Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 275.47 Billion |

| Market Size (2031) | USD 462.41 Billion |

| Growth Rate (2026 - 2031) | 10.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And North Africa Digital Payments Market Analysis by Mordor Intelligence

The Middle East and North Africa digital payments market was valued at USD 248.35 billion in 2025 and estimated to grow from USD 275.47 billion in 2026 to reach USD 462.41 billion by 2031, at a CAGR of 10.92% during the forecast period (2026-2031). Rapid real-time rails, policy-led cashless mandates, and cross-border e-commerce flows are cementing digital channels as the default settlement method across consumer and B2B contexts. Fintech sandboxes in Bahrain, Abu Dhabi, and Saudi Arabia are accelerating wallet and API innovation, while super-app ecosystems in the Gulf are embedding payments inside everyday consumer journeys. Regional processors are pursuing scale through mergers, and global networks are deepening local partnerships to capture rising card-not-present volumes. Heightened fraud risks in Egypt and Morocco are prompting substantial investments in AI-driven risk engines, tightening the link between security posture and customer adoption.

Key Report Takeaways

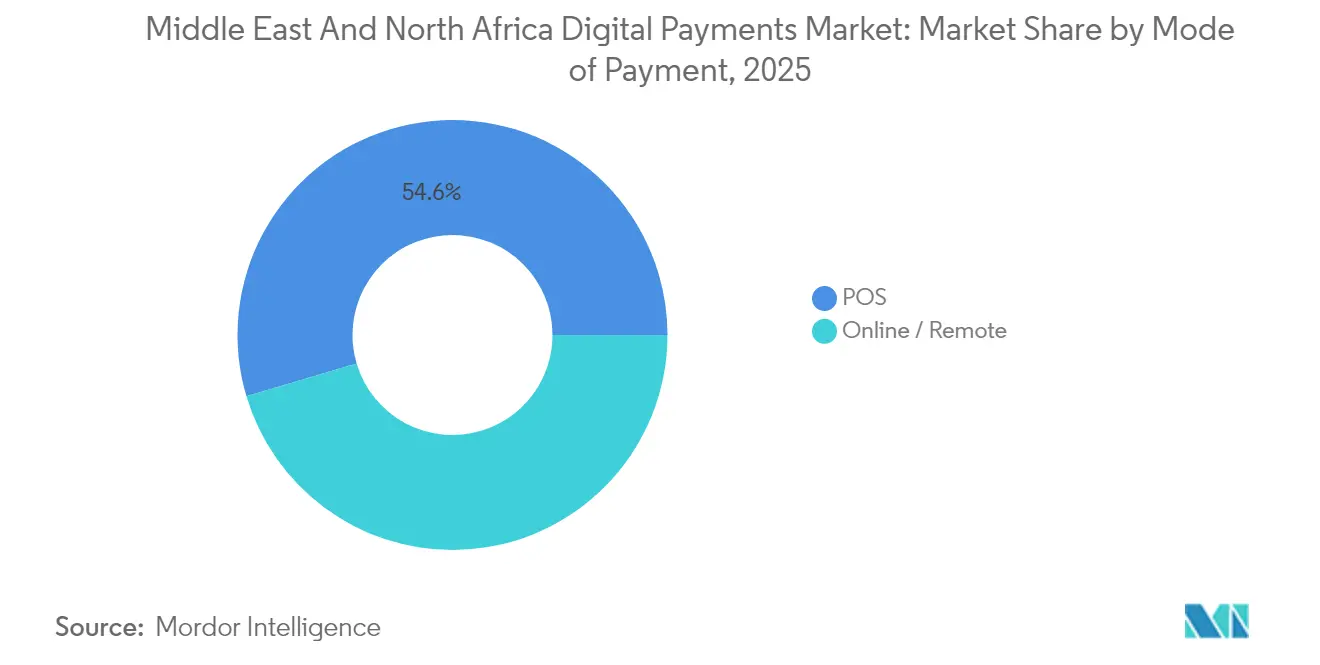

- By mode of payment, the Point-of-Sale segment led with a 54.60% share of the Middle East and North Africa digital payments market in 2025; Online/Remote payments are expected to advance at a 14.45% CAGR through 2031.

- By component, Solutions commanded a 60.85% share of the Middle East and North Africa digital payments market size in 2025, while Services are forecast to expand at an 18.05% CAGR between 2026 and 2031.

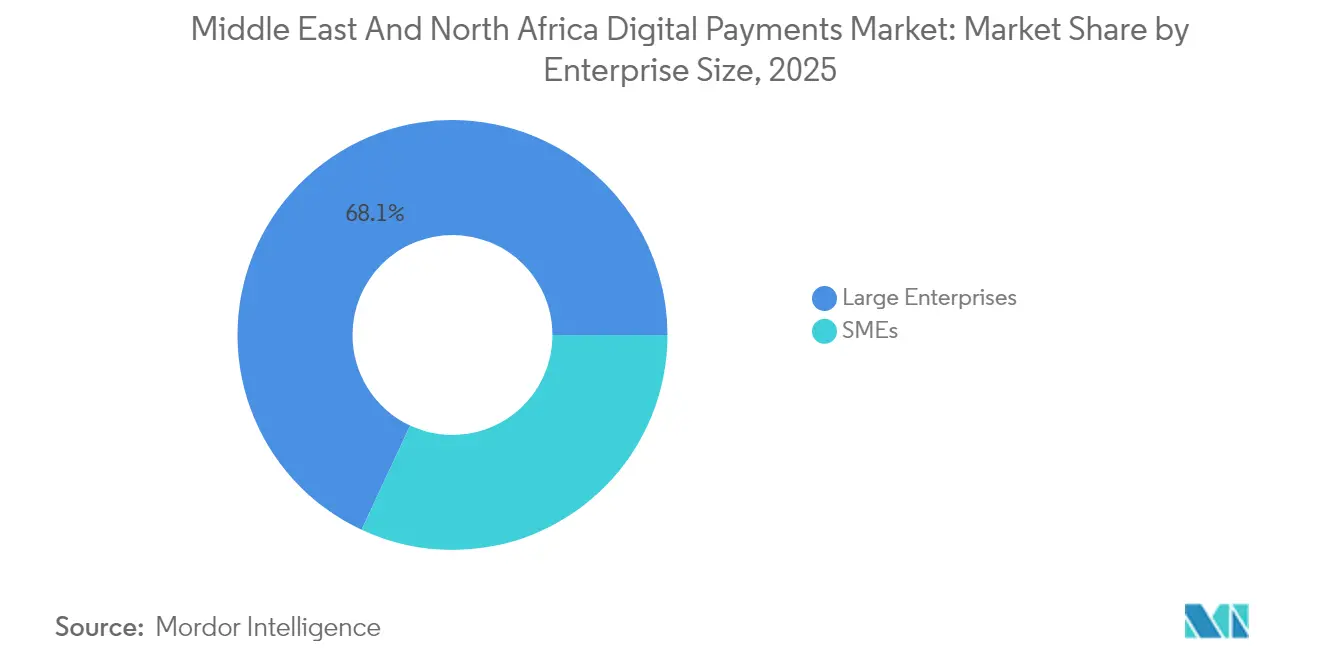

- By enterprise size, large enterprises accounted for 68.05% of the 2025 revenue of the Middle East and North Africa digital payments market, whereas the SME segment is projected to grow at a 21.85% CAGR through 2031.

- By end-user industry, the Retail and E-commerce sector captured 37.95% of the Middle East and North Africa digital payments market revenue in 2025; Other End-user Industries are projected to grow at the fastest rate of 19.15% CAGR.

- By geography, the United Arab Emirates held a 24.05% share of the Middle East and North Africa digital payments market in 2025, and Turkey is set to post a 20.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And North Africa Digital Payments Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Real-time Payment Rails Roll-out across GCC and Egypt | +3.2% | GCC countries and Egypt, with spillover effects to North Africa | Medium term (2-4 years) |

| Government–backed Cashless Society Mandates in Saudi Arabia and UAE | +2.8% | Saudi Arabia and UAE primarily, with influence across GCC | Medium term (2-4 years) |

| Surge in Cross-border E-commerce Imports via Turkey and UAE Free-Zones | +1.9% | UAE, Turkey, with regional impact across MENA | Short term (≤ 2 years) |

| FinTech Sandboxes liberalising Digital Wallet Licensing in Bahrain, Abu Dhabi, and Saudi | +1.4% | Bahrain, UAE (Abu Dhabi), Saudi Arabia | Medium term (2-4 years) |

| High Expat Remittance Volumes converging on Mobile P2P Platforms | +1.2% | UAE, Saudi Arabia, Qatar, Kuwait | Short term (≤ 2 years) |

| Retailer-led Super-App Race accelerating Embedded Payments | +0.9% | UAE, Saudi Arabia, Egypt, Turkey | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Real-time Payment Rails: Transforming Transaction Velocity

Saudi Arabia’s SARIE processed 463 million transfers worth SAR 3.2 trillion in 2024, up 42% year-on-year. The UAE Instant Payment Platform captured 28% of domestic transfers within six months. Instant settlement has shortened working-capital cycles for SMEs, catalysed overlay services such as request-to-pay, and fostered wallet uptake among cash-centric segments. Processors are integrating ISO 20022 messaging to enable richer remittance data, a prerequisite for B2B embedded finance. Banks are recalibrating fee models as intraday liquidity risks decline, while merchants report lower cart abandonment thanks to irrevocable push-payments. The network effects are expected to peak between 2026-2028 as remaining GCC banks finalise full API connectivity.

Government-backed Cashless Mandates: Policy-driven Transformation

Saudi Arabia reached 79% non-cash retail transactions by Q1 2025, surpassing Vision 2030’s interim 70% goal. Dubai recorded 88% cashless usage under its Cashless Strategy. Fiscal authorities are linking VAT rebates and procurement contracts to digital acceptance, turning compliance into a commercial incentive. Central banks are synchronising open-finance and token-service rules to streamline wallet provisioning and ensure data portability. Public-sector payroll disbursements now default to wallets, driving inclusion among migrant workers. With statutory e-invoice mandates due in most GCC markets by 2026, card-present and account-to-account rails will converge around national ID tokenisation, tightening KYC assurance.

Cross-border E-commerce: Reshaping Regional Trade Flows

E-commerce GMV in MENA expanded 30% in 2024, with average order values climbing to USD 35.6. UAE free-zones and Turkish fulfilment hubs channel the bulk of cross-border parcels, placing multi-currency processing and local-method acceptance on the strategic roadmap of PSPs. BNPL penetration is rising fastest in cross-border baskets, lifting approval conversion. Processors are introducing smart routing to mitigate foreign-exchange liquidity constraints, especially in markets with capital-control regimes. Compliance teams are prioritising simplified customs documentation and instant duty calculation inside checkout flows, which further lowers friction for first-time buyers. The accelerated ramp-up is front-loaded into 2025-2026 as global brands localise in Arabic and Turkish.

Fintech Sandboxes: Cultivating Innovation Ecosystems

UAE’s FIT Programme counted 329 active fintechs in 2024, 128.5% more than 2021. Bahrain’s sandbox is piloting blockchain-based remittances that promise sub-USD 1 settlement cost into Africa corridors. Saudi sandbox cohorts have accelerated wallet user growth to 14 million. Sandbox waivers lower capital requirements and streamline proof-of-concepts, encouraging cloud-native micro-service architectures that can be exported across MENA. Early-stage PSPs leverage these programmes to demonstrate regulatory compliance before scaling, compressing go-to-market cycles from 24 months to less than 10. As regulators tighten graduation criteria, market entrants will pivot to specialised use cases such as microlending and supply-chain finance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Interchange / MDR Caps across MENA Jurisdictions | -1.1% | Pan-MENA, particularly affecting cross-border merchants | Medium term (2-4 years) |

| Cyber-fraud escalation in Egypt and Morocco is dampening consumer trust | -0.8% | Egypt, Morocco, with spillover effects to other North African markets | Short term (≤ 2 years) |

| Legacy POS infrastructure outside Tier-1 cities | -0.7% | North Africa, Turkey, Egypt, Jordan | Long term (≥ 4 years) |

| Foreign-currency liquidity pressure on cross-border settlements | -0.5% | Egypt, Turkey, Morocco, Tunisia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Interchange and MDR Caps: Economics Under Pressure

Disparate merchant-discount-rate ceilings complicate cross-border acquiring economics. PSPs operating in both UAE (flexible MDR) and Egypt (tighter caps) struggle to harmonise blended pricing models, leading to margin compression. SMEs delay terminal deployment when economics appear unfavourable, prolonging cash reliance. Regional associations are lobbying for convergence around cost-based interchange, but legislative cycles point to a multi-year resolution. In the interim, acquirers bundle value-added services such as analytics and instant settlement to defend fee revenue. Tokenised account-to-account propositions also emerge as MDR-free alternatives, reshaping gateway strategy.

Cyber-fraud Escalation: Barriers in Emerging Markets

Visa’s 2025 study reveals that 97% of GCC consumers employ at least one security measure online, yet fraud incidents have risen sharply in Egypt and Morocco.[3]Visa, “Consumers Embrace Security Measures as Digital Payments Continue to Grow,” visa.com Phishing and SIM-swap schemes target first-time wallet users, eroding confidence. Banks are embedding AI-based deep authorisation to cut false positives by 20% while catching synthetic identities in near real-time. Mandatory 3-D Secure adoption is expanding to low-value transactions, but poor network latency can increase abandonment. Education campaigns run in Arabic and French aim to rebuild trust, and the PCI Council’s regional office is rolling out compliance clinics for small acquirers. A measurable impact on uptake is expected once fraud-loss ratios fall below the 10-basis-point mark, which is targeted for mid-2026.

Segment Analysis

By Mode of Payment: Online/Remote Segment Disrupting Traditional POS Dominance

The Middle East and North Africa digital payments market recorded 54.60% of its 2025 transaction value at the point of sale; however, online and remote channels grew at a 14.45% CAGR, chipping away at historical dominance. Mobile wallets already account for 18% of in-store spending in the Gulf and are expected to exceed one-third by 2027 as Near-Field Communication (NFC) acceptance becomes ubiquitous. QR-code rails launched by central banks are further collapsing the distinction between “card-present” and “card-not-present,” delivering checkout consistency in both physical stores and social-commerce feeds.

Heightened e-commerce adoption after the 2024 pandemic phase-out created durable behavioral change: 85% of regional consumers tested at least one emerging method, such as tokenized click-to-pay or BNPL checkout. Processors now optimise for gateway orchestration that can auto-failover between local schemes, international networks, and account-to-account options in under 200 milliseconds. As instant rails converge with open-banking APIs, PSPs expect authorisation cost reductions of up to 40 basis points, sustaining the margin economics of remote commerce as volume scales.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Services Growth Outpacing Solutions as Complexity Rises

Solutions gateways, processors, wallets, and fraud engines held 60.85% of the Middle East and North Africa digital payments market size in 2025, reflecting the foundational nature of core infrastructure. Yet Services are projected to climb 18.05% CAGR to 2031, overtaking software revenue in fast-growing sub-markets such as Saudi Arabia. Consultancies are booked nine months in advance for open-API readiness audits, and cloud migration mandates from regulators intensify demand for integration specialists.

Managed fraud monitoring is shifting from licence fees to usage-based models that flex with transaction peaks during Ramadan and Singles’ Day. Banks outsource white-label wallets to platform providers, preferring SLA-backed uptime guarantees over in-house builds. Regulatory support functions, including reporting, dispute management, and consumer-protection dashboards, round out service bundles, pushing the average contract value 1.7 times higher than its 2023 equivalents. Consequently, hybrid vendors that pair modular SaaS with advisory retainment enjoy double-digit expansion in bookings through 2028.

By Enterprise Size: SMEs Driving Unprecedented Growth through Digital Adoption

Large enterprises still generated 68.05% of transaction flows in 2025, leveraging omnichannel orchestration and direct scheme memberships to squeeze processing costs. Nevertheless, the SME cohort is on a 21.85% CAGR run rate, the fastest across the Middle East and North Africa digital payments market. Wallet-based soft-POS products such as Geidea’s smartphone app eliminate hardware outlays, unlocking acceptance for micro-retailers. In the Gulf, government procurement portals now mandate digital invoicing, nudging SME suppliers into formal payment rails.

Mastercard’s SME Confidence Index shows that 72% of surveyed firms expect equal or higher revenue in 2025, prompting investment in global storefronts and the localization of checkout flows. Cross-border enablement is top priority: 79% of SMEs plan to sell internationally, relying on multi-currency settlement, real-time FX quotes, and built-in duty calculation. PSPs court this segment with revenue-based financing and embedded working-capital lines, deepening wallet share beyond payments alone.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-user Industry: Diversification beyond Retail and E-commerce

Retail and E-commerce retained 37.95% of the 2025 value pool, but other industries, government, education, utilities, and gaming are collectively expanding at a 19.15% CAGR, tilting the demand mix. Government agencies in the UAE now issue 100% of resident visa fees through wallets or cards, driving steady baseline volume. Utility providers adopt autopay mandates that cut delinquency by 15 percentage points. The MENA gaming sector, valued at USD 7.45 billion in 2023 and growing at a 9.4% CAGR, integrates frictionless top-ups through carrier billing and tokenised cards, extending the lifetime value of players.

Education institutions pivoted to recurring digital tuition plans during pandemic lockdowns and have retained them for convenience, creating seasonally predictable payment spikes each semester. Healthcare providers' interest in the instant disbursement of insurance reimbursements is another greenfield, positioning PSPs with payout capabilities for outsized growth. Combined, these verticals diversify revenue sources and reduce cyclicality tied to retail sales cycles.

Geography Analysis

The UAE accounted for 24.05% of the Middle East and North Africa digital payments market in 2025, driven by 329 active fintech companies and a supportive Financial Infrastructure Transformation roadmap. Real-time rails, open-finance regulations, and an 88% cashless adoption rate underpin an addressable fintech revenue pool projected to reach USD 3.56 billion by 2025 and USD 6.43 billion by 2030. Cross-border corridors leveraging Dubai ports contribute a disproportionate share of high-value, multi-currency flows, prompting PSPs to embed automated sanctions screening and real-time duty calculation as value-added services.

Turkey is the fastest-growing market, forecast at a 20.75% CAGR through 2031, driven by a youthful, mobile-first consumer base and nascent cryptocurrency regulation, which is expected to exit the FATF grey list. Domestic processors are racing to integrate instant card withdrawal into gaming and influencer-commerce apps, while manufacturers leverage B2B BNPL for export receivables.

Saudi Arabia’s e-payments reached 79% of retail transactions in early 2025, with Vision 2030 milestones driving aggressive wallet issuance and open banking rollouts. Venture funding flows confirm momentum: the Kingdom captured 58% of MENA VC dollars in Q1 2025, with fintechs taking 57% of that haul. Banks pivot to product factories that unbundle issuing, acquiring, and lending via micro-services, aligning with SAMA’s graduated licensing regime.

Egypt offers scale with latent potential; policy frameworks such as the National Payment Council’s financial-inclusion strategy are nudging consumers toward wallets. Fawry’s network processes millions of daily micro-transactions, and new partnerships like dubizzle-Paymob extend acceptance to classifieds marketplaces. Yet cyber-fraud episodes keep trust fragile, triggering coordinated public-private security programmes.

Morocco, the third-largest Arab fintech hub, is building payment corridors into Francophone Africa. Venture-backed PayTic plans to roll out issuer processing across the continent, and regulators are drafting open-API standards. Consumer adoption concentrates in urban Casablanca and Rabat, leaving rural digitisation as the next frontier contingent on mobile-coverage upgrades.

Competitive Landscape

The Middle East and North Africa digital payments market is dominated by prominent players such as Visa, Mastercard, and PayPal, alongside regional players including Network International, Fawry, and STC Pay. Consolidation is evident, as PayU’s 43.5% stake in Mindgate anchors a real-time processing capability that complements its regional acquiring footprint.[1]Prosus, “PayU Joins Mindgate as a Strategic Investor to Accelerate Global Innovation,” prosus.com Global networks invest heavily in tokenisation and AI-based fraud tools to preserve interchange relevance as account-to-account rails mature.

Strategic alliances dominate the expansion strategy. Mastercard paired with Corpay to scale business-to-business cross-border payouts, blending network tokenisation with Corpay’s FX platform.[2]Mastercard, “Mastercard and Corpay Launch Strategic Partnership in Cross-Border Payments,” mastercard.com Visa’s Deep Authorization engine reduces false fraud declines in card-not-present flows, giving issuers a competitive lift in e-commerce traffic.

Super-app ambitions among retailers and telcos reshape channel control. Areeba’s partnership with Foo delivers turnkey card programmes and wallets to banks pursuing embedded finance, shortening time-to-market and diversifying revenue beyond interchange. Geidea’s SoftPOS expansion into Egypt converts smartphones into terminals, attacking the last-mile acceptance gap and bolstering its regional merchant base.

Middle East And North Africa Digital Payments Industry Leaders

Paypal Holdings Inc.

ACI Worldwide Inc.

Visa Inc.

Mastercard Incorporated

Samsung Electronics Co., Ltd. (Samsung Pay)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Mastercard and Corpay launched a cross-border payments partnership, positioning joint network tokenisation and FX capabilities to serve enterprises’ treasury needs.

- May 2025: Mashreq aligned with Al Etihad Payments to unveil real-time rails for UAE SMEs, aiming to cut settlement cycles from T+1 to seconds.

- April 2025: PayPal and TerraPay teamed up to enhance instant cross-border payouts into Africa from Middle-East senders, expanding PayPal’s addressable remittance corridors.

- April 2025: Dubai-based Fuse raised USD 6.6 million to lower MENA cross-border transaction costs, betting on direct-bank integrations for sub-minute settlement.

Middle East And North Africa Digital Payments Market Report Scope

The report on digital payments in the Middle East and North Africa segments the market by payment mode, distinguishing between Point of Sale (POS) and Online/Remote Payment. Further categorization by component divides the market into solutions, such as Gateway, Processing, Wallet, Fraud, and others, and services, which encompass Consulting, Integration, and Support. The segmentation by enterprise size differentiates between Large Enterprises and Small and Medium Enterprises (SMEs). End-user industries are categorized into Retail and E-Commerce, Media and Entertainment, Healthcare, Hospitality and Travel, and Other Industries, which include Education, Utilities, and Government. Geographically, the report encompasses Saudi Arabia, the United Arab Emirates, Egypt, Turkey, Morocco, and the broader Middle East and North Africa region. All market forecasts are expressed in USD value.

By Mode of Payment

| Point of Sale (POS) |

| Online / Remote Payment |

By Component

| Solutions (Gateway, Processing, Wallet, Fraud, Other) |

| Services (Consulting, Integration, Support) |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By End-user Industry

| Retail and E-commerce |

| Media and Entertainment |

| Healthcare |

| Hospitality and Travel |

| Other End-user Industries (Education, Utilities, Govt.) |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Egypt |

| Turkey |

| Morocco |

| Rest of Middle East and North Africa |

| By Mode of Payment | Point of Sale (POS) |

| Online / Remote Payment | |

| By Component | Solutions (Gateway, Processing, Wallet, Fraud, Other) |

| Services (Consulting, Integration, Support) | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-user Industry | Retail and E-commerce |

| Media and Entertainment | |

| Healthcare | |

| Hospitality and Travel | |

| Other End-user Industries (Education, Utilities, Govt.) | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| Morocco | |

| Rest of Middle East and North Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the MENA digital payments market?

The MENA digital payments market size is USD 275.47 billion in 2026 and is forecast to reach USD 462.41 billion by 2031.

Which payment mode is expanding fastest?

Online/Remote payments are growing at a 14.45% CAGR, outpacing the Point-of-Sale segment that currently leads in share.

Why are services revenues accelerating quicker than solutions?

Implementation complexity around open banking, instant rails, and fraud management is driving 18.05% CAGR in services as firms seek specialised expertise.

Which country offers the highest growth potential?

Turkey is projected to record a 20.75% CAGR through 2031 owing to its young population, smartphone uptake, and supportive fintech regulation.

How are SMEs influencing market dynamics?

SMEs, growing at 21.85% CAGR, are adopting soft-POS and multi-currency gateways to expand cross-border sales, boosting transaction volumes beyond large-enterprise channels.

What is the principal challenge restraining wider adoption?

Fragmented interchange caps and escalating cyber-fraud, particularly in Egypt and Morocco, are dampening merchant economics and consumer trust, respectively.