Market Size of Middle East And Africa Freight & Logistics Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

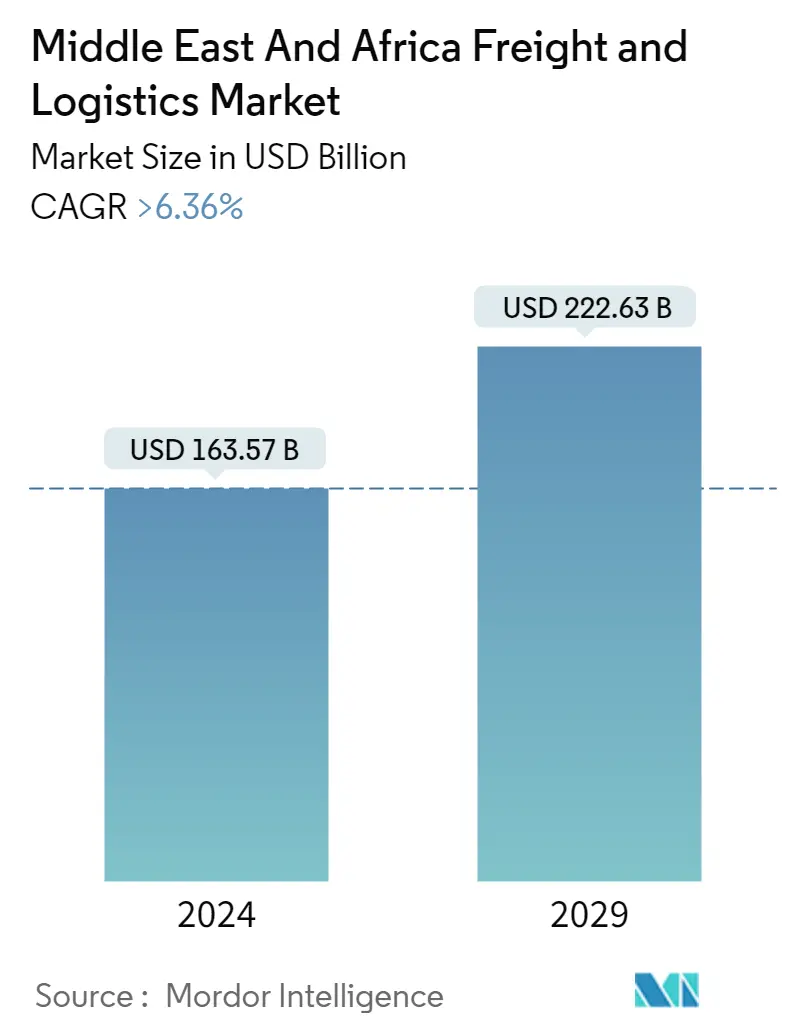

| Market Size (2024) | USD 163.57 Billion |

| Market Size (2029) | USD 222.63 Billion |

| CAGR (2024 - 2029) | > 6.36 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East & Africa Transport and Logistics Market Analysis

The Middle East And Africa Freight & Logistics Market size is estimated at USD 163.57 billion in 2024, and is expected to reach USD 222.63 billion by 2029, growing at a CAGR of greater than 6.36% during the forecast period (2024-2029).

During the past decade, globalization and technology created new opportunities for internationalization, boosting the supply chains and competitiveness in Africa. Currently, the most important countries in terms of logistics are Algeria, Angola, the Democratic Republic of Congo, Egypt, Ghana, Kenya, Mozambique, Nigeria, South Africa, and Tanzania. Some of them own key ports in the continent. For example, Barra owns Dande and Lobito in Angola, Lekki in Nigeria, Musoma in Tanzania, and Lamu in Kenya.

The political instability of some countries is likely to make territorial integration inappropriate in the short term. Domestic markets are predominant in this zone since there is little interaction among regions, which has led to a stagnation in international trade.

The economy is highly dependent on mining, which represents a third of the GDP. Morocco is a stable partner. Meanwhile, Egypt and Algeria have the highest production values. However, they are known for their little international interaction and lack of developed logistics corridors. African logistics companies are going beyond megacities and are looking to connect Africa's rural communities to regional supply chains.

While megacities are attracting millions of young Africans, Africa's population remains predominantly rural.

Despite a sustained period of decline over the last few years, affected by a fall in oil prices and geopolitical strife, Middle-East and Africa is fast becoming a region of automotive and supply chain opportunity. Carmakers such as VW, Toyota, GM, Groupe PSA, and Mercedes-Benz are investing in the local assembly, ranging from North African countries, including Morocco, Algeria, and Egypt, to sub-Saharan markets, such as Rwanda, Ethiopia, Kenya, and Ghana. The region also has some notable logistics developments.

Middle East & Africa Transport and Logistics Industry Segmentation

Logistics is a part of supply chain management that deals with the efficient forward and reverse flow of goods, services, and related information from the point of origin to the point of consumption according to the needs of customers.

The Middle East and Africa Logistics Market is Segmented by function, by end-user, by country. By function the market is segmented by freight transport, freight forwarding, warehousing, and value-added services and other services by end user the market is segmented by manufacturing and automotive, oil and gas, mining, and quarrying, agriculture, fishing, and forestry, construction, distributive trade, healthcare and pharmaceutical, and other end users by country the market is segmented by United Arab Emirates, Saudi Arabia, Qatar, South Africa, Egypt, Morocco, Nigeria, and Rest of Middle-East and Africa. The report offers market sizes and forecasts for the market in value (USD) for all the segments.

| By Function | ||||||

| ||||||

| Freight Forwarding | ||||||

| Warehousing | ||||||

| Value-added Services and Other Functions |

| By End User | |

| Manufacturing and Automotive | |

| Oil and Gas, Mining, and Quarrying | |

| Agriculture, Fishing, and Forestry | |

| Construction | |

| Distributive Trade (Wholesale and Retail Segments - FMCG Included) | |

| Other End Users (Telecommunications and Pharmaceuticals) |

| By Country | |

| United Arab Emirates | |

| Saudi Arabia | |

| Qatar | |

| South Africa | |

| Egypt | |

| Morocco | |

| Nigeria | |

| Rest of Middle-East and Africa |

Middle East And Africa Freight & Logistics Market Size Summary

The Middle East and Africa logistics market is poised for significant growth, driven by globalization and technological advancements that have enhanced supply chains and competitiveness across the region. Key countries such as Algeria, Angola, Egypt, Ghana, Kenya, Nigeria, and South Africa play pivotal roles, with strategic ports facilitating trade. Despite challenges like political instability and limited regional interaction, the market is expanding beyond urban centers to connect rural communities with regional supply chains. The automotive sector is also witnessing increased investment from major car manufacturers, further bolstering the logistics landscape. The region's airports, particularly in the Middle East, are experiencing substantial growth in cargo volumes, supported by strategic investments in infrastructure and a favorable regulatory environment. This growth is complemented by the development of airport hubs that cater to significant passenger and cargo traffic, with a focus on enhancing the overall travel experience.

Saudi Arabia stands out as a key logistics hub due to its strategic geographical location and ambitious infrastructure plans under the Saudi Vision 2030 initiative. This plan aims to reduce oil dependency by enhancing logistics capabilities through process streamlining, market liberalization, and the establishment of new economic zones. The Kingdom has made substantial capital investments to increase cargo capacity and simplify logistics operations, positioning itself as a central player in the Middle East logistics market. The market is characterized by a mix of international and local players, with major companies like DHL, FedEx, and UPS leading the charge. Recent collaborations and fleet expansions, such as those by Saudi Logistics Services and Almajdouie Logistics, highlight the ongoing efforts to strengthen logistics operations in the region, driven by the growing e-commerce sector and infrastructure development.

Middle East And Africa Freight & Logistics Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Rise In E-commerce Growth in The Region

-

1.2.2 Development of Logistic Infrastructure

-

-

1.3 Market Restraints

-

1.3.1 Poor Infrastruture

-

-

1.4 Market Opportunities

-

1.4.1 Logistics turns to tech to meet new demand

-

1.4.2 Government Initiatives

-

-

1.5 Value Chain/Supply Chain Analysis

-

1.6 Porter's Five Forces Analysis

-

1.6.1 Threat of New Entrants

-

1.6.2 Bargaining Power of Buyers/Consumers

-

1.6.3 Bargaining Power of Suppliers

-

1.6.4 Threat of Substitute Products

-

1.6.5 Intensity of Competitive Rivalry

-

-

1.7 Impact of COVID-19 on the market

-

-

2. MARKET SEGMENTATION

-

2.1 By Function

-

2.1.1 Freight Transport

-

2.1.1.1 Road

-

2.1.1.2 Water

-

2.1.1.3 Air

-

2.1.1.4 Rail

-

-

2.1.2 Freight Forwarding

-

2.1.3 Warehousing

-

2.1.4 Value-added Services and Other Functions

-

-

2.2 By End User

-

2.2.1 Manufacturing and Automotive

-

2.2.2 Oil and Gas, Mining, and Quarrying

-

2.2.3 Agriculture, Fishing, and Forestry

-

2.2.4 Construction

-

2.2.5 Distributive Trade (Wholesale and Retail Segments - FMCG Included)

-

2.2.6 Other End Users (Telecommunications and Pharmaceuticals)

-

-

2.3 By Country

-

2.3.1 United Arab Emirates

-

2.3.2 Saudi Arabia

-

2.3.3 Qatar

-

2.3.4 South Africa

-

2.3.5 Egypt

-

2.3.6 Morocco

-

2.3.7 Nigeria

-

2.3.8 Rest of Middle-East and Africa

-

-

Middle East And Africa Freight & Logistics Market Size FAQs

How big is the Middle East And Africa Freight & Logistics Market?

The Middle East And Africa Freight & Logistics Market size is expected to reach USD 163.57 billion in 2024 and grow at a CAGR of greater than 6.36% to reach USD 222.63 billion by 2029.

What is the current Middle East And Africa Freight & Logistics Market size?

In 2024, the Middle East And Africa Freight & Logistics Market size is expected to reach USD 163.57 billion.