Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

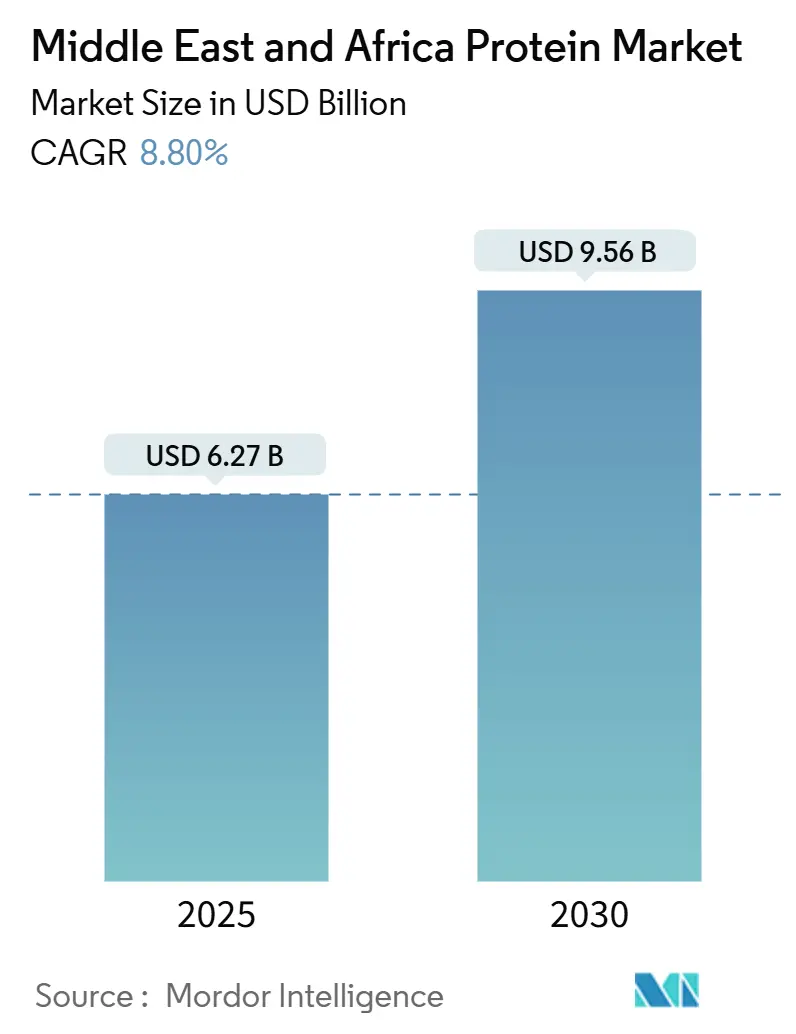

| Market Size (2025) | USD 6.27 Billion |

| Market Size (2030) | USD 9.56 Billion |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Protein Market Analysis by Mordor Intelligence

The Middle East and Africa protein market is estimated at USD 6.27 billion in 2025 and is projected to reach USD 9.56 billion by 2030, registering a CAGR of 8.80% during the forecast period. This growth positions the region as one of the fastest-growing protein markets globally, driven by government food-security initiatives, a large youth demographic, and increasing food-processing capabilities. While animal-based protein sources dominate in terms of volume, rising awareness of non-communicable diseases has encouraged the incorporation of plant-based proteins, such as soy and pea isolates, into bakery, dairy-alternative, and meat-analogue products. Investments in technologies like filtration, enzymatic hydrolysis, and spray-drying have reduced the production costs of high-purity isolates. Additionally, innovative feed contracts mitigate risks associated with fluctuating global oilseed prices. Policymakers are also fostering local production capacity through initiatives such as Saudi Arabia’s Vision 2030 and Morocco’s Green Generation Strategy, which ensure guaranteed offtake volumes to attract private investment. In South Africa, government incentives are drawing multinational ingredient producers to strengthen the domestic supply chain.

Key Report Takeaways

- By source, animal-based proteins held 52.18% of the Middle East and Africa protein market share in 2024, while plant proteins led growth at 8.87% CAGR to 2030.

- By form, isolates captured 39.21% revenue share of the Middle East and Africa protein market size in 2024; hydrolysates record the fastest trajectory, advancing at 9.05% CAGR between 2025 and 2030.

- By application, food and beverages accounted for 75.67% of 2024 demand, whereas sports and nutrition formulations are forecast to post an 8.97% CAGR over 2025-2030.

- By geography, Saudi Arabia dominated with 28.19% market share in 2024; South Africa is poised for the highest growth, registering an 8.89% CAGR to 2030.

