Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.69 Billion |

| Market Size (2030) | USD 5.63 Billion |

| Growth Rate (2025 - 2030) | 8.81% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Venture Capital Market Analysis by Mordor Intelligence

The Middle East and Africa venture capital market size stood at USD 3.69 billion in 2025 and is projected to reach USD 5.63 billion by 2030, expanding at an 8.81% CAGR during the forecast period. Robust sovereign‐wealth funding, rapid financial-technology uptake, and regulatory modernization underpin growth despite recent global liquidity tightening. Patient domestic capital from Gulf sovereign funds, particularly the Public Investment Fund’s plan to deploy USD 70 billion annually after 2025, shields the ecosystem from interest-rate volatility. Sector leadership remains with fintech, yet healthcare delivers the fastest growth on the back of Vision 2030 reforms and dedicated vehicles such as the USD 250 million Afiyah Fund. Early-stage deal dominance continues, but rising venture-debt volumes and larger follow-on checks signal a transition toward scale-up finance sophistication.

Key Report Takeaways

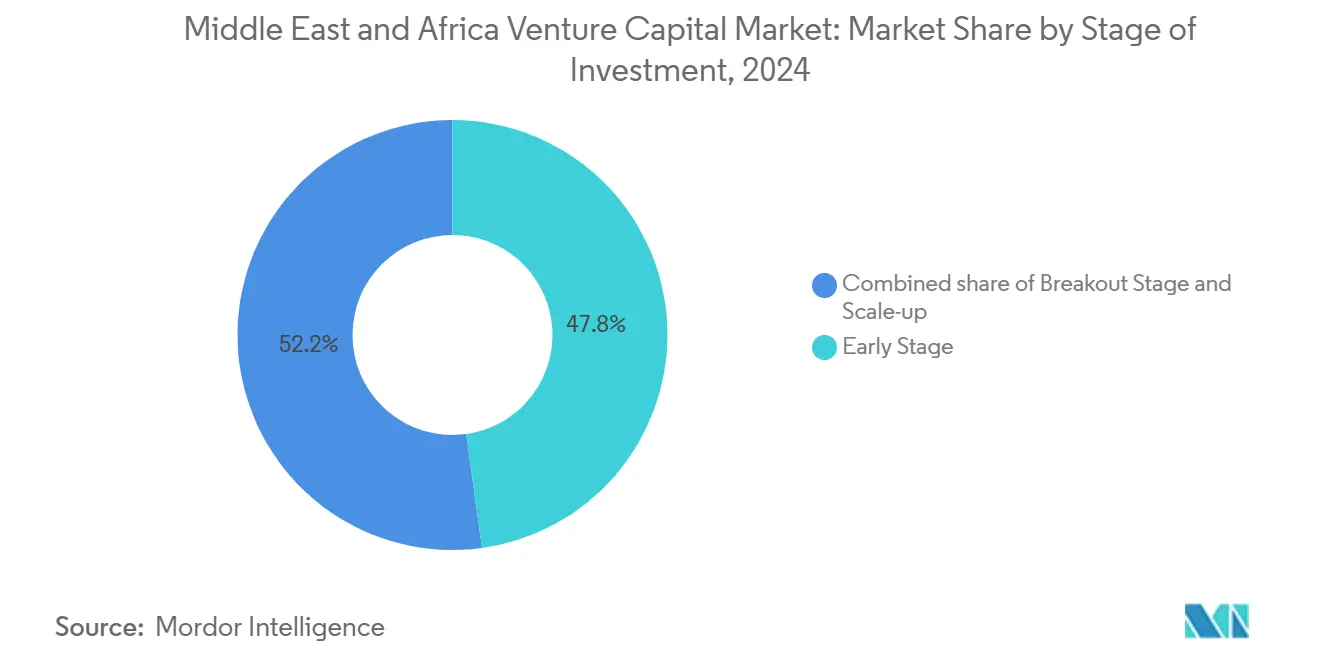

- By stage, early investments captured 47.8% of the Middle East and Africa venture capital market share in 2024, while scale-up rounds are forecast to grow at 9.34% CAGR through 2030.

- By industry, fintech led with 34.6% revenue share in 2024; healthcare is projected to advance at 9.03% CAGR to 2030.

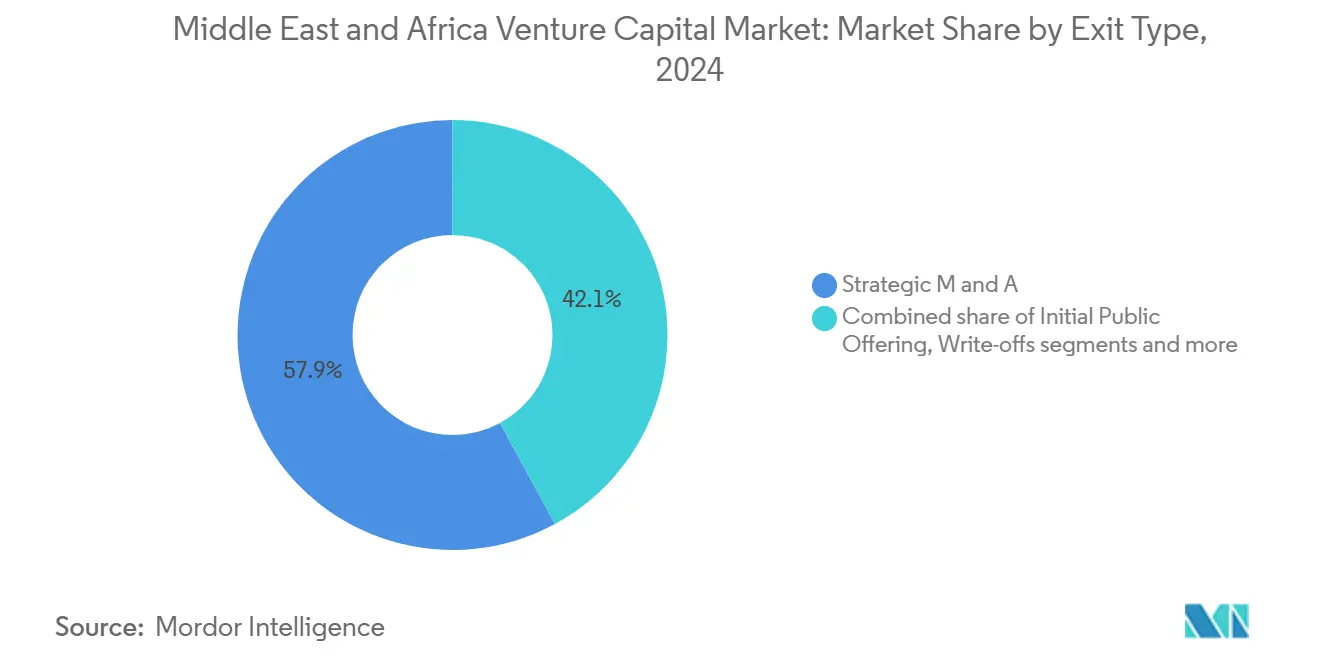

- By exit route, strategic mergers and acquisitions accounted for 57.9% of the Middle East and Africa venture capital market size in 2024, and IPOs are expanding at a 9.83% CAGR.

- By geography, the UAE commanded a 43.8% share in 2024, whereas Saudi Arabia is recording the highest forecast CAGR at 10.21% to 2030.

Middle East And Africa Venture Capital Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant sovereign-backed startup funds | +2.1% | UAE, Saudi Arabia, Qatar, Kuwait | Long term (≥ 4 years) |

| Rapid fintech adoption across MEA | +1.8% | Global MEA, concentrated in UAE, Saudi, Egypt, Nigeria | Medium term (2-4 years) |

| Business-friendly regulatory reforms | +1.4% | UAE (ADGM, DIFC), Saudi Arabia, Egypt | Medium term (2-4 years) |

| Surge in Sharia-compliant impact investing | +0.9% | GCC states, Muslim-majority African markets | Long term (≥ 4 years) |

| Diaspora-led angel networks catalyzing later rounds | +0.7% | Cross-border MEA-US, MEA-Europe corridors | Short term (≤ 2 years) |

| Cross-border CVC from telcos & energy majors | +0.6% | Regional GCC, selective African markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Abundant Sovereign-Backed Startup Funds

Gulf sovereign funds collectively manage roughly USD 4 trillion and supply more than 54% of global sovereign deployment in 2024. Saudi Arabia’s Public Investment Fund earmarks over 70% of its rising annual outlays for domestic assets, channeling long-dated capital into local venture vehicles. Mubadala’s creation of MGX, with stakes in OpenAI and Databricks, exemplifies strategic technology investing that extends beyond traditional VC horizons[1]“Opinion | SWFs, AI and the New Space Race,” fDi Intelligence, fdiintelligence.com. Sovereign participation stabilizes valuations and offers follow-on certainty, mitigating global risk-off episodes. Development-finance institutions have joined these funds in blended-finance structures worth USD 213 billion, widening pools available to startups tackling social and climate challenges[2]Javier Capapé Aguilar & Drew Johnson, “Sovereign Wealth Funds 2024,” IE University, static.ie.edu.

Rapid Fintech Adoption Across MEA

Fintech dominated with a 34.6% share in 2024 as regional e-commerce is set to hit USD 50 billion in 2025, lifting demand for digital payments. African mobile-money accounts surpassed 2.1 billion, providing a distribution backbone that venture-funded wallets can monetize. Outbound remittances of AED 145.7 billion from the UAE and USD 38.56 billion from Saudi Arabia highlight cross-border payment opportunities. Real-time transaction values in the Middle East are forecast to quadruple to USD 2.6 billion by 2027, reinforcing revenue visibility for payment-rail startups. Regulatory sandboxes and open-banking mandates in Bahrain and Saudi Arabia accelerate licensing, shortening go-to-market periods and attracting patient capital.

Business-Friendly Regulatory Reforms

The UAE’s 2023 federal e-commerce law and Saudi data-privacy sandbox streamline compliance and boost investor confidence. Free-zone regimes such as DIFC and ADGM offer 100% foreign ownership and fast-track fund licensing, lowering setup costs for general partners. Sustainable-finance guidelines crafted by the UAE’s inter-agency working group align disclosure rules across regulators, supporting ESG-oriented vehicles. Saudi renewable-energy targets of 58.7 GW by 2030 generate predictable demand for clean-tech solutions, widening sectoral scope for investors. GDPR-style data laws across Qatar and Saudi Arabia harmonize cross-border data flows, reducing operational friction for cloud-based startups.

Surge in Sharia-Compliant Impact Investing

Islamic-finance super-apps such as IMAN illustrate venture-backed avenues to meet the USD 13.2 billion SME financing gap in nine MENA economies. GCC green-sukuk issuance ballooned to USD 28.5 billion in 2022, offering structured exits for compliant startups via Nasdaq Dubai’s globally leading ESG-sukuk platform. ADGM now certifies “Green” or “Climate Transition” funds, giving clarity for impact-focused limited partners. Regulatory fee waivers on sustainability listings in Dubai cut capital-market access costs, enlarging the exit universe. The World Bank’s Global Findex shows sizeable unbanked Muslim-majority populations, underscoring demand for Sharia-compliant fintech backed by region-specific venture vehicles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited exit avenues & shallow capital markets | -1.6% | Africa-focused, selective Middle East markets | Long term (≥ 4 years) |

| Political-economic instability in select markets | -1.2% | Fragile African states, conflict-affected regions | Short term (≤ 2 years) |

| Talent drain via global remote-work migration | -0.8% | Sub-Saharan Africa, emerging MENA markets | Medium term (2-4 years) |

| Currency volatility eroding exit returns | -0.7% | Nigeria, Egypt, South Africa, select African markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Exit Avenues & Shallow Capital Markets

Africa recorded only 26 venture-backed exits in 2024, returning just USD 0.13 per invested dollar, underscoring liquidity headwinds[3]Francesca Tabor, “Investing in African Startups,” FRANKI T, frankit.com. MENA startups have raised USD 11 billion since 2021, yet fewer than 7.5% achieved exits, pointing to a growth-stage funding gap near USD 20 billion. UAE listing rules requiring two years of profitability curb IPO access for high-growth startups and skew exits toward strategic sales. Fragmented national exchanges raise cross-border compliance costs, discouraging dual listings that could broaden investor bases. Limited analyst coverage in post-IPO trading suppresses liquidity, dampening valuation multiples and recycle rates for venture funds.

Political-Economic Instability in Select Markets

Nigeria’s naira slid 40.9% in 2024 after deregulation, diluting USD returns for investors. High startup-formation costs equal to 36% of per-capita income in Sub-Saharan Africa compare poorly with 3% in OECD peers, restraining pipeline creation. Limited broadband (37% penetration) and unreliable electricity (43% access) cap technology addressable market, forcing investors to price infrastructure risk. Divergent ESG standards across jurisdictions complicate due diligence workloads, lengthening deal cycles for cross-border funds. Ongoing talent emigration, 30% of college-educated African youth, elevates recruitment costs for portfolio companies, eroding competitiveness.

Segment Analysis

By Stage of Investment: Early Dominance Drives Scale-Up Acceleration

Early-stage funding held 47.8% of the Middle East and Africa venture capital market share in 2024, reflecting generous sovereign seed programs and sandbox initiatives that derisk product validation. Scale-up rounds, though smaller in count, are projected to post the ecosystem’s fastest 9.34% CAGR to 2030 as breakout firms bridge the USD 10-15 million financing gap through rising venture-debt lines. Average initial checks of USD 500,000-1.5 million and reserve ratios near 45% position funds to support multiple follow-on cycles, sustaining portfolio momentum. Venture-debt deals jumped from USD 202 million in 2022 to USD 757 million in 2023, evidencing late-stage financing sophistication that nurtures scale-ups through capital-intensive growth phases. Strengthened valuation governance post-2022 ensures disciplined step-ups tied to institutional priced rounds, reinforcing market resilience.

Growth-stage scarcity has drawn global co-investors, with sovereign funds syndicating larger tickets alongside Silicon Valley and Asian firms, improving exit optionality. Early-stage abundance is enabled by angel collectives like COREangels MEA and fund-of-funds programs such as VC Grow that back first-time managers averaging USD 40 million vehicles. Breakout rounds benefit from enhanced third-party valuation services and updated governance codes introduced across DIFC and ADGM in 2024, lowering diligence friction for foreign limited partners. The Middle East and Africa venture capital market size devoted to scale-up deals is set to expand faster than any other stage as sovereign investors pursue domestic tech champions to advance industrial diversification agendas. Overall, stage distribution signals a maturing capital stack transitioning from pure company formation toward balanced growth-equity support.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Industry: Fintech Leadership Meets Healthcare Innovation

Fintech commanded 34.6% of 2024 funding, underpinned by soaring digital-payments penetration and regulatory clarity on open banking. Healthcare, while smaller, is forecast to post the highest 9.03% CAGR as Vision 2030 initiatives funnel patient capital into life-science infrastructure and biotech R&D, expanding the Middle East and Africa venture capital market size allocated to medical innovation. Enterprise software captures a steady share through AI and automation platforms aligned with billion-dollar national AI programs such as Saudi Project Transcendence. Energy transition plays attract sovereign backing, with Gulf funds investing USD 26.1 billion in renewables and hydrogen supply chains during 2023. Transportation and robotics secure niche allocations tied to smart-city megaprojects and manufacturing automation roadmaps across the GCC.

The Afiyah Fund expects to mobilize up to USD 500 million into Saudi health services, amplifying specialized capital depth and reinforcing the sector’s outsized growth trajectory. Nigerian fintech leader OPay neared a USD 3 billion valuation in 2024, showcasing scalable unit economics that entice cross-regional investors. Enterprise AI vendor DXwand raised USD 4 million to scale multilingual customer-engagement engines, spotlighting natural-language AI demand in Arabic markets. Energy and mobility startups leverage policy certainty—such as PIF’s target to develop 70% of Saudi renewable capacity—to de-risk project pipelines and entice blended-finance participation. Sectoral diversification beyond fintech strengthens portfolio risk profiles and aligns with sovereign imperatives to build knowledge-economy capabilities.

By Exit Type: Strategic Acquisitions Dominate IPO Acceleration

Strategic M&A delivered 57.9% of liquidity in 2024, reflecting the prevalence of corporate buyers seeking technology capabilities across telecom, energy, and banking verticals. Initial public offerings, though only a fraction of exits, are forecast to rise ata 9.83% CAGR as regional exchanges relax eligibility and deepen aftermarket support, expanding the Middle East and Africa venture capital market share realized via public routes. Secondary sales and continuation funds gain traction, mirroring global GP-led trends that peaked at USD 162 billion in 2024. Write-offs remain within historical norms despite 2022–2023 markdowns as valuation discipline and follow-on reserves temper impairment risk. Capital-market initiatives such as Dubai’s carbon-credit trading pilot and Abu Dhabi’s ESG index foster diversified investor bases, supporting future venture-backed listings.

Heightened IPO momentum aligns with sovereign privatization pipelines and global index inclusion efforts, which can lift free-float and liquidity thresholds. Corporate-venture participation, 13% of 2024 funding, creates natural acquirers, shortening average hold periods and improving cash-on-cash multiples for early-stage funds. Secondary sales benefit from growing fund-of-funds interest that provides recycling avenues without full public-market exposure. Exchange reforms tackling foreign-ownership caps and fast-track prospectus reviews in the UAE and Saudi Arabia are expected to further unlock IPO throughput by 2027. Collectively, exit-route diversification reduces portfolio-duration risk and underpins long-term return sustainability across the ecosystem.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The UAE held a dominant 43.8% share in 2024, leveraging DIFC and ADGM frameworks that streamline fund licensing and enable 100% foreign ownership, making Dubai and Abu Dhabi regional launchpads. Sovereign vehicles such as Mubadala and ADQ accelerated venture deployment, with Mubadala’s deal value surging 175% in 2024, elevating local dry powder and boosting the Middle East and Africa venture capital market size centered in the Emirates. Harmonized sustainable-finance rules plus waiver incentives on green listings broaden exit avenues, reinforcing investor confidence. Outbound technology M&A by Emirati funds recycles capital and embeds global intelligence back into domestic portfolios, nurturing a virtuous funding loop. Large-scale AI investments, including Microsoft’s USD 1.5 billion into G42, create downstream deal flow for frontier-tech startups.

Saudi Arabia posts the fastest 10.21% CAGR through 2030, driven by Vision 2030, Jada Fund of Funds, and sandbox programs hosted by the Saudi Data & AI Authority. PIF’s USD 70 billion annual deployment goal, paired with Project Transcendence’s USD 100 billion AI ecosystem, lifts domestic demand for venture finance and boosts the Middle East and Africa venture capital market size allocated to Saudi startups. Healthcare vehicles such as the Afiyah Fund and renewable-energy mandates create sector-specific pull for investors targeting long-duration assets. Buy-now-pay-later adoption, growing from 3 million users in 2021 to over 10 million in 2022, illustrates rapid consumer-tech scaling potential. Regulatory clarity on data privacy and virtual assets positions the kingdom as an emerging hub for fintech and Web3 innovation.

Nigeria and South Africa lead Africa’s venture landscape, with Nigeria attracting USD 520 million in 2024 (+11% YoY) as fintech giants such as OPay demonstrate four-fold customer growth. South Africa benefits from liquid capital markets and established governance standards, anchoring pan-African fund managers. Egypt, Kenya, and Tanzania headline the “Rest of MEA” opportunity set; Tanzania’s USD 52 million raise in 2024 equaled 1,150% growth, exemplifying base-effect acceleration. Diaspora capital bridges markets through initiatives like the US-MENA Tech Summit, expanding syndicate size, and derisking cross-border deployment. Combined, geographic spread allows portfolio diversification while tapping Saudi growth momentum and UAE infrastructure advantages, balancing return potential with risk mitigation.

Competitive Landscape

Funding concentration remains moderate, with early-stage deals spread across various emerging managers. In contrast, growth rounds exceeding USD 10 million are primarily dominated by sovereign funds and a small group of established general partners (GPs). In 2024, investors from the UAE and Saudi Arabia contributed to over 90% of the GCC's deal volume, showcasing their significant influence in the region. Meanwhile, African investments were more dispersed, with capital flowing into key markets such as Nigeria, Kenya, South Africa, and Egypt. Co-investment has become a standard practice, as sovereign entities collaborate with global funds to bring in expertise and share the costs of due diligence. For instance, Mubadala's participation in Silicon Valley AI rounds through syndicates highlights this trend. Additionally, corporate venture capital accounted for 13% of total funding in 2024, with major telecom and energy companies leveraging their financial resources to secure strategic positions in emerging technologies. A gap in mid-ticket deals, particularly in the USD 10-15 million range, has created opportunities for specialized growth funds and debt providers to enter the market.

Regulatory expertise has emerged as a critical factor distinguishing market leaders. Firms with dedicated in-house policy teams are better equipped to navigate complex data-localization laws across the GCC and Africa. This capability enables them to close deals faster and ensures smoother compliance after investments are made. The adoption of advanced technologies, such as AI-driven deal sourcing and automated dashboards for limited partners (LPs), has further enhanced operational efficiency. These tools allow managers to oversee larger portfolios without needing to proportionally increase their workforce, providing a competitive advantage in managing resources effectively.

The market is also witnessing a rise in specialized investment vehicles, which cater to niche themes and counter the limitations of generic strategies. For example, TVM Capital’s Afiyah Fund focuses on healthcare, while MGX targets global AI infrastructure, reflecting a growing trend toward thematic investments. Additionally, diaspora-driven networks like COREangels MEA are playing a pivotal role in channeling overseas talent and capital into underserved African cities. This approach is expanding the competitive landscape and fostering growth in regions that have traditionally been overlooked, creating new opportunities for investors and entrepreneurs alike[4]“COREangels Founder Advocates for African Entrepreneurship,” COREangels, coreangels.com.

Middle East And Africa Venture Capital Industry Leaders

Wamda Capital

Middle East Venture Partners (MEVP)

Global Ventures

Partech Partners

Beco Capital

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Wamda Capital joined Prosus to inject USD 10 million seed funding into UAE-based AI platform qeen.ai, which has generated over 1 million SKU descriptions since Q2 2024.

- January 2025: BioSapien extended its pre-Series A to USD 7 million, marking Golden Gate Ventures’ first MENA deployment and enabling MediChip™ colorectal cancer trials in the UAE.

- January 2025: MoneyHash secured USD 5.2 million pre-Series A led by Flourish Ventures to scale its MEA payment-orchestration stack, citing 3× lower failure rates for merchants.

- December 2024: Saudi AI-infrastructure firm OmniOps raised SAR 30 million (USD 8 million) from GMS Capital Ventures to expand HPC clusters serving national carriers.

Middle East And Africa Venture Capital Market Report Scope

Venture capital (VC) is a form of private equity and a type of financing that investors provide to startup companies and small businesses that are believed to have long-term growth potential. Venture capital generally comes from well-off investors, investment banks, and any other financial institutions. The report on the Middle East and Africa Venture Capital market comprehensively evaluates market segmentation, product categories, existing market trends, market dynamics shifts, and growth opportunities. Middle East and Africa Venture Capital Markets are segmented by type (local investors and international investors), industry (real estate, financial services, food & beverage, healthcare, transport, and logistics, IT & ITeS, education, and Other Industries (Energy, etc.)), and Country (United Arab Emirates, Saudi Arabia, Egypt, and rest of Middle East and Africa). The report offers Market size and forecasts for the Middle East and Africa Venture Capital Market in terms of transaction volume and/or revenue (USD) for all the above segments.

By Stage of Investment

| Early Stage |

| Breakout Stage |

| Scale-up |

By Industry

| Health |

| Fintech |

| Enterprise Software |

| Energy |

| Transportation |

| Robotics |

| Other Industries |

By Exit Type

| Initial Public Offering (IPO) |

| Strategic M&A |

| Secondary Sale / Buy-out |

| Write-offs |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Rest of Middle East & Africa |

| By Stage of Investment | Early Stage |

| Breakout Stage | |

| Scale-up | |

| By Industry | Health |

| Fintech | |

| Enterprise Software | |

| Energy | |

| Transportation | |

| Robotics | |

| Other Industries | |

| By Exit Type | Initial Public Offering (IPO) |

| Strategic M&A | |

| Secondary Sale / Buy-out | |

| Write-offs | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Middle East and Africa venture capital space today?

The market is valued at USD 3.69 billion in 2025 and is projected to reach USD 5.63 billion by 2030 at an 8.81% CAGR.

Which sector attracts the most funding?

Fintech leads with 34.6% of 2024 deployment thanks to booming digital-payments adoption and supportive regulation.

Where is growth fastest geographically?

Saudi Arabia is forecast to post the highest 10.21% CAGR through 2030, driven by Vision 2030 and PIF capital inflows.

What is the primary exit route for investors?

Strategic mergers and acquisitions delivered 57.9% of exits in 2024, although IPO activity is rising quickly.

What challenges most limit returns?

Shallow public markets and currency volatility, especially in select African economies, constrain exit valuations and recycle rates.

How are sovereign wealth funds influencing the landscape?

Gulf sovereigns manage about USD 4 trillion and increasingly channel patient, strategic capital into domestic startups, stabilizing funding across cycles.