Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

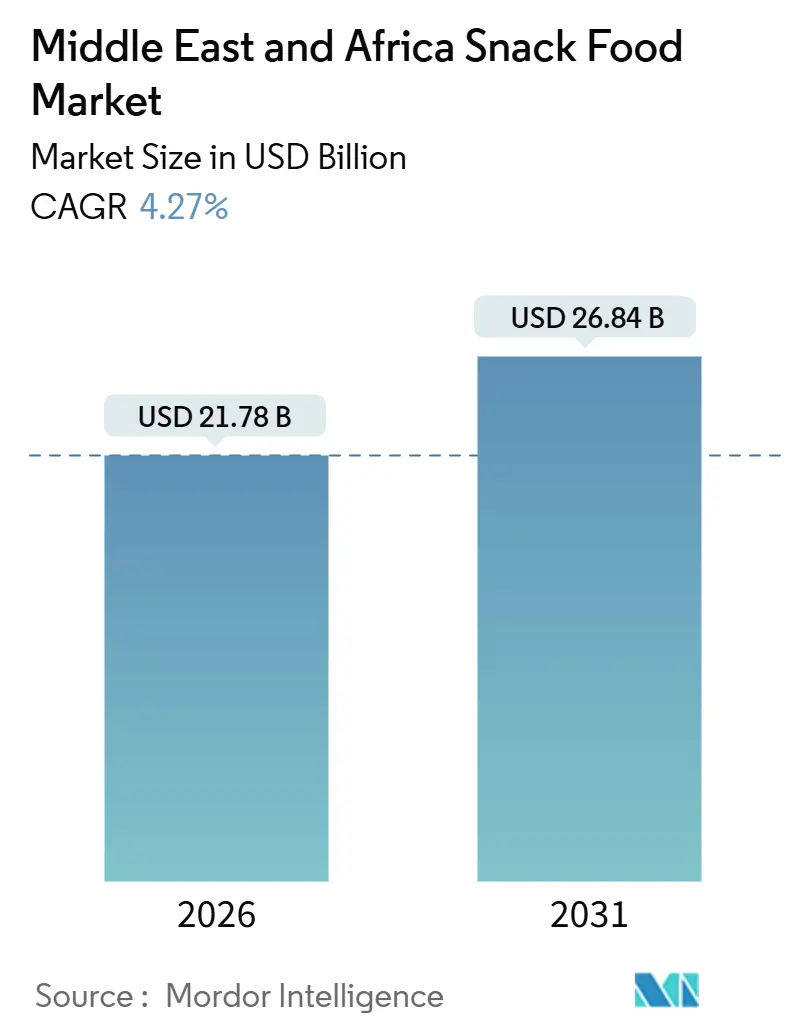

| Market Size (2026) | USD 21.78 Billion |

| Market Size (2031) | USD 26.84 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

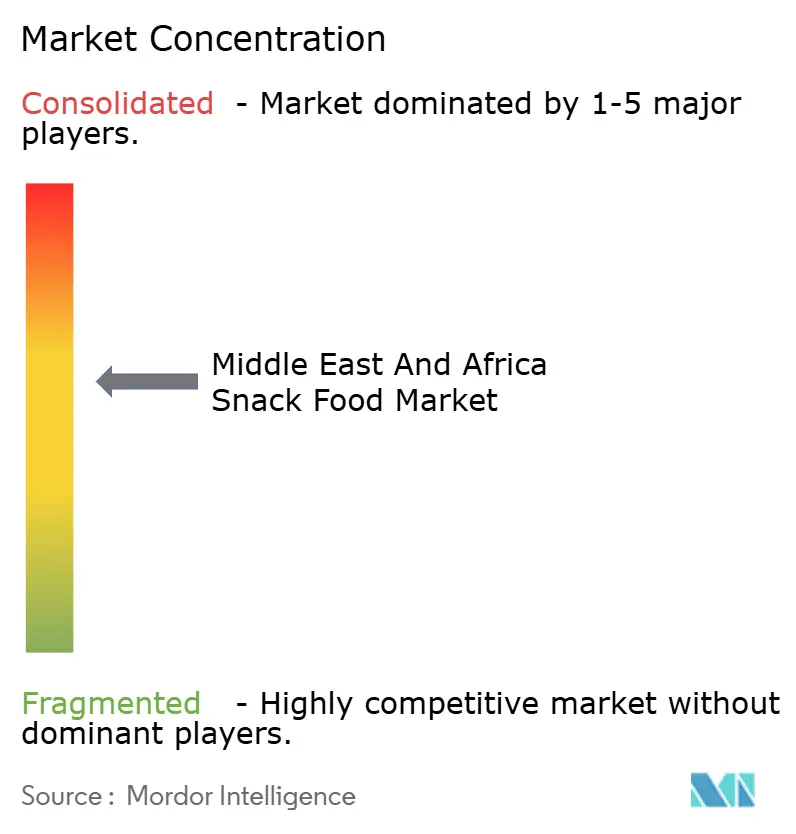

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Snack Food Market Analysis by Mordor Intelligence

The Middle East and Africa snack food market was valued at USD 21.78 billion in 2026 and is expected to reach USD 26.84 billion by 2031, registering a Compound Annual Growth Rate (CAGR) of 4.27%. Factors such as increasing urban populations, stricter labeling regulations, and continuous flavor innovation are driving growth in volumes while reshaping product portfolios. In 2025, Saudi Arabia was the largest national market; however, growth is increasingly shifting toward the United Arab Emirates, South Africa, and select North African economies, which are adopting plant-based ingredients and premium product positioning. Shelf-life requirements, influenced by high ambient temperatures, are leading to a transition in packaging toward aluminum cans and recyclable mono-material films. Additionally, investments under Saudi Arabia's Vision 2030 initiative are strengthening local manufacturing capabilities, reducing supply chain lengths, and lowering reliance on imports. At the same time, regulatory front-of-pack labeling that highlights excess sodium and saturated fat is encouraging reformulation of traditional product lines. This is creating opportunities for protein-rich meat snacks, organic products, and functional snack extensions that appeal to health-conscious consumers.

