Middle East And Africa High Voltage Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

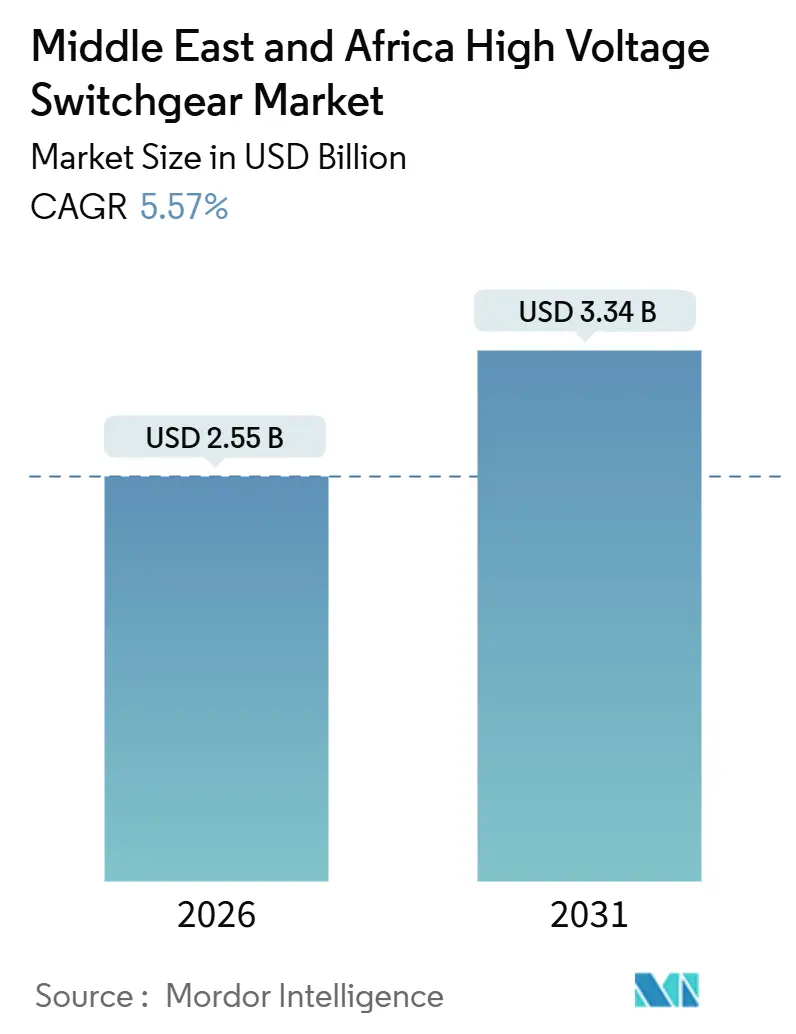

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa High Voltage Switchgear Market Analysis by Mordor Intelligence

The Middle East And Africa High Voltage Switchgear Market size is estimated at USD 2.55 billion in 2026, and is expected to reach USD 3.34 billion by 2031, at a CAGR of 5.57% during the forecast period (2026-2031).

A structural pivot toward HVDC-enabled green-hydrogen export corridors, sovereign transmission backbones that bypass aging AC grids, and multi-gigawatt utility procurement programs anchor this upturn. Saudi Arabia retained 25.89% of 2025 revenue as Vision 2030 accelerated substation rollout, while Egypt delivered the region’s fastest switchgear growth on the back of its 3 GW Egypt-Saudi interconnector and a 14 GW renewables pipeline. Utilities drove 72.68% of 2025 demand and will outpace overall growth, supported by GCC mandates to harden grids against renewable intermittency and cross-border wheeling needs. Gas-insulated switchgear (GIS) is gaining ground in space-constrained industrial megaprojects even though air-insulated switchgear (AIS) remains dominant, and DC switchgear is scaling rapidly as HVDC Light corridors displace conventional AC. Competitive intensity is moderate, with four global vendors capturing more than half of high-end tenders and niche suppliers using local-content rules to penetrate sub-132 kV niches.

