Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

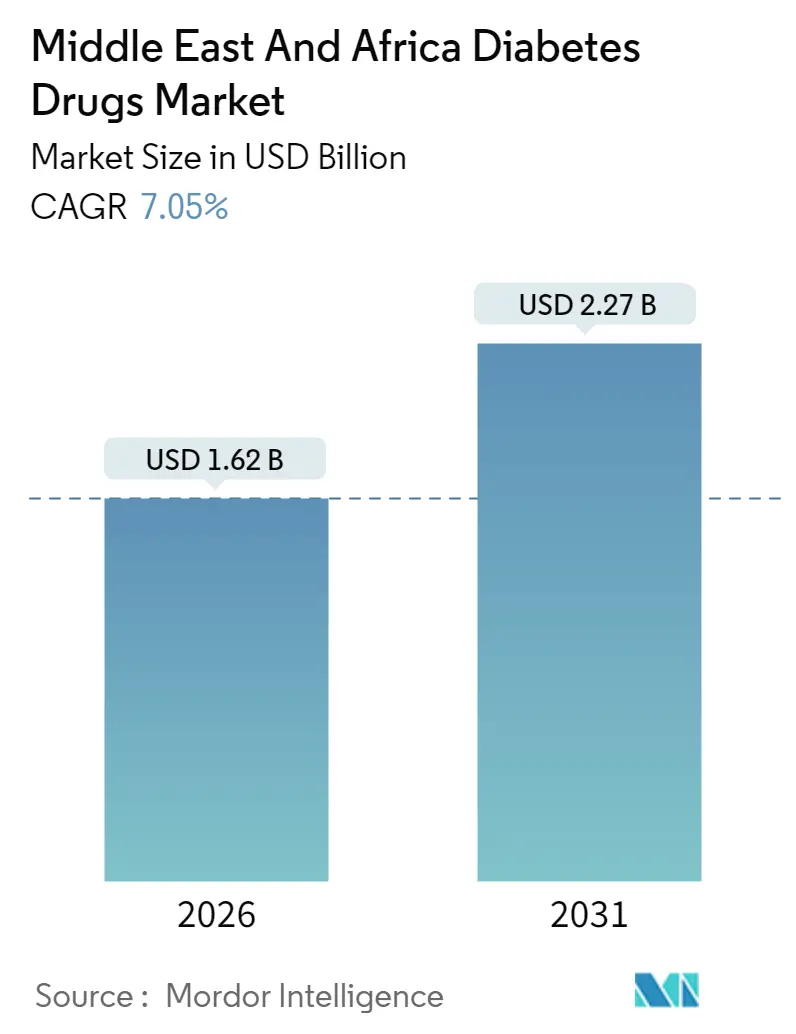

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Diabetes Drugs Market Analysis by Mordor Intelligence

Middle East and Africa diabetes drugs market size in 2026 is estimated at USD 1.62 billion, growing from 2025 value of USD 1.51 billion with 2031 projections showing USD 2.27 billion, growing at 7.05% CAGR over 2026-2031. Accelerating prevalence of type 2 diabetes, rising obesity rates, and the expanding pool of younger, urban patients are generating durable demand. Government localization mandates in Saudi Arabia and Egypt, coupled with the UAE’s fast-track approval pathways, are stimulating domestic production of insulin and novel injectables. Premium GLP-1 receptor agonists such as oral semaglutide and once-weekly tirzepatide are gaining traction among insured Gulf Cooperation Council (GCC) populations, while price-sensitive segments in Sub-Saharan Africa continue to rely on human insulin supplied through new public-private partnerships. Meanwhile, e-pharmacy platforms are changing how patients obtain medications, and real-world evidence from regional studies is guiding physicians toward earlier initiation of combination therapy.

Key Report Takeaways

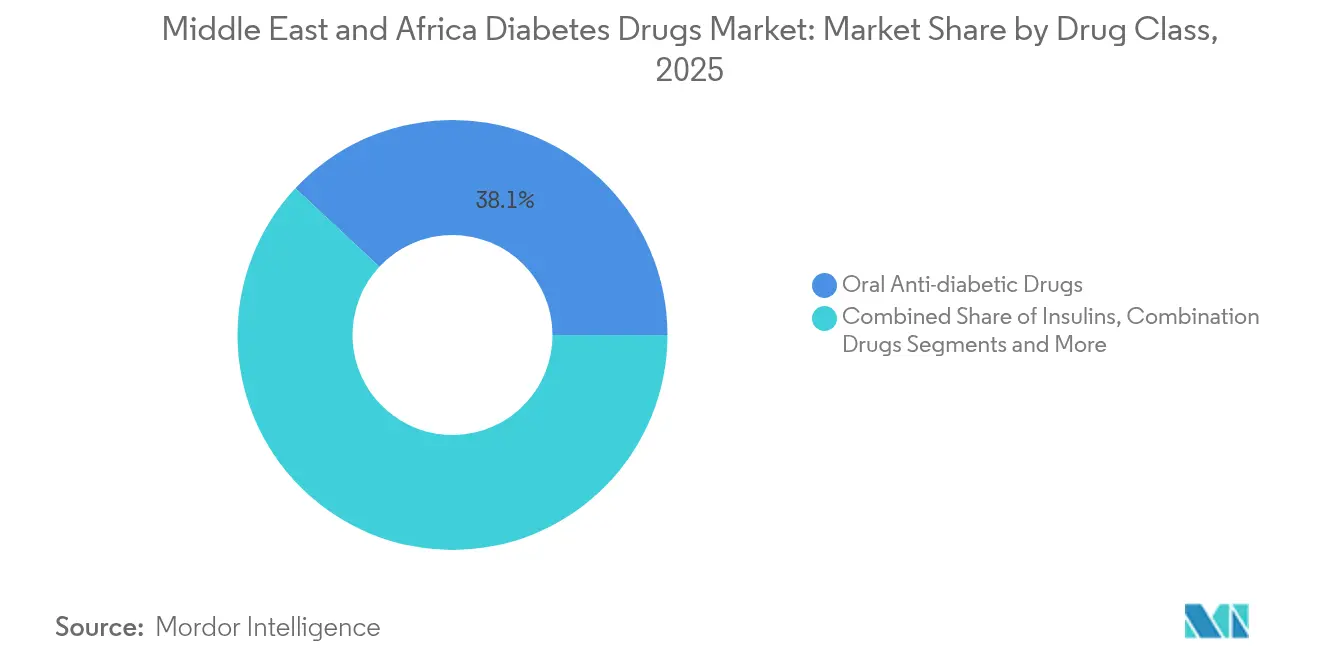

- By therapy class, oral anti-diabetic drugs led with 38.05% revenue share in 2025, while non-insulin injectables are forecast to expand at a 8.98% CAGR through 2031.

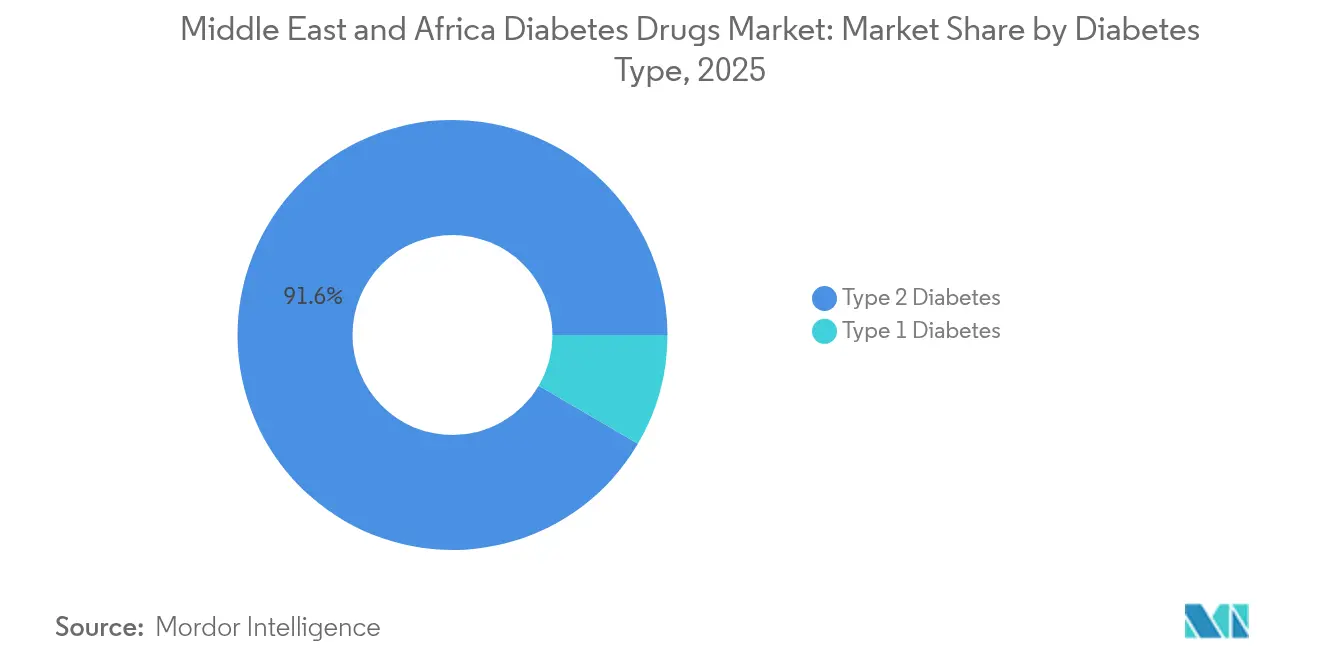

- By diabetes type, type 2 diabetes commanded 91.55% of the Middle East and Africa diabetes drugs market share in 2025 and is projected to grow at an 8.21% CAGR to 2031.

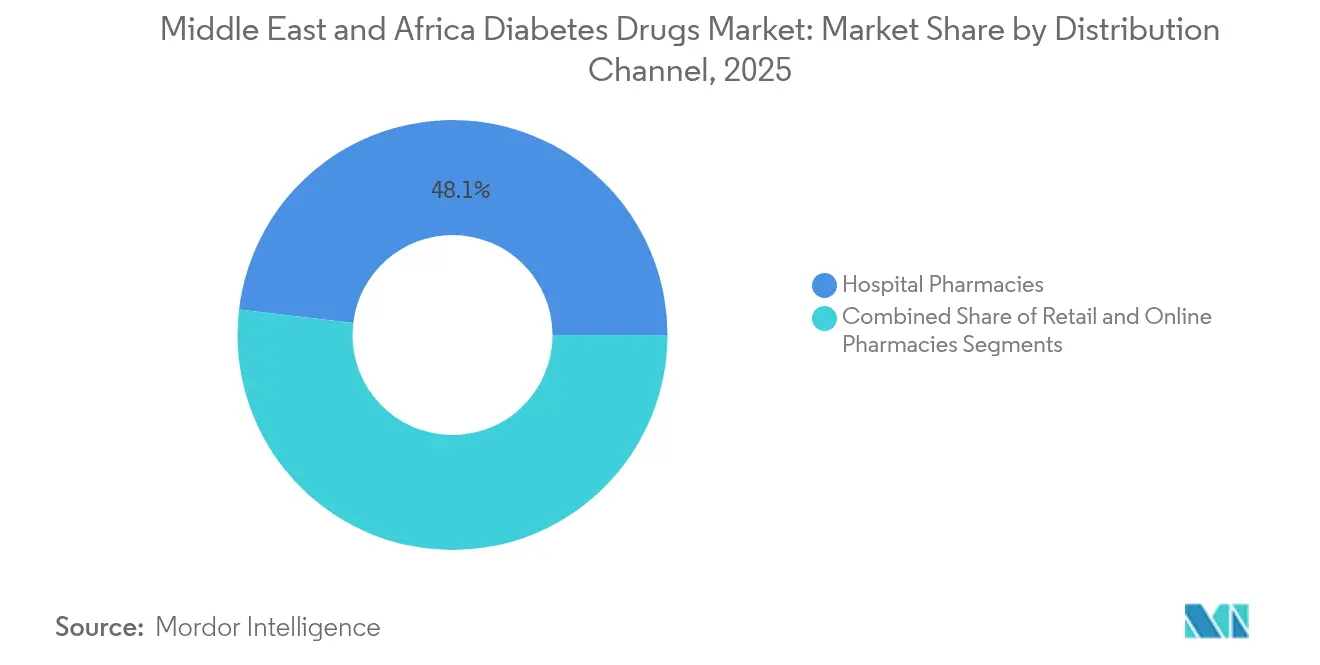

- By distribution channel, hospital pharmacies held 48.10% of the Middle East and Africa diabetes drugs market size in 2025, whereas online pharmacies are advancing at an 11.05% CAGR through 2031.

- By geography, Saudi Arabia accounted for 29.60% of revenue in 2025; the UAE shows the fastest momentum with an 8.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes & obesity | +1.8% | GCC, Egypt | Long term (≥ 4 years) |

| Government initiatives for improving diabetic medication access | +1.2% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2-4 years) |

| Expanding health insurance coverage in GCC | +0.9% | GCC | Medium term (2-4 years) |

| Rapid growth of e-pharmacy platforms | +0.6% | GCC, South Africa | Short term (≤ 2 years) |

| Growing adoption of fixed-dose combinations | +0.7% | GCC | Short term (≤ 2 years) |

| Emergence of low-cost generic/biosimilar medications | +1.1% | Sub-Saharan Africa, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Obesity

Newly published 2024 hospital registry updates confirm double-digit diabetes prevalence across GCC states, with Saudi clinics reporting baseline HbA1c readings above 10% in incoming patients, underscoring the severity of metabolic deterioration.[1]Elsevier, “Oral Semaglutide Effectiveness in Real-World Practice,” deman.elsevier.com Urban migration, dietary westernization, and sedentary work patterns continue to raise body-mass indices, lengthening lifetime treatment duration. The trend is spreading southward as processed foods penetrate major African cities where healthcare access is fragmented. For pharmaceutical companies, this enlarges the addressable population for basal insulin, GLP-1 agonists, and emerging once-weekly pills. It also strengthens the case for preventive public-health spending, which in turn supports formularies covering weight-control agents.

Government Initiatives for Improving Diabetic Medication Access

Saudi Arabia’s National Unified Procurement Company (NUPCO) signed ten memoranda of understanding with multinational manufacturers in October 2024 to localize insulin and GLP-1 production, improving supply security while meeting Vision 2030 objectives. Egypt followed suit in December 2024 when Eli Lilly and EVA Pharma launched the first domestically produced insulin glargine, targeting one million patients by 2030. In the UAE, the 2025 Federal Decree-Law No. 38 sets conditional approval pathways and mandatory pharmacovigilance, shortening the time to market for innovative molecules.[2]UAE Government, “Federal Decree-Law Governing Medical Products, Pharmacists and Pharmaceutical Establishments,” uaelegislation.gov.aeCollectively, these policies reduce import dependence, enforce quality standards, and foster technology transfer, making locally sourced biologics more affordable.

Expanding Health Insurance Coverage in GCC

Comprehensive insurance mandates are reshaping buying power. A 2024 real-world tirzepatide study in an Arab cohort showed that 64.1% of insured patients achieved HbA1c targets below 7% within 40 weeks despite the drug’s premium price point.[3]Elsevier, “Oral Semaglutide Effectiveness in Real-World Practice,” deman.elsevier.comAs Gulf payers broaden diabetes formularies, innovative therapies experience faster uptake, allowing manufacturers to maintain value-based pricing while reducing out-of-pocket expenditures for nationals and expatriates alike. Wider coverage also drives adherence because patients can afford continuous glucose-monitoring (CGM) sensors and follow-up consultations. For multinational firms, it signals a shift away from volume-driven tender models toward outcomes-driven contracting.

Rapid Growth of e-Pharmacy Platforms

Saudi Arabia’s clarification of online dispensing rules in 2024 enabled fully licensed e-pharmacies to cover the complete reimbursement spectrum, propelling penetration from single digits pre-COVID to more than half of repeat prescriptions today. Similar reforms are being drafted in Qatar and Bahrain, unlocking regional scale for digital platforms. Patients appreciate home delivery, discreet counseling, and automated refill reminders, attributes that are particularly valuable for chronic diseases. Health-tech start-ups now integrate e-pharmacies with remote endocrinology consults, creating data ecosystems that support personalized titration algorithms. For wholesalers, online channels reduce last-mile costs and improve demand-forecast accuracy.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of novel therapies | -1.4% | Sub-Saharan Africa, Egypt | Long term (≥ 4 years) |

| Counterfeit drugs in informal channels | -0.5% | Conflict-affected markets | Short term (≤ 2 years) |

| Cold-chain gaps in rural Sub-Saharan Africa | -0.8% | Sub-Saharan Africa | Medium term (2-4 years) |

| Physician inertia to intensify therapy | -0.9% | Region-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Novel Therapies

Even as the Middle East and Africa diabetes drugs market expands, affordability gaps widen between affluent GCC consumers and low-income groups in Sub-Saharan Africa. A 2025 qualitative assessment across Ethiopian primary-care clinics found that constrained household budgets, scarce insurance options, and limited device availability continue to hamper optimal care, especially for insulin-requiring patients. Nigerian field interviews completed in June 2024 revealed that more than 80% of respondents considered branded medication prices prohibitive, steering them toward older generics. Consequently, manufacturers must craft tiered-pricing and donation programs while governments seek bulk-procurement partnerships to bridge therapeutic inequality.

Counterfeit Drugs in Informal Channels

Conflict-affected zones remain fertile ground for substandard antidiabetic products. A May 2025 study examining supply routes into Yemen documented that up to 60% of sampled medicines failed regulatory specifications, putting patients at risk of treatment failure and complications. Smugglers exploit porous borders and shortages of fully licensed pharmacies, undermining trust in legitimate brands. Health authorities are responding with barcode-based track-and-trace systems and mobile-app verification. For multinational companies, stronger serialisation requirements raise compliance costs but protect market share by assuring product integrity.

Segment Analysis

By Therapy Class: Injectables Erode Oral Dominance

Non-insulin injectables are projected to grow at 8.98% annually, gradually eating into the 38.05% share that oral drugs held in 2025. The shift became evident when Saudi clinicians documented a 3.1% mean HbA1c decline and a 19.7% BMI reduction six months after initiating oral semaglutide in routine practice. The Middle East and Africa diabetes drugs market size for non-insulin injectables is expected to climb at double the pace of basal insulin because payers are linking reimbursement to weight management and cardiovascular outcomes. Weekly tirzepatide therapy replicated pivotal-trial efficacy in a 2024 UAE cohort, with nearly two-thirds of patients achieving glycemic targets inside 40 weeks. These results embolden regional formularies to list premium GLP-1/GIP co-agonists earlier in treatment algorithms.

GLP-1 demand is also spreading south as Novo Nordisk and Aspen begin local insulin cartridge production in South Africa, freeing capacity to import incretin mimetics into neighboring markets. Fixed-dose tablets that combine metformin with DPP-4 inhibitors are positioned for short-term uptake because they simplify regimens for multi-morbid elderly patients. Ramadan-specific adherence research, such as the 2025 O-SEMA-FAST study, is informing culturally tailored prescribing patterns during fasting periods. Overall, competition is intensifying as biosimilar GLP-1s approach patent expiry in the late 2020s, at which point low-cost regional manufacturers plan to launch.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Diabetes Type: Type 2 Shapes Long-Term Demand

Type 2 diabetes represented 91.55% of total cases in 2025, reinforcing its status as the cornerstone of commercial forecasting. The Middle East and Africa diabetes drugs market size for type 2 therapies is forecast to expand at an 8.21% CAGR thanks to earlier screening, wider CGM use, and employer-sponsored wellness schemes. Saudi registry data collected in 2024 reveal baseline HbA1c readings above 10%, validating physician calls for quicker intensification. In Egypt, domestic insulin glargine production is expected to lower unit prices, which could lift adherence among nearly 11 million diagnosed adults.

Type 1 diabetes, though a smaller segment, remains clinically complex and cost intensive. The 2024 GCC endocrine consensus supports early adoption of hybrid closed-loop insulin pumps for children, but rollout depends on reimbursement approvals and skilled nursing staff. Teplizumab gained UAE compassionate-use clearance in late 2024, offering the first disease-modifying option for at-risk relatives. Market participants expect uptake to concentrate in tertiary centres before broadening once diagnostic antibody testing becomes routine.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Omnichannel Dispensing Gains Ground

Hospital pharmacies held 48.10% of the Middle East and Africa diabetes drugs market share in 2025 as they handle complex titration cases and insurance pre-authorisations. Yet online outlets, expanding at an 11.05% CAGR, are the standout growth story. GCC legislation enacted in 2024 clarified cold-chain carriage, mandatory pharmacist counselling, and patient-data privacy requirements, energising venture-backed platforms to aggregate supply. Early adopters value doorstep delivery of sensors and pens, especially during extreme summer temperatures.

Retail chains are pivoting to click-and-collect models and subscription-based refill packs, while wholesalers deploy predictive-analytics dashboards that feed electronic medical records. Ethiopia’s 2024 affordability survey highlights how flexible payment options at community pharmacies can cushion out-of-pocket shocks for families facing inflationary pressure. Combined, these shifts forge a hybrid ecosystem where patients initiate complex regimens in hospitals, refill through e-pharmacies, and tap retail outlets for over-the-counter test strips.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Saudi Arabia remains the largest national market with a 29.60% revenue contribution in 2025. Vision 2030’s localisation clauses compel global manufacturers to establish fill-and-finish plants, and the Saudi Food and Drug Authority’s 2024 fast-track framework cuts dossier review time to 60 days for breakthrough therapies. Demand is further buoyed by public-sector insurance that reimburses CGM devices for citizens. As localisation scales, the Middle East and Africa diabetes drugs market could see a reduction in import costs that benefits neighbouring Gulf states through intra-GCC trade.

The UAE delivers the highest forward CAGR at 8.79%. Dubai’s health-tourism hub status and Abu Dhabi’s 2024 collaboration with Sanofi on AI-driven screening position the federation as the region’s innovation sandbox. Federal Decree-Law No. 38 of 2025 unifies pharmacovigilance and post-marketing surveillance, an important enabler for first-in-region launches of dual-agonist injectables.

South Africa anchors Sub-Saharan demand thanks to local insulin cartridge production that commenced in 2024 under a Novo Nordisk–Aspen venture. Egypt’s fast-growing population and newly built EVA Pharma insulin line broaden North-African self-sufficiency. Elsewhere, Nigeria and Kenya are piloting digital-wallet subsidy schemes that credit low-income patients each month, while conflict-affected areas grapple with counterfeit-medicine vigilance. Collectively, these developments reinforce geographical bifurcation: wealthier nations drive uptake of novel GLP-1s, and lower-income states concentrate on human insulin and generics.

Competitive Landscape

The Middle East and Africa diabetes drugs market exhibits moderate concentration as global innovators pair up with local contract manufacturers and distributors. Novo Nordisk leverages a South African fill-and-finish partnership to serve 4.1 million chronic users, simultaneously negotiating with NUPCO in Saudi Arabia for basal-insulin localisation. Eli Lilly’s December 2024 launch of domestically produced insulin glargine in Egypt through EVA Pharma underscores the competitive importance of local cost structure and Ministry of Health endorsement.

Regional champions Hikma and Julphar extend portfolios with biosimilar insulin and metformin-sitagliptin fixed combinations, addressing price-sensitive tender markets. Digital-health entrants such as Sihatech and Vezeeta integrate e-pharmacy, teleconsultation, and lab scheduling to capture data-driven revenue streams, making them attractive co-marketing partners for device makers. Sanofi’s 2024 agreement with Abu Dhabi’s Department of Health adds AI-powered rare-disease screening that could cross-pollinate diabetes-complication detection.

Overall competition is intensifying, yet intellectual-property cliffs for key GLP-1s after 2027 may trigger biosimilar price wars. Multinationals are therefore racing to bundle holistic solutions combining drugs, sensors, and software. Meanwhile, public procurement agencies push for dual sourcing to mitigate supply disruptions. Such dynamics solidify a landscape where top-five players control more than 65% of branded revenues, while a long tail of generics manufacturers dominates volume sales in lower-income territories.

.

Middle East And Africa Diabetes Drugs Industry Leaders

Astrazeneca

Eli Lilly

Sanofi

Novo Nordisk

Merck & Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: Eli Lilly and EVA Pharma secured Egyptian approval for locally manufactured insulin glargine, their first jointly produced insulin and a milestone toward supplying one million patients by 2030.

- June 2024: Abu Dhabi’s Department of Health and Sanofi signed a collaboration covering clinical research, patient recruitment, and AI-based screening for rare metabolic diseases, reinforcing the emirate’s role as a regional innovation hub.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Middle East & Africa diabetes drugs market as the value of prescription-strength agents, including insulins, oral antihyperglycemics, non-insulin injectables, and fixed-dose combinations, supplied through licensed channels to manage chronic hyperglycemia in type 1 and type 2 adults. Each therapy class is modeled in USD and standard units across Saudi Arabia, UAE, Iran, Egypt, Oman, South Africa, and the broader region.

Scope exclusion: glucose-monitoring devices, veterinary preparations, and nutraceuticals are outside the count.

Segmentation Overview

- By Therapy Class

- Oral Anti-diabetic Drugs

- Insulins

- Combination Drugs

- Non-Insulin Injectable Drugs

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- Saudi Arabia

- United Arab Emirates

- Oman

- Iran

- Egypt

- South Africa

- Rest of Middle East & Africa

Detailed Research Methodology and Data Validation

Primary Research

Interviews with endocrinologists, hospital pharmacists, and regulatory officers across GCC hubs, Egypt, and South Africa clarified real-world switching to weekly GLP-1s, insurer reimbursement ceilings, and parallel-trade leakages, allowing us to adjust channel splits and average selling prices.

Desk Research

Our analysts first screened open datasets from bodies such as the International Diabetes Federation, WHO mortality files, Gulf Cooperation Council health ministries, and customs trade records for insulin and metformin HS codes. Company 10-Ks, audited financials pulled via D&B Hoovers, and peer-reviewed journals on GLP-1 uptake patterns then sharpened prevalence, pricing, and uptake assumptions. Paid feeds, including Dow Jones Factiva for regional tender awards and Marklines for injectable-pen localization, helped trace competitive moves. The sources listed are illustrative; a wider pool was consulted during validation.

Market-Sizing & Forecasting

A transparent top-down reconstruction, including diabetic population, treated share, daily dose, and net ASP, anchors each therapy pool, while selective bottom-up supplier roll-ups on long-acting insulin pens check totals. Key variables include adult diabetes prevalence, per-capita drug spend, reimbursement coverage ratios, GLP-1 prescription penetration, average pack price, and import duty shifts. Multivariate regression on these drivers, followed by scenario analysis for obesity growth and formulary changes, generates the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs pass variance checks against IQVIA MAT audits and customs values, after which a senior reviewer signs off. We refresh models annually and trigger mid-cycle updates when policy or patent shocks occur.

Credibility Behind Mordor's Middle East And Africa Diabetes Drugs Treatment Baseline

Published estimates often diverge because firms track different geographies, bundle devices, or apply unmatched ASPs.

Key gap drivers include competitor models that fold in glucose sensors, limit scope to GCC only, or escalate totals by using global list prices without discount ladders, whereas Mordor's cadence favors annual field-price audits and full MEA country coverage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.51 B (2025) | Mordor Intelligence | - |

| USD 2.84 B (2024) | Global Consultancy A | Includes devices and pipeline therapies; revenue recognized at ex-factory list levels. |

| USD 1.25 B (2024) | Trade Journal B | Covers only GCC and South Africa; relies on retail audit sales, excludes hospital tenders. |

These contrasts show that Mordor's full-regional scope, field-validated ASPs, and routinely updated prevalence base offer the most balanced, reproducible starting point for strategic decisions.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Middle East and Africa diabetes drugs market?

The Middle East and Africa diabetes treatment market size was USD 1.62 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 7.05% CAGR, reaching USD 2.27 billion by 2031.

Which therapy class is growing the fastest?

Non-insulin injectables, led by GLP-1 receptor agonists, are advancing at a 8.98% CAGR.

Why are e-pharmacy platforms important for diabetes care in the region?

Regulatory reforms and consumer demand for home delivery are driving an 11.05% CAGR for online pharmacies, improving access to chronic medications

Which country leads the market and which grows the quickest?

Saudi Arabia holds the largest share at 29.60%, while the UAE records the highest growth at an 8.79% CAGR.

What are the main challenges facing market growth?

High prices of novel therapies and the circulation of counterfeit drugs in informal markets continue to restrict equitable access across lower-income patient populations.