Key Report Takeaways

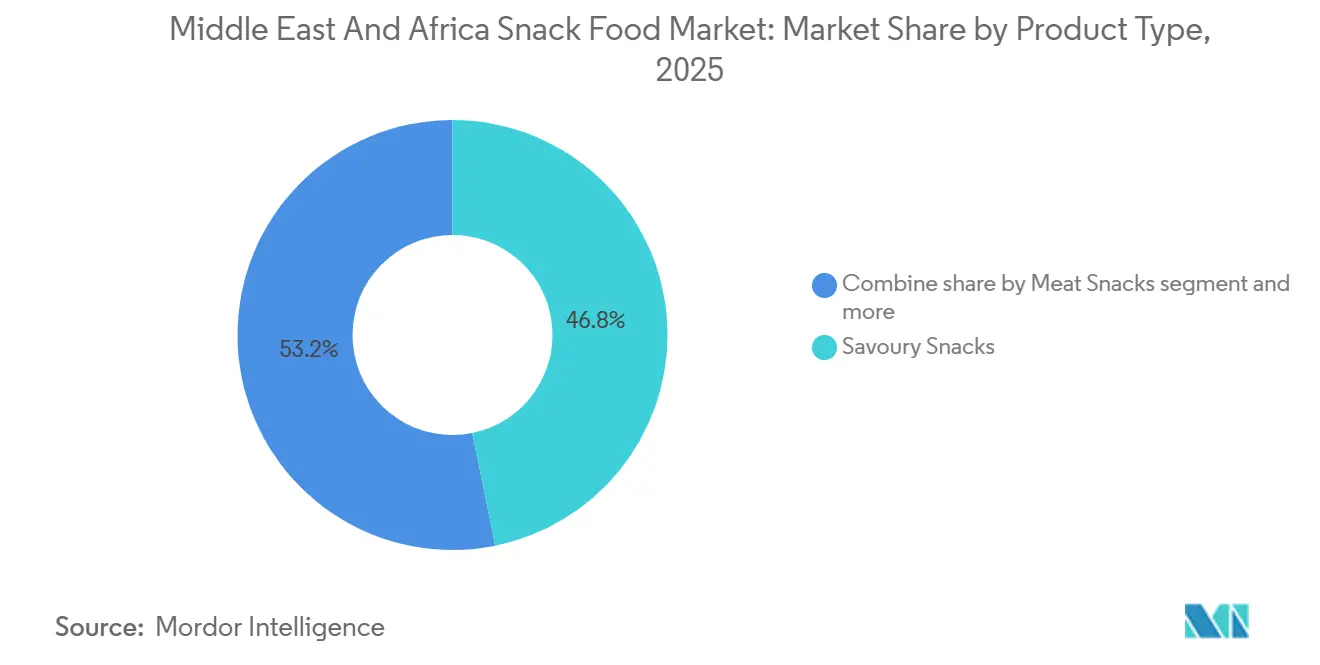

- By product type, savoury snacks led with 46.82% of volume in 2025, while meat snacks are projected to expand at a 5.08% CAGR through 2031.

- By ingredient type, conventional formulations retained 60.74% of value in 2025, yet organic and clean-label variants are advancing at a 4.87% CAGR to 2031.

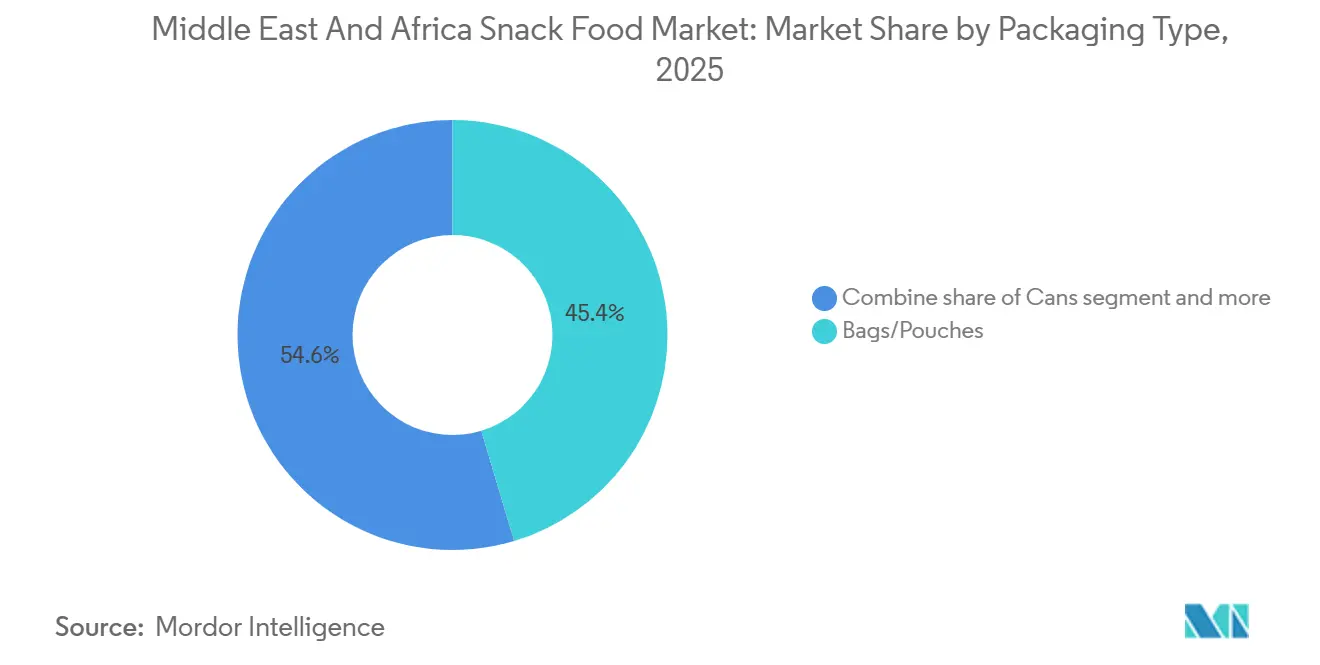

- By packaging type, bags and pouches dominated with 45.37% share in 2025, but cans are on track for the quickest rise at a 5.22% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 35.37% of sales in 2025, whereas online retail is set to climb at a 5.13% CAGR to 2031.

- By geography, Saudi Arabia held 27.44% of the Middle East and Africa snack food market share in 2025, whereas the United Arab Emirates is forecast to post the fastest growth at a 5.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Snack Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busier lifestyles and on-the-go consumption | +0.9% | Gulf Cooperation Council core, spillover to urban North Africa | Medium term (2-4 years) |

| Growth of plant-based and alternative-ingredient snacks | +0.6% | United Arab Emirates, Saudi Arabia, South Africa | Long term (≥ 4 years) |

| Portability and convenient packaging formats | +0.7% | Global, with early gains in Saudi Arabia, United Arab Emirates, Turkey | Short term (≤ 2 years) |

| Reinvention of traditional and local flavours in modern formats | +0.5% | Gulf Cooperation Council, Turkey, North Africa | Medium term (2-4 years) |

| Rising health and wellness awareness favouring better-for-you snacks | +0.8% | United Arab Emirates, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Shift from loose/unpackaged to branded packaged snacks | +0.7% | Sub-Saharan Africa, North Africa, with concentration in South Africa, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Busier lifestyles and on-the-go consumption

Urbanization rates in Gulf Cooperation Council (GCC) countries exceeded 85% in 2025, reshaping traditional meal patterns and increasing demand for grab-and-go options suited to commuting and workplace routines. In Saudi Arabia, women's labor-force participation reached 35.6% in 2024, marking a 10-percentage-point rise since 2020 and contributing to the growth of dual-income households that prioritize convenience over home-cooked meals. The United Arab Emirates (UAE) reported 4.2 snack occasions per capita per day in 2025, up from 2.8 in 2020, driven by extended working hours and traffic congestion in cities like Dubai and Abu Dhabi, which encourage consumers to opt for portable nutrition solutions. According to PwC's Middle East Consumer Survey 2025, 62% of respondents in Saudi Arabia and the UAE identified time scarcity as the primary factor influencing snack purchases, surpassing considerations of taste or price. This shift in consumer behavior is leading brands to focus on single-serve packaging and resealable formats tailored to mobile consumption, while retailers are expanding checkout-aisle assortments to capture impulse purchases during peak commuting periods.

Growth of plant-based and alternative-ingredient snacks

Plant-based snack launches in the Middle East saw a year-over-year increase in 2025, with the United Arab Emirates contributing a growing percentage of new stock-keeping units (SKUs), according to data from retail audits. Products such as chickpea puffs, lentil crisps, and fava-bean chips are replacing conventional potato-based snacks in premium segments. This shift is largely driven by the rise of flexitarian diets, which aim to reduce meat consumption without requiring its complete elimination. The clean-label ingredients market in the Middle East and Africa is expanding at a growth rate of 7.34 percent, as consumers increasingly scrutinize ingredient lists for artificial additives and demand greater transparency in sourcing. In March 2025, Nestlé introduced a date-and-oat bar in Saudi Arabia, utilizing locally sourced dates to align with heritage preferences while meeting clean-label standards. South Africa's plant-based protein market experienced growth in 2024, with biltong producers launching mushroom-based jerky alternatives to cater to vegan and vegetarian consumers. This diversification of ingredients is reshaping supply chains, as brands establish direct partnerships with pulse farmers in Turkey and legume processors in Egypt to secure non-genetically modified organism (non-GMO), organic inputs that command premium prices.

Portability and convenient packaging formats

Single-serve and resealable packaging formats accounted for a significant share of new snack launches in the Gulf Cooperation Council in 2025, highlighting a strategic focus on portion control and convenience for on-the-go consumption. In January 2025, Almarai introduced a cheese-cracker combo pack designed to fit car cup holders and backpack side pockets, catering to commuters and school-age children. According to Tetra Pak's research in the Middle East, a majority of consumers associate resealable packaging with freshness and value, prompting brands to adopt zip-lock closures and peel-and-reseal films, despite a notable cost premium compared to traditional pillow packs. The trend toward portability is further reflected in vending-machine placements, which saw a significant increase across Saudi Arabia's metro stations and corporate campuses in 2024, offering ambient-stable snacks in compact formats. Additionally, Saudi Basic Industries Corporation's collaboration with regional converters to develop mono-material polypropylene films supports recyclable packaging that complies with Emirates Authority for Standardization and Metrology sustainability guidelines while maintaining the barrier properties necessary for extended shelf life in high-humidity environments.

Reinvention of traditional and local flavours in modern formats

Za'atar-seasoned chips, halloumi-flavored crisps, and date-filled bars are transitioning from artisanal bakeries to supermarket shelves, supported by Halal certification that enables cross-border distribution within the Gulf Cooperation Council. PepsiCo's Lay's brand introduced a za'atar variant in the United Arab Emirates, capturing market share in the premium savory segment within a few months, according to Nielsen retail tracking. Turkish snack manufacturers are exporting simit-inspired crackers and Turkish delight-infused confections to Gulf markets, leveraging cultural affinity and nostalgia among expatriate communities. Edita Food Industries launched a manakish-flavored puff in Egypt, combining thyme, sesame, and sumac in a baked format that appeals to health-conscious consumers seeking traditional flavors without deep-frying. This flavor localization strategy is gaining traction in markets where global brands previously dominated with universally positioned products, as regional players utilize culinary heritage to differentiate and build loyalty among domestic consumers who value authenticity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health concerns over salt, sugar, fat, and additives | -0.6% | Gulf Cooperation Council, South Africa | Short term (≤ 2 years) |

| Stringent and evolving food-safety and labelling regulations | -0.5% | Saudi Arabia, United Arab Emirates, Turkey | Medium term (2-4 years) |

| Supply-chain and logistics constraints in remote areas | -0.4% | Sub-Saharan Africa, North Africa interior | Long term (≥ 4 years) |

| Political instability and trade barriers in certain countries | -0.3% | Sudan, Yemen, Libya, with spillover to Egypt, Turkey | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health concerns over salt, sugar, fat, and additives

Public health campaigns addressing non-communicable diseases have increased scrutiny on snack formulations, with Gulf Cooperation Council (GCC) governments highlighting the link between high sodium and trans-fat consumption and the growing prevalence of obesity and diabetes. According to the Saudi Food and Drug Authority, over one-third of adults in Saudi Arabia are classified as obese. In response, front-of-pack warning labels were introduced in the year 2024 to identify products exceeding specified thresholds for sodium, sugar, and saturated fat [1]Source: Saudi Food and Drug Authority, “Front-of-Pack Nutrition Warning Labels,” sfda.gov.sa. This regulatory measure has led to the reformulation of a significant portion of savoury snack portfolios, as brands aim to avoid red octagon warnings that may deter health-conscious consumers. For instance, Nestlé reduced the sugar content in its KitKat bars sold in the United Arab Emirates by a notable percentage in the year 2024, replacing sucrose with stevia and erythritol blends to maintain sweetness without adding calories. However, reformulation efforts have increased costs and required adjustments to taste profiles, delaying product launches and compressing profit margins as companies strive to meet nutritional standards while maintaining consumer appeal. Additionally, the shift toward cleaner labels has revealed supply chain challenges, as natural preservatives and non-hydrogenated oils are more expensive and require cold-chain logistics, increasing distribution costs significantly in high-temperature regions.

Stringent and evolving food-safety and labelling regulations

Regulatory fragmentation across the Middle East and Africa is creating challenges for product launches and increasing compliance costs, as brands face varying standards for labeling, ingredient approvals, and shelf-life testing. The Saudi Food and Drug Authority requires Arabic-language nutrition panels and Halal certification for all packaged foods, while the Emirates Authority for Standardization and Metrology mandates third-party testing for microbiological contaminants and heavy metals [2]Source: International Trade Administration, “Labeling/Marking Requirements,” trade.gov. In the year 2024, Turkey's Ministry of Agriculture and Forestry introduced new allergen-labeling requirements, necessitating packaging redesigns for products containing sesame, tree nuts, and sulfites. These regulatory changes are delaying time-to-market by several months, as companies undertake stability studies and reformulate products to meet local requirements. Additionally, South Africa's Department of Health implemented sodium reduction targets in the same year, limiting salt content in savory snacks to a specific threshold, which led to a significant percentage of legacy products being removed from shelves. Compliance costs, including legal reviews, laboratory testing, and packaging redesigns, range from fifty thousand to one hundred fifty thousand United States dollars per stock-keeping unit, posing significant challenges for small and medium-sized enterprises that lack the scale to distribute regulatory costs across multiple markets.

Segment Analysis

By Product Type: Meat Snacks Outpace Traditional Categories

Meat snacks are expected to grow at a rate of 5.08% through 2031, marking the fastest growth among product types. This growth is driven by the increasing popularity of high-protein diets and the adoption of ketogenic dietary habits, which are fueling demand for products such as biltong, jerky, and droëwors. In 2024, South Africa's biltong exports to the Middle East increased by 14%, with the United Arab Emirates and Saudi Arabia accounting for 60% of these shipments, according to data from the South African Meat Industry Company.

Savoury snacks accounted for 46.82% of the market in 2025, led by products like potato chips, extruded puffs, and crackers, which benefit from well-established distribution networks and strong brand loyalty. However, growth in this segment is slowing as health concerns related to sodium and trans fats drive reformulation efforts and regulatory labeling requirements. Confectionery snacks, including chocolate bars and gummy candies, are facing margin pressures due to cocoa price volatility, which rose by 40% in 2024 following supply disruptions in West Africa. Bakery snacks, such as biscuits and cookies, continue to perform well in North Africa and Turkey, where tea-time traditions support steady per-capita consumption. Fruit snacks are gaining popularity in the United Arab Emirates, with date-based bars and dried-fruit mixes aligning with clean-label preferences. Additionally, frozen snacks, such as samosas and spring rolls, are expanding in urban Gulf markets, supported by home freezer penetration exceeding 75%, which facilitates bulk purchases and extended storage.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ingredient Type: Clean-Label Gains Momentum

Organic and clean-label snacks are anticipated to grow at a compound annual growth rate (CAGR) of 4.87% through 2031, surpassing the growth of conventional formulations, which accounted for 60.74% of the market in 2025. The clean-label ingredients market in the Middle East and Africa is expanding at a CAGR of 7.34%, driven by increasing consumer demand for transparency and naturally sourced products. While conventional snacks continue to dominate due to cost advantages and established supply chains, reformulation efforts are gradually reducing their market share as brands replace synthetic additives with natural alternatives.

In November 2024, Mondelez introduced a clean-label Oreo variant in Saudi Arabia, replacing artificial vanillin with vanilla extract and removing high-fructose corn syrup. This reformulation increased input costs by 8% but improved brand perception among health-conscious millennial consumers. Organic certification frameworks, such as European Union (EU) Organic and United States Department of Agriculture (USDA) Organic, are gaining traction in Gulf Cooperation Council (GCC) markets. Imported organic snacks from Europe and North America occupy shelf space in premium retailers like Waitrose and Spinneys. However, local organic production remains limited, with Turkey and South Africa accounting for 85% of the region's organic farmland. Investment in organic pulse cultivation is increasing as brands aim to localize supply chains and reduce reliance on imports.

By Packaging Type: Cans Surge on Sustainability Push

The cans packaging market is expected to grow at a rate of 5.22% through 2031, making it the fastest-growing packaging type. This growth is primarily driven by brands addressing sustainability requirements and the need for extended shelf life in regions with high-temperature climates. In 2025, bags and pouches accounted for 45.37% of the packaging market, supported by their cost efficiency and design flexibility. However, environmental concerns about single-use plastics have led to regulatory measures. The Emirates Authority for Standardization and Metrology (ESMA) introduced recyclability targets in 2024, requiring 50% of snack packaging to be recyclable or compostable by 2027. These regulations favor the use of aluminum cans and mono-material films over multi-layer laminates.

In March 2025, PepsiCo introduced a canned potato-chip line in the United Arab Emirates, presenting the format as both premium and environmentally friendly. This approach helped the company secure a 12% market share in the premium segment within six months. Cans provide extended shelf life and superior barrier properties, which are essential in Gulf markets where ambient temperatures often exceed 40 degrees Celsius for extended periods. However, higher unit costs and weight constraints limit their adoption in value-focused segments. Meanwhile, bags and pouches remain the preferred choice in North Africa and sub-Saharan Africa, where price sensitivity and informal distribution networks make lightweight, flexible packaging a more practical and cost-effective option.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Retail Accelerates

Online retail is projected to grow at a rate of 5.13% through 2031, making it the fastest-growing distribution channel. This growth is fueled by the increasing use of mobile commerce and the adoption of digital payment systems, which are transforming purchasing behavior in Gulf Cooperation Council (GCC) markets. Supermarkets and hypermarkets are expected to account for 35.37% of sales in 2025, driven by major chains such as Carrefour, LuLu, and Panda, which provide a wide variety of products and attractive promotional offers. At the same time, online platforms are gaining momentum, with gross merchandise value for snacks rising by 35% during Ramadan 2025 across leading Middle Eastern e-commerce platforms. Saudi Arabia's Monsha'at (General Authority for Small and Medium Enterprises) reported Q4 2024 e-commerce statistics, showing a 10% growth in active registrations and the issuance of 40,953 commercial records [3]Source: Monsha'at, “E-commerce Programs and Services,” monshaat.gov.sa.

Convenience stores are expanding in urban areas, benefiting from 24-hour operations and their proximity to residential neighborhoods, which encourage impulse purchases. However, rising rent and labor costs are putting pressure on profitability in this channel. Other distribution channels, such as vending machines and direct-to-consumer subscriptions, are gaining popularity in niche markets. For example, Almarai introduced a subscription service for cheese-based snacks in Saudi Arabia in April 2025. E-commerce growth is particularly strong in the United Arab Emirates (UAE) and Saudi Arabia, where smartphone penetration exceeds 95% and last-mile delivery infrastructure is well-developed, enabling same-day delivery in major cities. Mobile commerce accounted for over 40% of online snack purchases in 2025, supported by app-based platforms such as Noon, Talabat, and Careem Now, which integrate payment, delivery, and loyalty programs. Supermarkets are actively defending their market share through omnichannel strategies, with Carrefour and LuLu launching click and collect services that combine the convenience of online shopping with in-store pickup.

Geography Analysis

Saudi Arabia accounted for 27.44% of the market in 2025, supported by Vision 2030 initiatives aimed at increasing investment in local food manufacturing and reducing reliance on imports. The kingdom's packaged food retail market is driven by factors such as population growth, urbanization, and rising disposable incomes. High-growth categories include snack bars, fruit snacks, and savory snacks, which benefit from the expansion of modern trade and promotional activities during Ramadan and Eid. The Saudi Food and Drug Authority's (SFDA) introduction of front-of-pack warning labels in January 2024 has prompted brands to reformulate products to avoid red octagon warnings that deter health-conscious consumers. Almarai, the region's largest dairy and food company, expanded its snack portfolio in 2024 with cheese-cracker combinations and protein bars, leveraging its distribution network to achieve nationwide penetration within six months. However, supply chain challenges persist in remote provinces, where infrastructure limitations and low population density increase distribution costs and limit retail density.

The United Arab Emirates (UAE) is projected to grow at a rate of 5.01% through 2031, the fastest among the geographies analyzed. This growth is fueled by premium product positioning, a diverse expatriate population, and a mature e-commerce ecosystem. Plant-based snack launches in the UAE increased by 18% in 2025, with products such as chickpea puffs and lentil crisps gaining traction in health-conscious segments. Dubai and Abu Dhabi account for 70% of the country's snack consumption, supported by high per-capita incomes and modern trade penetration exceeding 80%. The Emirates Authority for Standardization and Metrology's (ESMA) recyclability targets are driving packaging innovation, with brands adopting aluminum cans and mono-material films to meet 2027 compliance mandates.

South Africa's snack market exhibits a clear divide between urban centers, where branded packaged snacks dominate, and rural areas, where loose, unpackaged products retain market share due to price sensitivity and limited retail infrastructure. Biltong exports to the Middle East increased by 14% in 2024, positioning South Africa as a key supplier of high-protein meat snacks. Turkey's snack market is influenced by local flavor preferences, with simit-inspired crackers and Turkish delight-infused confections gaining popularity in both domestic and export markets. In the rest of the Middle East and Africa, including countries such as Egypt, Nigeria, and Kenya, the market remains fragmented. Informal trade accounts for over 50% of the volume, but regulatory enforcement and the expansion of modern trade are gradually formalizing the market.

Competitive Landscape

The Middle East and Africa snack food market shows a moderate level of concentration, balancing the influence of multinational corporations with the specialization of regional players. Companies such as PepsiCo, Unilever, and Mondelez International utilize their global supply chains and strong brand recognition to lead the savoury and confectionery segments. At the same time, local companies like Almarai, Edita Food Industries, and Ülker build consumer loyalty through localized flavors and extensive distribution networks.

Key strategies in the market include premiumization, health-oriented product positioning, and geographic expansion. Multinational corporations are increasingly acquiring minority stakes in regional brands to ease market entry and address regulatory challenges. Opportunities are emerging in areas such as organic snacks, meat-based formats, and e-commerce channels. These segments allow smaller players to establish a foothold before larger competitors consolidate their positions. However, established companies often face challenges in adapting quickly, creating room for more agile entrants to grow.

Technology is playing a significant role in reshaping competition. Companies are adopting artificial intelligence for demand forecasting and route optimization, which helps reduce stockouts and improve fill rates in fragmented distribution networks. For example, Nestlé's use of blockchain technology for supply-chain traceability in Saudi Arabia, launched in 2024, enhances transparency and ensures compliance with Halal certification requirements. This capability provides a competitive advantage that smaller competitors may find difficult to replicate.

Middle East And Africa Snack Food Industry Leaders

Unilever PLC

PepsiCo Inc.

Nestlé S.A.

General Mills Inc.

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Arla Foods introduced Protein Puddings in Saudi Arabia, a high-protein, lactose-free snack containing 20g of protein, 158 kcal, and no added sugar. The product is available in chocolate, salted caramel, and hazelnut latte flavors.

- August 2024: Crispy unveiled Sweet Chilli Rings in Saudi Arabia, expanding its flavoured snack offerings in the Middle East market. The product launch reflects growing consumer appetite for bold, innovative flavours and convenient single‑serve snacking formats, supporting category growth in the Kingdom's competitive savory snacks segment.

- October 2024: The Yoghurt Shop, an Australian family-owned Greek yoghurt brand, has launched its products in Saudi Arabia through Tamimi Markets across the country. The brand offers artisan varieties, including Passion Fruit, Caramel Crumble, and Honey Spice Muesli, all made without artificial thickeners.

Middle East And Africa Snack Food Market Report Scope

Snack foods, often referred to as nutrient-dense snacks, are packed with essential nutrients and typically feature low levels of saturated fats, added sugar, and sodium. These snacks serve as quick and convenient meal options. The Middle East and Africa snack food market is categorized by type into frozen snacks, savory snacks, fruit snacks, confectionery snacks, bakery snacks, meat snacks, and other types. Based on ingredient type, the market is divided into organic/clean-label and conventional snacks. In terms of packaging, it is segmented into bags/pouches, cans, and others. By distribution channel, the market includes supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Geographically, the market is analyzed across South Africa, Saudi Arabia, the United Arab Emirates, and the rest of the Middle East and Africa. The market sizing has been done in value terms in USD and volume in tons for all the abovementioned segments.

By Product Type

| Frozen Snacks |

| Savoury Snacks |

| Fruit Snacks |

| Confectionery Snacks |

| Bakery Snacks |

| Meat Snacks |

| Others |

By Indredient Type

| Organic/Clean-Label |

| Conventional |

By Packaging Type

| Bags/Pouches |

| Cans |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Frozen Snacks |

| Savoury Snacks | |

| Fruit Snacks | |

| Confectionery Snacks | |

| Bakery Snacks | |

| Meat Snacks | |

| Others | |

| By Indredient Type | Organic/Clean-Label |

| Conventional | |

| By Packaging Type | Bags/Pouches |

| Cans | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Middle East and Africa snack food market?

The Middle East and Africa snack food market size reached USD 21.78 billion in 2026.

Which country is growing the fastest within the region?

The United Arab Emirates is forecast to grow at a 5.01% CAGR through 2031, the quickest pace among major geographies.

Which product type is expected to record the highest growth?

Meat snacks are projected to expand at a 5.08% CAGR thanks to high-protein positioning and Halal-certified launches.

How will online retail influence snack sales over the next five years?

Online retail is set to post a 5.13% CAGR as smartphone penetration and rapid-delivery infrastructure drive digital purchases.