Key Report Takeaways

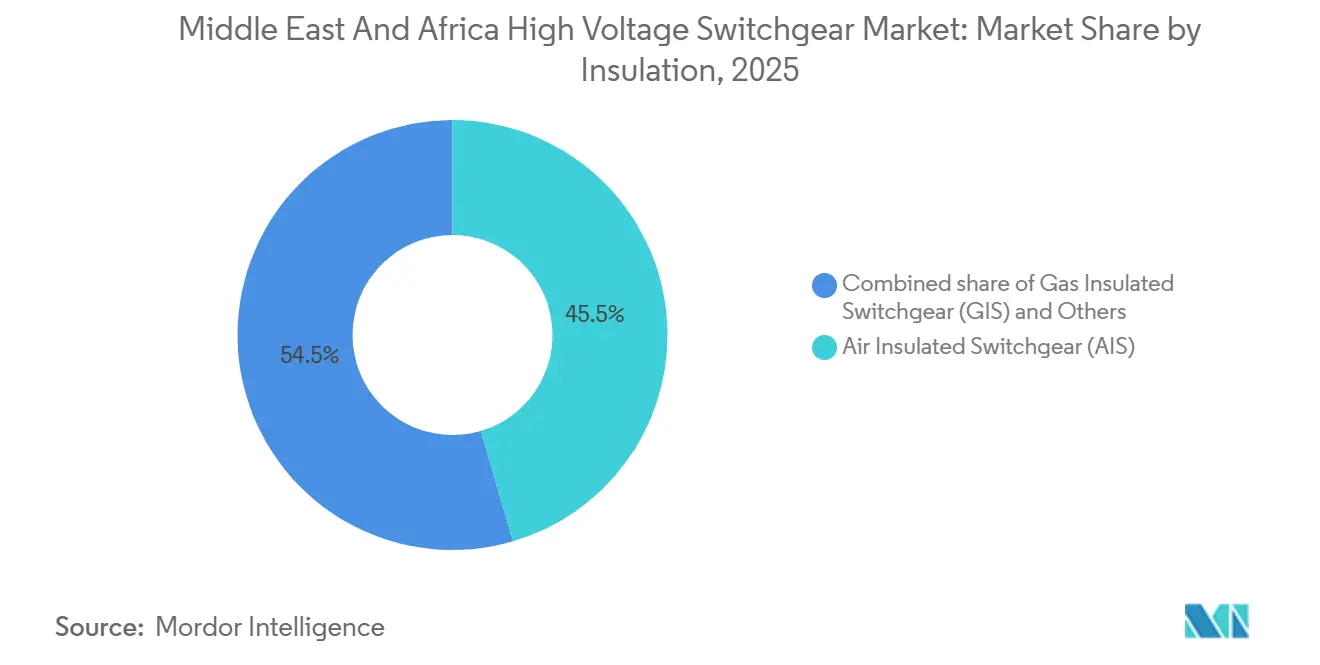

- By insulation, gas insulated switchgear posted a 7.23% growth rate through 2031, while air insulated switchgear retained 45.45% of the Middle East and Africa high voltage switchgear market share in 2025.

- By current type, DC switchgear expanded at 8.85% CAGR, whereas AC switchgear accounted for 90.11% share of the Middle East and Africa high voltage switchgear market size in 2025.

