Market Size of Middle East And Africa Defense Industry

| Study Period | 2019 - 2029 |

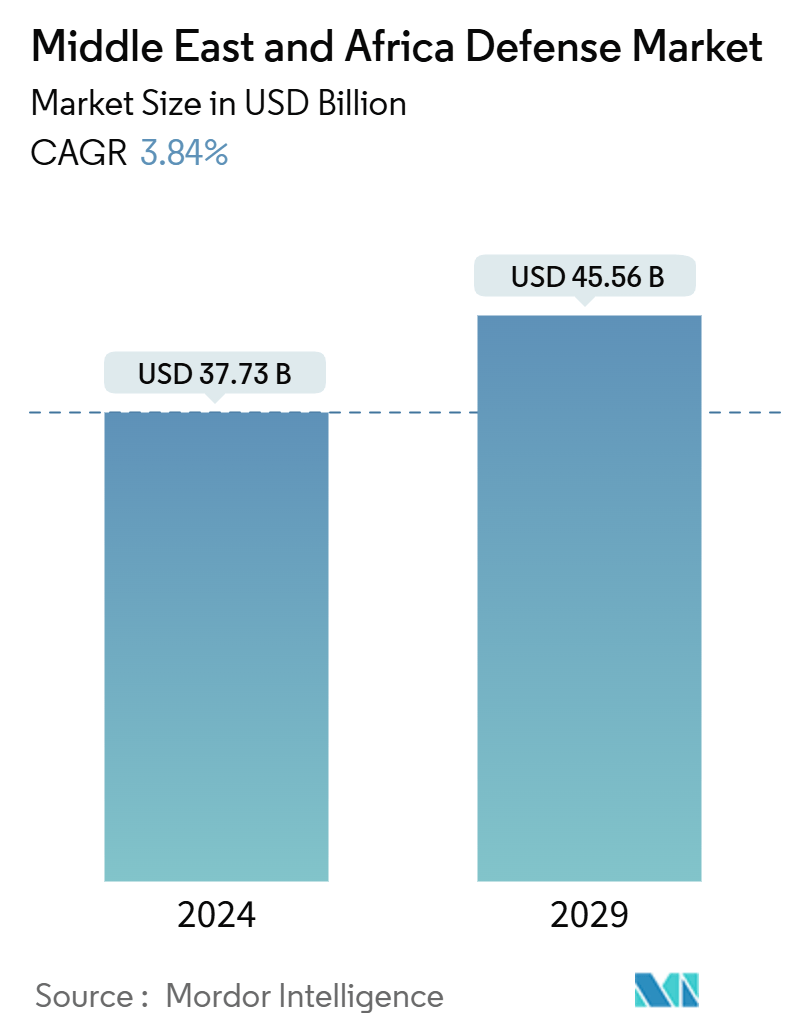

| Market Size (2024) | USD 37.73 Billion |

| Market Size (2029) | USD 45.56 Billion |

| CAGR (2024 - 2029) | 3.84 % |

| Fastest Growing Market | Middle East |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East And Africa Defense Market Analysis

The Middle East And Africa Defense Market size is estimated at USD 37.73 billion in 2024, and is expected to reach USD 45.56 billion by 2029, at a CAGR of 3.84% during the forecast period (2024-2029).

The Middle East and Africa defense market is on the upswing, driven by rising geopolitical tensions, regional conflicts, and heightened military investments. Leading the charge are countries like Saudi Arabia, the United Arab Emirates, Israel, and Egypt, which are channeling billions into modernizing their military assets.

The MEA defense market is pursuing cutting-edge technologies, emphasizing artificial intelligence, cyber warfare, and electronic warfare systems. Furthermore, there's a noticeable trend of collaboration with global defense giants, focusing on technology transfers and local production.

Geopolitical instability and regional conflicts are primary catalysts for the MEA defense market's growth. Nations in the Middle East and Africa, often caught in border disputes and counter-terrorism operations, are ramping up investments to modernize and expand their defense capabilities. Ongoing tensions, such as those between Iran and certain GCC nations, alongside conflicts in Yemen, Libya, and Syria, have driven countries like Saudi Arabia, the UAE, and Israel to bolster their defense budgets. These nations procure advanced military assets, from missile defense systems to UAVs, to enhance their strategic deterrence and operational readiness. This push for advanced defense technology not only aims to bolster national security but also seeks to promote regional stability.

However, the MEA defense market grapples with a significant challenge: balancing the drive for advanced defense capabilities with fiscal constraints, especially amid economic uncertainties. Oil-dependent economies in the region find their defense budgets swayed by fluctuating oil prices, often influenced by geopolitical tensions and global economic shifts. Recent international economic slowdowns and changing energy policies have led to oil market volatility, straining defense budgets. As they modernize their defense, nations like Saudi Arabia and the UAE are also navigating the challenge of maintaining robust defense spending while pursuing economic diversification and infrastructure investments under their Vision 2030 initiatives.

The region's dependence on foreign defense suppliers and the intricacies of international defense trade—like sanctions and export controls—complicates procurement. The ever-shifting geopolitical landscape, marked by changing alliances and rivalries, further complicates defense acquisitions and strategic planning. For instance, sanctions on Iran and the looming threat of new sanctions on other regional entities can disrupt supply chains and stall vital defense initiatives. Navigating these fiscal and geopolitical waters is crucial to ensuring that defense modernization doesn't come at the expense of broader economic stability and growth aspirations.

Middle East And Africa Defense Industry Segmentation

The Middle East and African defense market analyzes different defense equipment used to maintain the region's military strength. The study covers all aspects and is expected to provide insights into budget allocation and spending in the Middle East and African defense market during the forecast period.

The Middle East and Africa defense market is segmented into procurement, MRO, and geography. By procurement, the market is segmented into personnel training and protection, communication systems, weapons and ammunition, and vehicles. Vehicles include land, air, and sea-based vehicles. MRO segments the market into communication systems, weapons, ammunition, and vehicles. The report also covers the market sizes and forecasts for the major countries across the region. The market sizing and forecasts have been provided in value (USD).

| Procurement | |||||

| Personnel Training and Protection | |||||

| Communication Systems | |||||

| Weapons and Ammunition | |||||

|

| MRO | |

| Communication Systems | |

| Weapons and Ammunition | |

| Vehicles |

| Geography | |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Egypt | |

| Algeria | |

| South Africa | |

| Morocco | |

| Rest of Middle East and Africa |

Middle East And Africa Defense Market Size Summary

The Middle East and Africa defense market is experiencing significant growth, driven by increased defense spending due to geopolitical tensions and regional conflicts. Countries such as Saudi Arabia, the United Arab Emirates, Israel, and Egypt are leading this surge by investing heavily in the modernization of their military capabilities. The focus is on integrating advanced technologies, including artificial intelligence, cyber warfare, and electronic warfare systems, to enhance national security and regional stability. The market is also witnessing increased collaboration with global defense manufacturers for technology transfer and local production, further bolstering the defense industrial base in the region. However, the market faces challenges such as fiscal constraints due to fluctuating oil prices and the complexities of international defense trade, which require careful navigation to balance defense advancements with economic stability.

The vehicle segment is anticipated to be a rapidly growing area within the defense market, fueled by the need for modern armored vehicles to address regional security threats. Countries like Saudi Arabia and the United Arab Emirates are at the forefront of this segment, investing in advanced systems and strategic partnerships to enhance their defense capabilities. Additionally, the adoption of unmanned aerial vehicles (UAVs) is on the rise, with countries such as Saudi Arabia, the United Arab Emirates, and Israel expanding their UAV arsenals through both local production and international cooperation. The market is characterized by a fragmented landscape with both regional and international players, including prominent companies like Boeing, Lockheed Martin, and Saudi Arabian Military Industries, contributing to the diverse range of military products and solutions available. Government initiatives, such as Saudi Arabia's Vision 2030, are further driving the localization of defense manufacturing, reducing foreign dependence, and fostering technological advancements in the region.

Middle East And Africa Defense Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Buyers/Consumers

-

1.4.2 Bargaining Power of Suppliers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Procurement

-

2.1.1 Personnel Training and Protection

-

2.1.2 Communication Systems

-

2.1.3 Weapons and Ammunition

-

2.1.4 Vehicles

-

2.1.4.1 Land-based Vehicles

-

2.1.4.2 Sea-based Vehicles

-

2.1.4.3 Air-based Vehicles

-

-

-

2.2 MRO

-

2.2.1 Communication Systems

-

2.2.2 Weapons and Ammunition

-

2.2.3 Vehicles

-

-

2.3 Geography

-

2.3.1 Saudi Arabia

-

2.3.2 Turkey

-

2.3.3 Israel

-

2.3.4 Egypt

-

2.3.5 Algeria

-

2.3.6 South Africa

-

2.3.7 Morocco

-

2.3.8 Rest of Middle East and Africa

-

-

Middle East And Africa Defense Market Size FAQs

How big is the Middle East And Africa Defense Market?

The Middle East And Africa Defense Market size is expected to reach USD 37.73 billion in 2024 and grow at a CAGR of 3.84% to reach USD 45.56 billion by 2029.

What is the current Middle East And Africa Defense Market size?

In 2024, the Middle East And Africa Defense Market size is expected to reach USD 37.73 billion.