Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

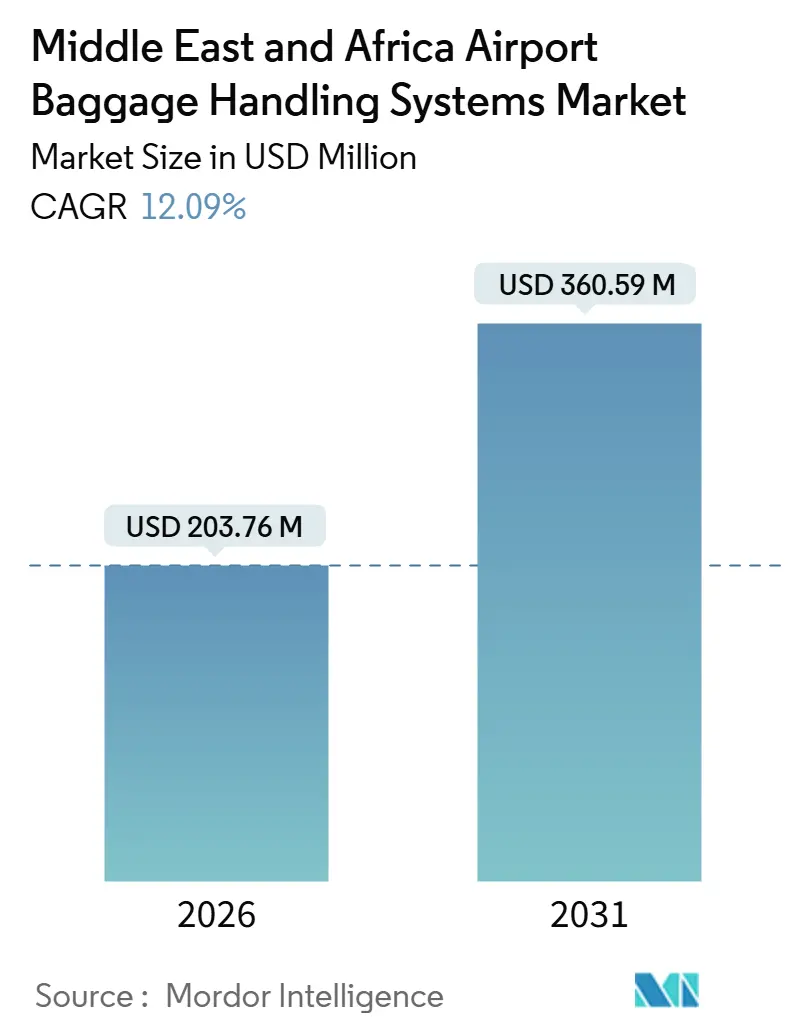

| Market Size (2026) | USD 203.76 Million |

| Market Size (2031) | USD 360.59 Million |

| Growth Rate (2026 - 2031) | 12.09% CAGR |

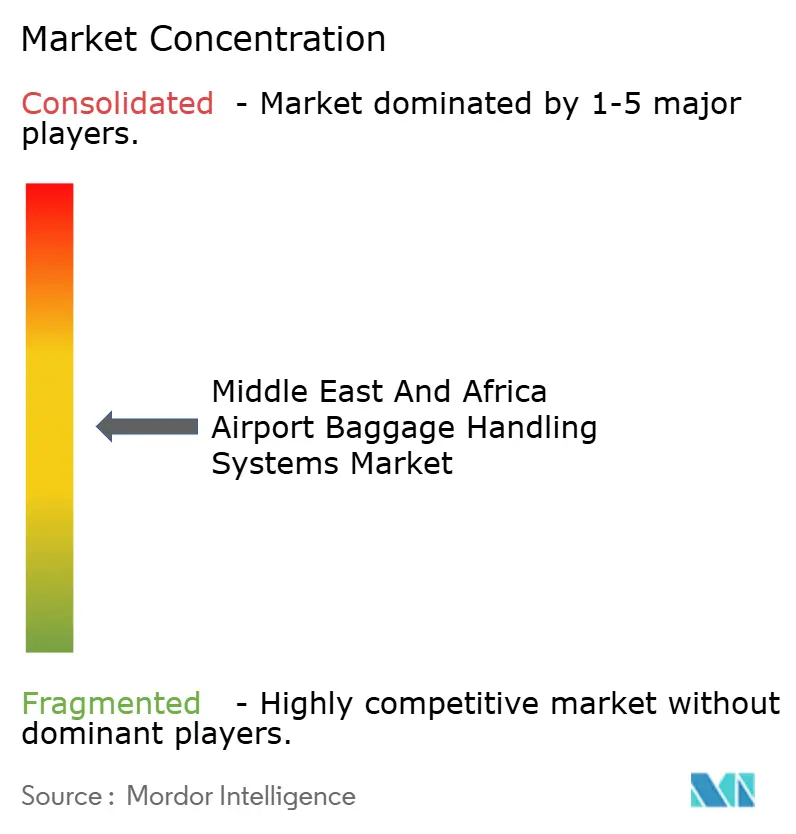

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Airport Baggage Handling Systems Market Analysis by Mordor Intelligence

The Middle East and Africa airport baggage handling systems market size is estimated at USD 203.76 million in 2026 and is projected to reach USD 360.59 million by 2031, growing at a CAGR of 12.09%. Sovereign-wealth-backed hub projects in the Gulf, accelerating ICAO Annex 17 compliance programs, and recovering capital outlays in Sub-Saharan Africa underpin this double-digit trajectory. Mega-hub expansions, such as Dubai’s USD 35 billion Al Maktoum International upgrade, Saudi Arabia’s USD 50 billion King Salman International blueprint, and Ethiopia’s USD 12.5 billion Bishoftu scheme, are driving orders for high-throughput sorters, early-bag storage, and AI-enabled tracking platforms.

Mandatory screening and cybersecurity statutes in the UAE and Saudi Arabia are prompting airports to adopt Standard 3 scanners and encrypted data centers, while IATA Resolution 753 retrofits are driving the adoption of RFID and computer-vision tools to reduce the regional mishandling rate of 6.02 per 1,000 bags. Operators are prioritizing lifecycle service contracts that integrate digital twin analytics and predictive maintenance with hardware, reducing downtime and the total cost of ownership. For instance, Dubai Airports’ 2024 AI materials-planning roll-out resulted in an 82% reduction in aging work orders and a 12% decrease in excess inventory.

Key Report Takeaways

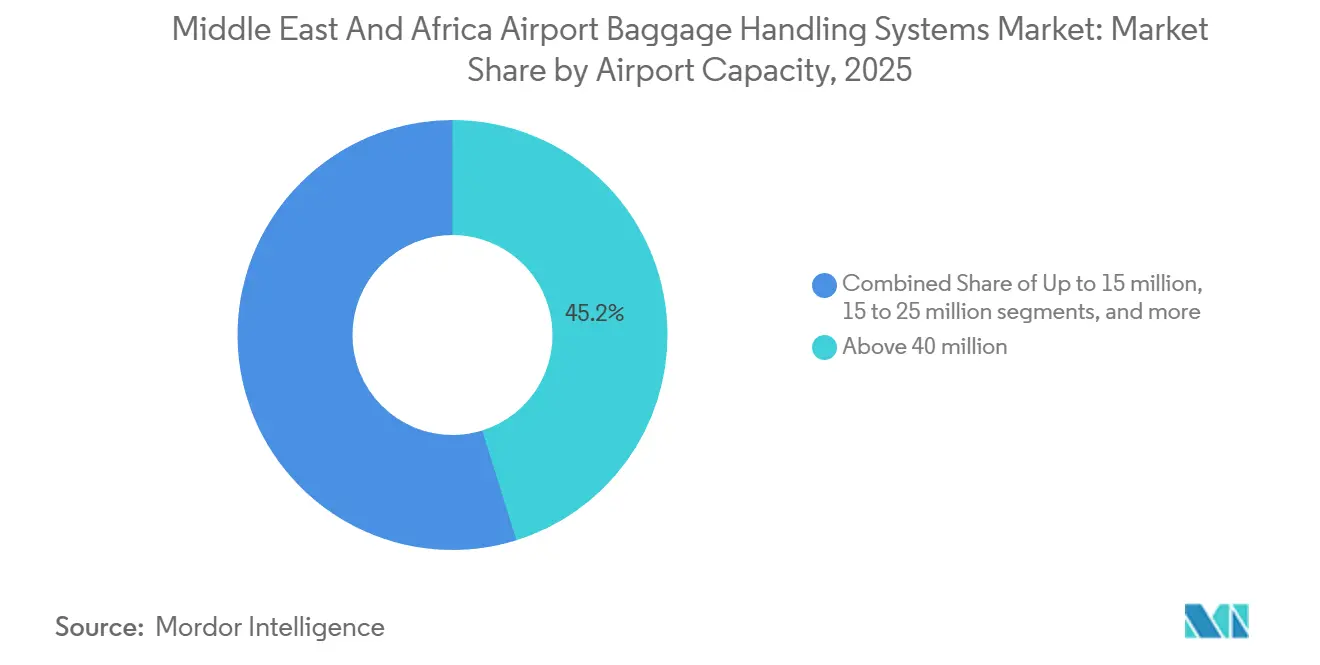

- By airport capacity, hubs designed for more than 40 million passengers captured 45.20% of the Middle East and Africa airport baggage handling systems market share in 2025 and are forecast to expand at a 12.57% CAGR to 2031.

- By solution, conveying and sorting systems led with 31.93% revenue in 2025, while tracking and tracing platforms are the fastest-growing, set to climb at 13.03% CAGR through 2031.

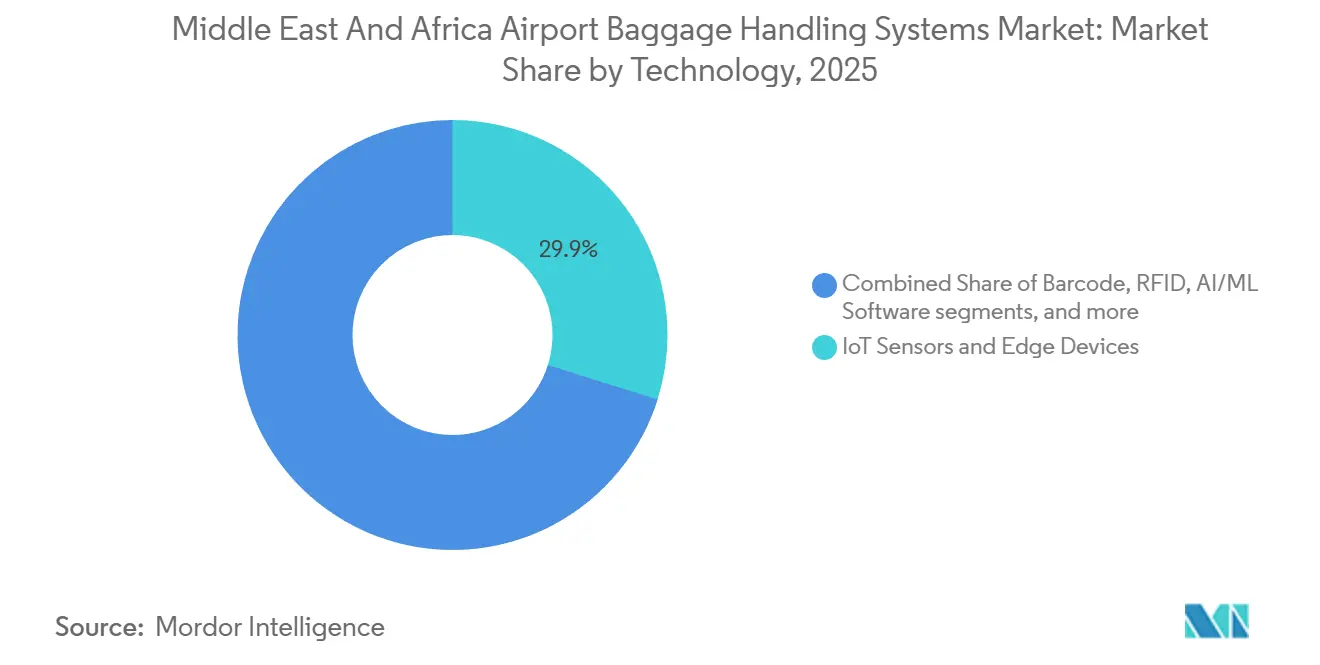

- By 2025, IoT sensors and edge devices held a 29.85% share; AI/ML software recorded the fastest growth, advancing at a 17.86% CAGR to 2031.

- By system type, conveyor belt networks dominated with a 44.15% share in 2025; however, hybrid and emerging architectures are advancing at a 14.47% CAGR over the forecast period.

- By geography, the Middle East contributed 80.84% of the 2025 revenue and is projected to log a 12.74% CAGR through 2031, driven by Saudi and Emirati mega-projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Airport Baggage Handling Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid airport capacity expansions across the GCC | +2.8% | Saudi Arabia, UAE, Qatar, Kuwait, Oman, Turkey | Medium term (2-4 years) |

| Government-backed tourism diversification programs | +2.1% | Saudi Arabia, UAE, Qatar, Egypt | Medium term (2-4 years) |

| Mandatory ICAO Annex 17 security compliance upgrades | +1.6% | GCC and North Africa | Short term (≤ 2 years) |

| Shift toward end-to-end self-service passenger journeys | +1.4% | UAE, Qatar, Saudi Arabia, South Africa, Egypt | Medium term (2-4 years) |

| AI-powered predictive maintenance to cut downtime | +1.9% | Dubai, Jeddah, Doha, South Africa, Egypt | Short term (≤ 2 years) |

| Green-airport mandates favoring low-energy conveyors | +1.2% | UAE, Qatar, Egypt, Morocco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Airport Capacity Expansions Across the Gulf Cooperation Council (GCC)

Dubai’s Al Maktoum expansion and Saudi Arabia’s King Salman International master plan, when fully built, aim to process more than 445 million passengers annually, obliging airports to install sorters that can move 15,000-20,000 bags per hour. Saudi Vision 2030 further mandates upgrades at Abha and Taif, multiplying demand for integrated conveying, screening, and early bag storage subsystems. Qatar’s Hamad International reached 40% self-check-in adoption in 2024, pairing capacity boosts with automation to shrink dwell times. Red Sea International Airport’s carbon-neutral design showcases cloud-based tracking from day one, underscoring how greenfield builds bypass legacy constraints. Kuwait and Turkey add further pipeline depth with ICAO-compliant DCV and tote networks specified in tender documents.

Government-Backed Tourism Diversification Programs

Saudi Arabia earmarked USD 800 billion for NEOM, Red Sea, and Qiddiya destinations, whose visitor targets hinge on seamless baggage transfer and high retail yields. Egypt’s IFC-supported PPP for 11 airports incorporates AI analytics to reduce mishandling at leisure gateways, such as Hurghada, which is expected to serve 50 million passengers in 2024. Abu Dhabi’s Smart Travel initiative reduced identity checks to seven seconds, reallocating counter space to retail and increasing non-aeronautical revenue by up to 20%. Qatar’s FIFA-driven LEED upgrades incorporated energy-efficient conveyors, which reduced electricity use by 30%. Morocco’s 2024 Alstef award mirrors the GCC model in North Africa, indicative of contagion effects along tourism corridors.

Mandatory ICAO Annex 17 Security Compliance Upgrades

Only 27% of African airports met the requirements of Resolution 753 in 2024, compared to 75% worldwide, resulting in a USD 400 million retrofit backlog for RFID, CT scanners, and analytics layers. The UAE’s 2023 cybersecurity strategy now obliges encrypted baggage data and local servers, adding 10-15% to project budgets but lowering ransomware exposure.[1]UAE GCAA Communications, “National Civil Aviation Cybersecurity Strategy,” UAE General Civil Aviation Authority, gcaa.gov.ae Saudi GACA’s economic code imposes service-level penalties for first-bag and last-bag delivery, encouraging operators to adopt real-time tracking. Dubai’s 2025 multi-terminal rollout of HI-SCAN 6040 CTiX systems demonstrates that Standard 3 screening is integrated with AI object recognition for enhanced throughput. Egypt’s PPP framework mirrors these moves, embedding innovative systems across 11 airports to meet ICAO timelines.

Shift Toward End-to-End Self-Service Passenger Journeys

Hamad International compressed the bag-drop time to three minutes and reduced queueing space by shifting 40% of passengers to kiosks. Dubai eliminated counters for hand-baggage-only travelers in 2024, freeing up 2,000 square meters for retail and lounges, and increasing per-passenger ancillary revenue by up to 20%. King Khalid International introduced passport e-gates, which clear 175,000 passengers daily, reducing immigration lines by 40%.[2]Ministry of Transport KSA, “Airport Expansions and E-Gates,” Saudi Ministry of Transport, mot.gov.sa Abu Dhabi’s biometric corridor aims to achieve document-free flows, thereby improving the accuracy of passenger-bag reconciliation. SITA and IDEMIA’s ALIX AI computer-vision pairing adds a tamper-detection layer by matching bag photos from check-in to reclaim.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-Saharan capex constraints post-COVID-19 | -1.8% | Kenya, Ethiopia, South Africa, Nigeria | Medium term (2-4 years) |

| High integration complexity with legacy information technology (IT) and operational technology (OT) | -1.3% | Kenya, South Africa, Egypt, multi-terminal Middle East hubs | Short term (≤ 2 years) |

| Volatile regional supply chain for electromechanical parts | -0.9% | Import-dependent Middle East and Africa | Medium term (2-4 years) |

| Heightened cybersecurity and data-sovereignty legislation | -0.7% | UAE, Saudi Arabia, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sub-Saharan Capex Constraints Post-COVID-19

Kenya's Jomo Kenyatta International lacks an inter-terminal conveyor spine, which inflates minimum connection times and depresses ASQ scores. At the same time, its USD 560 million greenfield terminal remains contingent on multilateral finance approvals. South Africa's investment plan prioritized runway upgrades over baggage basement improvements, delaying reclaim hall upgrades by up to two years.[3]ACSA Media, “Capital Investment Programme,” Airports Company South Africa, airports.co.za Ethiopia's Bishoftu airport relies on a USD 500 million AfDB tranche amid swings in airline profitability, exemplifying balance-sheet stress in state-led ventures. The World Bank Group's diagnostics reveal a historic pattern of airport revenues being diverted to non-aviation budgets, thereby perpetuating funding gaps for core systems. These limitations slow order placement for Standard 3 scanners, RFID retrofits, and AI maintenance suites despite clear operational need.

High Integration Complexity with Legacy Information Technology (IT) and Operational Technology (OT)

Melbourne Airport's 18-month Nukon integration demonstrates the extensive coordination and resources required to unify siloed operational data, a challenge for African operators constrained by political election cycle timelines. SITA's 2025 resilience white paper highlights the costs associated with migrating from teletype to API messaging, a hurdle for airports still running DOS-era mainframes. TRB's 2025 guide links multi-terminal layouts to exponential complexity in retrofit projects, driving up both risk and budget. JKIA's lack of a shared conveyor loop forces manual transfers and lowers hub competitiveness for Kenya Airways connections. Iraqi Airways' hybrid SITA Flex deployment in 2024 necessitated bespoke interfaces, highlighting the hidden costs associated with even cloud-first strategies.

Segment Analysis

By Airport Capacity: Mega-Hubs Streamline Capital and Talent

The above 40 million tier accounted for 45.20% of 2025 revenue within the Middle East and Africa airport baggage handling systems market size and is projected to post a 12.57% CAGR through 2031. Projects in Dubai, Riyadh, and Addis Ababa require sorters that can handle over 15,000 bags per hour, early-bag storage with more than 100,000 positions, and redundant DCV loops to ensure minimum connection times. These mega-hubs also attract the highest share of predictive-maintenance pilots, ensuring uptime commitments of 99.5% or higher.

Mid-tier hubs (25 to 40 million passengers), such as Doha and Cairo, are installing RFID tunnels and computer-vision portals to reduce mishandling during peak transit periods. Facilities in the 15 to 25 million passenger band, exemplified by Jeddah Terminal 1, utilize tote-based ICS to streamline interline transfers. In contrast, sub-15 million passenger gateways in Saudi Arabia and Kenya opt for modular conveyors that scale with incremental gate additions. The Middle East and Africa airport baggage handling systems market continues to favor scalable blueprints that enable airports to graduate from one capacity bracket to the next without rendering previous capital investments obsolete.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Solution: Tracking Platforms Accelerate Under Compliance Pressure

Conveying and sorting solutions retained a 31.93% share in 2025; however, tracking and tracing platforms are rising at a 13.03% CAGR, the fastest among solutions within the Middle East and Africa airport baggage handling systems market. ICAO Annex 17 and Resolution 753 compliance timelines require operators to retrofit their systems with RFID tunnels, computer vision scanners, and cloud dashboards for real-time reconciliation.

Security screening demand pivots around Standard 3 CT systems with AI threat detection, typified by Dubai’s fleet-wide HI-SCAN 6040 CTiX order. Self-service check-in and ticketing modules support end-to-end passenger journeys and free terminal footprints for retail. Early-bag storage is growing at transfer-heavy hubs, lowering recirculation and shaving conveyor wear. As a result, the Middle East and Africa airport baggage handling systems market size allocated to software subscriptions at present routinely embeds Bag Manager or equivalent APIs in EPC packages.

By Technology: AI/ML Software Unlocks Predictive Payoff

IoT sensors and edge devices presently command 29.85% of technology revenue. Still, AI/ML layers are expanding at 17.86% CAGR, the fastest in the Middle East and Africa airport baggage handling systems market.[4]Vanderlande White Paper Team, “Robotics and AI in End-to-End Baggage Operations,” Vanderlande, vanderlande.com Sensor-rich conveyor drives, DCV motors, and diverters feed health data into cloud twins that predict failure windows 48-72 hours ahead, letting engineers intervene during night banks.

RFID remains key to achieving 100% bag tracking, with 99.98% read accuracy compared to 94-95% for barcodes; however, its adoption in Africa lags due to pushback against capital expenditure. Optical character recognition plug-ins, such as Siemens’ Baggage Vision System, bring barcode lanes closer to RFID precision at lower cost, easing migration paths. Robotics and autonomous vehicles, including Aurrigo’s Auto-DollyTug and Vanderlande’s FLEET Batch, pilot autonomous carting from make-up to stand, offsetting labor shortages and improving airside ergonomics.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By System Type: Hybrid Designs Blend Legacy Belts With Autonomy

Conveyor belts still account for 44.15% of revenue, but hybrid architectures that integrate autonomous carriers and DCVs into legacy spines are expected to expand at a 14.47% CAGR through 2031. Tilt-tray and cross-belt sorters hold the speed benchmark, achieving 2,400 discharges per hour with dynamic tilting trays.

DCV routes and tote-based ICS provide precise bag tracking with a minimal footprint, making them ideal for space-constrained African refurbishments. Hybrid blueprints typically hold belts for trunk flow and deploy AGVs for last-mile delivery to aircraft stands, enhancing operational flexibility. Forbo low-friction belts and Daifuku’s Mobile Inspection Tables reduce energy draw and maintenance manhours, reinforcing the sustainability value proposition of mixed architectures in the Middle East and Africa airport baggage handling systems market.

Geography Analysis

The Middle East generated 80.84% of 2025 revenue in the Middle East and Africa airport baggage handling systems market and is set to rise at a 12.74% CAGR to 2031, fueled by giga-projects in Saudi Arabia and the UAE. Saudi Vision 2030 alone demands terminal expansions at 29 airports, each embedding screened conveyor loops, RFID portals, and cyber-secure data centers. Emirati regulations require encrypted, locally hosted baggage data, pushing vendors to partner with Gulf cloud providers. Qatar, Kuwait, and Turkey round out the demand map with upgrades that specify LEED-aligned conveyors and predictive-maintenance contracts.

Africa’s slice remains modest yet strategically significant. Ethiopia’s Bishoftu build, backed by a USD 500 million AfDB loan, targets 100 million passengers and 3.73 million tons of cargo annually, necessitating interline-ready baggage basements. South Africa’s ACSA has earmarked USD 1.15 billion through 2029, although some reclaim expansions slipped two years after the pandemic hit revenue. Egypt’s PPP with IFC for 11 airports includes AI baggage analytics at Hurghada, while Kenya’s JKIA seeks donor funding for a 31 million-passenger terminal to resolve current inter-terminal bottlenecks.

Sub-Saharan procurement cycles are lengthier, not only due to financing hurdles but also to supply-chain volatility for electromechanical spares. IATA Resolution 753 compliance remains stuck at 27% of African gateways, creating a USD 400 million retrofit backlog that the Middle East and Africa airport baggage handling systems market could unlock if multilateral funding channels stabilize.

Competitive Landscape

European integrators, such as Vanderlande Industries B.V., BEUMER Group GmbH & Co. KG, and Alstef Group SAS, secure mega-hub contracts by bundling design-build-operate models with digital twin analytics, predictive maintenance, and obsolescence management, providing airport sponsors with a single performance warranty. Vanderlande’s 2025 takeover of Siemens Logistics deepened its software bench, as seen in the VIBES roll-out at Jeddah, which combines TUBTRAX DCVs with Bagstore early-bag storage to achieve 99.5% availability.

SITA differentiates itself via software-as-a-service; its Flex, Bag Manager, and Maestro suites enable greenfield work at Red Sea International, Hurghada, and Baghdad by lowering capital expenditures and shortening deployment timelines. Smiths Detection, Leonardo, and Rapiscan focus on Standard 3 screening niches, often piggybacking on prime contractors for system-wide bids. Alstef and Pteris Global chase mid-tier African projects with modular lines that scale incrementally.

White-space prospects include Kenya’s pending 31 million-passenger terminal and Ethiopia’s Bishoftu project, where tender packages emphasize transferable maintenance knowledge and local assembly options. Robotics and autonomous vehicles appear as a disruptive force; Vanderlande’s FLEET Batch pilot at Oslo Terminal 2 and Aurrigo’s trials at Changi port suggest labor-light, energy-lean operations. The Middle East and Africa airport baggage handling systems market thus rewards vendors that stitch hardware, software, and data services into holistic cost-of-ownership narratives rather than lowest-price conveyor bids.

Middle East And Africa Airport Baggage Handling Systems Industry Leaders

BEUMER Group GmbH & Co. KG

Vanderlande Industries B.V.

Smiths Group plc

Rapiscan Systems, Inc.

Alstef Group SAS

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: DAEP selected Smiths Detection, a business unit of Smiths Group and a global leader in threat detection and screening technologies, to deploy an integrated suite of AI-driven checkpoint screening solutions across all terminals at Dubai International Airport.

- December 2024: SITA N.V. formed a strategic partnership with Saudi Arabia's Red Sea International Airport to implement technology solutions across the airport's operations. The partnership includes SITA Bag Manager for baggage reconciliation, which enables real-time tracking of bags loaded onto planes, ULDs, and carts throughout the airport.

- July 2023: Vanderlande Industries secured a contract to provide the baggage handling systems at Saudi Arabia's new Red Sea International Airport, along with a ten-year operations and maintenance service agreement. The company will implement its BAXORTER sorter technology for both inbound and outbound baggage handling systems.

Middle East And Africa Airport Baggage Handling Systems Market Report Scope

The Middle East and Africa airport baggage handling systems market encompasses automated equipment, software platforms, and integrated solutions for passenger baggage processing from check-in through reclaim, including conveying systems, sortation technologies, security screening integration, tracking solutions, and lifecycle services, while excluding manual handling equipment and cargo-specific systems, with market evolution toward AI-powered automation and biometric integration.

The Middle East and Africa airport baggage handling systems market is segmented based on airport capacity, solution, technology, system type, and geography. By airport capacity, the market is segmented into up to 15 million, 15 to 25 million, 25 to 40 million, and above 40 million. By solution, the market is segmented into check-in and ticketing systems, security screening systems, conveying and sorting systems, early baggage storage, baggage reclaim/unloading, and tracking and tracing. By technology, the market is segmented into barcode, RFID, IoT sensors and edge devices, robotics and autonomous vehicles, and AI/ML software. By system type, the market is segmented into conveyor belt systems, tilt-tray and cross-belt sorters, destination-coded vehicles, tote-based/individual carrier systems, and hybrid and other emerging systems. The report also offers market sizes and forecasts for eight countries across the region. For each segment, the market sizes and forecasts have been done based on value (USD).

By Airport Capacity

| Up to 15 million |

| 15 to 25 million |

| 25 to 40 million |

| Above 40 million |

By Solution

| Check-In and Ticketing Systems |

| Security Screening Systems |

| Conveying and Sorting Systems |

| Early Baggage Storage |

| Baggage Reclaim/Unloading |

| Tracking and Tracing |

By Technology

| Barcode |

| RFID |

| IoT Sensors and Edge Devices |

| Robotics and Autonomous Vehicles |

| AI/ML Software |

By System Type

| Conveyor Belt Systems |

| Tilt-Tray and Cross-Belt Sorters |

| Destination-Coded Vehicle (DCV) |

| Tote-based/Individual Carrier Systems |

| Hybrid and Other Emerging Systems |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Oman | |

| Qatar | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Airport Capacity | Up to 15 million | |

| 15 to 25 million | ||

| 25 to 40 million | ||

| Above 40 million | ||

| By Solution | Check-In and Ticketing Systems | |

| Security Screening Systems | ||

| Conveying and Sorting Systems | ||

| Early Baggage Storage | ||

| Baggage Reclaim/Unloading | ||

| Tracking and Tracing | ||

| By Technology | Barcode | |

| RFID | ||

| IoT Sensors and Edge Devices | ||

| Robotics and Autonomous Vehicles | ||

| AI/ML Software | ||

| By System Type | Conveyor Belt Systems | |

| Tilt-Tray and Cross-Belt Sorters | ||

| Destination-Coded Vehicle (DCV) | ||

| Tote-based/Individual Carrier Systems | ||

| Hybrid and Other Emerging Systems | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Kuwait | ||

| Oman | ||

| Qatar | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Middle East and Africa airport baggage handling systems market in 2031?

The Middle East and Africa airport baggage handling systems market is projected to reach USD 360.59 million by 2031.

Which airport capacity segment leads spending on baggage systems?

Hubs designed for more than 40 million passengers held 45.20% share in 2025 and are growing at 12.57% CAGR.

How are airports improving baggage-system uptime?

Operators deploy AI/ML predictive maintenance, trimming unplanned downtime by up to 25% and reducing spare-parts stockouts.

Why is RFID adoption accelerating in the region?

ICAO Annex 17 and IATA Resolution 753 deadlines push airports to install RFID tunnels that achieve 99.98% read rates and cut mishandling.

Which vendors dominate mega-hub projects?

European integrators Vanderlande Industries B.V., BEUMER Group GmbH & Co. KG, and Alstef Group SAS secure most large contracts by offering turnkey solutions bundled with digital-twin analytics.

How do sustainability goals influence system design?

LEED and eco-airport mandates steer procurement toward low-friction belts and energy-efficient conveyors that deliver up to 45% power savings.