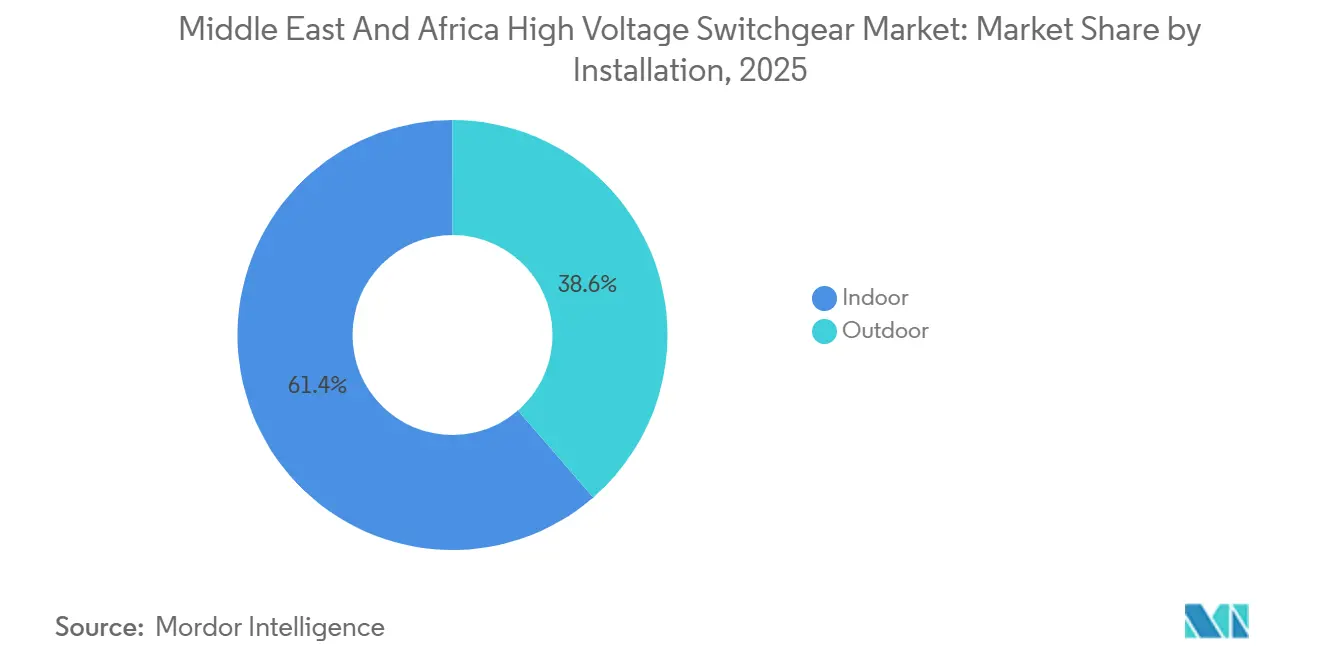

- By installation, outdoor systems advanced at 8.49% CAGR, and indoor units captured 61.36% of the Middle East and Africa high voltage switchgear market share in 2025.

- By end-user, utilities held 72.68% of the Middle East and Africa high voltage switchgear market size in 2025 and are forecast to expand at a 7.71% CAGR to 2031.

- By geography, Saudi Arabia led with 25.89% revenue share in 2025, while Egypt recorded the highest CAGR at 9.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa High Voltage Switchgear Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of HV transmission projects | +1.2% | Saudi Arabia, Egypt, UAE, Qatar, Bahrain | Medium term (2-4 years) |

| Increasing renewable-energy grid integration | +1.0% | Morocco, Egypt, South Africa, Kenya | Long term (≥ 4 years) |

| Industrial megaprojects | +0.9% | Saudi Arabia, UAE, Oman | Medium term (2-4 years) |

| Growing data-center build-out | +0.5% | Kenya, South Africa, UAE, Egypt | Short term (≤ 2 years) |

| Refugee-camp electrification | +0.3% | Jordan, Kenya, Uganda, Ethiopia | Long term (≥ 4 years) |

| Green-hydrogen export corridors | +0.8% | Saudi Arabia, UAE, Egypt, Morocco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of HV Transmission Projects

The 3 GW, ±500 kV Egypt-Saudi HVDC interconnector reached 95% completion in 2025, creating the first asynchronous link between North Africa and the Arabian Peninsula.[1]Hitachi Energy, “Egypt-Saudi HVDC Interconnector,” hitachienergy.com Saudi Arabia’s NEOM-Yanbu 525 kV corridor and the Riyadh-Kudmi 500 kV line illustrate a broader pivot to long-haul HVDC, which lowers line losses and bypasses congested AC corridors. GCCIA’s Al-Fadhili upgrade added 1,800 MW of transfer capacity in 2025, boosting resilience for the six-nation grid.[2]GCC Interconnection Authority, “Grid Statistics,” gccia.com.sa These flagship projects accelerate orders for 525 kV DC breakers, converter-station GIS, and protection relay systems.

Increasing Renewable Energy Grid Integration Needs

Morocco’s 1,000 km Boujdour-Tanxift ultra-high-voltage line will evacuate 2 GW of solar and wind by 2028 and requires switchgear tolerant of rapid voltage transients.[3]Masen, “Boujdour-Tanxift Transmission Line,” masen.ma Kenya’s grid now exceeds 90% renewables, prompting KETRACO to deploy 400 kV substations with relays that isolate faults within 20 milliseconds. South Africa’s REIPPPP sped up GIS retrofits at 132 kV and 275 kV sites along coastal corridors. ABB’s 420 kV GIS at the Green Duba solar park in Saudi Arabia shows how compact switchgear cuts civil works by 30% and shortens build time.[4]ABB, “Green Duba 420 kV GIS,” abb.com Harmonized IEC 62271-200:2023 adoption across the Gulf standardizes performance requirements, encouraging cross-border equipment sourcing.

Industrial Megaprojects

NEOM’s green-hydrogen plant needs 92 GIS bays at 380 kV to synchronize electrolyzers, desalination units, and ammonia synthesis loops, a package supplied by GE Vernova. ADNOC’s USD 5.5 billion Ruwais LNG complex and Oman’s Duqm refinery expansion both specify outdoor hybrid switchgear that withstands corrosive marine atmospheres. DEWA’s AED 7.6 billion transmission plan includes 49 new 132 kV and two 400 kV substations, reinforcing the UAE backbone.

Surge In Green-Hydrogen Export Corridors Requiring HVDC Hubs

The NEOM-Yanbu 3 GW HVDC Light link integrates electrolyzer clusters with export terminals and provides black-start capability, functions that AC networks struggle to support. Morocco’s feasibility study for a 24 GW North Africa-Europe interconnector foresees ±525 kV subsea cables paired with GIS converter stations, advancing the kingdom’s vision of becoming an EU power bridge. Egypt and the UAE pursue similar hydrogen corridors aligned with the India-Middle East-Europe Economic Corridor. As electrolyzer supply chains mature and European carbon-border rules favor green hydrogen after 2028, HVDC nodes will scale.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile public-sector capex | –0.6% | Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman | Short term (≤ 2 years) |

| Persistent counterfeits & grey imports | –0.4% | Egypt, Nigeria, Kenya, Morocco, wider MEA | Medium term (2-4 years) |

| Delays in wheeling code harmonization | –0.3% | GCC states, Egypt-Saudi corridor, North Africa coastal interconnects | Long term (≥ 4 years) |

| Scarcity of SF₆-free maintenance expertise | –0.2% | South Africa, Kenya, Morocco, broader MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Public-Sector Capex Due To Oil-Price Swings

Brent crude fluctuated between USD 70 and USD 90 per barrel in 2024 and trimmed Saudi discretionary infrastructure funding by about 10%. Egypt’s currency crunch similarly delayed USD 400 million of 220 kV upgrades. The UAE maintained outlays using sovereign-wealth reserves, but ADNOC still cut upstream budgets by 5% in 2024.

Persistent Counterfeits And Grey Imports Eroding Margins

SASO issued 11,589 IECEE certificates in 2023, yet counterfeit breakers still cause substation failures in Nigeria and Egypt. Grey imports undercut OEM prices by 15-20% in the sub-132 kV bracket and complicate warranty enforcement. Harmonized GSO IEC 60947-1:2024 is expected to tighten customs checks after 2027.

Segment Analysis

By Insulation: GIS Scales In Constrained Industrial Sites

Air-insulated switchgear retained 45.45% of 2025 revenue within the Middle East and Africa high voltage switchgear market share, underpinned by its cost advantage in land-abundant utility substations. Gas-insulated switchgear is growing at a 7.23% CAGR, supported by megaprojects such as NEOM’s coastal hydrogen complex, which ordered 92 bays at 380 kV. Compact GIS reduces footprint roughly tenfold versus AIS, slashing civil works spend and enabling faster commissioning.

The Middle East and Africa high voltage switchgear market size tied to GIS will widen further as urban densification prompts indoor upgrades and as SF₆-free variants comply with tightening environmental rules. Hybrid solutions using clean-air insulation satisfy offshore and mobile needs, while GSO-aligned IEC standards harmonize short-circuit testing, improving cross-border procurement efficiency. Utilities still favor AIS for greenfield transmission yards where land is cheap, but industrial and commercial operators increasingly specify GIS to unlock real-estate value.

