, 2017 - 2022

- Figure 9:

- MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, VALUE, USD, 2017 - 2030

- Figure 10:

- VALUE OF MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, BY AIRCRAFT TYPE, USD, MIDDLE EAST, 2017 - 2030

- Figure 11:

- VALUE SHARE OF MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, BY AIRCRAFT TYPE, %, MIDDLE EAST, 2017 VS 2023 VS 2030

- Figure 12:

- VALUE OF NARROWBODY MARKET, USD, MIDDLE EAST , 2017 - 2030

- Figure 13:

- VALUE SHARE OF NARROWBODY BY CABIN CLASS, USD, MIDDLE EAST, 2023 VS 2030

- Figure 14:

- VALUE OF WIDEBODY MARKET, USD, MIDDLE EAST , 2017 - 2030

- Figure 15:

- VALUE SHARE OF WIDEBODY BY CABIN CLASS, USD, MIDDLE EAST, 2023 VS 2030

- Figure 16:

- VALUE OF MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, BY COUNTRY, USD, MIDDLE EAST, 2017 - 2030

- Figure 17:

- VALUE SHARE OF MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, BY COUNTRY, %, MIDDLE EAST, 2017 VS 2023 VS 2030

- Figure 18:

- VALUE OF SAUDI ARABIA MARKET, USD, SAUDI ARABIA , 2017 - 2030

- Figure 19:

- VALUE SHARE OF SAUDI ARABIA BY AIRCRAFT TYPE, USD, SAUDI ARABIA, 2023 VS 2030

- Figure 20:

- VALUE OF UNITED ARAB EMIRATES MARKET, USD, UNITED ARAB EMIRATES , 2017 - 2030

- Figure 21:

- VALUE SHARE OF UNITED ARAB EMIRATES BY AIRCRAFT TYPE, USD, UNITED ARAB EMIRATES, 2023 VS 2030

- Figure 22:

- VALUE OF REST OF MIDDLE EAST MARKET, USD, REST OF MIDDLE EAST , 2017 - 2030

- Figure 23:

- VALUE SHARE OF REST OF MIDDLE EAST BY AIRCRAFT TYPE, USD, REST OF MIDDLE EAST, 2023 VS 2030

- Figure 24:

- NUMBER OF STRATEGIC MOVES OF MOST ACTIVE COMPANIES, MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, MIDDLE EAST, 2017 - 2022

- Figure 25:

- TOTAL NUMBER OF STRATEGIC MOVES OF COMPANIES, MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET, MIDDLE EAST, 2017 - 2022

- Figure 26:

- MARKET SHARE OF MIDDLE EAST COMMERCIAL AIRCRAFT IN-FLIGHT ENTERTAINMENT SYSTEM MARKET (%), BY SUPPLIER, 2022

Middle East Commercial Aircraft In-Flight Entertainment System Industry Segmentation

Narrowbody, Widebody are covered as segments by Aircraft Type. Saudi Arabia, United Arab Emirates are covered as segments by Country.| Aircraft Type | Narrowbody |

| Widebody | |

| Country | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Need A Different Region or Segment?

Customize Now

Market Definition

- Product Type - Entertainment provided to aircraft passengers during a flight refers to In-flight entertainment. The seatback screens which are used to provide entertainment are included under the IFE system product type.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF