Middle East And North Africa Oilfield Services Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Growth Rate | 4.00% CAGR |

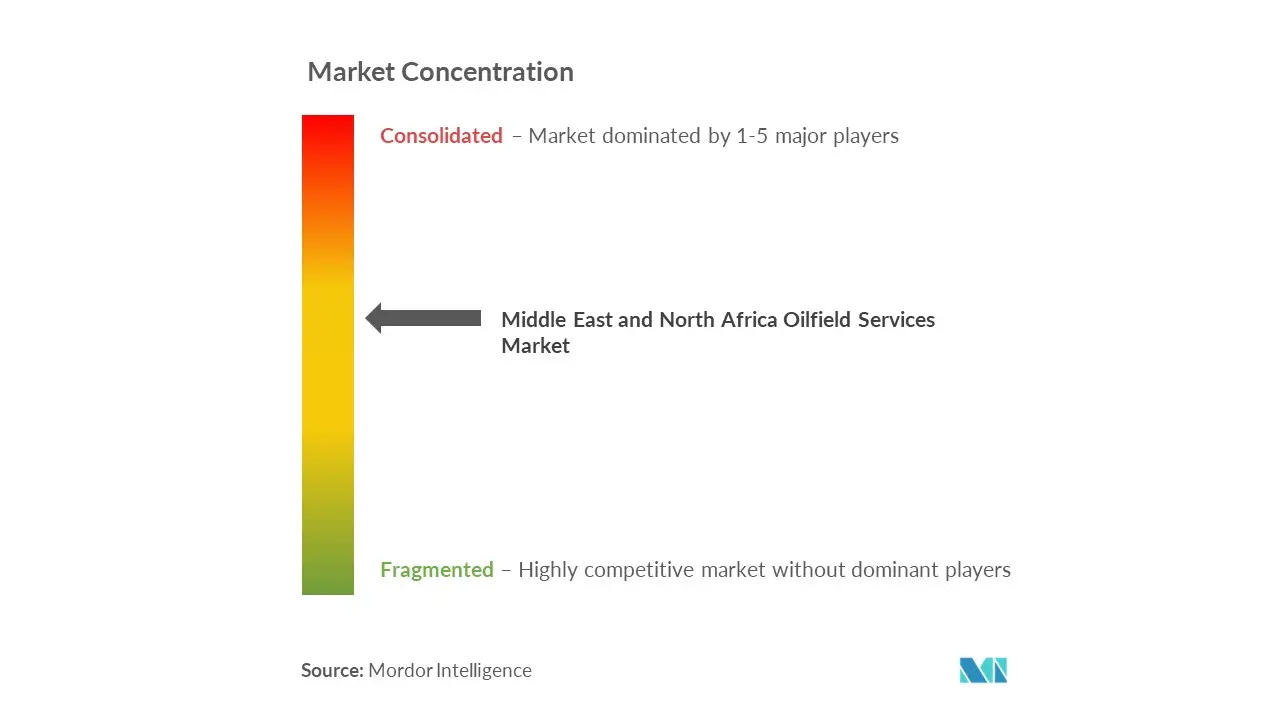

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And North Africa Oilfield Services Market Analysis by Mordor Intelligence

The Middle East And North Africa Oilfield Services Market is expected to register a CAGR of greater than 4% during the forecast period.

The Middle East and North Africa oilfield services sector is experiencing significant transformation driven by increased upstream activities and technological advancement. In March 2024, Abu Dhabi National Oil Company (ADNOC) awarded substantial contracts worth USD 946 million for the long-term development of its Umm Shaif offshore services oilfield, demonstrating the region's commitment to expanding production capabilities. The sector has witnessed a notable uptick in drilling services activities, with the regional rig count reaching 293 active rigs in 2023, reflecting the robust recovery and expansion of exploration and production activities across the region.

The industry is witnessing a dramatic shift toward digitalization and advanced technologies in oilfield services. Major service providers are introducing innovative solutions such as high-definition NMR logging-while-drilling services and advanced automation systems. For instance, in 2023, Schlumberger introduced the MagniSphere service, delivering real-time producibility analysis for optimum well placement, showcasing the industry's evolution toward more efficient and precise operations. These technological advancements are fundamentally transforming traditional oil production services, enabling operators to maximize reservoir exposure and optimize production while reducing operational risks.

The offshore services segment is emerging as a crucial growth driver, particularly in the Mediterranean and Red Sea regions. Recent discoveries in Egypt's offshore regions have sparked increased exploration activities, with the country awarding eight oil blocks in 2023 to major international players including Eni SpA and BP PLC. The Egyptian government's ambitious target to export 7.5 million metric tons per year of gas and LNG by 2024 has catalyzed increased drilling services activities and exploration agreements, driving demand for specialized offshore oil and gas services.

The market is witnessing substantial investments in capacity expansion and infrastructure development. In Saudi Arabia, Saudi Aramco has announced plans to increase its investment by approximately 50% in 2024, targeting investments between USD 40-50 billion to enhance production capacity. This investment surge aligns with the country's objective to increase crude oil production capacity to 13 million barrels per day by 2027. The United Arab Emirates has similarly demonstrated its commitment to sector growth through ADNOC's USD 150 billion five-year capital expenditure plan, focusing on expanding both upstream and downstream capabilities.

Middle East And North Africa Oilfield Services Market Trends and Insights

Rising Drilling Activities and Infrastructure Investments

The Middle East and North Africa region has emerged as a global hotspot for drilling services, with substantial investments flowing into oilfield services infrastructure. According to the International Rig Count data from September 2022, the region deployed 342 rigs, representing an impressive 38.9% of global rig deployments, highlighting the region's significance in global drilling operations. This extensive drilling infrastructure is supported by major investment initiatives from national oil companies, exemplified by ADNOC's comprehensive growth strategy that includes a $127 billion investment plan for 2022-2026, focusing on expanding production capabilities and modernizing drilling operations.

The investment momentum is further reinforced by strategic partnerships between national oil companies and oilfield service providers. For instance, in August 2022, ADNOC established five crucial framework agreements with major service providers including Schlumberger, Halliburton, and Weatherford, specifically targeting directional drilling and logging while drilling (LWD) services for both onshore and offshore assets. These five-year agreements, with potential two-year extensions, demonstrate the long-term commitment to maintaining and expanding drilling infrastructure in the region, thereby driving sustained demand for oil drilling equipment and drilling services.

Cost-Effective Production and Capacity Expansion Plans

The MENA region's oilfield services market is significantly driven by the exceptional cost-effectiveness of production operations, particularly in key markets like Saudi Arabia. The region maintains one of the world's lowest drilling and production cost structures, with Saudi Aramco reporting an average upstream lifting cost of just $3 per barrel, making it highly economical to expand operations and develop new fields. This cost advantage has enabled major operators to pursue aggressive capacity expansion plans, as evidenced by Saudi Aramco's announcement to increase its capital expenditure to $40-50 billion in 2022, representing a 50% increase from the previous year.

The favorable cost economics have encouraged ambitious production capacity enhancement targets across the region. Saudi Aramco's strategic plan to boost crude production capacity to 13 million barrels per day by 2027, coupled with its goal to increase gas production by 50% by 2030, exemplifies the scale of expansion activities. These extensive capacity enhancement initiatives necessitate comprehensive oilfield services support, from drilling and well completion services to maintenance and optimization services, creating a robust demand environment for service providers across the value chain.

Development of New Fields and Technological Advancement

The discovery and development of new fields, particularly unconventional resources, is emerging as a crucial driver for the oilfield services market in the MENA region. The development of Saudi Arabia's Jafurah Shale play, the country's largest unconventional gas field with an estimated 200 trillion cubic feet of gas reserves, represents a significant opportunity for specialized oilfield services. These unconventional developments require advanced drilling techniques, specialized well intervention services, and innovative production optimization solutions, driving demand for cutting-edge oilfield services and technologies.

The market is further propelled by the accelerated development of offshore fields, particularly in the UAE's waters. ADNOC's fast-tracking of major offshore field developments has created substantial demand for specialized offshore drilling and completion services. This trend is supported by the implementation of advanced technologies and innovative drilling solutions, as evidenced by the recent framework agreements for directional drilling and logging while drilling services. The focus on offshore development, combined with the push for unconventional resources, is creating diverse service requirements and driving technological advancement in the oilfield services sector, including the need for wireline services and hydraulic fracturing services.

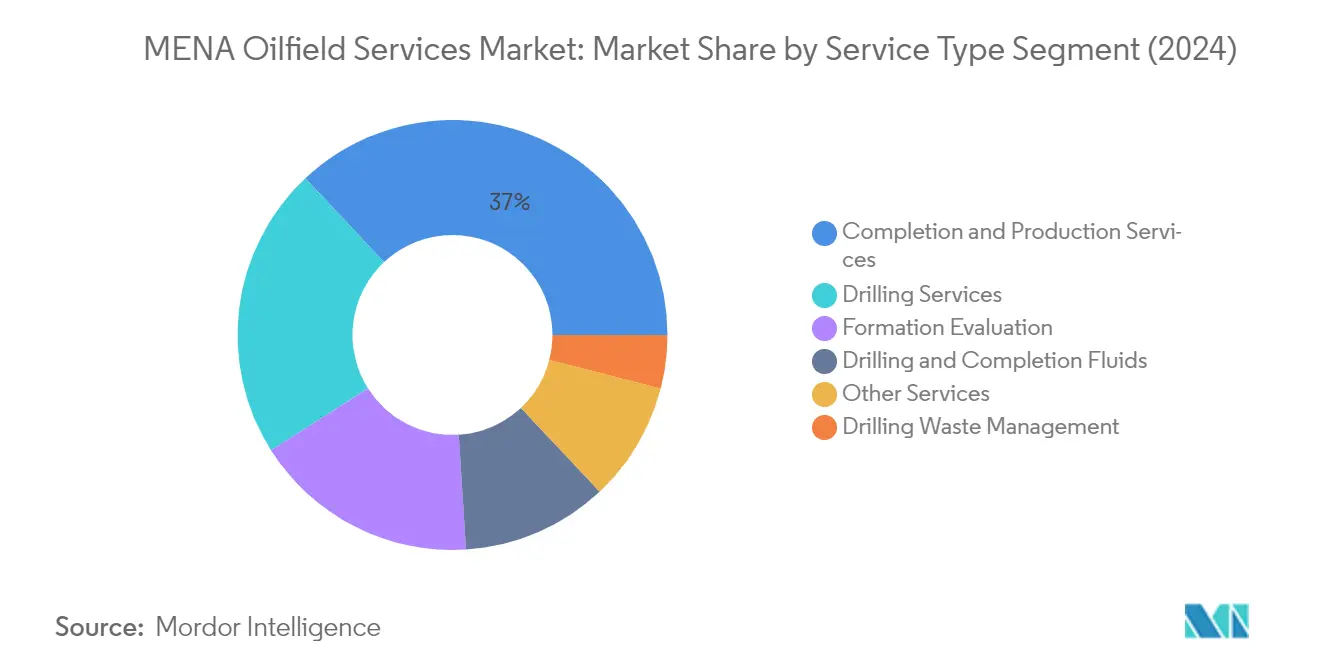

Segment Analysis: Service Type

Completion and Production Services Segment in MENA Oilfield Services Market

The Completion and Production Services segment dominates the Middle East and North Africa (MENA) oilfield services market, holding approximately 37% market share in 2024. This segment's prominence is driven by increasing investments in well completion services across major oil-producing nations like Saudi Arabia, UAE, and Kuwait. The segment encompasses various critical services, including multistage completions, intelligent completions, well intervention services, and artificial lift systems. Major developments supporting this segment include ADNOC's USD 946 million offshore contract for the Umm Shaif oilfield development and Saudi Aramco's significant investments in completion technologies for the Jafurah unconventional gas project.

Completion and Production Services Segment Growth in MENA Oilfield Services Market

The Completion and Production Services segment is experiencing the fastest growth in the MENA oilfield services market for the period 2024-2029. This growth is primarily driven by the increasing complexity of well completion services in both conventional and unconventional reservoirs across the region. The segment's expansion is supported by technological advancements in smart completion systems, enhanced production techniques, and the rising demand for well intervention services. Recent developments, such as Kuwait's agreement with Saudi Arabia to develop the Durra offshore gas field and Egypt's ambitious plans to boost gas production, are further accelerating the segment's growth trajectory.

Remaining Segments in Service Type

The other significant segments in the MENA oilfield services market include drilling services, formation evaluation, drilling and completion fluids, drilling waste management services, and other services. Drilling services remain crucial for exploration and development activities, while formation evaluation services provide essential data for reservoir characterization and well planning. The drilling and completion fluids segment plays a vital role in maintaining wellbore stability and optimizing drilling operations. The drilling waste management services segment is gaining importance due to increasing environmental regulations, while other services encompass specialized offerings such as rope access services and equipment maintenance.

Segment Analysis: Location

Onshore Segment in MENA Oilfield Services Market

The onshore segment continues to dominate the Middle East and North Africa oilfield services market, commanding approximately 89% of the total market share in 2024. This dominance is primarily attributed to the extensive onshore oil and gas fields across the region, particularly in countries like Saudi Arabia, Kuwait, and Iraq. The segment's strength is reinforced by lower operational costs compared to offshore operations, easier accessibility, and the presence of major conventional oil reserves in onshore locations. The segment is particularly driven by significant investments in conventional onshore and shale oil and gas development, with countries like the United Arab Emirates discovering substantial onshore unconventional oil resources and Saudi Arabia expanding its onshore drilling activities to maintain its production capacity.

Offshore Segment in MENA Oilfield Services Market

The offshore segment is emerging as the fastest-growing segment in the MENA oilfield services market for the period 2024-2029. This growth is being fueled by significant offshore discoveries, particularly in the Mediterranean region near Egypt, and increased investment in offshore exploration activities. The segment is witnessing substantial momentum with new projects being initiated across the region, including Abu Dhabi's offshore gas field developments and Qatar's North Field expansion project. The growth is further supported by technological advancements in offshore drilling capabilities and the region's strategic focus on developing its offshore resources to maintain its position as a global energy hub.

Middle East And North Africa Oilfield Services Market Geography Segment Analysis

Middle East and North Africa Oilfield Services Market in the Middle East

The Middle East region represents a crucial market for oilfield services, characterized by extensive oil and gas reserves and ongoing development projects. The region encompasses major oil-producing nations, including Saudi Arabia, Qatar, Kuwait, Iraq, and the United Arab Emirates, each contributing significantly to the global energy landscape. These countries are actively investing in both conventional and unconventional resource development, with a particular focus on enhancing recovery from mature fields while simultaneously exploring new reserves. The region's oilfield services market is driven by national oil companies' ambitious production targets and their commitment to maintaining a global market position through technological advancement and operational efficiency improvements.

Middle East and North Africa Oilfield Services Market in Saudi Arabia

Saudi Arabia maintains its position as the dominant force in the Middle East oilfield services market, holding approximately 13% market share in 2024. The kingdom's market leadership is underpinned by its massive conventional oil reserves and continuous investment in field development projects. Saudi Aramco, the state oil company, continues to drive market growth through its comprehensive drilling programs and enhanced oil recovery initiatives. The country's oilfield services sector benefits from ongoing developments in both onshore and offshore fields, with particular emphasis on the Ghawar field, the world's largest conventional onshore oil field. Saudi Arabia's market position is further strengthened by its investment in unconventional resources and commitment to maintaining its production capacity.

Middle East and North Africa Oilfield Services Market Growth Outlook - Saudi Arabia

Saudi Arabia is projected to maintain the highest growth rate in the Middle East region, with an expected growth rate of approximately 6% from 2024 to 2029. This growth trajectory is supported by the kingdom's ambitious plans to expand its production capacity and develop its unconventional resources. The country's growth is driven by major expansion projects across its oilfield portfolio, including developments in the Marjan and Berri fields. Saudi Arabia's commitment to technological advancement in oilfield services, particularly in areas such as drilling efficiency and enhanced oil recovery techniques, continues to attract significant investments. The kingdom's focus on maintaining its position as a global energy leader while incorporating sustainable practices and new technologies supports this robust growth outlook.

Middle East and North Africa Oilfield Services Market in North Africa

The North African region represents a significant market for energy services, with Algeria, Egypt, and Libya as key players in the sector. Each country brings unique opportunities and challenges to the market, with varying degrees of political stability and resource accessibility influencing market dynamics. The region's oil exploration services sector is characterized by a mix of mature fields requiring enhanced recovery techniques and new exploration opportunities, particularly in offshore areas.

Middle East and North Africa Oilfield Services Market in Algeria

Algeria stands as the largest petroleum services market in North Africa, with its extensive hydrocarbon reserves and established oil and gas infrastructure. The country's position is supported by its significant conventional resources and growing focus on unconventional potential. Algeria's national oil company, Sonatrach, continues to drive market growth through its comprehensive development programs and partnerships with international service providers. The country's market leadership is reinforced by its strategic location and well-developed export infrastructure.

Middle East and North Africa Oilfield Services Market Growth Outlook - Algeria

Algeria demonstrates the strongest growth potential in the North African region, supported by its ambitious plans to enhance hydrocarbon production and develop new resources. The country's growth trajectory is driven by ongoing investments in both onshore services and subsea services projects, with particular emphasis on enhancing recovery from mature fields while exploring new opportunities. Algeria's commitment to modernizing its oilfield infrastructure and adopting new technologies positions it favorably for sustained growth. The country's favorable investment climate and strategic focus on energy sector development continue to attract both national and international investments in energy services.

Competitive Landscape

Top Companies in Middle East and North Africa Oilfield Services Market

The market features prominent global players like Schlumberger, Baker Hughes, Halliburton, Weatherford International, and Transocean leading the competitive landscape. These companies are heavily investing in digital transformation and oilfield services automation technologies, with initiatives ranging from integrated drilling solutions to artificial intelligence-powered decision support systems. The industry is witnessing a strong push towards sustainable practices, particularly in water management and emissions reduction, exemplified by innovations like seawater fracking technology. Companies are increasingly focusing on forming strategic partnerships and joint ventures with local players to strengthen their regional presence and meet localization requirements. There is also a notable trend towards offering integrated service packages that combine multiple capabilities, from drilling and evaluation to completion and production oil well services, allowing providers to capture more value across the operational chain.

Consolidated Market with Strong Regional Partnerships

The oilfield services market in MENA exhibits a moderately consolidated structure, dominated by international service providers who have established strong local partnerships and joint ventures with national oil companies. These global players leverage their technological expertise and comprehensive service portfolios while working alongside domestic companies like Arabian Drilling Company, APC Oilfield Services, and Middle East Oilfield Services, who bring crucial local market knowledge and established relationships with regional stakeholders. The market has witnessed significant consolidation through strategic mergers and acquisitions, aimed at expanding service capabilities and geographical reach.

The competitive dynamics are shaped by the strong presence of national oil companies and their increasing focus on domestic capacity building. Major players are establishing regional headquarters and training centers, particularly in hubs like Dubai and Abu Dhabi, to strengthen their local presence and meet increasing localization requirements. The market also sees active participation from Chinese service providers who are gradually expanding their footprint through competitive pricing and technology offerings, adding another layer of competition to the established players.

Innovation and Local Integration Drive Success

Success in the MENA oilfield services market increasingly depends on companies' ability to combine technological innovation with strong local integration. Service providers must develop comprehensive digital solutions while maintaining strong relationships with national oil companies and adhering to local content requirements. The ability to offer integrated service packages, optimize operational costs through automation and digital technologies, and demonstrate environmental stewardship through sustainable practices has become crucial for maintaining market position.

Future market share gains will largely depend on companies' ability to navigate the region's complex regulatory environment while delivering cost-effective solutions that address the specific challenges of MENA's mature fields and unconventional resources. Service providers must balance investment in new technologies with price competitiveness, particularly as national oil companies become more sophisticated in their procurement strategies. The relatively low threat of substitutes is counterbalanced by high buyer concentration and increasing pressure for localization, making it essential for companies to develop strong local capabilities while maintaining technological leadership. In this context, the role of energy services and oil equipment services becomes increasingly significant as they provide the necessary support for operational excellence.

Middle East And North Africa Oilfield Services Industry Leaders

Schlumberger Limited

Weatherford International PLC

Baker Hughes Company

Halliburton Company

Transocean Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- In August 2022, ADNOC Offshore awarded a 5-year contract totaling USD 1.7 billion to ADNOC Logistics & Services (ADNOC L&S) for the hire of 13 self-propelled jack-up barges, which will be deployed across ADNOC's offshore fields. The barges will be utilized for rigless well intervention and pre- and post-drilling operations, and for topside maintenance and integrity restoration activities.

- In March 2022, Saudi Aramco awarded a major gas well drilling contract to Schlumberger. The integrated project scope consists of several drilling rigs and technologies and services, which includes drill bits, measurement while drilling (MWD) and logging while drilling (LWD), drilling fluids, cementing, and completion. Additionally, Schlumberger is under contract to provide digital solutions to enhance integrated drilling performance, including the DrillOps, an on-target well delivery solution which uses data analysis and machine learning to automate and execute a digital well plan.

Middle East And North Africa Oilfield Services Market Report Scope

Oilfield services are defined as services provided by services associated with the oil and gas exploration and production processes, i.e. the upstream sector of the energy industry. The Middle East and North Africa Oilfield Services Market is segmented by Service Type, Location of Deployment and Geography. By Service Type, the market is segmented into Drilling, Completion, Production and Intervention and Other Services. By Location of Deployment, the market is segmented in Onshore and Offshore. By Geography, the market is segmented into (Saudi Arabia, United Arab Emirates, Iran, Iraq, Egypt, Algeria and Others. For each segment, the market sizing and forecasts have been done based on revenue (USD Million).

Key Questions Answered in the Report

What is the current Middle East And North Africa Oilfield Services Market size?

The Middle East And North Africa Oilfield Services Market is projected to register a CAGR of greater than 4% during the forecast period (2025-2030)

Who are the key players in Middle East And North Africa Oilfield Services Market?

Schlumberger Limited, Weatherford International PLC, Baker Hughes Company, Halliburton Company and Transocean Ltd. are the major companies operating in the Middle East And North Africa Oilfield Services Market.

What years does this Middle East And North Africa Oilfield Services Market cover?

The report covers the Middle East And North Africa Oilfield Services Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Middle East And North Africa Oilfield Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.