Middle East And Africa Protein Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of food and beverage industry | +1.8% | Saudi Arabia, United Arab Emirates, Egypt, South Africa | Medium term (2-4 years) |

| Strong cultural preference for animal protein | +1.5% | Gulf Cooperation Council countries, Turkey, North Africa | Long term (≥ 4 years) |

| Protein deficiency and malnutrition gap | +1.2% | Nigeria, Egypt, Sub-Saharan Africa | Long term (≥ 4 years) |

| Growing sports-nutrition demand among young population | +1.0% | Saudi Arabia, United Arab Emirates, South Africa | Short term (≤ 2 years) |

| Rise of plant-based and vegan protein owing to NCD burden | +1.4% | Gulf Cooperation Council countries, Egypt, South Africa | Medium term (2-4 years) |

| Government food-security initiatives supporting local protein processing | +1.9% | Saudi Arabia, Egypt, Morocco, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government food-security initiatives supporting local protein processing

Government-led food security initiatives in the Middle East and Africa are transforming protein supply chains by promoting local production of isolates, concentrates, and other value-added protein ingredients. In Saudi Arabia, Vision 2030 emphasizes improving agricultural productivity through advanced farming techniques, precision agriculture, and smart irrigation systems, supported by public-private partnerships to enhance supply chain efficiency. Between 2018 and 2024, the Saudi Agricultural Development Fund allocated USD1.33 billion in loans, enabling processors to access affordable capital while mitigating investment risks through guaranteed feedstock supply and offtake agreements [1]Source: Vision 2030, "Vision 2030 Annual Report 2024," vision2030.gov. In Egypt, government programs have achieved 60% self-sufficiency in meat and near-complete self-sufficiency in poultry, highlighting the success of state-led efforts in bolstering local protein production [2]Source: State Information Service, "Egypt achieves 60% self-sufficiency in meat, near-complete self-sufficiency in poultry," sis.gov.eg. These initiatives collectively reduce capital costs for private processors, promote the adoption of advanced protein processing technologies, and foster the growth of a robust, regionally integrated protein market across the Middle East and Africa region.

Expansion of food and beverage industry

The Middle East and Africa (MEA) region is experiencing significant growth in the food and beverage industry, driven by factors such as population growth, urbanization, shifting dietary habits, and increasing demand for convenient, nutritious, and protein-rich foods. This growth is creating substantial opportunities for the protein market, particularly in protein isolates, concentrates, and functional protein ingredients. In Saudi Arabia, the food industry includes approximately 1,300 registered companies, with about 80% classified as large enterprises employing over 100 staff. Food processing dominates the domestic market, contributing over 75% of total revenue [3]Source: USDA, "Retail Foods Annual," usda.gov. This underscores the sector's strategic importance and its potential for adopting protein ingredients. Across the MEA region, the rising demand for packaged and processed foods, dairy, meat, and bakery products is driving the need for protein-rich formulations that align with consumer preferences for health, taste, and convenience. The ongoing expansion of the food and beverage industry is encouraging investments in protein processing infrastructure, research and development, and innovative product launches. These developments are enabling manufacturers to scale operations and diversify their offerings.

Rise of Plant-based and vegan protein owing to NCD burden

The increasing prevalence of non-communicable diseases (NCDs), such as obesity, diabetes, cardiovascular diseases, and hypertension, is driving a shift toward healthier dietary choices in the Middle East and Africa (MEA). Consumers are progressively adopting plant-based and vegan protein sources as part of preventive nutrition strategies aimed at reducing saturated fat intake, lowering cholesterol levels, and improving overall health. This shift is further supported by heightened health awareness, government-led nutritional education initiatives, and the influence of global wellness movements. The growing consumption of plant-based proteins not only addresses public health challenges but also aligns with environmental sustainability objectives. This creates opportunities for protein ingredient suppliers, food processors, and alternative protein startups to expand their operations. As awareness of NCD-related risks continues to rise, the MEA protein market is expected to experience sustained growth, driven by increasing consumer demand for nutritious, sustainable, and functional plant-based protein solutions.