Note: Segment shares of all individual segments available upon report purchase

By Current Type: HVDC Corridors Propel DC Adoption

AC switchgear captured 90.11% of 2025 revenue, reflecting legacy 50/60 Hz networks. DC switchgear, though only 9.89% of volume, is projected to expand at an 8.85% CAGR as HVDC Light links such as the 3 GW NEOM-Yanbu and 3 GW Egypt-Saudi corridors progress. Hybrid mechanical-semiconductor DC breakers handle fault current interruption without natural zero crossings, unlocking new point-to-point corridors.

The Middle East and Africa high voltage switchgear market size associated with DC projects will rise as green-hydrogen exporters link electrolyzer clusters directly to converters, bypassing repetitive AC-DC-AC stages. AC technology remains the backbone for meshed grids, distribution feeders, and most industrial plants, but DC is emerging as the favored architecture for cross-border power trade and long-distance, high-capacity evacuation.

By Installation: Outdoor Innovations Tackle Harsh Climates

Indoor equipment held 61.36% of 2025 spending, thanks to controlled environments that protect against dust and 50 °C heat. Hyperscale data centers in Nairobi and Dubai deploy indoor GIS with remote monitoring to meet 99.995% uptime. Outdoor switchgear, however, is outpacing at 8.49% CAGR, led by pre-assembled modules that shrink on-site labor by up to 35%.

Outdoor units in DEWA’s 400 kV network withstand sandstorms and extreme temperatures, aided by IP65 enclosures, corrosion-resistant coatings, and natural convection cooling. As project owners compress schedules to integrate renewables, factory-tested outdoor skids become attractive, broadening the Middle East and Africa high voltage switchgear market.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Utilities Still Dominate As Industrial Demand Diversifies

Utilities absorbed 72.68% of 2025 demand and are forecast to grow at a 7.71% CAGR as Saudi Arabia’s Vision 2030, Egypt’s 14 GW renewables program, and Morocco’s UHV line drive bulk procurement. The Middle East and Africa high voltage switchgear market share linked to utilities will stay above two-thirds, but industrial complexes, LNG terminals, and mining operations are diversifying revenue streams.

Industrial megaprojects such as Ruwais LNG, Duqm refinery, and South African platinum mines require ruggedized switchgear with arc-flash mitigation. Commercial real estate and EV-ready smart communities in Riyadh and Cairo are specifying compact ring-main units. Refugee-camp mini-grids, though small, present double-digit growth and premium margins for standardized microgrid switchgear.

Geography Analysis

Saudi Arabia accounted for 25.89% of 2025 revenue, anchored by Vision 2030’s USD 500 billion infrastructure program and the Al-Fadhili grid upgrade that lifted transfer capacity by 1,800 MW. The NEOM-Yanbu and Riyadh-Kudmi HVDC projects alone represent more than USD 2 billion in switchgear opportunity through 2028. Egypt, benefiting from the 3 GW Egypt-Saudi interconnector and Europe-oriented hydrogen plans, is projected to expand switchgear spending at a 9.06% CAGR to 2031.

The United Arab Emirates continues to invest via DEWA’s AED 7.6 billion program, integrating 5 GW of solar by 2030 and backing ADNOC’s Ruwais LNG complex. Morocco’s Boujdour-Tanxift UHV corridor and Noor Midelt hybrid solar plant strengthen its role as an exporter to Europe. South Africa’s USD 8.5 billion Just Energy Transition Partnership obliges Eskom to deploy GIS at 132 kV to 400 kV. Qatar, Oman, and Kenya contribute mid-single-digit growth through industrial zones and geothermal-linked substations.

Nigeria’s Siemens Electrification Project targets 25 GW by 2034 and, despite currency and regulatory hurdles, positions the country as sub-Saharan Africa’s second-largest market after South Africa. Smaller nations such as Jordan, Ethiopia, and Uganda add incremental demand via refugee-camp electrification and dam-linked transmission corridors, broadening geographic diversification within the Middle East and Africa high voltage switchgear market.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

Four global players, Hitachi Energy, Siemens, Schneider Electric, and ABB, collectively commanded roughly 55-60% of extra-high-voltage and HVDC tenders in 2025. Hitachi Energy leads HVDC thanks to its converter-station portfolio used on the Egypt-Saudi, NEOM-Yanbu, and Al-Fadhili projects. Siemens and Schneider differentiate through digital twins and predictive-maintenance suites that cut unplanned outages by up to 20%. ABB’s GIS footprint benefits from compact designs that lower civil costs.

