Market Size of Middle-East And Africa Armored Vehicles Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

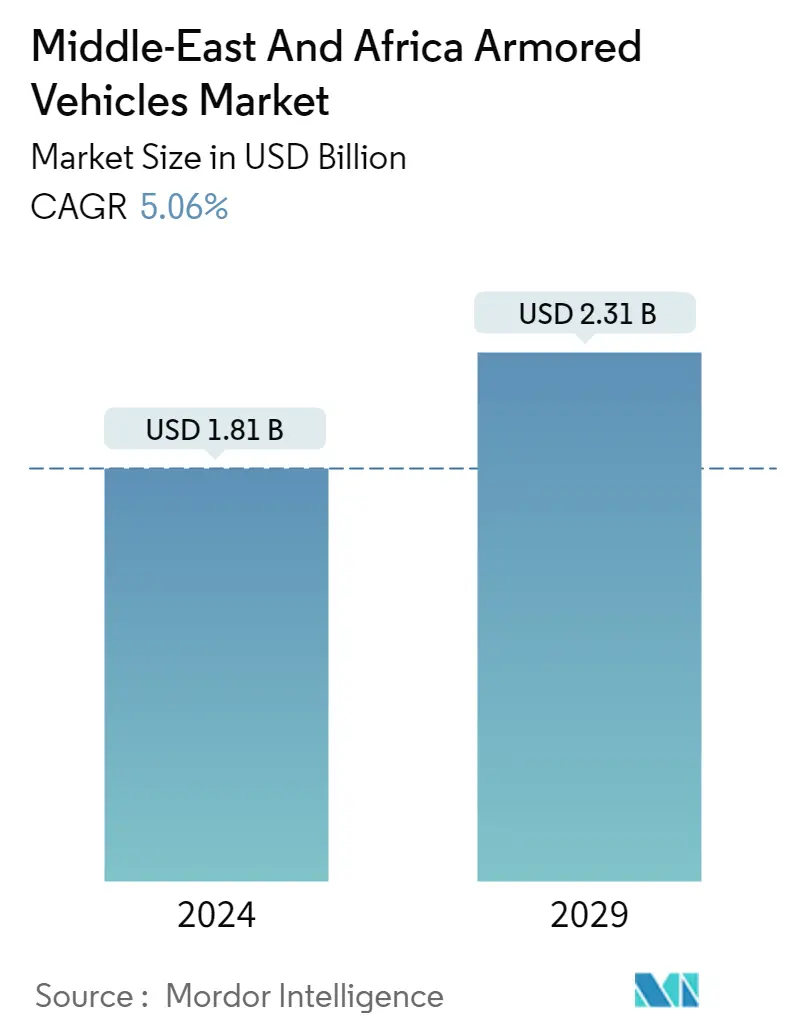

| Market Size (2024) | USD 1.81 Billion |

| Market Size (2029) | USD 2.31 Billion |

| CAGR (2024 - 2029) | 5.06 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East and Africa Armoured Vehicle Market Analysis

The Middle-East And Africa Armored Vehicles Market size is estimated at USD 1.81 billion in 2024, and is expected to reach USD 2.31 billion by 2029, growing at a CAGR of 5.06% during the forecast period (2024-2029).

An increase in the number of geopolitical and military conflicts in the Middle East and rising security concerns due to terrorist activities leads to growing spending on the defense sector from the Middle Eastern countries. Middle Eastern countries like Saudi Arabia, UAE, and Israel increased their defense expenditure and focus on improving defense capabilities due to rising security threats. Rising procurement of advanced weapons and armored vehicles and the development of next-generation fighting vehicles drive the growth of the market.

The total defense spending of the countries in the Middle East was USD 184 billion in 2022. According to the Stockholm International Peace Research Institute (SIPRI) report published in 2022, Saudi Arabia was the fifth largest defense spender in the world with a defense budget of USD 75 billion. Furthermore, the governments in the region are supporting the local manufacturing of armored vehicles. On the other hand, the occurrence of regular maintenance and electrical failures in armored vehicles and the absence of major armored vehicles OEMs in the region hinders the growth of the market.

Middle East and Africa Armoured Vehicle Industry Segmentation

An armored vehicle is a land vehicle protected by armor, generally combining operational mobility with offensive and defensive capabilities. Armored vehicles can be wheeled or tracked, depending on the type.

The Middle East and Africa armored vehicles market is segmented based on type and geography. By type, the market is segmented into main battle tank (MBT), armored personnel carrier (APC), infantry fighting vehicle (IFV), and other types. The other vehicles include mine-resistant ambush-protected (MRAP), armored cars, vehicles carrying armored self-propelled artillery, light armored vehicles, armored ambulances, armored recovery vehicles, assault amphibious vehicles, armored vehicle-launched bridge (AVLB), etc. The report also offers the market size and forecasts for five countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD).

| Type | |

| Main Battle Tank (MBT) | |

| Armored Personnel Carrier (APC) | |

| Infantry Fighting Vehicle (IFV) | |

| Other Types |

| Geography | |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| South Africa | |

| Rest of Middle East & Africa |

Middle-East And Africa Armored Vehicles Market Size Summary

The Middle East and Africa armored vehicle market is experiencing a robust expansion, driven by increased defense spending and a focus on enhancing military capabilities in response to geopolitical tensions and security threats. Countries such as Saudi Arabia, the UAE, and Israel are at the forefront of this growth, investing heavily in advanced weapons and next-generation fighting vehicles. The market is characterized by a semi-consolidated structure, with a few key players holding significant market shares. These include Mahindra Emirates Vehicle Armouring, NIMR Automotive, and Rheinmetall AG, among others. The region's governments are also promoting local manufacturing to bolster the defense sector, although challenges such as maintenance issues and the lack of major OEMs in the region pose hurdles to market growth.

The armored personnel carrier (APC) segment is poised for significant growth, fueled by military modernization programs and the procurement of advanced APCs. Countries in the region are upgrading their fleets with new vehicles that offer enhanced protection and situational awareness. Notable developments include Israel's introduction of the Eitan APC and the UAE's EDT Enigma AMFV. Saudi Arabia remains a dominant force in the market, with plans to further expand its armored vehicle fleet and invest substantially in military infrastructure. International manufacturers are also looking to increase their presence in the region, with companies like Oshkosh Defence focusing on strategic sales initiatives. These dynamics are expected to drive continued growth and innovation in the Middle East and Africa armored vehicle market over the forecast period.

Middle-East And Africa Armored Vehicles Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Type

-

2.1.1 Main Battle Tank (MBT)

-

2.1.2 Armored Personnel Carrier (APC)

-

2.1.3 Infantry Fighting Vehicle (IFV)

-

2.1.4 Other Types

-

-

2.2 Geography

-

2.2.1 Saudi Arabia

-

2.2.2 United Arab Emirates

-

2.2.3 Turkey

-

2.2.4 Israel

-

2.2.5 South Africa

-

2.2.6 Rest of Middle East & Africa

-

-

Middle-East And Africa Armored Vehicles Market Size FAQs

How big is the Middle-East And Africa Armored Vehicles Market?

The Middle-East And Africa Armored Vehicles Market size is expected to reach USD 1.81 billion in 2024 and grow at a CAGR of 5.06% to reach USD 2.31 billion by 2029.

What is the current Middle-East And Africa Armored Vehicles Market size?

In 2024, the Middle-East And Africa Armored Vehicles Market size is expected to reach USD 1.81 billion.