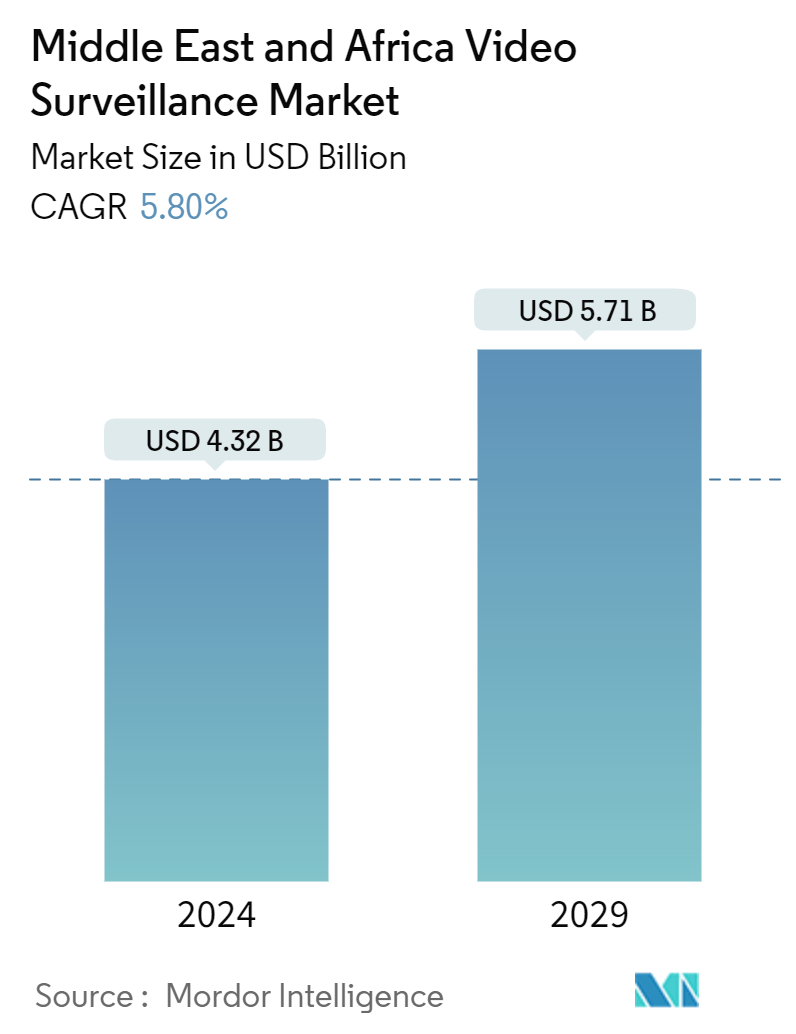

Market Size of Middle East And Africa Video Surveillance Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 4.32 Billion |

| Market Size (2029) | USD 5.71 Billion |

| CAGR (2024 - 2029) | 5.80 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East And Africa Video Surveillance Market Analysis

The Middle East And Africa Video Surveillance Market size is estimated at USD 4.32 billion in 2024, and is expected to reach USD 5.71 billion by 2029, growing at a CAGR of 5.80% during the forecast period (2024-2029).

The countries in the Middle East have technologically advanced digital surveillance infrastructure, especially in the Gulf Cooperation Council (GCC) states. In the past 10 years, governments of the Middle East have employed digital information and communication technologies to reinforce control over their citizens. Drawing inspiration from models provided by China, Russia, and Israel, Middle Eastern governments have implemented policies and strategies aimed at censorship, digital deception, and mass surveillance.

Two factors in the region have majorly supported this growing focus on digital surveillance. First, the GCC states are among the most “successful” models presenting authoritarian adaptation to digital activism in the Middle East. These states primarily avoided the violence and chaos that emerged from the suppression of the “Arab Spring” movements. However, the GCC military, security assistance to Bahrain, and simmering tensions in eastern Saudi Arabia were important exceptions. Domestically, these states are particularly susceptible to the perceived risks of social media and are heavily committed to preventing the resurgence of revolutionary politics. Notably, they have also sought to influence the course of devastating conflicts persisting in Libya, Syria, and Yemen online and offline, with various results.

Secondly, the Gulf states are significantly well-connected, both in terms of their internet penetration rates that are consistently the highest in the region and compare favorably worldwide, and because their openness to global capital has turned them sites of significant digital expertise in e-government, health, energy, and other critical sectors. These states have sought to utilize their reputation as major players in digital innovation to underpin long-term efforts at economic diversification and deflect political criticism.

Moreover, from the ‘Golden Shield Project’ to the Great Firewall, Sky-Net, and Sharp Eyes, China has been a model for digital authoritarianism and remains the main supplier of advanced mass surveillance technologies. The making of a ‘Silk Digital Road’ has further favored the export of technologies and knowledge toward the regions: Egypt, Morocco, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) to build a digital totalitarian state, with the United Arab Emirates investing in sophisticated programs such as smart cities technology and the “Police without Policemen” program.

In April 2024, for the first time since its inception, the Gulf Cooperation Council (GCC) announced its ‘Vision for Regional Security’ at a ceremony held in its headquarters in Riyadh. The ‘Vision for Regional Security’ emphasizes that it is based on the principles of shared destiny and indivisible security of the member states, and any threat to one is a threat to all the member states.

Moreover, in December 2023, the United Arab Emirates announced installing 12,000 surveillance cameras at the United Nations' COP28 climate summit in Dubai. Also, the country already has deployed facial recognition at immigration gates at Dubai International Airport, the world’s busiest for international travel. Thus, with such announcements coming into the picture, the fact gets strength that digital surveillance technologies play a central role in these dynamics, thus driving the role of video surveillance in the regional market.

Middle East And Africa Video Surveillance Industry Segmentation

Video surveillance systems contain one or more video cameras connected to a network that sends the captured video or audio data to a specific location. The captured images are monitored in real-time or sent to a central location for recording and storage. Many applications, such as crime prevention, industrial process monitoring, and traffic management, increasingly utilize video surveillance systems. The market is defined by the revenue from the sales of different video surveillance products that find applications for various end users across the countries, including the United Arab Emirates, Saudi Arabia, and South Africa.

The Middle East and African video surveillance systems market is segmented by type (hardware [camera [analog, IP cameras, and hybrid], storage], software [video analytics and video management software], services [VsaaS]), end-user vertical (commercial, infrastructure, institutional, industrial, defense, residential), and country (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD).

| By Type | ||||||||

| ||||||||

| ||||||||

| Services (VSaaS) |

| By End-user Vertical | |

| Commercial | |

| Infrastructure | |

| Institutional | |

| Industrial | |

| Defense | |

| Residential |

| By Country*** | |

| United Arab Emirates | |

| Saudi Arabia | |

| South Africa | |

| Iran | |

| Nigeria | |

| Iraq |

Middle East And Africa Video Surveillance Market Size Summary

The Middle East and Africa video surveillance market is experiencing significant growth, driven by advancements in digital surveillance infrastructure, particularly in the Gulf Cooperation Council (GCC) states. These countries have adopted sophisticated digital information and communication technologies to enhance control over their populations, drawing inspiration from models in China, Russia, and Israel. The GCC states, known for their high internet penetration and openness to global capital, are leveraging their status as digital innovation leaders to support economic diversification and mitigate political dissent. The region's focus on digital surveillance is further bolstered by geopolitical tensions and the need for enhanced security measures, as evidenced by initiatives like the United Arab Emirates' smart cities technology and the "Police without Policemen" program.

The market is characterized by a fragmented landscape with major players such as Panasonic, Samsung, Honeywell, and Bosch, who are employing strategies like partnerships, innovations, and acquisitions to strengthen their market position. The integration of AI technology for video analytics is transforming security procedures, particularly in Saudi Arabia, while maritime surveillance is gaining importance due to piracy threats in key shipping routes. Regulatory bodies in the GCC have mandated stringent surveillance measures, contributing to the market's expansion. The ongoing geopolitical conflicts and security challenges in the region are driving governments to increase their defense budgets, further fueling the demand for video surveillance solutions.

Middle East And Africa Video Surveillance Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Impact of Macro Economic Trends on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Hardware

-

2.1.1.1 Camera

-

2.1.1.1.1 Analog

-

2.1.1.1.2 IP Camera

-

2.1.1.1.3 Hybrid

-

-

2.1.1.2 Storage

-

-

2.1.2 Software

-

2.1.2.1 Video Analytics

-

2.1.2.2 Video Management Software

-

-

2.1.3 Services (VSaaS)

-

-

2.2 By End-user Vertical

-

2.2.1 Commercial

-

2.2.2 Infrastructure

-

2.2.3 Institutional

-

2.2.4 Industrial

-

2.2.5 Defense

-

2.2.6 Residential

-

-

2.3 By Country***

-

2.3.1 United Arab Emirates

-

2.3.2 Saudi Arabia

-

2.3.3 South Africa

-

2.3.4 Iran

-

2.3.5 Nigeria

-

2.3.6 Iraq

-

-

Middle East And Africa Video Surveillance Market Size FAQs

How big is the Middle East And Africa Video Surveillance Market?

The Middle East And Africa Video Surveillance Market size is expected to reach USD 4.32 billion in 2024 and grow at a CAGR of 5.80% to reach USD 5.71 billion by 2029.

What is the current Middle East And Africa Video Surveillance Market size?

In 2024, the Middle East And Africa Video Surveillance Market size is expected to reach USD 4.32 billion.