Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

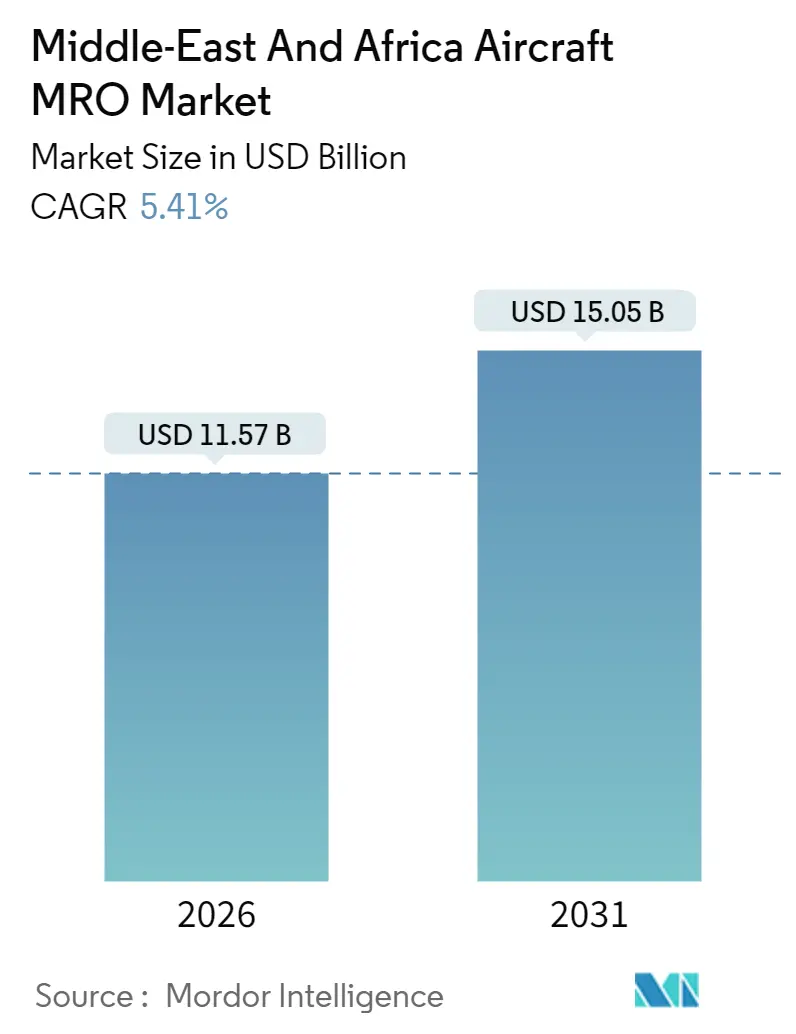

| Market Size (2026) | USD 11.57 Billion |

| Market Size (2031) | USD 15.05 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Aircraft MRO Market Analysis by Mordor Intelligence

The Middle East and Africa aircraft MRO market was valued at USD 10.98 billion in 2025 and estimated to grow from USD 11.57 billion in 2026 to reach USD 15.05 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031).

Rising investments in Gulf MRO hubs, collaborative frameworks among African flag carriers, and faster adoption of predictive maintenance are widening the addressable workload for engines, components, and line maintenance. The momentum is reinforced by the growth of narrowbody fleets under low-cost carrier strategies, defense-sector localization mandates that channel military work to domestic suppliers, and OEM power-by-the-hour contracts that bundle digital twins with real-time health monitoring. At the same time, shortages of licensed technicians and geopolitical bottlenecks in parts logistics lengthen turnaround cycles and inflate AOG costs, prompting operators to stockpile rotables and negotiate pre-positioned inventory clauses. Competitive dynamics are shifting as OEM-affiliated providers embed analytics into long-term service agreements while independent third-party shops counter with flexible capacity and multi-platform authorizations, creating a nuanced landscape across the aircraft MRO market.

Key Report Takeaways

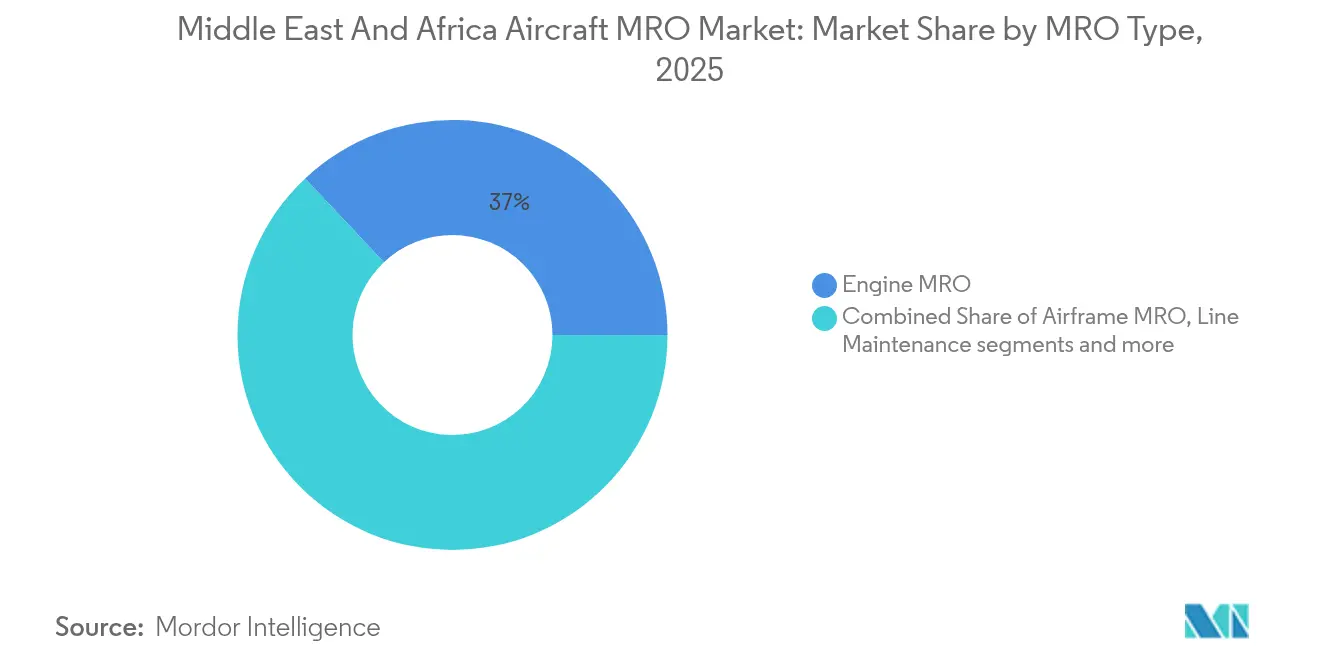

- By MRO type, engine work led with a 37.02% share in 2025, while line maintenance is forecast to post the fastest 6.05% CAGR through 2031, reflecting widespread on-wing service adoption.

- By aviation segment, commercial operations captured 64.72% of the revenue in 2025; military programs are set to log the quickest 6.92% CAGR, driven by localization targets in Saudi Arabia and the UAE.

