| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 4.03 Billion |

| Market Size (2030) | USD 4.88 Billion |

| CAGR (2025 - 2030) | 3.90 % |

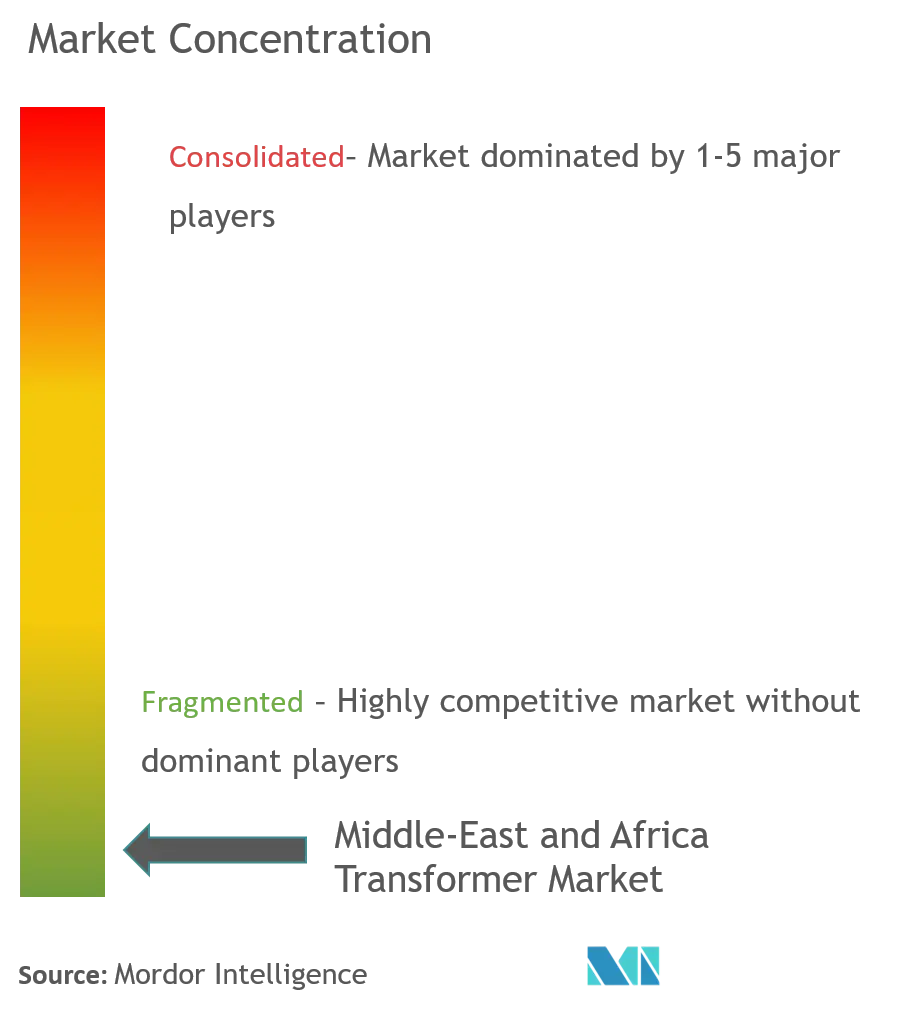

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Middle East And Africa Transformer Market Analysis

The Middle East And Africa Transformer Market size is estimated at USD 4.03 billion in 2025, and is expected to reach USD 4.88 billion by 2030, at a CAGR of 3.9% during the forecast period (2025-2030).

The Middle East and Africa transformer market is experiencing significant transformation driven by rapid industrialization and infrastructure development across the region. Saudi Arabia, a key market player, generated approximately 401.6 TWh of electricity in 2022, highlighting the robust energy demand in the region. The growing focus on industrial diversification, particularly in Gulf Cooperation Council (GCC) countries, has led to increased investments in power infrastructure development. Major utilities are undertaking substantial grid modernization initiatives, with companies like Saudi Electricity Company (SEC) announcing investments worth SAR 500 billion by 2030 for building electricity transmission networks.

The market is witnessing a notable shift towards grid modernization and smart infrastructure development. In December 2023, ENOWA, NEOM's utility subsidiary, announced the development of a blueprint for the world's first high-voltage renewable smart transformer grid, demonstrating the region's commitment to advanced power infrastructure. This transformation is further evidenced by significant contract awards, such as HD Hyundai Electric securing a USD 72.3 million contract in November 2023 for Saudi Arabian city development, focusing on power equipment supply including transformers and high-voltage circuit breakers.

The industry is experiencing increased localization efforts and strategic partnerships to strengthen domestic manufacturing capabilities. In July 2023, Saudi Power Transformers, a subsidiary of Electrical Industries Company, secured a significant USD 41 million contract with Saudi Aramco for transformer supply, reinforcing the trend toward local production. The transmission infrastructure development is gaining momentum, with South Africa's ambitious plans requiring the addition of 14,000 kilometers of extra-high voltage lines and 170 transformers to accommodate 105,865 MVA of transformer capacity over the next decade.

The market is characterized by substantial investments in power distribution infrastructure and cross-border interconnection projects. In December 2023, Larsen & Toubro Construction secured a major order for power distribution projects in the Middle East, encompassing the engineering, supply, and commissioning of substations with distribution transformers and monitoring systems. The region is also witnessing increased focus on grid reliability and efficiency improvements, with utilities implementing advanced monitoring and control systems. These developments are complemented by strategic initiatives to enhance power distribution networks, particularly in rapidly growing urban areas and industrial zones.

Middle East And Africa Transformer Market Trends

Increasing Integration of Renewable Energy Generation

The Middle East & African renewable energy market is experiencing significant growth driven by ambitious government targets and declining costs of renewable power generation. According to the Energy Institute Statistical Review of World Energy 2023, renewables contributed around 11% to the global power generation mix in 2022, with continued growth expected as countries focus on reducing carbon emissions and achieving net-zero targets. The integration of renewable energy sources, particularly solar and wind power, requires substantial upgrades to existing transmission and distribution infrastructure, creating increased demand for transformers. This is evidenced by major recent developments such as Saudi Arabia's target to install 58.7 GW of renewable energy capacity by 2030 and the UAE's goal to increase clean energy capacity from 3.7 GW to 14.2 GW by 2030.

The region has witnessed significant investments in renewable energy infrastructure throughout 2023, demonstrating a strong commitment to grid modernization. In October 2023, the Saudi Electricity Company (SEC) secured a USD 3 billion international facility agreement focused on building smart grids and integrating renewable energy projects. Additionally, in May 2023, Hitachi Energy signed agreements with ENOWA and the Saudi Electricity Company for three high-voltage direct current (HVDC) transmission systems with a total power capacity of up to 9 GW, along with capacity reservations for two additional HVDC projects rated up to 3 GW each. These investments are complemented by the region's vast renewable potential, with Saudi Arabia alone possessing an offshore wind technical potential of 106 GW and about 78 GW of floating offshore wind energy potential, according to the Global Wind Energy Council. The integration of such large-scale renewable projects necessitates advanced transformer infrastructure to ensure efficient power transmission and distribution. The demand for power transformers and voltage transformers is expected to rise significantly as these projects progress, highlighting the critical role of electrical transformers in the region's energy transition.

Understand The Key Trends Shaping This Market

Download PDF

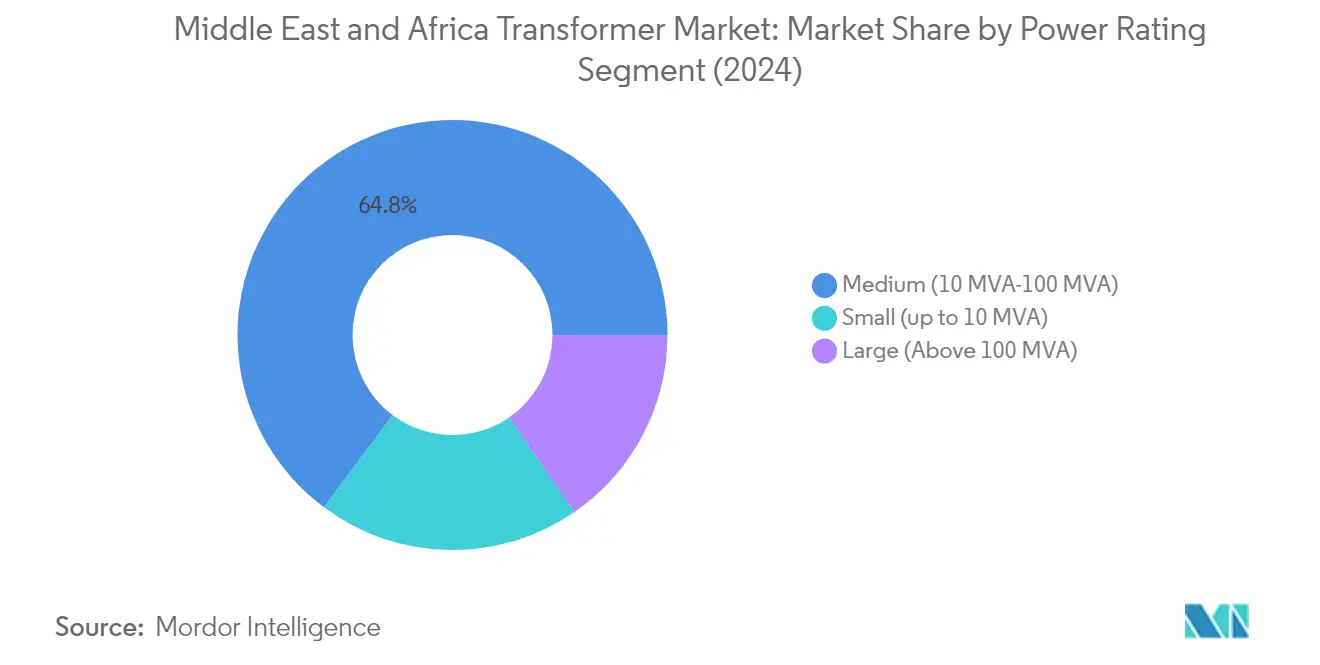

Segment Analysis: Power Rating

Medium Power Rating Segment in Middle East and Africa Transformer Market

The medium power rating segment (10 MVA-100 MVA) dominates the Middle East and Africa transformer market, commanding approximately 65% market share in 2024, while also exhibiting the strongest growth trajectory with a projected growth rate of around 4% from 2024-2029. This segment's prominence is driven by its widespread application in various industrial sectors, power distribution networks, and renewable energy integration projects across the region. The segment's robust performance is supported by significant investments in transmission and distribution infrastructure upgrades, particularly in countries like Saudi Arabia, UAE, and Egypt. Recent developments include major projects such as the NEOM smart city initiative in Saudi Arabia and Dubai's comprehensive grid modernization programs, which heavily utilize medium-rated transformers. The versatility of medium voltage transformers in handling both utility-scale power distribution and large industrial applications makes them essential components in the region's expanding energy infrastructure.

Large Power Rating Segment in Middle East and Africa Transformer Market

The large power rating segment (above 100 MVA) demonstrates significant growth potential in the Middle East and Africa transformer market, with a projected growth rate of approximately 4% from 2024-2029. This growth is primarily driven by increasing investments in high-voltage transmission infrastructure and large-scale power generation projects across the region. The segment's expansion is supported by major utility-scale renewable energy projects, particularly in Saudi Arabia and the UAE, where large power transformers are crucial for grid integration. Recent developments include the Saudi-Egypt interconnector project and various HVDC transmission initiatives that require high-capacity transformers. The segment's growth is further bolstered by the region's focus on grid reliability improvement and cross-border power exchange projects, which necessitate the deployment of large power transformers for efficient power transmission over long distances.

Small Power Rating Segment in Middle East and Africa Transformer Market

The small power rating segment (up to 10 MVA) plays a vital role in the Middle East and Africa transformer market, particularly in distribution networks and commercial applications. This segment is essential for last-mile power distribution and serves various sectors including residential complexes, commercial buildings, and small industrial facilities. The segment's significance is particularly evident in urban development projects and rural electrification initiatives across the region. Small power transformers are crucial components in the region's efforts to improve power access in remote areas and support the growing demand from commercial and residential sectors. The segment's development is closely tied to urbanization trends and the increasing focus on improving power distribution efficiency in both developed and emerging areas across the Middle East and Africa.

Segment Analysis: By Cooling Type

Oil-Cooled Segment in Middle East and Africa Transformer Market

The oil-filled transformer segment dominates the Middle East and Africa transformer market, accounting for approximately 87% market share in 2024. This significant market position is driven by the segment's superior cooling capabilities and suitability for high-capacity applications, particularly in power generation and transmission infrastructure. Oil-filled transformers are extensively deployed in outdoor spaces and oversized electrical loads, making them ideal for the region's growing power infrastructure needs. The segment is also witnessing strong growth momentum, expected to expand at around 4% from 2024-2029, supported by increasing investments in power generation and transmission plants across the region. In July 2023, Saudi Power Transformers secured a notable USD 41 million contract with Aramco for supplying oil-filled transformers, demonstrating the continued demand for these transformers in major infrastructure projects. The segment's growth is further bolstered by its widespread application in distribution, power, and industrial transformers, particularly in regions experiencing rapid industrial development and grid modernization initiatives.

Air-Cooled Segment in Middle East and Africa Transformer Market

The air-cooled transformer segment is experiencing steady growth in the Middle East and Africa transformer market, with a projected growth rate of approximately 3.4% from 2024-2029. This growth is primarily driven by the increasing demand for transformers in commercial and residential applications, where air-cooled transformers offer advantages such as lower maintenance requirements and environmental friendliness. The segment's expansion is supported by the rising adoption in various applications, including high-rise buildings, airports, stadiums, hotels, shopping malls, chemical and refinery plants, and residential complexes. In April 2023, the Saudi Transformer Company collaborated with Crompton Greaves to manufacture the latest technological innovations in transformers, including air-cooled variants, demonstrating the industry's commitment to advancing this technology. The segment's growth is further enhanced by its suitability for indoor installations and areas where environmental considerations are paramount, making it an increasingly attractive option for urban development projects across the region.

Segment Analysis: By Transformer Type

Power Transformer Segment in Middle East and Africa Transformer Market

Power transformers dominate the Middle East and Africa transformer market, accounting for approximately 73% of the total market value in 2024. These transformers play a crucial role in the region's power infrastructure, primarily handling high voltage transmission and being essential components in power generation facilities, transmission substations, and large industrial applications. The segment's prominence is driven by massive investments in power generation projects, particularly in countries like Saudi Arabia and the United Arab Emirates, along with the increasing integration of renewable energy sources into the grid. The segment is expected to maintain its strong growth trajectory, with a projected growth rate of around 4% from 2024 to 2029, supported by ongoing infrastructure development projects and grid modernization initiatives across the region. The growth is further bolstered by the rising demand for electricity, expansion of transmission networks, and the need to replace aging infrastructure. Additionally, the implementation of smart grid technologies and the development of cross-border power interconnection projects are creating substantial opportunities for power transformer deployments in the region.

Distribution Transformer Segment in Middle East and Africa Transformer Market

The distribution transformer segment serves as a critical component in the Middle East and Africa's power distribution network, facilitating the final voltage transformation in the power distribution system. These transformers are essential for stepping down voltage to levels suitable for commercial, residential, and small industrial applications. The segment is witnessing steady growth driven by increasing urbanization, rural electrification initiatives, and the expansion of distribution networks across the region. Distribution transformers are particularly crucial in supporting the region's growing focus on renewable energy integration at the distribution level, especially for solar rooftop installations and small-scale renewable projects. The segment's growth is further supported by government initiatives to improve electricity access in remote areas, modernization of existing distribution infrastructure, and the implementation of smart grid technologies at the distribution level. The increasing adoption of energy-efficient distribution transformers, coupled with stringent energy efficiency regulations, is also contributing to the segment's development in the region.

Middle East And Africa Transformer Market Geography Segment Analysis

Transformer Market in Saudi Arabia

Saudi Arabia dominates the Middle East and Africa transformer market, commanding approximately 35% market share in 2024, while also demonstrating the region's strongest growth trajectory with a projected CAGR of nearly 5% from 2024-2029. The country's ambitious Vision 2030 initiative has been a key driver, focusing on diversifying the economy and modernizing infrastructure. The Saudi Electricity Company (SEC) is spearheading massive investments in grid infrastructure, with particular emphasis on smart grid technologies and renewable energy integration. The development of mega-projects like NEOM city and the Red Sea Project has created substantial demand for both power transformers and distribution transformers. Additionally, the country's push towards renewable energy, aiming to generate 50% of its electricity from renewable sources by 2030, has necessitated significant transformer infrastructure upgrades to handle the integration of these new power sources into the existing grid.

Transformer Market in United Arab Emirates

The United Arab Emirates has established itself as a crucial market for transformers in the Middle East and Africa region, driven by its aggressive infrastructure development and smart city initiatives. The country's power sector is undergoing a significant transformation with the implementation of advanced grid technologies and renewable energy projects. Dubai's ambitious plans, including the Mohammed bin Rashid Al Maktoum Solar Park and various smart city initiatives, have created substantial demand for advanced transformer solutions. The UAE's commitment to energy diversification and sustainability has led to increased investments in grid infrastructure modernization. The country's focus on developing nuclear power capabilities, alongside its renewable energy targets, has further amplified the need for sophisticated electrical transformer systems. Additionally, rapid urbanization and the development of new economic zones have necessitated extensive power distribution networks, driving demand for various types of transformers.

Transformer Market in Egypt

Egypt's transformer market has emerged as a vital component of the country's ambitious power sector development plans. The nation's strategic position as a regional energy hub has driven significant investments in its electricity infrastructure. Egypt's commitment to modernizing its power grid and increasing its renewable energy capacity has created substantial opportunities in the transformer sector. The country's efforts to upgrade and interconnect its national grid with regional neighbors, particularly through projects aimed at developing a unified national grid connecting Arab countries, Africa, and Europe, have boosted transformer demand. The government's focus on industrial development and urban expansion projects has further accelerated the need for reliable power distribution infrastructure. Additionally, Egypt's growing emphasis on renewable energy integration and smart grid technologies has created new requirements for advanced transformer solutions, particularly in areas designated for solar and wind power projects.

Transformer Market in Other Countries

The transformer market in other Middle East and African countries presents a diverse landscape of opportunities and challenges. Countries like Qatar and Kuwait are focusing on diversifying their energy infrastructure beyond traditional fossil fuels, while nations such as Nigeria and South Africa are working to address power reliability issues and expand their grid coverage. Iran's significant investments in renewable energy infrastructure and grid modernization have created new demands for transformer technologies. Countries in North Africa, including Libya and Tunisia, are gradually rebuilding and modernizing their power infrastructure. The region also includes emerging markets in East Africa, such as Kenya and Ethiopia, where rapid urbanization and industrialization are driving the need for expanded power distribution networks. These markets are characterized by varying levels of infrastructure development, regulatory frameworks, and investment priorities, creating a complex but potentially rewarding market landscape for transformer manufacturers and suppliers.

