Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

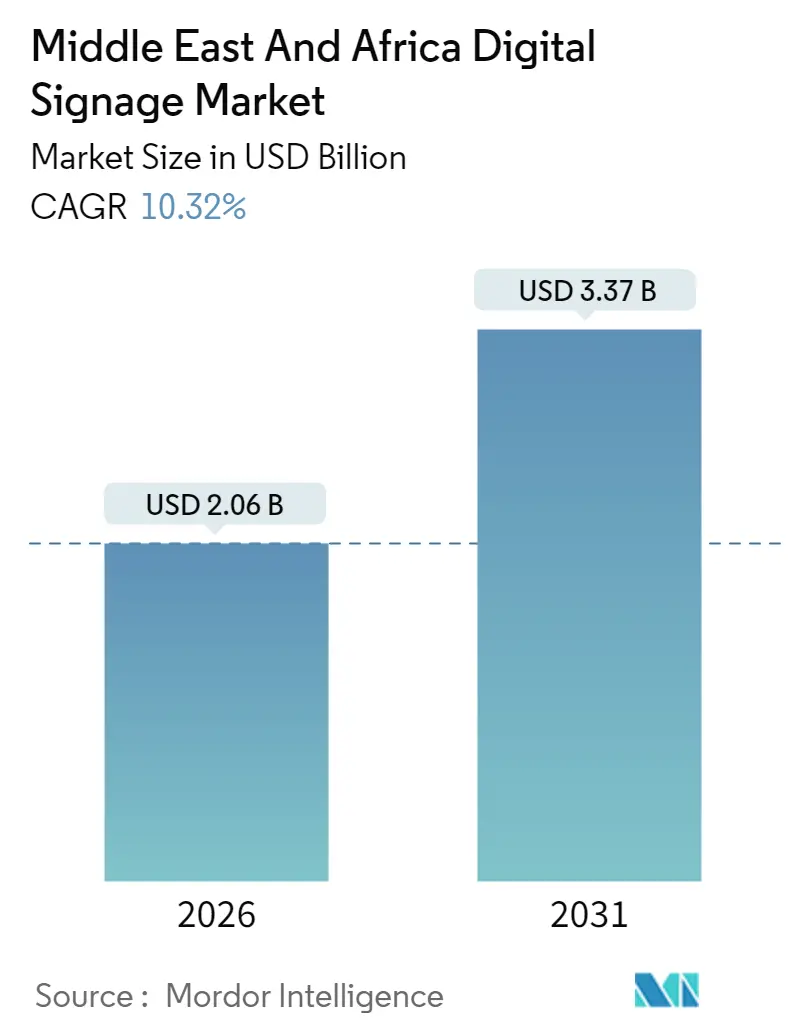

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Digital Signage Market Analysis by Mordor Intelligence

The Middle East and Africa digital signage market is expected to grow from USD 1.87 billion in 2025 to USD 2.06 billion in 2026 and is forecast to reach USD 3.37 billion by 2031 at 10.32% CAGR over 2026-2031. Government smart-city programs, pilgrimage-driven seasonal spikes, and accelerating retail digitization reinforce the growth momentum that places the region among the fastest-expanding digital signage arenas worldwide. Religious tourism in Saudi Arabia, combined with large-format display rollouts in malls across the Gulf Cooperation Council, generates buying cycles that differ markedly from Western demand patterns. Sovereign technology initiatives embed displays into traffic control, healthcare, and public-safety systems, while local integrators gain traction with Arabic content localization and extreme-weather hardware adaptations. Hardware prices for mid-sized LED panels fell 15% in 2024, easing entry barriers for African retailers and public agencies. Meanwhile, software-as-a-service models shift the customer focus from capital expenditure to predictable operating expenses, thereby raising adoption among smaller venue operators.

Key Report Takeaways

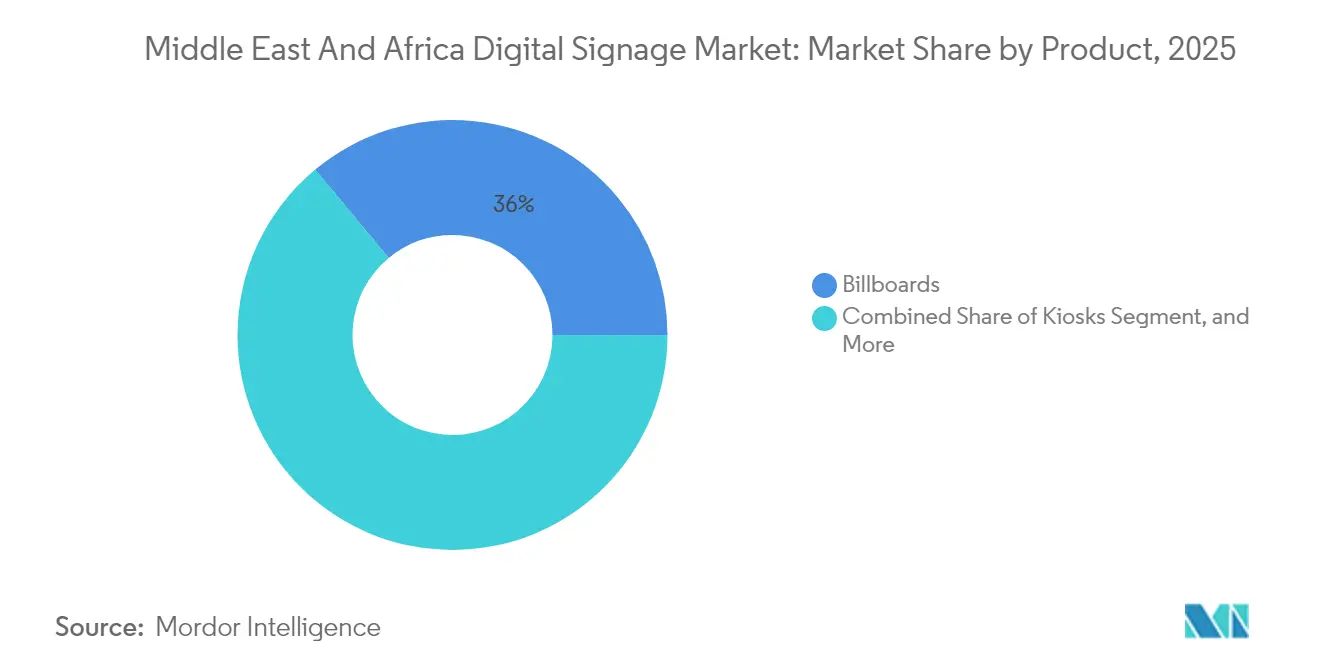

- By product, billboards led with a 36.02% share of the Middle East and Africa digital signage market in 2025, while kiosks recorded the fastest growth at a 12.48% CAGR through 2031.

- By type, hardware commanded 66.12% of the Middle East and Africa digital signage market size in 2025, whereas services are expected to advance at an 11.35% CAGR through 2031.