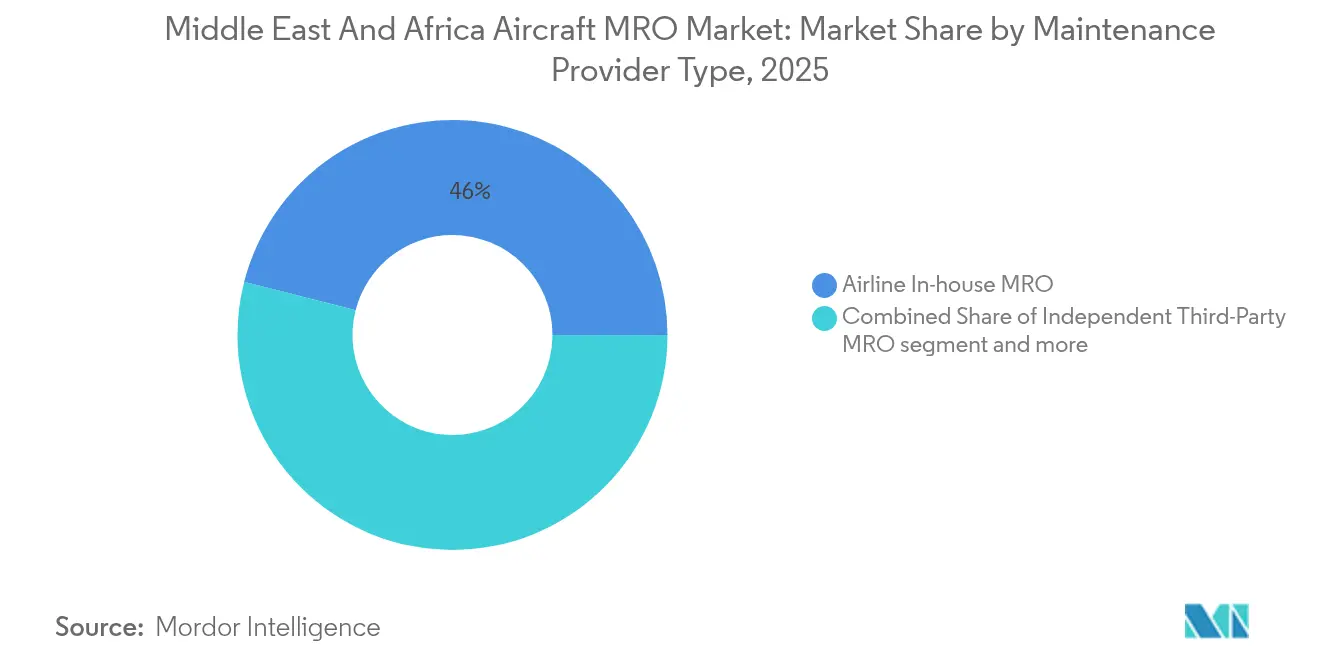

- By maintenance provider, airline in-house shops held a 46.02% share of the aircraft MRO market in 2025. Still, OEM-affiliated providers are advancing at a 6.7% CAGR by leveraging predictive analytics in power-by-the-hour agreements.

- By geography, the Middle East accounted for 68.01% of 2025 revenue, whereas Africa is on track to deliver the sharpest 6.95% CAGR to 2031, as five national carriers pool their engine and component resources.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And Africa Aircraft MRO Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet renewal programs by Gulf and African flag carriers | +1.2% | UAE, Saudi Arabia, Qatar, Ethiopia, Egypt | Medium term (2–4 years) |

| Expansion of low-cost carriers across the GCC and North Africa | +0.9% | UAE, Saudi Arabia, Egypt, Morocco | Short term (≤ 2 years) |

| Increasing adoption of OEM power-by-the-hour service agreements | +0.8% | Middle East, selected African hubs | Medium term (2–4 years) |

| Defense localization initiatives supporting domestic engine MRO capabilities | +0.7% | Saudi Arabia, UAE, Turkey, Egypt | Long term (≥ 4 years) |

| Growth of on-wing and mobile engine MRO service offerings | +0.6% | Dubai, Doha, Addis Ababa, Johannesburg | Short term (≤ 2 years) |

| Adoption of predictive maintenance analytics by regional MRO hubs | +0.5% | UAE, Qatar | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fleet Renewal Programs by Gulf and African Flag Carriers

Gulf and African airlines are re-equipping with A320neo, 737 MAX, 777X, and A350 aircraft, driving a surge in early-life engine shop visits for LEAP-1A, GEnx, and Trent XWB powerplants.[1]Ethiopian Airlines, “Fleet Information,” ethiopianairlines.com GE Aerospace invested USD 10 million in test-cell upgrades in Dubai and Doha to meet the next-generation workload.[2]GE Aerospace, “Middle East On Wing Support Expansion,” geaerospace.com Younger fleets deliver fuel savings but demand tighter adherence to OEM restoration intervals to safeguard operating-cost guarantees. Carriers that secure overhaul slots early gain dispatch reliability advantages, prompting competitors to book capacity years in advance. The resulting front-loaded demand accelerates engine-service revenue growth faster than global fleet expansion.

Expansion of Low-Cost Carriers Across the GCC and North Africa

Flydubai, Air Arabia, and Jazeera Airways operate high-utilization narrow-body fleets exceeding 11 flight hours daily, compressing A-check cycles and amplifying demand for line maintenance. