Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

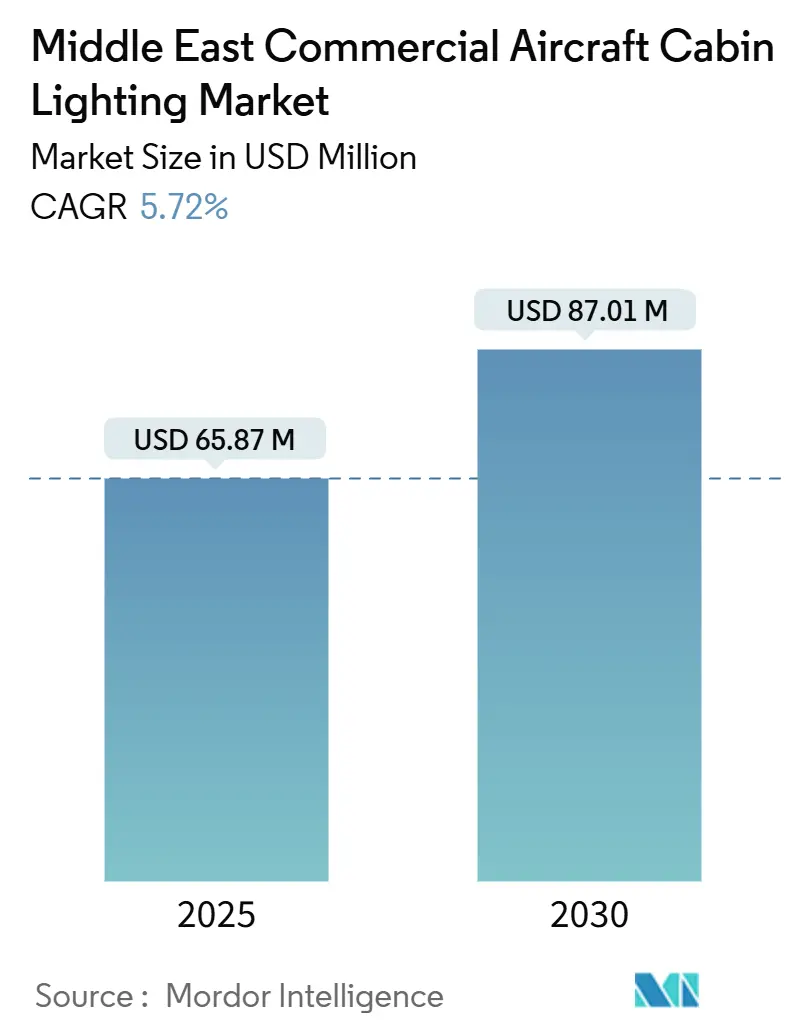

| Market Size (2025) | USD 65.87 Million |

| Market Size (2030) | USD 87.01 Million |

| Growth Rate (2025 - 2030) | 5.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Commercial Aircraft Cabin Lighting Market Analysis by Mordor Intelligence

The Middle East commercial aircraft cabin lighting market size stands at USD 65.87 million in 2025 and is projected to reach USD 87.01 million by 2030, expanding at a 5.72% CAGR. This growth trajectory is underpinned by the region’s fleet-expansion wave, sizeable retrofit programs, and human-centric lighting upgrades that position the Middle East commercial aircraft cabin lighting market at the heart of a fast-evolving aviation ecosystem. Demand is concentrated in narrowbody fleets, premium-cabin refurbishments, and domestic localization initiatives that align with Saudi Vision 2030. Airlines prioritize ceiling and wall lighting to create immersive brand experiences, while supply-chain bottlenecks around semiconductors are accelerating regional manufacturing incentives. Competitive intensity remains moderate; incumbent OEMs leverage long-standing airline contracts. However, OLED integration and rapid-install LED retrofits redefine product roadmaps across the Middle East commercial aircraft cabin lighting market.

Key Report Takeaways

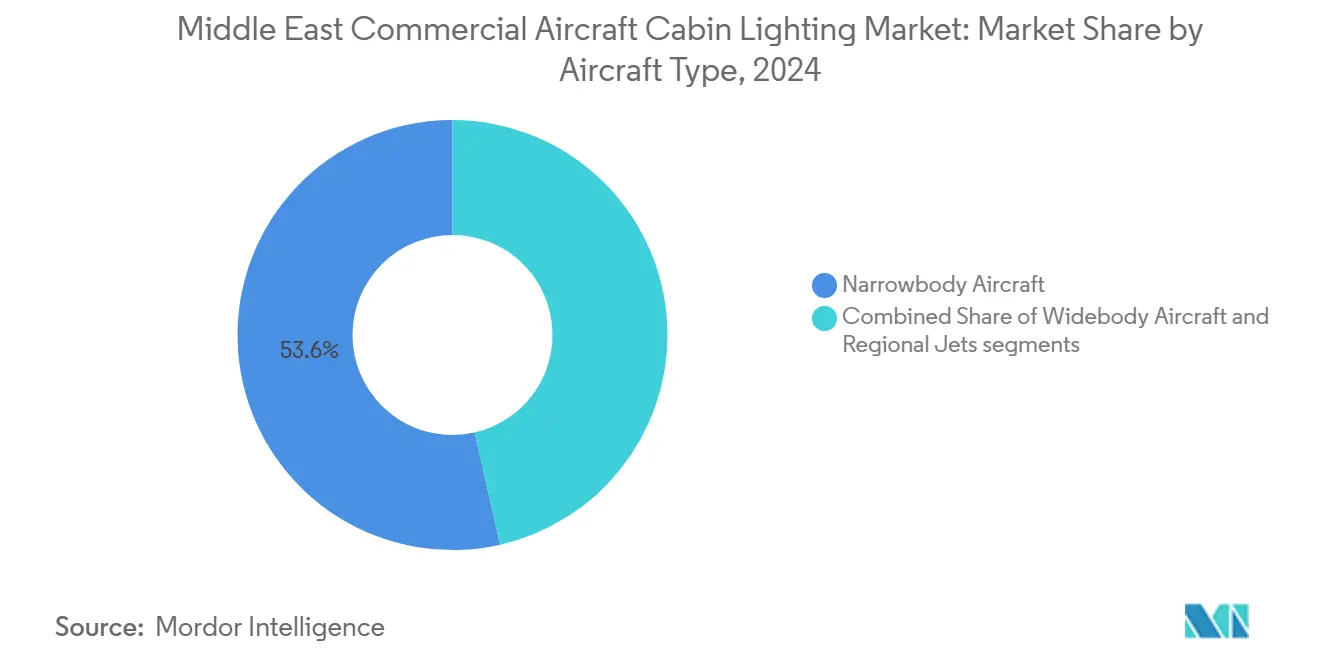

- By aircraft type, narrowbody aircraft captured 53.56% of the Middle East commercial aircraft cabin lighting market share in 2024. They also registered the highest 7.87% CAGR through 2030, reflecting low-cost carrier expansion and regional connectivity strategies.

- By light type, ceiling and wall lights held a 37.34% share of the Middle East commercial aircraft cabin lighting market in 2024; reading lights led growth at a 5.12% CAGR to 2030, driven by passenger demand for personalized illumination.

- By cabin class, economy class generated 57.86% revenue in 2024, whereas premium economy seats are forecasted to climb at a 6.25% CAGR owing to Emirates’ large-scale retrofits.

- By end user, OEM linefit installations accounted for 61.12% of the Middle East commercial aircraft cabin lighting market size in 2024; aftermarket demand, however, accelerates at 5.34% CAGR as airlines expedite cabin modernizations.

- By geography, Saudi Arabia led with a 48.59% revenue share in 2024, while the UAE is the fastest-growing geography at 7.75% CAGR through 2030, propelled by Emirates’ USD 5 billion retrofit program.

Middle East Commercial Aircraft Cabin Lighting Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising narrowbody fleet expansion by regional LCCs | +1.8% | Saudi Arabia and the UAE core spill over to Qatar | Medium term (2-4 years) |

| Increasing retrofit demand from Gulf-based cabin-upgrade programs | +1.2% | UAE and Saudi Arabia, with Qatar secondary | Short term (≤ 2 years) |

| Passenger preference for mood-lighting-enabled ambience | +0.9% | Global, premium focus in Gulf states | Long term (≥ 4 years) |

| Deliveries linked to mega events (e.g., Expo 2030, Asian Games) | +0.7% | Saudi Arabia primary, UAE secondary | Short term (≤ 2 years) |

| Saudi Vision 2030 regional-airport network boosting LED demand | +0.6% | Saudi Arabia national, early gains in Riyadh and Jeddah | Medium term (2-4 years) |

| Localization incentives for in-kingdom production of lighting sub-assemblies | +0.4% | Saudi Arabia national, potential UAE adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Narrowbody Fleet Expansion by Regional LCCs

Low-cost carriers (LCCs) fundamentally reshape demand as flynas orders 160 Airbus jets and flydubai operates 80 B737s fitted with Sky Interior systems that minimize jetlag.[1]Civil Aviation and Airports Authority Somaliland, “Fly Dubai,” caaasl.govsomaliland.org High daily utilization pushes replacement cycles, stimulating aftermarket volumes for the Middle East commercial aircraft cabin lighting market. Airlines favor plug-and-play LED packages such as liTeMood that cut power consumption by 55% and can be installed in 6 hours, aligning with turnaround imperatives.[2]STG Aerospace, “liTeMood,” stgaerospace.com Narrowbody aircraft underpin 45% of Saudi seat capacity, reinforcing demand for standardized lighting optimized for short-to-medium haul sectors. Certification via GCAA and GACA pathways ensures upgrade compatibility across mixed fleets, cementing narrowbody dominance within the Middle East commercial aircraft cabin lighting market.

Increasing Retrofit Demand From Gulf-based Cabin-upgrade Programs

Emirates’ 191-aircraft retrofit is the largest in commercial history, creating concentrated procurement windows for lighting suppliers able to support 16-day turnaround targets.[3]Emirates, “Emirates Undertakes Largest Known Fleet Retrofit Project,” emirates.com Saudia’s parallel program, spanning A330s and B777s, and 39 forthcoming B787s, extends the retrofit surge through 2027.[4]Staff Report, “Saudia Announces Seating Agreement With Collins Aerospace and A330/777 Retrofit Program,” pax-intl.com Integrated mood-lighting solutions complement seat upgrades and brand refreshes, while Saudia Technic’s in-house repair capability opens doors for local suppliers. With Qatar Airways eyeing new first-class products, the momentum for retrofitting propels aftermarket revenues across the Middle East commercial aircraft cabin lighting market.

Passenger Preference for Mood-lighting-enabled Ambience

Human-centric lighting has become a competitive differentiator, illustrated by Riyadh Air’s curated schemes that shift to support travelers’ circadian rhythms. Advanced LEDs offering 16.7 million colors let carriers align lighting with cultural themes, lavender, mocha gold, and indigo, bolstering brand identity. Technologies such as Jetlite’s chronobiological modules provide blue “vitalize” and red “relax” modes, enhancing wellness on long-haul sectors. Integration with seat controls and IFE platforms deepens personalization, raising customer-satisfaction metrics that feed loyalty programs. As Gulf airlines race to elevate passenger experience, mood lighting is central to the Middle East commercial aircraft cabin lighting market.

Deliveries Linked to Mega Events (Expo 2030, Asian Games)

Saudi Arabia’s Expo 2030 and FIFA World Cup 2034 create compressed delivery timetables for ~475 ordered aircraft, accelerating lighting specification cycles. Riyadh Air’s 2025 launch showcases lighting as a national technology statement, while airport expansions such as King Salman International integrate ground-to-air ambience continuity. OEM-ready, certified lighting products gain an advantage amid tight timelines, reinforcing incumbent positions in the Middle East commercial aircraft cabin lighting market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor and LED-driver shortages inflating lead times | –1.4% | Global, acute in Middle East supply chains | Short term (≤ 2 years) |

| High DO-160/CS-ETSO certification costs | –0.8% | Regional, affects local suppliers and retrofits | Medium term (2-4 years) |

| Limited MRO capability for smart-lighting systems | –0.6% | Middle East regional, secondary airports | Medium term (2-4 years) |

| Emerging OLED-panel concepts cannibalizing LED strip demand post-2028 | –0.4% | Global, early adoption in Gulf premium cabins | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor and LED-driver Shortages Inflating Lead Times

Global chip scarcity has stretched component lead times from 120 to 400 days, delaying new deliveries and retrofit schedules. Middle Eastern carriers lack proximate electronics hubs, forcing larger buffer stocks and raising working-capital needs. OEM prioritization of linefit programs over aftermarket orders intensifies retrofit delays across the Middle East commercial aircraft cabin lighting market. Localization initiatives aim to mitigate exposure, yet meaningful semiconductor capacity remains several years out.

High DO-160/CS-ETSO Certification Costs

Certification can exceed USD 500,000 per variant, which is a barrier for new entrants and innovative concepts. The 12–18-month approval window clashes with airlines’ rapid-retrofit timetables, sustaining dependence on pre-certified catalogs from established suppliers. Although GCAA and GACA recognize FAA/EASA approvals, regional manufacturers still carry the financial burden, constraining diversification within the Middle East commercial aircraft cabin lighting market.

Segment Analysis

By Aircraft Type: Narrowbody Fleet Cement Dual Leadership

Narrowbody jets claimed 53.56% revenue in 2024 and led the Middle East commercial aircraft cabin lighting market size expansion with a 7.87% CAGR to 2030. Cost-effective point-to-point networks and LCC growth underpin enduring demand for standardized LED packages that enable rapid installations across B737 and A320 families. Widebodies still dominate premium long-haul missions; Emirates’ A380 and B777 retrofits showcase ultra-long-haul mood lighting that promotes circadian alignment. Regional jets serve underserved secondary cities, utilizing lightweight fixtures that minimize power consumption.

The narrowbody edge stems from scale economies: plug-and-play kits, such as liTeMood, slash installation time to 6 hours, minimizing ground time and aligning with the high utilization typical of Gulf carriers. Boeing Sky Interior and Airbus Airspace cabins pre-wire ambient-lighting controls, giving OEM solutions technological headroom. Fleet harmonization through GCAA/GACA approval pathways further solidifies the prominence of narrowbody aircraft in the Middle East commercial aircraft cabin lighting market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Light Type: Ceiling Dominance Alongside Reading-light Innovation

Ceiling and wall fixtures held a 37.34% share in 2024, reflecting their significant role in defining the brand's ambiance across cabin zones. Reading lights record the fastest 5.12% CAGR, courtesy of passenger desire for individualized spaces and STG Aerospace’s new optics that cut cross-seat glare by 80%.

Floor-path photoluminescent strips gain traction for weight-saving and maintenance-free advantages, while lavatory and signage lighting enjoy steady replacement cycles due to safety mandates. Integrated fiber-optic systems from SCHOTT consolidate multiple zones under a single LED, reducing weight and wiring complexity. The trend toward tunable-white and circadian features reinforces ceiling domination while elevating reading-light sophistication within the Middle East commercial aircraft cabin lighting market.

By Cabin Class: Economy Scale Meets Premium Innovation

Economy cabins generated 57.86% of 2024 revenues, anchoring the Middle East commercial aircraft cabin lighting market through sheer seat volumes. Premium economy, however, is the expansion hotspot, with a 6.25% CAGR on Emirates’ eight 104-seat rollout, which blends ambient LEDs with soft-gold tones.

Business-class suites integrate scenario-based lighting with privacy doors, while first-class innovations from Qatar Airways merge OLED panels with AI-driven controls. Class-specific color palettes foster brand identity: Riyadh Air deploys lavender in economy class and mocha gold in premium cabins, demonstrating the role of lighting in its segmentation strategy. Suppliers must balance scale efficiencies with customization flexibility across the Middle East commercial aircraft cabin lighting market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: OEM Leadership with Aftermarket Acceleration

OEM linefit solutions accounted for 61.12% of 2024 revenue, benefiting from warranty packages and seamless integration with avionics. Collins Aerospace’s half-century distribution alliance with Satair secures continued reach into Airbus and Boeing programs.

Aftermarket demand grows at a 5.34% CAGR as airlines extend fleet life amid delivery delays; Emirates’ 191-aircraft retrofit typifies high-volume opportunities for quick-install, pre-certified kits. Regional MRO expansion, Saudia Technic’s mega village, and Lufthansa Technik tie-ups enhance local support networks, reducing lead times and cost burdens across the Middle East commercial aircraft cabin lighting market.

Geography Analysis

Saudi Arabia led with a 48.59% share in 2024, reflecting Vision 2030’s aviation blueprint and ~475 aircraft to meet the 150 million visitor goals. Retrofit projects spanning Saudia’s A330s and B777s, as well as 39 B787 deliveries, generate sustained lighting demand. Asheil Lighting’s upcoming LED plant at Shaqraa illustrates localization that will underpin future aftermarket growth. Regulatory reforms granting FAA/EASA reciprocity streamline certification for global suppliers, ensuring Saudi leadership in the Middle East commercial aircraft cabin lighting market.

The UAE is the fastest-growing geography, with a 7.75% CAGR, driven by the Emirates’ USD 5 billion retrofit campaign and Dubai’s role as a global hub. Dubai Airports’ replacement of 330,000 lighting units underscores national ambitions to showcase energy efficiency. The GCAA’s local manufacturing approvals pave the way for assembly lines that could serve new deliveries and retrofits across the Middle East commercial aircraft cabin lighting market.

The Rest of the Middle East markets, including Qatar and Oman, offer niche growth opportunities. Qatar Airways’ adoption of Panasonic’s Converix AI platform will embed smart-lighting subsystems on forthcoming B777-9s, setting technological benchmarks for neighboring carriers. Spillover demand from mega events and hub expansions ensures that secondary markets remain integral to regional supply-chain ecosystems, anchoring the Middle East commercial aircraft cabin lighting market.

Competitive Landscape

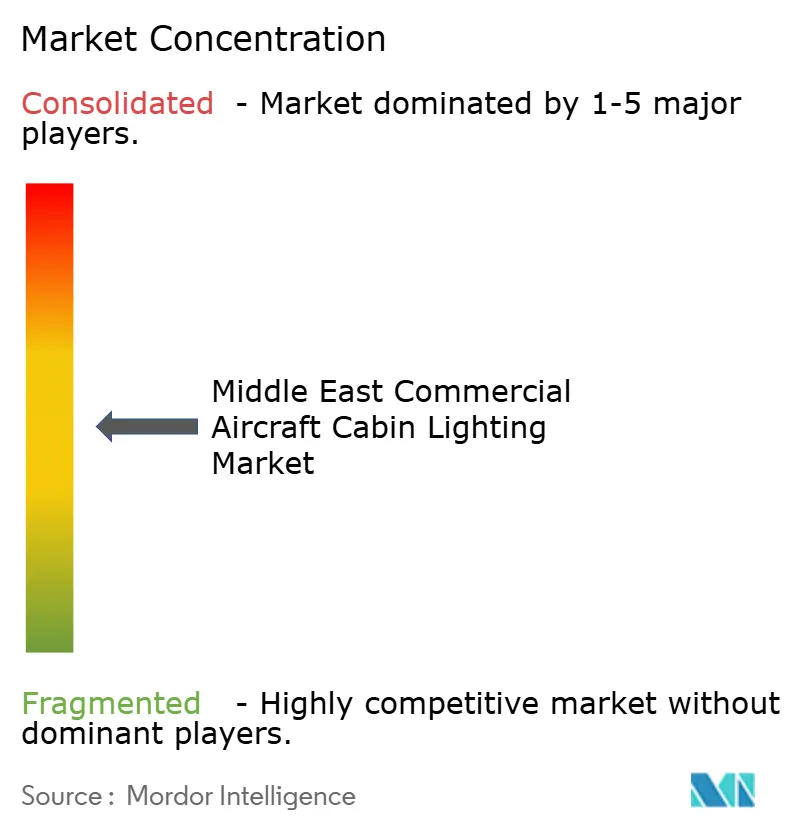

Market concentration is moderate; established OEMs, such as Collins Aerospace, Astronics, Safran, and Diehl Aviation, defend their share through integrated cabin portfolios and long-term airline agreements. The 4-year extension of Collins’ 50-year Satair distribution pact maintains its reach across Airbus and Boeing platforms.

Disruptive forces center on rapid-retrofit LED kits. STG Aerospace’s liTeMood completes A320 installations in six hours and supports wireless scene updates, providing airlines with flexibility without requiring recertification. OLED-based ambient displays herald another evolution; Panasonic’s adoption of Astrova by Riyadh Air may cannibalize legacy strip-lighting revenues over time.

Localization programs in Saudi Arabia and the UAE incentivize joint ventures, presenting market-entry channels for niche suppliers willing to transfer technology. However, certification hurdles and capital intensity shield incumbents, reinforcing moderate concentration across the Middle East commercial aircraft cabin lighting market.

Middle East Commercial Aircraft Cabin Lighting Industry Leaders

Astronics Corporation

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Safran SA

Luminator Holding LP

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components. This renewed contract also encompasses lighting solutions.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin illumination technologies at the AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to significantly enhance the passenger experience.

- June 2023: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

Middle East Commercial Aircraft Cabin Lighting Market Report Scope

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Light Type

| Reading Lights |

| Ceiling and Wall Lights |

| Signage Lights |

| Lavatory Lights |

| Floor-path Lighting Strips |

By Cabin Class

| First Class |

| Business Class |

| Economy Class |

| Premium Economy Class |

By End User

| OEM Linefit |

| Aftermarket/Retrofit |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Light Type | Reading Lights |

| Ceiling and Wall Lights | |

| Signage Lights | |

| Lavatory Lights | |

| Floor-path Lighting Strips | |

| By Cabin Class | First Class |

| Business Class | |

| Economy Class | |

| Premium Economy Class | |

| By End User | OEM Linefit |

| Aftermarket/Retrofit | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Need A Different Region or Segment?

Customize Now

Market Definition

- Product Type - The interior lights of aircraft which provide illumination for instruments, cabins, and other sections that are occupied by passengers are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF