Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

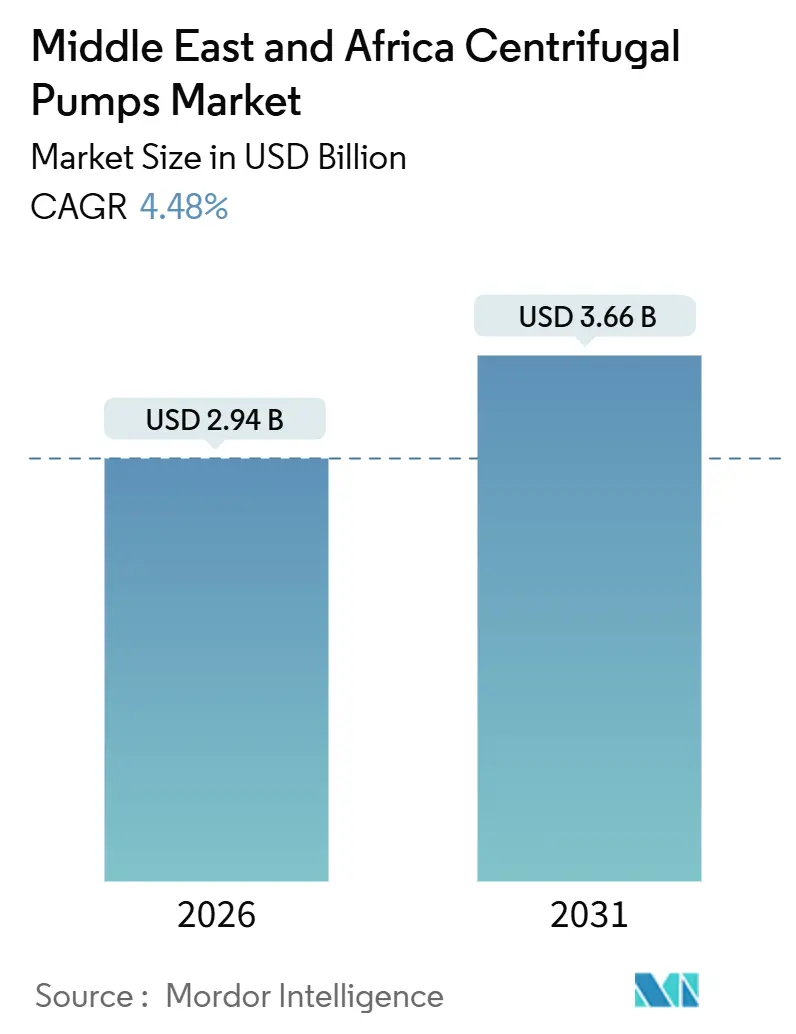

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 3.66 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Centrifugal Pumps Market Analysis by Mordor Intelligence

The centrifugal pumps market size in the Middle East and Africa is USD 2.94 billion in 2026 and is projected to reach USD 3.66 billion by 2031, translating into a 4.48% CAGR through the forecast period. Escalating desalination investments, wastewater-reuse targets, and mineral-processing expansions are jointly raising the baseline demand for engineered pumps across the region. Government localization mandates in Saudi Arabia and the United Arab Emirates are shortening delivery cycles and nudging buyers toward vendors with regional assembly capacity. Sustainability policies, including energy-efficiency requirements and life-cycle carbon audits, are encouraging operators to specify premium hydraulics and variable-speed drives. Meanwhile, nickel price swings and counterfeit spare parts continue to pressure margins and reliability, prompting end users to favor suppliers with robust quality-assurance programs. These cross-currents together underpin a resilient centrifugal pumps market that is set to expand even amid occasional volatility in the commodity cycle.

Key Report Takeaways

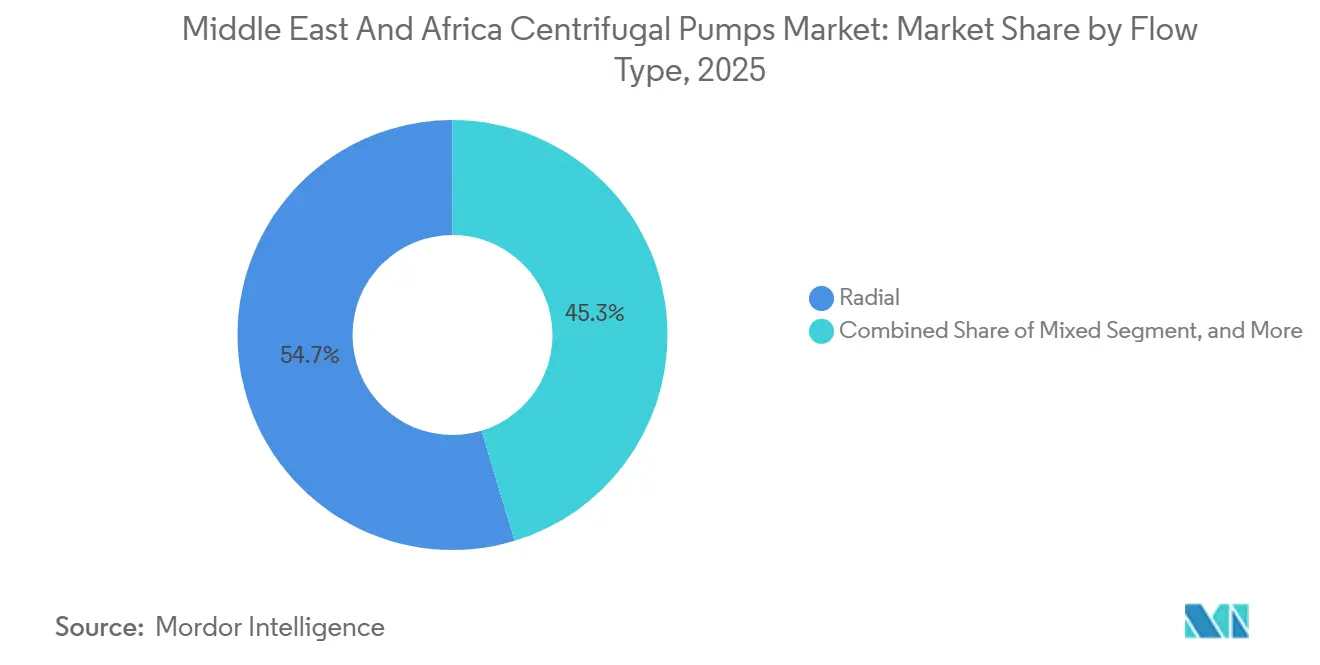

- By flow type, radial-flow designs held 54.67% of the Middle East And Africa centrifugal pumps market share in 2025, while mixed-flow units are advancing at a 5.07% CAGR through 2031.

- By number of stages, single-stage pumps commanded 62.31% of the Middle East And Africa centrifugal pumps market share in 2025; multi-stage configurations are forecast to grow at a 4.86% CAGR through 2031.

- By end-user industry, oil and gas accounted for 39.78% of the Middle East And Africa centrifugal pumps market share in 2025, but water and wastewater applications are expanding the centrifugal pumps market at a rapid 10.13% CAGR to 2031.