Get Analysis on Important Geographic Markets

Download PDF

Middle East And Africa Transformer Industry Overview

Top Companies in Middle East and Africa Transformer Market

The Middle East and Africa transformer market features prominent global players like Siemens AG, General Electric, Schneider Electric SE, Hitachi Energy, and Toshiba Corporation alongside regional manufacturers. These companies are driving innovation through the development of smart transformers and grid solutions tailored for renewable energy integration. Operational agility is demonstrated through localized manufacturing facilities, particularly in Saudi Arabia and the UAE, enabling faster response to market demands and reduced logistics costs. Strategic partnerships with state-owned utilities and energy companies have become increasingly common, as evidenced by collaborations with entities like the Saudi Electricity Company and the Egyptian Electricity Transmission Company. Market leaders are expanding their presence through investments in service centers, project sites, and R&D facilities across the region, while also focusing on developing environmentally sustainable transformer solutions.

Fragmented Market with Strong Global Presence

The transformer market in the Middle East and Africa exhibits a moderately fragmented structure, characterized by the presence of both multinational corporations and local manufacturers. Global conglomerates leverage their technological expertise and extensive R&D capabilities to maintain market leadership, while local players compete through their understanding of regional requirements and established distribution networks. The market has witnessed significant consolidation through strategic agreements and joint ventures, particularly in key markets like Saudi Arabia and the UAE.

Recent market developments indicate an increasing trend toward the localization of manufacturing capabilities, with global players establishing production facilities in strategic locations across the region. Mergers and acquisitions activity has been notably focused on enhancing technological capabilities and expanding geographical presence, with particular emphasis on smart grid technologies and renewable energy integration solutions. The competitive dynamics are further shaped by the strong presence of Asian manufacturers, particularly from South Korea and Japan, who have established significant market share through competitive pricing and reliable product offerings.

Innovation and Localization Drive Market Success

For established players to maintain and expand their market share, a focus on technological innovation, particularly in smart transformers and grid solutions, has become crucial. Companies are increasingly investing in research and development to develop products that align with the region's growing renewable energy sector and smart grid initiatives. The ability to offer comprehensive solutions, including installation, maintenance, and after-sales services, while maintaining strong relationships with key stakeholders like government utilities and private sector clients, has emerged as a critical success factor.

New entrants and challenger companies can gain ground by focusing on specific market segments or geographical areas where they can build expertise and reputation. The relatively high buyer concentration, particularly with state-owned utilities being major customers, necessitates strong relationship building and local presence. While the threat of substitution remains low due to the essential nature of transformers in power infrastructure, regulatory requirements regarding energy efficiency and environmental standards are becoming increasingly stringent, requiring companies to adapt their product offerings accordingly. Success in this market increasingly depends on the ability to provide customized solutions while maintaining cost competitiveness and meeting local content requirements.

Middle East And Africa Transformer Market Leaders

-

Siemens AG

-

General Electric Company

-

Toshiba Corporation

-

Eaton Corporation Plc

-

HD HYUNDAI ELECTRIC CO. LTD.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Middle East And Africa Transformer Market News

- December 2023: The power and distribution business of Larsen & Toubro (L&T) Construction had secured an order for its power and distribution vertical in the Middle East region. The order is for engineering, supply, construction, installation, testing, and commissioning of a substation that includes a transformer, reactor, substation control, and monitoring systems in the United Arab Emirates.

- November 2023: HD Hyundai Electric Co., a subsidiary of South Korea’s HD Hyundai Co., made a deal worth USD 72.3 million for Saudi Arabian City development. The deal involves providing crucial power equipment for city development projects near Diriyah, Saudi Arabia. The components supplied are power transformers, high-voltage circuit breakers, and reactors, amongst others.

Middle East And Africa Transformer Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Global Inclination towards Renewable-based Power Generation

- 4.5.1.2 Growing Power Demand in Line with the Increasing Population

- 4.5.2 Restraints

- 4.5.2.1 High Initial Cost

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Power Rating

- 5.1.1 Large

- 5.1.2 Medium

- 5.1.3 Small

-

5.2 Cooling Type

- 5.2.1 Air-Cooled

- 5.2.2 Oil-Cooled

-

5.3 Transformer Type

- 5.3.1 Power Transformer

- 5.3.2 Distribution Transformer

-

5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Egypt

- 5.4.4 Nigeria

- 5.4.5 Qatar

- 5.4.6 South Africa

- 5.4.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Eaton Corporation Plc

- 6.3.2 Siemens AG

- 6.3.3 General Electric Company

- 6.3.4 Toshiba Corporation

- 6.3.5 Schneider Electric SE

- 6.3.6 HD HYUNDAI ELECTRIC CO. LTD.

- 6.3.7 Hyosung Heavy Industries Corporation

- 6.3.8 Bharat Heavy Electricals Limited

- 6.3.9 Mitsubishi Electric Corporation

- 6.3.10 Hitachi Energy Ltd.

- *List Not Exhaustive

- 6.4 Market Ranking/Share (%) Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Innovations like Smart Transformers

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Middle East And Africa Transformer Industry Segmentation

A transformer is a device that transfers electric energy from one alternating-current circuit to one or more other circuits, either increasing (stepping up) or reducing (stepping down) the voltage. Transformers are employed for widely varying purposes. They reduce the voltage of conventional power circuits and operate low-voltage devices, such as doorbells and toy electric trains. They also help raise the voltage from electric generators so that electric power can be transmitted over long distances.

The Middle-East and Africa transformer market is segmented by power rating, cooling type, transformer type, and geography. By power rating, the market is segmented into large, medium, and small. By cooling type, the market is segmented into air-cooled and oil-cooled. By transformer type, the market is segmented into power transformer and distribution transformer. The report also covers the market size and forecasts for the transformer market across major countries in the Middle East and African region. For each segment, the market sizing and forecasts are done based on revenue.

| Power Rating | Large |

| Medium | |

| Small | |

| Cooling Type | Air-Cooled |

| Oil-Cooled | |

| Transformer Type | Power Transformer |

| Distribution Transformer | |

| Geography | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Nigeria | |

| Qatar | |

| South Africa | |

| Rest of Middle-East and Africa |

Need A Different Region or Segment?

Customize Now

Middle East And Africa Transformer Market Research FAQs

How big is the Middle East And Africa Transformer Market?

The Middle East And Africa Transformer Market size is expected to reach USD 4.03 billion in 2025 and grow at a CAGR of 3.9% to reach USD 4.88 billion by 2030.

What is the current Middle East And Africa Transformer Market size?

In 2025, the Middle East And Africa Transformer Market size is expected to reach USD 4.03 billion.

Who are the key players in Middle East And Africa Transformer Market?

Siemens AG, General Electric Company, Toshiba Corporation, Eaton Corporation Plc and HD HYUNDAI ELECTRIC CO. LTD. are the major companies operating in the Middle East And Africa Transformer Market.

What years does this Middle East And Africa Transformer Market cover, and what was the market size in 2024?

In 2024, the Middle East And Africa Transformer Market size was estimated at USD 3.87 billion. The report covers the Middle East And Africa Transformer Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Middle East And Africa Transformer Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Middle East And Africa Transformer Market Research

Mordor Intelligence provides a comprehensive analysis of the transformer industry. With decades of expertise in electrical transformer market research, our detailed report covers a wide range of technologies. These include power transformer systems and specialized current transformer applications. The analysis encompasses various types, such as step up transformer, step down transformer, and isolation transformer technologies. Additionally, it explores three phase transformer and single phase transformer configurations. The report also examines instrument transformer and potential transformer developments, focusing on distribution transformer and voltage transformer innovations.

Stakeholders gain valuable insights into autotransformer and toroidal transformer segments. The report offers detailed analysis of high voltage transformer, medium voltage transformer, and low voltage transformer markets. The report PDF, available for download, provides comprehensive coverage of dry type transformer and industrial transformer applications, including oil filled transformer technologies. The analysis extends to emerging traction transformer systems, smart transformer innovations, and grid transformer infrastructure. It also addresses power electronics transformer developments. This extensive research enables businesses to make informed decisions across the entire transformer value chain.