Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

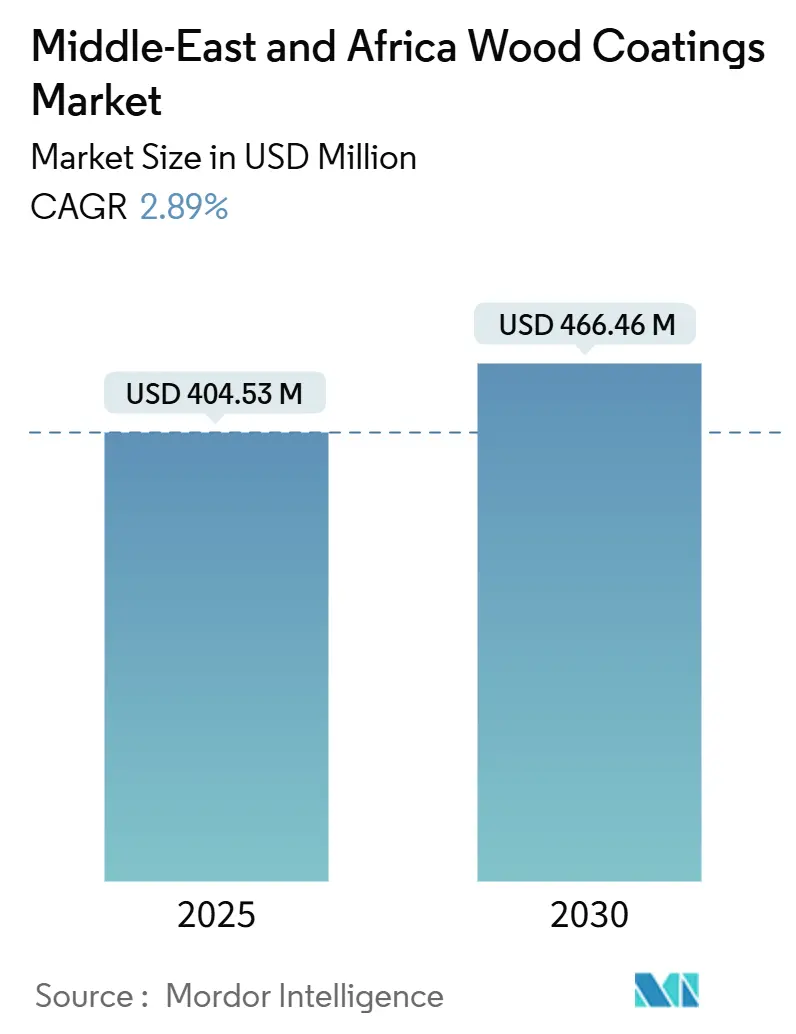

| Market Size (2025) | USD 404.53 Million |

| Market Size (2030) | USD 466.46 Million |

| Growth Rate (2025 - 2030) | 2.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Wood Coatings Market Analysis by Mordor Intelligence

The Middle East and Africa wood coatings market size is estimated at USD 404.53 million in 2025 and is expected to reach USD 466.46 million by 2030, at a CAGR of 2.89% during the forecast period (2025-2030). A widening gap is forming between Gulf Cooperation Council projects that demand premium, durability-focused finishes and East African furniture hubs that emphasize cost-efficient solvent systems. Global suppliers that can synchronize both ends of the spectrum capture share because contractors in Saudi Arabia and the United Arab Emirates specify two-component polyurethane for coastal humidity, while workshops in Kenya and Nigeria still depend on nitrocellulose to maximize daily throughput. Propylene-linked resin costs rose 30% in 2024, squeezing gross margins for formulators lacking long-term feedstock contracts. Meanwhile, Egypt, Morocco, and South Africa tightened VOC ceilings modeled on EU Directive 2004/42/EC, accelerating water-borne technology beyond 3.6% annual growth even as solvent-borne volumes remain dominant in price-sensitive inland markets.

Key Report Takeaways

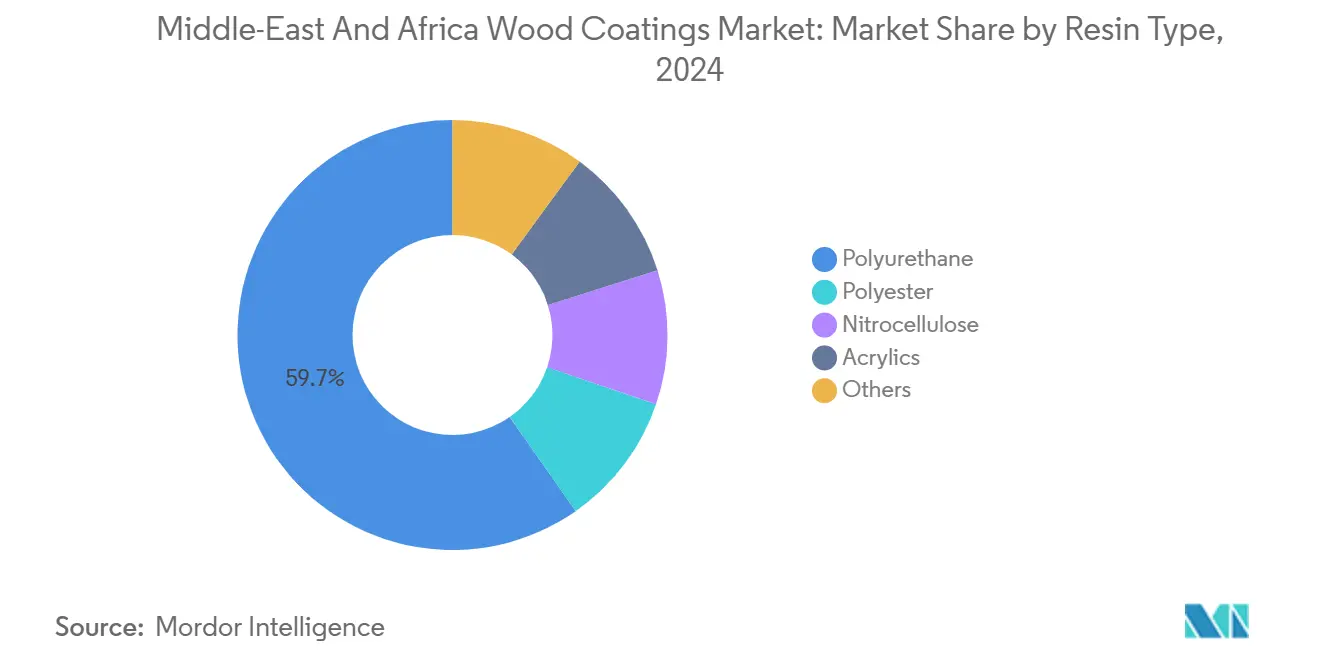

- By resin type, polyurethane led the Middle East and Africa wood coatings market with a 59.72% share in 2024 and is projected to expand at a 3.01% CAGR through 2030.

- By technology, solvent-borne products retained 56.76% revenue share in 2024, whereas water-borne offerings are set to grow at a 3.65% CAGR, the fastest among all technologies.

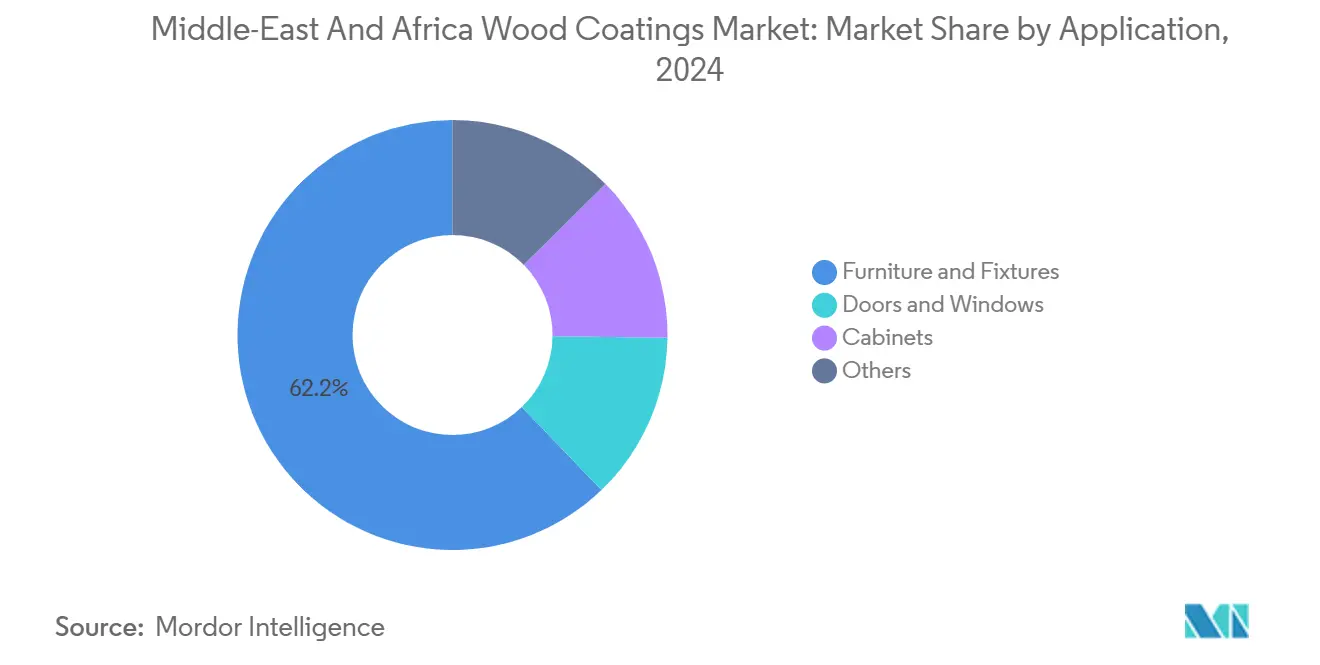

- By application, furniture and fixtures captured 62.19% of the 2024 demand; cabinets are advancing at a 3.10% CAGR through 2030, driven by the adoption of factory-finished MDF in Gulf residential towers.

- By geography, Saudi Arabia commanded a 21.67% share of the Middle East and Africa wood coatings market in 2024; the United Arab Emirates is forecast to post the fastest geographic growth at a 3.24% CAGR through 2030.

Middle-East And Africa Wood Coatings Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in GCC and East Africa construction pipeline | +0.9% | Saudi Arabia, UAE, Qatar, Kenya, Ethiopia | Medium term (2-4 years) |

| Expansion of regional furniture manufacturing hubs | +0.7% | Egypt, Morocco, Kenya, South Africa | Short term (≤ 2 years) |

| Regulatory shift toward water-borne systems | +0.5% | Egypt, Morocco, South Africa, spillover to GCC | Long term (≥ 4 years) |

| Tourism mega-projects demanding premium wood finishes | +0.6% | Saudi Arabia, UAE, Egypt | Medium term (2-4 years) |

| Rise of digital printing on engineered wood | +0.3% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Surge in GCC and East Africa Construction Pipeline

Public capital outlays are reshaping demand across building types. Saudi Arabia’s Public Investment Fund has directed USD 40 billion to projects that prioritize wood-intensive hospitality interiors, driving the specification of marine-grade polyurethane that withstands 90% humidity. Kenya’s affordable-housing program, which stipulates the use of locally sourced timber for the joinery, boosted interior-wood demand. Ethiopian customs tariffs discourage waterborne primer imports, so solvent lines remain dominant despite Addis Ababa’s real estate boom. Formulators therefore operate dual production lines to serve both high-performance Gulf projects and cost-sensitive East African housing.

Expansion of Regional Furniture Manufacturing Hubs

Morocco exported USD 358 million in furniture during 2024, led by Casablanca and Tangier plants that have adopted two-component polyurethane to meet European scratch-resistance standards. Kenya’s furniture sector, valued at USD 452 million, continues to struggle with a shortage of kiln-dried timber; reject rates for UV-cured finishes remain high, reinforcing nitrocellulose’s dominance. South Africa’s Western Cape manufacturers pivoted to engineered wood, reducing solvent emissions by 35% in line with provincial air-quality plans. Export-oriented hubs demand consistent, compliant coatings, whereas small workshops in Kenya and South Africa often prioritize price over performance.

Regulatory Shift Toward Water-Borne Systems

Egypt capped VOC content at 250 g/L for wood finishes, effective 2024, rendering 40% of nitrocellulose formulas non-compliant[1]Egypt Ministry of Environment, “VOC Decree 964/2023,” eeaa.gov.eg . Morocco harmonized limits with EU Directive 2004/42/EC, driving local formulators to reformulate or import compliant lines. South Africa issued 14 compliance notices to furniture makers in 2024, accelerating the need for booth retrofits that cost USD 27,000-43,000 each. GCC contractors are increasingly pursuing LEED points, which indirectly raises the requirement for low-VOC materials. Adoption remains uneven because Kenyan operators resist longer drying times.

Tourism Mega-Projects Demanding Premium Wood Finishes

Saudi Arabia’s Red Sea Project mandates UV-inhibited polyurethane for exterior cladding, raising per-square-meter coating cost by 40%. Expo City Dubai specifies factory-finished panels with UV-cured topcoats to compress schedules across 438 hectares. Egypt’s North Coast resorts adopted digitally printed panels to cut lead times to 10 days. Qatar’s Lusail district maintained nitrocellulose for heritage screens because waterborne systems could not achieve the required gloss threshold. Premium projects account for 18-20% of revenue, despite comprising only 8-10% of the volume.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC / REACH-like regulations | -0.4% | Egypt, Morocco, South Africa, spillover to GCC | Medium term (2-4 years) |

| Petro-resin price volatility | -0.5% | Global, acute in Kenya and Nigeria | Short term (≤ 2 years) |

| Shortage of kiln-dried timber supply | -0.3% | Kenya, Nigeria, Ethiopia, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC / REACH-Like Regulations

Egypt’s 250 g/L cap disqualified many nitrocellulose lines, forcing import of water-borne alternatives at 15-20% higher cost. Morocco now requires VOC declarations for exports to Europe, adding testing overhead that small workshops struggle to absorb. South African authorities issued 14 compliance notices in 2024; non-compliant plants faced shutdown threats. GCC projects increasingly request LEED-aligned low-VOC coatings, pushing water-borne penetration from 30% in 2022 to 48% in 2024. Capital costs for spray-line retrofits remain a hurdle, so many Kenyan and Nigerian shops keep solvent products despite lower margins.

Petro-Resin Price Volatility

Propylene spot prices surged sharply in 2024 following outages at Chinese crackers, which inflated acrylic and polyurethane costs. MDI and TDI prices increased by 18-22% following European capacity constraints, which hurt formulators without supply contracts. Solvent costs fluctuated in tandem with crude, swinging between USD 75-92 per barrel, yet small East African customers resisted quarterly repricing, squeezing working capital. Limited hedging liquidity in regional derivatives markets leaves most formulators exposed to price shocks.

Segment Analysis

By Resin Type: Polyurethane Dominance Anchored in Coastal Durability

Polyurethane captured 59.72% of the Middle-East and Africa wood coatings market share in 2024 and is rising at a 3.01% CAGR through 2030. Contractors in Jeddah, Doha, and Dubai routinely specify two-component PU for exterior joinery where 90% humidity threatens delamination. Polyester, which holds around 18%, remains popular in dry, inland Saudi regions, but exhibits brittleness under thermal cycling. Nitrocellulose fell to 12% because Egypt’s VOC cap forced exporters to drop legacy formulas. Water-borne polyurethane dispersions, marketed under the Bayhydur and Laromer brands, experienced double-digit growth in North Africa after distributors highlighted their EU compliance. UV-cured acrylics are expanding fast thanks to digital printing at Turkish and Egyptian MDF plants.

Polyurethane’s premium tier coexists with a value tier of single-component acrylics and residual nitrocellulose, which dominate the East African domestic furniture market. The bifurcation pressures vendors to run parallel supply chains. Over the forecast horizon, polyurethane’s share may inch higher as Gulf tourism projects multiply, while nitrocellulose continues to retreat in export-oriented clusters.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Water-Borne Gains Pace Despite Solvent-Borne Incumbency

Solvent-borne solutions retained 56.76% revenue in 2024, but water-borne volumes are set to grow 3.65% annually. Kenya and Nigeria still rely on solvent products because humidity-control infrastructure and reliable power remain scarce. UV-cured coatings, essential to digital printing, are gaining momentum at panel factories that now supply Gulf hospitality projects. Powder coatings remain pilot-scale, confined to NEOM tests where zero-VOC performance is critical. This two-speed transition enables multinational suppliers to leverage dual-cure portfolios, while regional firms pursue solvent substitution in export hubs.

By Application: Furniture Remains Core, Cabinets Climb

Furniture and fixtures retained 62.19% of 2024 demand and will grow at a 2.96% CAGR to 2030. Egypt’s Damietta hub alone aims for 1 million units of annual capacity by 2026, centralizing finishing and cutting coating waste by 22%. Morocco’s exporters accept 15-20% cost premiums on PU systems to retain EU contracts. Kenya’s lack of kiln-dried feedstock, with only 40% dried to specification, propels nitrocellulose reversion for throughput.

Doors and windows see steady gains as Gulf residential towers specify pre-finished frames, while cabinets benefit from factory-finished MDF panels that cut fit-out time by 18% on Dubai high-rises. Flooring, paneling, and outdoor furniture together account for roughly 9% of volume, often using heritage-compatible formulations in Oman and Qatar. Furniture’s share may dip slightly as cabinets advance in Gulf housing, yet export momentum in Egypt and Morocco anchors its dominance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Saudi Arabia’s 21.67% share is based on its vast construction portfolio and tourism resorts, which require marine-grade polyurethane. Vision 2030 housing plans specify factory-finished doors for 40% of 300,000 annual units, cementing demand for high-durability coatings. The United Arab Emirates, projected to grow at a rate of 3.24% annually through 2030, relies on Expo City Dubai and Saadiyat Cultural District, both of which require UV-cured panels for color fidelity[2]Expo City Dubai, “Master Plan Overview,” expocitydubai.com.

Egypt’s Damietta consolidates 400 workshops, enhancing just-in-time delivery for export clients and raising waterborne adoption. Morocco’s USD 358 million export trade continues 3.06% growth as EU buyers audit VOC compliance. South Africa’s Western Cape has shifted to engineered wood that accepts acrylic emulsions, thereby reducing solvent emissions. Nigeria and Algeria face port and power bottlenecks; Lagos workshops lack humidity control, which constrains the use of waterborne transport, while Algerian mills struggle with six-week timber delays. Qatar still specifies nitrocellulose for heritage mashrabiya screens due to extreme heat.

Premium demand clusters exist in Saudi Arabia, the UAE, and Qatar, where green-building goals reward low-VOC and UV-cured systems. Kenya, Nigeria, and Ethiopia remain price-driven with solvent incumbency. Egypt and Morocco straddle both worlds, exporting compliant furniture while serving domestic markets that still seek cost efficiency.

Competitive Landscape

The Middle East and Africa wood coatings market is moderately consolidated, with global majors having exclusive GCC dealer networks that guarantee specification support and marine-grade tinting. National Paints in the UAE and Crown Paints in Kenya utilize domestic plants to circumvent tariffs and offer 48-hour delivery, aligning with localized procurement cycles. Multinationals deploy solvent, waterborne, and UV lines under one roof, while regional challengers focus on waterborne formulations priced below those of imported brands. White-space lies in integrating digital printing with a turnkey coating supply. Durst and Hymmen installed UV-LED inkjet systems at Turkish and Egyptian MDF facilities; however, no coatings producer offers a bundled ink-plus-topcoat service—an opportunity for dual-cure specialists at durst-group.com. Competitive intensity will intensify as VOC rules become stricter and exporters demand compliant chemistry without incurring cost spikes.

Middle-East And Africa Wood Coatings Industry Leaders

Akzo Nobel N.V.

Jotun

PPG Industries Inc.

The Sherwin-Williams Company

Kansai Paint Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Crown Paints Kenya introduced a water-borne range aligned to the EU VOC Directive 2004/42/EC to help domestic manufacturers retain European buyers.

- September 2024: Jotun invested USD 20 million to expand Egyptian water-borne capacity aimed at Damietta exporters.

- June 2024: Asian Paints’ Qatar arm added 10,000 tpy wood-coating lines to serve GCC hospitality projects specifying polyurethane dispersions.

Middle-East And Africa Wood Coatings Market Report Scope

By Resin Type

| Polyurethane |

| Polyester |

| Nitrocellulose |

| Acrylics |

| Others |

By Technology

| Water-borne |

| Solvent-borne |

| UV cured |

| Powder |

By Application

| Furniture and Fixtures |

| Doors and Windows |

| Cabinets |

| Others |

By Geography

| South Africa |

| Egypt |

| Morocco |

| Nigeria |

| Algeria |

| Kenya |

| Saudi Arabia |

| United Arab Emirates |

| Iran |

| Rest of Middle East and Africa |

| By Resin Type | Polyurethane |

| Polyester | |

| Nitrocellulose | |

| Acrylics | |

| Others | |

| By Technology | Water-borne |

| Solvent-borne | |

| UV cured | |

| Powder | |

| By Application | Furniture and Fixtures |

| Doors and Windows | |

| Cabinets | |

| Others | |

| By Geography | South Africa |

| Egypt | |

| Morocco | |

| Nigeria | |

| Algeria | |

| Kenya | |

| Saudi Arabia | |

| United Arab Emirates | |

| Iran | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Middle East and Africa wood coatings market in 2025?

The Middle East and Africa wood coatings market is estimated at USD 404.53 million, with a forecast value of USD 466.46 million by 2030.

Which resin leads demand in the region?

Polyurethane holds a 59.72% share thanks to its high-humidity durability and is growing at a 3.01% CAGR.

Why are water-borne coatings gaining ground?

Egypt, Morocco, and South Africa set VOC ceilings modeled on EU rules, pushing water-borne volumes even though solvent products remain larger overall.

What is the fastest-growing geography?

The United Arab Emirates is expanding at a 3.24% CAGR through 2030 on the back of Expo City Dubai and other mixed-use projects.

How do raw-material prices affect margins?

Propylene and isocyanate volatility raised resin costs by up to 22% in 2024, squeezing formulators without long-term feedstock contracts.

Which new technology could disrupt the market?

Digital inkjet printing paired with UV-cured topcoats can cut labor 25% and is already piloted at Turkish and Egyptian MDF plants.