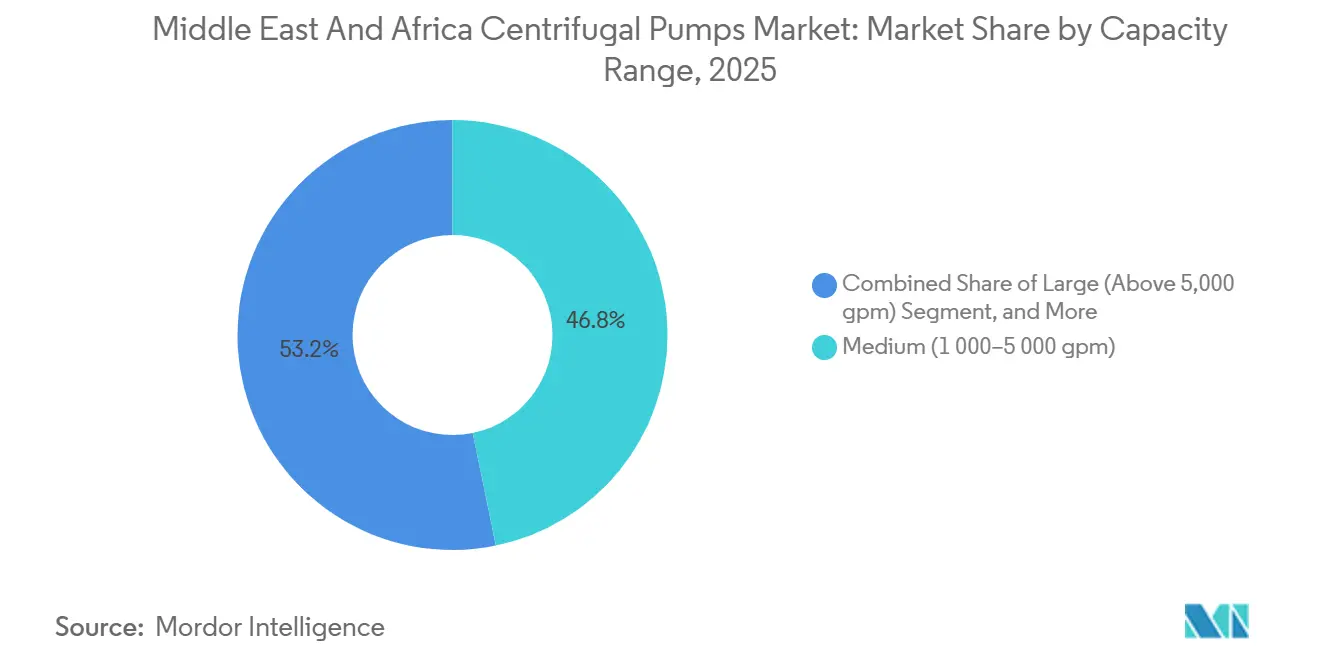

- By capacity range, medium-capacity units accounted for 46.77% of installations in 2025, whereas large-capacity models above 5,000 gpm are increasing at a 5.21% CAGR across the centrifugal pumps market.

- By material, stainless steel led with 47.89% of 2025 revenue, yet bronze is positioned to grow fastest at a 5.27% CAGR, reshaping the centrifugal pumps market toward alloy diversification.

- By geography, the Middle East contributed 28.16% of the 2025 value; Africa is advancing at a healthy 4.82% CAGR, expanding its role in the centrifugal pumps market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Centrifugal Pumps Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Industrialization and Urbanization Uptick | +0.9% | Middle East core, spillover to North Africa | Medium term (2-4 years) |

| Rising Investments in Urban Wastewater Treatment | +1.1% | Saudi Arabia, UAE, Kuwait, South Africa | Long term (≥ 4 years) |

| Expansion of Desalination Projects in Gulf Countries | +1.3% | Saudi Arabia, UAE, Oman, Qatar | Medium term (2-4 years) |

| Accelerated Mining Projects in Africa's Copper Belt | +0.7% | Democratic Republic of Congo, Zambia, South Africa | Long term (≥ 4 years) |

| Government-Led Oil and Gas Capacity Upgrades | +0.6% | Saudi Arabia, UAE, Iraq, Oman | Short term (≤ 2 years) |

| Local Manufacturing Incentives for Pump Components | +0.4% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialization and Urbanization Uptick

Urban residents already make up 89% of the Gulf Cooperation Council population, a density that forces municipalities to commission new potable-water, sewage-treatment, and fire-protection assets at an estimated 12,000–15,000 units annually.[1]United Nations Department of Economic and Social Affairs, “World Urbanization Prospects,” un.org Mega-projects such as NEOM in Saudi Arabia and Egypt’s New Administrative Capital embed high-efficiency centrifugal pumps rated above 3,000 gpm in desalination and transmission loops. District cooling, deep-basement dewatering, and NFPA-20-compliant fire systems add further layers of demand. Designers are increasingly specifying variable-speed drives and corrosion-resistant alloys to manage energy use and chloride-rich conditions. Collectively, these city-building programs anchor a long pipeline of recurring orders that reinforce the Middle East And Africa centrifugal pumps market across both base-load infrastructure and auxiliary services.

Rising Investments in Urban Wastewater Treatment

Saudi Arabia’s National Water Company is channeling USD 21 billion toward lifting wastewater throughput to 8.2 million m³/day by 2030.[2]National Water Company, “Strategic Wastewater Expansion Plan,” nwc.com.sa Kuwait’s USD 2.4 billion Sulaibiya upgrade and South Africa’s ZAR 3.2 billion Gauteng refurbishments underscore a region-wide shift toward higher treatment standards. Projects now favor membrane bioreactor or reverse-osmosis polishing, both of which demand low-pulsation, abrasion-resistant centrifugal pumps with stainless or duplex wetted parts. Variable-frequency drives are standard, cutting energy use 20%–30% while meeting ISO 50001 requirements. As utilities press to achieve 70% water reuse targets, the Middle East And Africa centrifugal pumps market gains exposure to long-term operations and maintenance contracts, enlarging lifetime revenue per installation.

Expansion of Desalination Projects in Gulf Countries

The United Arab Emirates brought on stream 909 million IGD of reverse-osmosis capacity in 2024, led by the 200 million GPD Taweelah facility that alone houses more than 150 high-pressure multi-stage pumps. Saudi Arabia’s USD 1.8 billion Yanbu-4 and Oman’s Salalah projects mirror each other in scale, each insisting on efficiencies beyond 82% and life-cycle carbon disclosures. Providers offering bronze or duplex alternatives with improved cavitation resistance have secured larger order books. Energy-recovery devices paired with precision hydraulics push buyers toward premium impeller profiles and tighter manufacturing tolerances, multiplying unit value. Desalination, therefore, stands as the single most powerful structural driver of the centrifugal pumps market through mid-decade.

Accelerated Mining Projects in Africa's Copper Belt

Ivanhoe Mines, Barrick Gold, and Anglo American together committed billions of dollars to expand concentrator throughput in the Democratic Republic of Congo, Zambia, and South Africa, unlocking demand for an additional 100-plus high-head slurry pumps between 2024 and 2028.[3]Ivanhoe Mines, “Kamoa-Kakula Phase 3 Expansion,” ivanhoemines.com Hard-iron and elastomer-lined casings are required to withstand silica loads above 15% by weight, which is pushing up average selling prices. Dewatering depths surpassing 400 m necessitate multi-stage vertical turbine models with bronze bowls to mitigate cavitation during restart cycles. With copper trading above USD 9,000/t, procurement budgets remain healthy, ensuring steady inflows to the Middle East And Africa centrifugal pumps market and buffering it against cyclical softness elsewhere.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cavitation and Priming Failures in Deep-Well Installations | -0.5% | Saudi Arabia, UAE, Oman (deep aquifer zones) | Short term (≤ 2 years) |

| Chemical Compatibility Limitations with Sour Crudes | -0.4% | Iraq, Oman, Saudi Arabia (sour-gas fields) | Medium term (2-4 years) |

| Price Volatility of Stainless-Steel and Alloy Inputs | -0.3% | Global, acute in import-dependent markets | Short term (≤ 2 years) |

| Persistent Counterfeit Spare-Parts Supply Chain | -0.2% | Africa, Middle East secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cavitation and Priming Failures in Deep-Well Installations

Static lifts above 300 m in Saudi fossil-aquifer zones produce low suction pressure, triggering vapor bubbles that erode impellers and trim efficiency by up to 25% within half a year. Similar issues in the UAE’s Al Ain wells required retrofits involving variable-frequency drives and vacuum-priming systems, at an additional USD 8,000-12,000 per site. Horizontal fire-water pumps also miss start-up targets when air pockets linger in suction lines, compromising NFPA compliance. Although self-priming designs and condition monitoring can halve failure rates, the added capital outlay slows adoption among budget-strained operators and dilutes the momentum of the Middle East And Africa centrifugal pumps market.

Chemical Compatibility Limitations with Sour Crudes

Hydrogen-sulfide levels topping 3,000 ppm in Iraq’s super-giant fields degrade carbon-steel casings within 18 months, while even 316L stainless shafts embrittle under sulfide stress. Saudi Aramco now insists on duplex or nickel-based alloys for all wetted parts in Jafurah, lifting unit prices by as much as 60%. Retrofitting Inconel 625 overlays in Oman’s Khazzan field doubled overhaul intervals but added USD 25,000 per pump. The resulting cost escalation narrows budgets for additional equipment, capping centrifugal pumps market expansion in sour-service domains until alloy prices moderate or alternative metallurgy emerges.

Segment Analysis

By Flow Type: Mixed-Flow Designs Bridge Volume and Head

Radial-flow pumps commanded 54.67% of the Middle East And Africa centrifugal pumps market in 2025, thanks to solid traction in municipal grids and HVAC cooling loops where heads rarely exceed 150 ft. Their straightforward hydraulics, broad supplier base, and compatibility with variable-speed drives reinforce procurement comfort. Mixed-flow configurations, however, are registering a 5.07% CAGR through 2031 as mining companies retrofit slurry circuits with hybrid impellers that tolerate 20%–30% solids without sacrificing efficiency. The Kamoa-Kakula expansion in the Democratic Republic of Congo typifies this pivot, specifying dozens of mixed-flow units for tailings discharge.

The design’s lower net-positive suction head requirement reduces excavation depth in new pump-station builds, a critical advantage in Africa’s shallow water tables. Flowserve’s 2024 release of a semi-open impeller further lengthens maintenance intervals to six months. Radial pumps retain dominance in high-pressure desalination, achieving efficiencies above 80% at 1,000 psi, while axial-flow units continue to serve flood-control projects in Egypt’s Nile Delta and Saudi date-palm irrigation where flows exceed 50,000 gpm. Collectively, these patterns sustain a balanced yet evolving Middle East And Africa centrifugal pumps market, in which mixed-flow technology is carving out a growing, high-margin niche.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Number of Stages: Multi-Stage Units Rise With Pressure Demands

Single-stage designs accounted for 62.31% of the centrifugal pump market in 2025 because their simplicity meets the majority of building-services and municipal-water applications. However, multi-stage models are advancing at a 4.86% CAGR, fueled by Saudi Arabia’s Jafurah field, where 18-stage barrel pumps deliver 8,000 psi water-alternating-gas injection. Desalination’s six- to eight-stage pumps feeding membranes at 1,200 psi represent another growth vein.

Sulzer’s HiFlux diffuser reduced inter-stage losses by 12%, offering payback in less than two years for continuous-duty installations. Yet the rotor-dynamic complexity of more than 10 stages pushes OEMs to provide finite-element validation and field balancing. Single-stage pumps still dominate NFPA-20 fire systems, but rising skyscraper heights may tilt preferences toward twin-stage split-case units that maintain head at 150% rated capacity. For now, the Middle East And Africa centrifugal pumps market balances mature single-stage volumes with premium multi-stage value growth.

By End-User Industry: Water Segment Surges Ahead

Oil and gas retained a 39.78% share in 2025, on the back of high-value upstream projects that bundle pumps, compressors, and separators. Nonetheless, the water and wastewater segment is growing at a striking 10.13% CAGR, buoyed by Gulf nations’ 70% reuse targets and more than 5 million m³/day of desalination capacity under construction. Municipal utilities award multi-year service contracts that lock in aftermarket revenue and lower lifetime ownership cost by 20%.

Mining is the next growth pocket, with copper belts demanding abrasion-resistant slurry pumps. Meanwhile, food and beverage facilities, such as Coca-Cola Beverages Africa’s new Namibian plant, adopt hygienic pumps that command 20%–30% premiums. Pharmaceutical and power generation add specialty applications requiring FDA-grade elastomers and high-temperature metallurgy. Although construction dewatering brings cyclical spikes aligned with mega-project timelines, it also introduces rental revenue models, expanding the Middle East And Africa centrifugal pumps market’s service dimension.

By Capacity Range: Mega-Projects Favor Large-Volume Units

Medium-capacity pumps between 1,000 and 5,000 gpm covered 46.77% of 2025 installations, thanks to standard motor sizing and manageable civil works. Larger models exceed 5,000 gpm and are growing at 5.21% CAGR, propelled by the 10,000 gpm seawater intakes at the UAE’s Taweelah plant and Zambia’s rainy-season mine dewatering. Skid-mounted packages in the 1,000-2,000 gpm range shorten commissioning from eight weeks to three weeks, appealing to fast-track peri-urban projects.

Small and micro pumps fill precision roles in labs and sanitation loops, benefiting from permanent-magnet motors that cut electricity use 30%-40%. For large-volume pumps, vibration isolation and computational modeling become critical to staying within ISO 10816 limits. Xylem’s acquisition of Evoqua bolstered its presence in this high-throughput tier, positioning the firm to capture larger slices of the Middle East And Africa centrifugal pumps market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Bronze Regains Popularity in Corrosive Duties

Stainless steel retained a 47.89% share in 2025 because it meets food, pharma, and desalination standards and offers reliable chloride stress-cracking resistance. Yet bronze is poised for the fastest ascent, with a 5.27% CAGR, supported by data showing that aluminum-bronze alloys extend overhaul intervals by 30% in retrofit desalination trains. Salalah’s 2024 project validated these gains by stretching service from 18 months to 30 months against a 25% higher purchase price.

Cast iron continues to supply budget-constrained municipal lines but remains vulnerable to dezincification in aggressive chemistries. Nickel volatility between USD 16,000 t and USD 20,000 t compressed margins 200–300 basis points for stainless suppliers, nudging buyers toward duplex or bronze where feasible. Titanium and Hastelloy address niche extremes, such as Red Sea brine discharge exceeding 60,000 ppm chlorides. As material science evolves, the Middle East And Africa centrifugal pumps market will likely diversify metallurgical portfolios to hedge against both corrosion and commodity swings.

Geography Analysis

The Middle East generated 28.16% of 2025 revenue, anchored by Saudi Arabia’s USD 1.2 trillion Public Investment Fund portfolio and the UAE’s industrial diversification roadmap. Localization initiatives such as Saudi T’AZEEZ and UAE NUSANED pushed OEMs to set up assembly hubs in Riyadh and Dubai, reducing lead times from 16 weeks to 8 weeks and bolstering regional centrifugal pumps market resilience.

Africa, advancing at 4.82% CAGR, is propelled by copper-belt expansions where Ivanhoe Mines plans to double output by 2028, requiring high-head slurry pumps across new concentrators. South Africa’s Rand Water earmarked ZAR 3.2 billion for pump-station refurbishments, modernizing its Gauteng backbone, and securing aftermarket revenue streams. Egypt’s Suez Canal Economic Zone attracted USD 2.1 billion in FDI in 2024, with multiple pump makers scouting for assembly sites that hedge tariff exposure.

Rest-of-region pockets, such as Iraq’s Rumaila sour-service operations and Kenya’s geothermal build-outs, drive niche demand for high-alloy, high-temperature variants. Local procurement rules, including South Africa’s 70% Mining Charter threshold, compel OEMs to source castings and machining locally, increasing the Middle East And Africa centrifugal pumps market’s domestic value-add over time. These nationwide initiatives steadily recalibrate supply chains toward a hybrid global-regional structure.

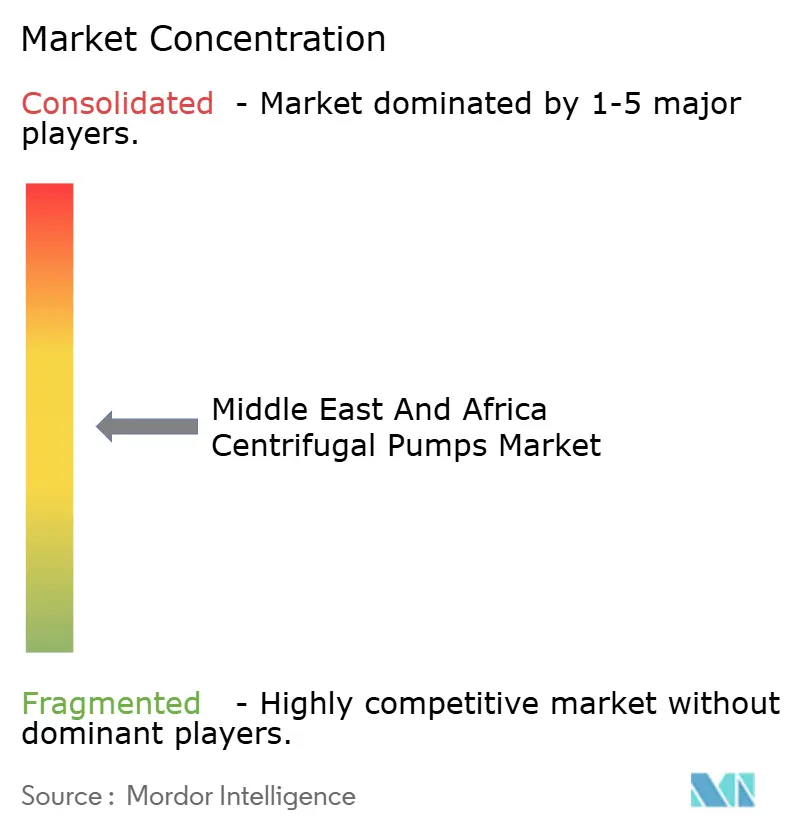

Competitive Landscape

The Middle East And Africa centrifugal pumps market shows moderate concentration. Global OEMs Flowserve, KSB, Sulzer, and Grundfos leverage decades-old vendor accreditations with Saudi Aramco, ADNOC, and utilities that impose stringent API 610 and ISO 9001 benchmarks. Flowserve’s delivery of 400 pumps to the Jafurah project illustrates the stickiness of such qualifications. Localization incentives like iktva push multinationals to deepen regional footprints, while mid-tier players equipped to invest in assembly plants gain tender advantages.

Chinese challengers Sanlian Pump and Leo Group undercut prices by 30%-40% and have captured up to 15% share in Africa’s municipal tenders, but shorter mean time between failures and sparse service networks temper broader uptake. Technology is emerging as a wedge: Grundfos’ IoT-enabled portfolio reduces downtime by 25%, commanding 10%–15% premiums while securing payback within 2 years. Quality gaps remain; audits reveal 20%-25% of installed units lack traceable mill certificates, complicating warranty and insurance coverage.

Strategic consolidation is reshaping the field. Xylem’s USD 7.5 billion acquisition of Evoqua broadened its wastewater treatment reach, while Pentair’s parallel move consolidated expertise in process water. Emerson’s USD 100 million SPARK plant in Saudi Arabia signals further localization among automation giants. In sum, competition hinges on a blend of localized manufacturing, digital differentiation, and life-cycle service capability.

Middle East And Africa Centrifugal Pumps Industry Leaders

Baker Hughes Company

Flowserve Corporation

Schlumberger Limited

The Weir Group plc

Xylem Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: KSB Middle East received UL safety certification for its Etanorm pump range, opening Gulf-wide fire-protection opportunities and enlarging its addressable market by an estimated 8%.

- April 2025: Rand Water allocated ZAR 3.2 billion (USD 170 million) in its 2025 capital budget for pump-station refurbishments and new installations across Gauteng Province to curb non-revenue water losses.

- March 2025: Grundfos posted double-digit revenue growth in the Middle East, driven by multi-stage submersible orders for Saudi rural water programs and digital-pump uptake in UAE smart-city projects.

- January 2025: KSB delivered 85 pumps for Egypt’s Alexandria wastewater-plant upgrade, integrating variable-frequency drives that cut energy use by 25% and meet ISO 50001 requirements.

Middle East And Africa Centrifugal Pumps Market Report Scope

The Middle East and Africa Centrifugal Pumps Market Report is Segmented by Flow Type (Axial, Radial, Mixed), Number of Stages (Single Stage, and Multi Stage), End-User Industry (Oil and Gas, Food and Beverages, Water and Wastewater, Pharmaceutical, Power, Construction, Metal and Mining, Other End-User Industries), Capacity Range (Micro (Below 500 gpm), Small (500-1,000 gpm), Medium (1,000-5,000 gpm), Large (Above 5,000 gpm)), Material (Cast Iron, Stainless Steel, Bronze, Other Materials), and Geography (Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Flow Type

| Axial |

| Radial |

| Mixed |

By Number of Stages

| Single Stage |

| Multi Stage |

By End-User Industry

| Oil and Gas |

| Food and Beverages |

| Water and Wastewater |

| Pharmaceutical |

| Power |

| Construction |

| Metal and Mining |

| Other End-User Industries |

By Capacity Range

| Micro (Below 500 gpm) |

| Small (500–1,000 gpm) |

| Medium (1,000–5,000 gpm) |

| Large (Above 5,000 gpm) |

By Material

| Cast Iron |

| Stainless Steel |

| Bronze |

| Other Materials |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Flow Type | Axial | |

| Radial | ||

| Mixed | ||

| By Number of Stages | Single Stage | |

| Multi Stage | ||

| By End-User Industry | Oil and Gas | |

| Food and Beverages | ||

| Water and Wastewater | ||

| Pharmaceutical | ||

| Power | ||

| Construction | ||

| Metal and Mining | ||

| Other End-User Industries | ||

| By Capacity Range | Micro (Below 500 gpm) | |

| Small (500–1,000 gpm) | ||

| Medium (1,000–5,000 gpm) | ||

| Large (Above 5,000 gpm) | ||

| By Material | Cast Iron | |

| Stainless Steel | ||

| Bronze | ||

| Other Materials | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the centrifugal pumps market in the Middle East and Africa by 2031?

The market is forecast to reach USD 3.66 billion by 2031, reflecting a 4.48% CAGR from 2026.

Which end-user segment is growing fastest through 2031?

Water and wastewater applications are expanding at an annual 10.13% clip as Gulf countries push 70% reuse targets.

Why are bronze alloys gaining traction in desalination plants?

Aluminum-bronze shows superior cavitation resistance and extends overhaul intervals by about 30%, lowering lifetime costs despite higher upfront prices.

How do localization mandates affect pump procurement in the Gulf?

Programs like Saudi T’AZEEZ and UAE NUSANED give bid advantages to vendors assembling pumps locally, cutting lead times and raising domestic value-add.

What technology trends are improving pump reliability?

IoT sensors, cloud-based analytics, and variable-speed drives collectively reduce unplanned downtime by roughly 25% and enhance energy efficiency.

Which capacity range is seeing the highest growth?

Large-capacity units above 5,000 gpm are increasing at 5.21% CAGR, driven by mega-desalination and deep-pit mining demands.