Growing sports-nutrition demand among young population

The increasing focus on health, fitness, and active lifestyles among the youth in the Middle East and Africa (MEA) is driving the demand for sports-nutrition products such as high-protein formulations, protein bars, shakes, and functional beverages. Millennials and Gen Z consumers are particularly emphasizing muscle development, endurance, recovery, and overall wellness, leading to a greater adoption of protein-rich diets designed for sports and performance requirements. In Saudi Arabia, the Households Sport Practice Survey by GASTAT revealed that 17.4% of the population participated in sports activities for over 150 minutes per week in 2024, indicating a substantial base of active consumers seeking nutritional support. This trend is also evident across urban centers in the region, where gym memberships, fitness programs, and participation in both recreational and competitive sports are on the rise. The expanding sports-nutrition market is prompting manufacturers to create high-protein, functional, and convenient products, including plant-based and whey protein options, to cater to the preferences of young and active consumers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile feedstock prices for animal and plant proteins | -1.3% | Global, acute in import-dependent Gulf Cooperation Council and North Africa | Short term (≤ 2 years) |

| Cultural resistance to genetically-engineered protein sources | -0.6% | Gulf Cooperation Council countries, North Africa | Long term (≥ 4 years) |

| Regulatory ambiguity around novel proteins (insect, cultured) | -0.9% | South Africa, Nigeria, Gulf Cooperation Council (excluding Qatar) | Medium term (2-4 years) |

| Dependence on imports for many protein forms | -1.1% | Gulf Cooperation Council countries, Egypt, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile feedstock prices for animal and plant proteins

Fluctuating raw material prices, including soy, pea, whey, and other protein-rich feedstocks, represent a significant restraint for the Middle East and Africa (MEA) protein market. Factors such as supply chain disruptions, extreme weather conditions, geopolitical tensions, and currency fluctuations often result in sharp increases in procurement costs for producers of both animal and plant-based proteins. These cost increases directly affect production expenses and reduce profit margins. In the Middle East and Africa (MEA) region, heavy reliance on imported feedstocks makes local processors particularly susceptible to global market fluctuations. For instance, rising global prices of soy and wheat can elevate costs for dairy, meat, and plant-protein product formulations. Similarly, price volatility in whey and other dairy by-products impacts the cost of animal-protein-based ingredients. This instability creates pricing pressures for manufacturers, reduces affordability for consumers, and may delay or limit the scaling of new protein-based product launches.

Regulatory ambiguity around novel proteins (insect, cultured)

The development of novel protein sources, such as insect-based and cultured proteins, in the Middle East and Africa (MEA) faces challenges due to regulatory uncertainty and a lack of clear guidance from food safety authorities. Many countries in the region do not have comprehensive frameworks for the approval, labeling, and commercialization of these alternative proteins, leading to delays in product launches and market entry. This regulatory uncertainty heightens compliance risks for manufacturers and investors, as approval timelines, safety standards, and permissible usage levels remain undefined. Consumer acceptance is also impacted, as the absence of clear regulatory endorsement can erode trust and hinder adoption. Furthermore, variations in regulations across Middle East and Africa (MEA) countries add complexity to cross-border trade and the scaling of novel protein products. As a result, while insect-based and cultured proteins offer potential for sustainable and high-quality nutrition, regulatory challenges continue to restrict investment and commercialization, thereby slowing their adoption in the Middle East and Africa (MEA) protein market.

Segment Analysis

By Source: Animal Proteins Hold Share, Plant Formats Gain Velocity

Animal-based proteins accounted for 52.18% of the market share in 2024, supported by halal-certified dairy and poultry systems that align with cultural norms and benefit from decades of infrastructure investment. Saudi Arabia's poultry sector alone invested over USD 1 billion in capacity expansions during 2024, aiming for 80% self-sufficiency by 2025. Additionally, Almarai's annual dairy production of 1.8 million tonnes supplies whey and casein for both domestic and export markets. These developments highlight the significant role of animal-based proteins in meeting both local and international demand, leveraging established infrastructure and cultural compatibility. However, plant-based proteins are projected to grow at the fastest rate, with a CAGR of 8.87% through 2030. This growth is driven by increasing industrial demand for soy and pea isolates, which are widely used in bakery products, dairy alternatives, and meat analogues. The rising interest in plant-based proteins reflects a shift in consumer preferences and industrial applications, emphasizing sustainability and dietary diversification.

Novel proteins, including insect, microbial, and cultured varieties, currently hold a minimal market share but are attracting significant research and development investment. These investments and advancements in novel protein technologies underscore the growing focus on innovation and alternative protein sources to address evolving market demands. While still in the early stages, the development of novel proteins represents a promising area for future growth, driven by technological progress and increasing interest in sustainable food production methods.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Isolates Dominate Functionality, Hydrolysates Capture Performance Segment

Isolates accounted for 39.21% of the market share in 2024, valued for their protein content exceeding 90% and neutral organoleptic properties, which allow for fortification without impacting taste or texture. These isolates, particularly dairy-based ones like whey protein isolate and milk protein isolate, are produced through membrane filtration. This process, as detailed in the International Dairy Federation's technical specifications, ensures consistent functionality across batches, making them a reliable choice for various applications. The high protein content and neutral flavor profile of isolates make them suitable for use in a wide range of food and beverage products, including those targeting health-conscious consumers.