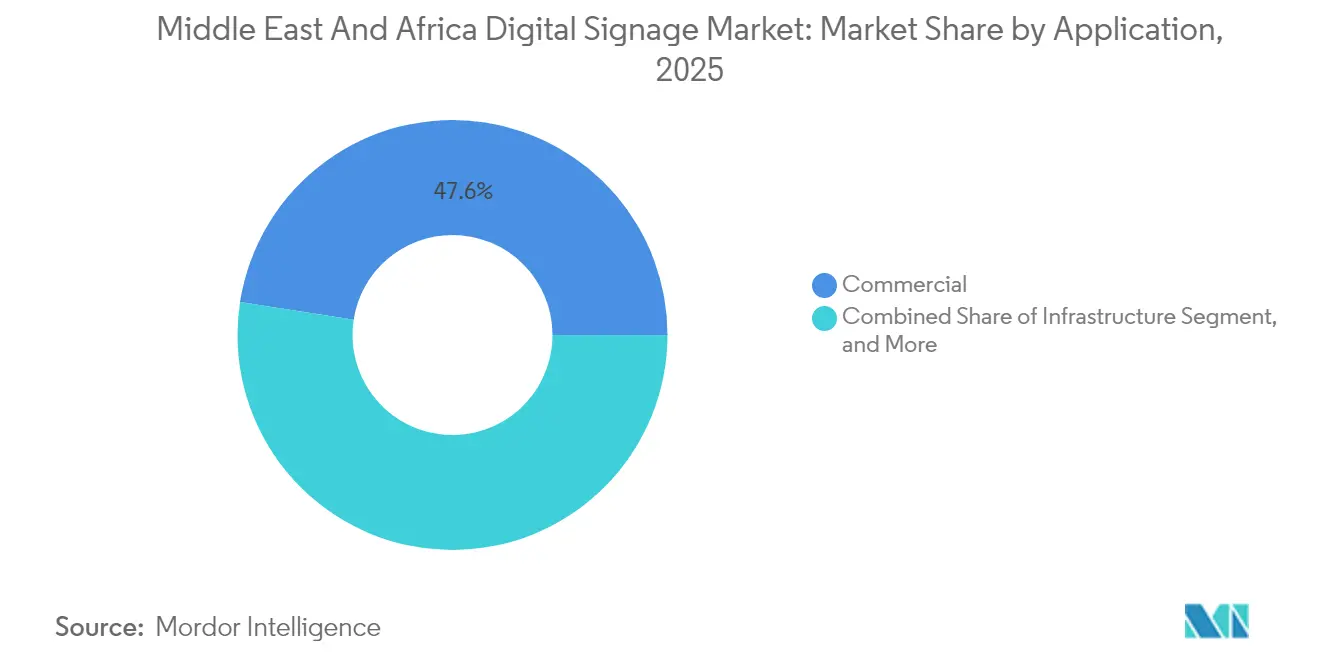

- By application, commercial deployments accounted for 47.55% of the Middle East and Africa digital signage market revenue in 2025, while infrastructure projects are expected to accelerate at a 12.68% CAGR through 2031.

- By display technology, LED retained a 48.45% share of the Middle East and Africa digital signage market in 2025, and OLED grew at a 12.34% CAGR through 2031.

- By region, the Middle East captured 63.72% of the value of the Middle East and Africa digital signage market in 2025, whereas Africa is projected to post the strongest CAGR of 11.69% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Digital Signage Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid retail roll-out of large-format LED and OLED screens | +2.1% | Middle East core, spill-over to North Africa | Medium term (2-4 years) |

| Government smart-city digital infrastructure programs | +2.8% | GCC countries, Egypt, South Africa | Long term (≥ 4 years) |

| Falling display pixel-USD cost | +1.9% | Global | Short term (≤ 2 years) |

| Brand owners' shift to data-rich DOOH campaigns | +1.6% | Urban centers across MEA | Medium term (2-4 years) |

| Pilgrimage-driven demand spikes in Mecca and Medina | +1.4% | Saudi Arabia, regional spillover | Long term (≥ 4 years) |

| AI-enabled Arabic audience analytics platforms | +1.2% | Arabic-speaking regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Retail Roll-out of Large-Format LED and OLED Screens

Retail chains across the Gulf continuously replace static posters with high-brightness LED walls that withstand daytime temperatures of up to 50 °C without color washout. Subway introduced self-order kiosks and an anamorphic screen at Dubai Mall, trimming queue time by 40% and cutting yearly menu-reprint costs by USD 100–200 per outlet.[1]Digital Signage Today Staff, “Subway Launches First Self-Order Kiosks and Anamorphic Screen in EMEA at Dubai Mall,” digitalsignagetoday.com Mid-sized panel prices fell 15% in 2024, making large-format displays more affordable for specialty stores that had previously shied away from capital-intensive upgrades. GCC developers plan to create 3.9 million m² of new retail space by 2028, generating persistent demand for content-ready screens optimized for Arabic and English messaging. African supermarkets further the trend by adopting energy-efficient LED menu boards that slice power bills by 20% and recoup investments in under three years.

Government Smart-City Digital Infrastructure Programs

Saudi Arabia, the UAE, and Qatar designate digital signage as core city infrastructure connecting traffic alerts, emergency broadcasts, and tourism information. The Kingdom budgets USD 1.18 trillion for integrated transport and hospitality corridors that embed outdoor-rated displays into roadsides, metro stations, and pilgrimage routes.[2]Government Communications Office, “Digital Transformation Strategy,” gov.qa Egypt’s National Strategy for Smart Cities installs unified content networks in new administrative capitals, while South Africa pilots display-equipped bus shelters to streamline commuter updates. Kenya’s Konza Technopolis hosts a local assembly of commercial panels, reducing logistics costs and customs delays, and providing African buyers with faster service turnarounds. Emerging standards for brightness, cybersecurity, and Arabic typography flow from these state programs and now shape vendor product roadmaps.

Pilgrimage-Driven Demand Spikes in Mecca and Medina

Annual pilgrim inflows exceeding 10 million elevate temporary screen demand in the holy cities, where multilingual way-finding and crowd-control graphics must survive dust storms and 24-hour operation. Operators deploy modular LED to handle year-round advertising and pivot to safety messaging during Hajj peaks, capturing incremental rentals that push utilization rates above 80%. Hardware fleets are engineered with redundant power supplies and sealed enclosures that resist sand infiltration, a specification later exported to wide-open highways in Egypt and Oman. Local integrators specialize in rendering Quran verses and right-to-left animation flows, giving them an edge over global firms that are less attuned to liturgical nuances.

AI-Enabled Arabic Audience Analytics Platforms

Fanar AI, Microsoft’s JAIS LLM, and Sodaclick deliver real-time gender, age, and mood detection in Modern Standard Arabic and dialects, raising ad engagement by double-digit percentages. Retailers trigger dynamic promotions when family groups approach, while transit authorities automatically switch to evacuation directions if crowd density exceeds safety thresholds. AI localization engines cut manual translation lead times from days to minutes, improving campaign agility during Ramadan or National Day events. Privacy-compliant edge processing keeps sensitive facial data onsite, aligning with Gulf cybersecurity mandates. Subscription-based analytics lift the services segment’s CAGR by turning one-off deployments into recurring insight contracts.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex and TCO for outdoor networks | -1.8% | Africa core, smaller Middle East markets | Short term (≤ 2 years) |

| Fragmented regional standards and content rules | -1.3% | Cross-border deployments, multi-country operators | Medium term (2-4 years) |

| Cyber-security and vandalism risks for public screens | -1.1% | Urban centers, high-traffic areas | Long term (≥ 4 years) |

| Extreme heat and dust driving maintenance costs | -0.9% | Desert regions, outdoor installations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex, Weather Exposure, and Ownership Costs

Outdoor-rated units cost 40–60% more than indoor equivalents because they integrate sealed aluminum housings, high-lumen LED, and reinforced anti-vandal glass. African buyers face additional hurdles due to patchy grid power and limited broadband coverage, which increases the costs of generators and cellular modems. Samsung’s CVE-2024-7399 advisory highlights new cyber-patch workloads that extend the payback cycles for budget-strapped municipalities.[3]Samsung Security Center, “CVE-2024-7399 Digital Display Vulnerability Advisory,” security.samsung.com In desert belts, fan filters clog within months, forcing quarterly service visits that elevate maintenance contracts by 25%. Managed service leasing models spread the burden, but cannot offset the steep upfront installation permits and import duties on hardware in Nigeria or Tanzania.

Fragmented Standards, Content Regulation, and Security Vulnerabilities

Operators spanning GCC, North Africa, and sub-Saharan Africa juggle conflicting rules on brightness caps, prayer-time advertising, and Arabic calligraphy sizing. Some jurisdictions require prior clearance from a censorship board, while others enforce data-sovereignty laws that prohibit cloud storage across borders. HKCERT’s 2024 study uncovered 20 unpatched web portals on public-facing display controllers, underscoring the need for region-specific security credentials. Divergent electromagnetic compliance codes force manufacturers to keep multiple SKU variants, hindering economies of scale. Marketing agencies must budget 15–20% extra for voice-over and dialect revision cycles, which can slow down multi-country campaign launches and dampen the network effect that drives programmatic DOOH adoption.

Segment Analysis

By Product: Interactive Kiosks Drive Next-Generation Engagement

Billboards accounted for 36.02% of the Middle East and Africa digital signage market value in 2025, reflecting the entrenched demand for outdoor media along GCC expressways and North African city arteries. Kiosks, however, are projected to post a 12.48% CAGR through 2031 as retailers and transport hubs pivot to touchless self-service, which cuts staffing costs and delivers bilingual guidance. The Middle East and Africa digital signage market size associated with kiosk deployments is projected to increase steadily as sensor prices decline. Momentum is particularly strong in Saudi malls where AI engines upsell pilgrimage merchandise, lifting basket sizes by 15%.

Adopters favor antimicrobial glass and gesture control to address hygiene concerns that have been amplified during the pandemic years. Software overlays integrate loyalty programs and digital wallets, boosting repeat visits. Smaller African airports are introducing multilingual way-finding kiosks that eliminate the need for printed signage refreshes and streamline passenger flow. Local content studios gain business by crafting culturally sensitive avatars that greet users in Arabic, Swahili, or Amharic, a nuance that global template vendors often overlook.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Services Segment Accelerates Amid Platform Shift

Hardware delivered 66.12% of the revenue in 2025, yet its growth pace lags behind service subscriptions, which expand at an annual rate of 11.35%. Regional buyers are increasingly leasing screens that come bundled with managed content, predictive maintenance, and AI analytics. The Middle East and Africa digital signage market benefits from this shift as smaller retailers defer hefty upfront investment. Samsung’s SmartThings Pro plugs display into wider IoT stacks, allowing energy savings of 15% through remote dimming.

Media players adopt system-on-chip designs that reduce installation labor and minimize failure points. Meanwhile, software vendors preload Arabic fonts and right-to-left UX libraries, slashing localization overhead. African resellers package data SIMs, solar-ready power kits, and vandal-proof housings under monthly fees that align with tight municipal budgets. These offerings expand the addressable opportunities beyond premium malls to secondary cities and rural bus stations, broadening the footprint of the Middle East and Africa digital signage market.

By Application: Infrastructure Investments Fuel Growth Beyond Commercial Dominance

Commercial venues still contributed 47.55% of the turnover in 2025, as quick-service restaurants, fashion chains, and corporate lobbies modernized their visual communication. Infrastructure deployments, however, book the highest 12.68% CAGR because ministries view displays as mission-critical for transport updates, safety alerts, and e-government outreach. The Middle East and Africa digital signage market size tied to infrastructure roll-outs is projected to widen sharply as metro expansions in Riyadh, Doha, and Cairo demand ruggedized, sunlight-readable panels.

Industrial complexes install digital scoreboards and machine-status dashboards to prevent downtime and enhance worker safety. Hospitals deploy patient-queuing screens that reduce perceived wait times by 30%, while universities stream lecture schedules and emergency notices campus-wide. Content management suites incorporate ISO-based uptime metrics to satisfy public-sector procurement clauses, steering private developers toward enterprise-grade platforms.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Display Technology: OLED Emergence Challenges LED Dominance

LED retained a 48.45% revenue share in 2025, favored for its 6,000-nit brightness and modular maintenance that suits desert climates. The Middle East and Africa digital signage market is driving the adoption of LED walls for outdoor arenas, road furniture, and sponsorship arches at pilgrimage checkpoints. OLED accelerates at 12.34% CAGR as luxury boutiques and corporate atriums crave near-black contrast and wafer-thin curvature.

Samsung’s Color Paper e-ink launch targets shelf-edge and way-finding settings where glare-free readability takes precedence over motion video. LCD remains a budget staple for indoor corporate communications, while mini-LED bridges cost and performance gaps, gaining uptake in African casinos and sports bars. Screen makers develop heat-dissipation chambers and UV-resistant coatings that extend the mean-time-between-failure beyond 60,000 hours, ensuring operators of lower lifetime costs despite higher sticker prices.

Geography Analysis

Saudi Arabia, the UAE, and Qatar collectively anchor the Middle East and Africa digital signage market with mature 5G backbones and proactive policy incentives. Riyadh’s Vision 2030 utilizes display networks in road tunnels, airport aprons, and Hajj transport nodes, where multilingual guidance reduces congestion and enhances pilgrim safety. Dubai’s USD 435 million domestic display spend thrives on data-rich DOOH inventory that provides real-time audience metrics to brand owners. Abu Dhabi aligns civic way-finding kiosks with a single CMS, which reduces content-update labor by 40%. Qatar’s Vision 2030 extends similar omnichannel frameworks across Education City, Lusail Stadium precincts, and metro interchanges, embedding procurement rules that favor energy-efficient, Arabic-first UI designs. Africa’s acceleration originates in Kenya’s Konza Technopolis, where 17 Korean companies assembled a USD 1.4 million electronics cluster, localizing digital signage hardware and creating 200 skilled jobs. The plant trims shipment time for large-format modules from 12 to 3 weeks, an advantage embraced by Nairobi retailers seeking rapid refresh cycles. South Africa leverages established fiber corridors to roll out 4K LED displays along Gautrain stations, monetizing commuter eyeballs with programmatic feeds synchronized to smartphone push notifications. Egypt’s smart-city roadmap incorporates solar-powered road signs that automatically switch to emergency broadcasts during sandstorm alerts, demonstrating public-safety integration beyond mere advertising. Nigeria’s population-dense Lagos and Abuja corridors attract foreign out-of-home investors despite power grid constraints, signaling a long-term upside for the Middle East and Africa digital signage market once infrastructure bottlenecks ease.

Regional gaps persist. Morocco, Oman, and Tanzania still rely on import-only supply chains, which can elevate landed costs by up to 25%. In response, assemblers in Dubai’s Jebel Ali Free Zone and Egypt’s Port Said offer bonded-warehouse kitting that circumvents multi-country tax layers. Pan-African regulatory bodies explore common standards for brightness, encryption, and emergency override to smooth cross-border transactions, a reform that could shave deployment lead times by two months and fuel the next chapter of the Middle East and Africa digital signage market expansion.

Competitive Landscape

Samsung, LG, and Sony together anchor technology leadership, contributing more than 45% of regional panel shipments in 2024. Samsung leverages its SmartThings Pro suite to bundle screens with IoT dashboards, drawing hospitality and healthcare clients that value ecosystem integration. The firm’s TV Plus expansion into Egypt and the UAE widens its content footprint, allowing advertisers to blend broadcast and place-based feeds within a single buying plan. LG targets KRW 10 trillion B2B revenue by 2030, emphasizing OLED poster walls and transparent displays that appeal to luxury malls and airport lounges.[4]LG Electronics, “LG Showcases B2B Solutions at Middle East and Africa Showcase 2024,” lgnewsroom.com Sony concentrates on high-brightness Crystal LED for flagship auditoriums but partners with local integrators for Arabic menu software, sidestepping cultural adaptation pitfalls.

Below the top tier, PPDS, Sharp NEC, and Hikvision compete for niche categories, ranging from DVLED tunnels to surveillance-linked passenger information screens. PPDS unveiled its modular Wave cloud CMS via Dubai partner events, courting resellers that crave fleet-wide remote management without deep coding skills. Sharp NEC pairs entrance-flow sensors with displays to hand retailers heat-map data, once limited to e-commerce. Hikvision cross-sells signage as part of security contracts, bundling vandal-proof housings and cybersecurity hardening into turnkey quotes.

Local specialists such as Red Solutions (Saudi Arabia), Almoe (UAE), and Iconic Media (South Africa) thrive on Arabic localization, dust-proof enclosure retrofits, and 24/7 on-site maintenance SLAs. Their intimate knowledge of prayer-time advertising restrictions and municipality permit workflows shortens rollout cycles by up to 30% compared with global rivals. Content studios like Rawa.ai pivot toward generative Arabic copywriting and dialect testing, forging SaaS alliances that boost margins and lock in customers. The competitive field thus combines the scale advantages of multinationals with the cultural agility of regional players, sustaining a dynamic yet moderately concentrated Middle East and Africa digital signage market.

Middle East And Africa Digital Signage Industry Leaders

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Sharp NEC Display Solutions, Ltd.

Sony Group Corporation

Koninklijke Philips N.V. (Philips Professional Displays)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Samsung marked its 15th consecutive year as the global digital signage leader and expanded Samsung TV Plus integration across Middle Eastern screens, underscoring a shift from standalone hardware to a comprehensive content ecosystem.

- August 2025: LG moved closer to its KRW 10 trillion (USD 8.4 billion) B2B revenue goal for 2030, scaling up plants in Saudi Arabia and Egypt to meet the accelerating demand for regional signage projects.

- July 2025: Under Vision 2030, Qatar stepped up multilingual, AI-driven display rollouts in transit hubs and government sites, improving real-time citizen information services.

- June 2025: Kenya’s Konza Technopolis attracted additional backing from Samsung, LG, and other Korean firms, expanding local electronics manufacturing and strengthening East Africa’s signage supply chain.

Middle East And Africa Digital Signage Market Report Scope

The study characterizes the Middle East and Africa digital signage market based on product, applications, and type, such as hardware, software, and services. The study is limited to products that are offered by the majority of vendors with a range of applications in end users, such as commercial, industrial, institutional, and infrastructure, among others. The scope of the study is currently focused on key countries in the region, such as Saudi Arabia, the United Arab Emirates, and South Africa, among others.

By Product

| Kiosks |

| Menu Boards |

| Billboards |

| Sign Boards |

| Other Products |

By Type

| Hardware | Displays (LCD/LED, OLED) |

| Projection Equipment | |

| Media Players | |

| Other Hardware | |

| Software | |

| Services |

By Application

| Commercial |

| Industrial |

| Institutional |

| Infrastructure |

| Other Applications |

By Display Technology

| LCD |

| LED |

| OLED |

| e-Paper |

By Region

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product | Kiosks | |

| Menu Boards | ||

| Billboards | ||

| Sign Boards | ||

| Other Products | ||

| By Type | Hardware | Displays (LCD/LED, OLED) |

| Projection Equipment | ||

| Media Players | ||

| Other Hardware | ||

| Software | ||

| Services | ||

| By Application | Commercial | |

| Industrial | ||

| Institutional | ||

| Infrastructure | ||

| Other Applications | ||

| By Display Technology | LCD | |

| LED | ||

| OLED | ||

| e-Paper | ||

| By Region | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Middle East and Africa digital signage market in 2026?

The Middle East and Africa digital signage market size is USD 2.06 billion in 2026, on track for USD 3.37 billion by 2031.

Which product category is growing fastest in the region?

Interactive kiosks lead growth with a projected 12.48% CAGR through 2031 as retailers and transport hubs adopt touchless self-service.

Why are smart-city projects important to digital signage adoption?

Government smart-city programs embed displays into traffic, safety, and citizen-service systems, adding 2.8% to the forecast CAGR.

What share do LED screens hold today?

LED accounts for 48.45% of revenue in 2025 owing to brightness and durability advantages in extreme heat.

Which geography is expanding quickest?

Africa is the fastest-growing territory, advancing at an 11.69% CAGR as telecom and power upgrades unlock new deployments.

How are vendors addressing Arabic content requirements?

Suppliers integrate AI-based Arabic NLP and dialect localization tools that generate culturally accurate messaging and boost engagement.