Second-tier suppliers such as CG Power, Hyosung Heavy Industries, and Larsen & Toubro capture distribution automation work aided by local-content rules. NOJA Power and Ormazabal win niche business in rural reclosers and commercial ring-main units. Chinese firms, including Chint, are pushing turnkey EPC packages at steep discounts under Belt and Road financing, though IEC certification gaps hinder entry into top-tier utility bids.

White-space opportunities revolve around SF₆-free maintenance services, DC switchgear for hydrogen corridors, and standardized microgrid panels for relief agencies. Vendors that secure technician upskilling and digital-service contracts lock in aftermarket revenue and counter growing price competition in primary equipment. Compliance with GSO IEC 62271-200:2023 and IEC 62271 1 rules will remain a key gatekeeper, filtering out grey-market imports and shaping long-term market share in the Middle East and Africa high voltage switchgear market.

Middle East And Africa High Voltage Switchgear Industry Leaders

Hitachi Energy

Siemens AG

Schneider Electric

General Electric

Mitsubishi Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Orascom Construction, an Egyptian engineering and construction company, stated that commissioning activities for the first phase (Pole I) of the Egypt-Saudi Arabia high voltage direct current (HVDC) interconnection are ongoing as of 2025. The company is partnering with Hitachi Energy as a contractor for this project.

- September 2025: The Electricity and Water Authority (EWA) of Bahrain awarded a project to establish a 400 kV grid substation in the Sitra industrial area. The contract is valued at approximately BHD 48.1 million (ISO code BHD).

- August 2025: Saeed Mohammed Al Tayer, MD & CEO of Dubai Electricity and Water Authority (DEWA), announced that DEWA’s electricity transmission projects exceed AED 7.6 billion. In H1 2025, DEWA commissioned four 132 kV substations with a 450 MVA capacity at AED 725 million, including 228 km of transmission cables.

- January 2024: Indian engineering and construction company Larsen & Toubro (L&T) secured an EPC contract for the 1800 MW Phase 6 of the Mohammed bin Rashid Al Maktoum Solar Park in Dubai. Awarded by Masdar to L&T's renewable EPC division, the 20 km2 solar photovoltaic plant will be commissioned in three phases.

Middle East And Africa High Voltage Switchgear Market Report Scope

High-voltage switchgear is vital to electrical grids or high-tension power distribution networks. It enables the safe, efficient, and reliable transfer of electrical energy by providing a means to safely disconnect and isolate electrical equipment from the power supply. Here is more about this type of switchgear.

The Middle East and Africa high voltage switchgear market is segmented by insulation, current type, installation, end-user, and geography. By insulation, the market is segmented into gas-insulated switchgear, air-insulated switchgear, and others. By current type, the market is segmented into AC switchgear and DC switchgear. By installation, the market is segmented into indoor and outdoor. By end-user, the market is segmented into utilities, residential, commercial, and industrial. The report also covers the market size and forecasts across major regional countries. Each segment's market size and forecast are based on revenue (USD billion).

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| South Africa |

| Egypt |

| Morocco |

| Rest of Middle East and Africa |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How large is the Middle East and Africa high voltage switchgear market in 2026?

It is projected at about USD 2.55 billion, following the 5.57% CAGR trajectory quantified in this report.

Which country is growing fastest for high voltage switchgear demand?

Egypt leads with a 9.06% CAGR to 2031, propelled by the Egypt-Saudi HVDC link and a 14 GW renewables pipeline.

What technology segment is expanding more quickly, GIS or AIS?

Gas insulated switchgear is advancing at 7.23% CAGR, outpacing air insulated alternatives due to footprint advantages in industrial megaprojects.

Why is DC switchgear gaining traction in the region?

HVDC corridors such as NEOM-Yanbu and Egypt-Saudi favor DC breakers that eliminate AC-DC-AC conversions and cut transmission losses.

How are oil-price swings affecting switchgear procurement?

Volatile crude prices reduce Gulf fiscal buffers and delay some utility tenders, trimming near-term market growth by about 0.6 percentage point.

Which vendors dominate HVDC projects in the region?

Hitachi Energy, Siemens, Schneider Electric and ABB collectively control roughly 55-60% of extra-high-voltage and HVDC switchgear awards.