Hydrolysates, on the other hand, are projected to grow at a compound annual growth rate (CAGR) of 9.05% through 2030. These undergo enzymatic pre-digestion, a process that enhances absorption rates, making them particularly effective for sports nutrition and clinical applications. Their rapid absorption properties are especially beneficial for athletes and patients requiring quick protein intake. Additionally, technological advancements in membrane filtration and enzymatic hydrolysis are playing a significant role in reducing production costs and expanding the range of applications for both isolates and hydrolysates, further driving their adoption in the market.

By Application: Food and Beverage Anchors Volume, Sports Nutrition Drives Margin

Food and beverage applications accounted for 75.67% of the market share in 2024, encompassing bakery fortification, dairy and dairy alternatives, meat products and analogues, and functional beverages. Within this category, dairy and dairy alternatives are increasingly merging as manufacturers combine whey isolates with almond or oat proteins to create hybrid products that meet both taste and health requirements. This trend reflects a growing consumer demand for products that balance nutritional benefits with appealing flavors. Almarai's 2024 high-protein dairy range illustrates this approach, offering over 20 grams of protein per serving while avoiding cultural resistance to fully plant-based labels. Such innovations highlight the evolving strategies of manufacturers to cater to diverse consumer preferences while maintaining market competitiveness.

The sports and performance nutrition segment is projected to grow at a CAGR of 8.97% through 2030, surpassing the overall market growth rate as youth demographics and fitness culture continue to converge. This growth is driven by an increasing focus on health and wellness among younger populations, coupled with a rising interest in fitness and athletic performance. The segment's expansion is further supported by advancements in product formulations, including the incorporation of high-quality protein sources and functional ingredients designed to enhance physical performance and recovery. As a result, sports and performance nutrition is emerging as a key area of growth within the broader market landscape.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Middle East and Africa (MEA) protein market is characterized by its diversity, influenced by varying dietary habits, economic conditions, and the maturity of the food industry across the region. In 2024, Saudi Arabia accounted for 28.19% of the protein market revenue, while the South Africa is projected to register a CAGR of 8.89%. The Gulf Cooperation Council (GCC) countries, including Saudi Arabia, the UAE, and Qatar, represent a premium and health-conscious segment, with significant demand for functional, plant-based, and sports nutrition proteins. Key growth drivers in this market include high disposable incomes, advanced retail infrastructure, and increasing awareness of health and wellness. Notably, the food processing sector contributes over 75% of domestic revenue in Saudi Arabia.

In North Africa, countries such as Egypt, Algeria, and Morocco benefit from large-scale government initiatives aimed at enhancing food self-sufficiency and boosting local protein production. For instance, Egypt has achieved 60% self-sufficiency in meat and nearly complete self-sufficiency in poultry, supported by state-backed agricultural development programs. These efforts promote investment in protein processing facilities and the adoption of both animal and plant-based protein technologies.

Sub-Saharan Africa presents a fragmented market landscape, with emerging economies like South Africa, Kenya, and Nigeria serving as regional hubs for protein processing, innovation, and exports. Growth in this region is driven by increasing urbanization, rising protein consumption, and the expansion of the middle class. However, challenges such as fluctuating feedstock prices, inadequate cold chain infrastructure, and regulatory inconsistencies pose obstacles to market expansion.

Competitive Landscape

The market demonstrates a moderate level of consolidation, with global ingredient companies and regional leaders collectively accounting for over 60% of the market share. Prominent players such as Cargill, ADM, and Kerry utilize their global research and development capabilities alongside substantial capital investments to maintain their competitive edge. Freight cost volatility and feedstock hedging capabilities play a significant role in differentiating market participants.

Multinational corporations are better equipped to manage fluctuations in ocean freight rates due to their scale and resources, allowing them to absorb cost spikes more effectively. In contrast, local firms often adopt strategies such as securing long-term supply agreements with growers in Brazil and Argentina to mitigate risks and ensure a stable supply of raw materials. These approaches underline the varying strategies employed by companies to navigate market challenges and maintain competitiveness.

Innovation opportunities are emerging in areas such as insect and cultured proteins, which hold potential for addressing future protein demands. However, regulatory uncertainties and approval processes create barriers to immediate commercialization, slowing the pace of adoption. Additionally, the clarification of GSO halal standards remains a critical factor influencing market dynamics. Once these standards are clearly defined, both multinational and regional players are expected to intensify efforts to secure first-mover advantages in segments such as fortified staples and ready-to-eat meals, which are anticipated to experience growing demand.

Middle East And Africa Protein Industry Leaders

-

Archer Daniels Midland Company

-

Cargill Inc.

-

Kerry Group plc

-

Royal FrieslandCampina N.V.

-

Glanbia plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: NiHTEK has launched NiHPRO Gourmet Isolate in the South African market through a partnership with wellness brand My Wellness, marking a notable development in clean-label protein products. Introduced in July 2025, this hydrolysed, non-dairy, allergen-free protein isolate is available in various flavors designed for taste, mixability, and versatility, catering to everyday athletes and health-conscious consumers. Utilizing proprietary technologies such as Advanced Precision Hydrolysis (APH) and Molecular Protein Infusion (MPi), NiHPRO offers high digestibility, an enhanced amino acid profile, and a smooth texture, free from common allergens, GMOs, and dairy, aligning with the rising demand for clean, high-performance nutrition solutions.

- March 2025: Unibio’s microbial single-cell protein, Uniprotein, has received approval from the Saudi Food and Drug Authority (SFDA) for use in aquaculture feed for fish, shrimp, and crustaceans. Following a detailed review process initiated in April 2023, the SFDA confirmed the safety of Uniprotein, allowing its sale and commercial testing in the Saudi feed market. Positioned as a sustainable and high-quality alternative to traditional protein sources like fishmeal and soy, Uniprotein closely matches fishmeal’s amino acid profile and is non-GMO, fully traceable, and free from pesticides and antibiotics.

- February 2025: Archer Daniels Midland (ADM), a global food processing and nutrition company, has inaugurated a new facility in the Lagos Free Trade Zone (LFZ) in Nigeria as part of its strategy to expand operations across Africa. This facility is designed to serve as a hub for innovation, collaboration, and growth, leveraging the LFZ’s strategic location, advanced infrastructure, and proximity to the Lekki port to enhance services across Human and Animal Nutrition, Carbohydrate Solutions, and related business segments.

- October 2023: Ingredion, a global provider of food ingredient solutions, collaborated with distributor Univar to present a range of plant-based, low-sugar, and natural product innovations at the Gulfood Manufacturing trade event in Dubai. The showcase aimed to address the growing consumer demand for healthier and clean-label foods. Featured products included plant-based protein applications and natural formulations such as vegetarian dishes, egg-free tahini mayo, sugar-free condiments, protein crackers, and reduced-sugar desserts, emphasizing the increasing focus on nutritional content and natural ingredients among UAE consumers.

Middle East And Africa Protein Market Report Scope

The Middle East & Africa rice protein market is segmented by product type rice protein isolate, rice protein concentrate, and others. Based on the application, the market is segmented as food and beverages, dietary supplements, and animal feed. The market is also classified by geography into Saudi Arabia, South Africa, and the Rest of the Middle East and Africa.

By Source

| Animal-Based-Protein |

| Plant-Based-Protein |

| Others ( Novel Protein, Insect, Microbial, Cultured) |

By Form

| Isolates |

| Concentrates |

| Hydrolysates |

By Application

| Food and Beverages | Bakery and Cereals |

| Dairy and Dairy Alternatives | |

| Meat products and Analogues | |

| Others | |

| Sports and Performance Nutrition | |

| Animal Feed | |

| Others |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Source | Animal-Based-Protein | |

| Plant-Based-Protein | ||

| Others ( Novel Protein, Insect, Microbial, Cultured) | ||

| By Form | Isolates | |

| Concentrates | ||

| Hydrolysates | ||

| By Application | Food and Beverages | Bakery and Cereals |

| Dairy and Dairy Alternatives | ||

| Meat products and Analogues | ||

| Others | ||

| Sports and Performance Nutrition | ||

| Animal Feed | ||

| Others | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Middle East and Africa protein market?

The market is valued at USD 6.27 billion in 2025 and is projected to reach USD 9.56 billion by 2030.

Which country leads regional demand?

Saudi Arabia holds the largest share, accounting for 28.19% of 2024 revenue.

Which protein source is growing fastest?

Plant-based proteins are forecast to grow at an 8.87% CAGR through 2030.

Why are hydrolysates gaining traction?

Enzymatic pre-digestion accelerates absorption, making hydrolysates popular in sports-nutrition and clinical formulas.

Page last updated on: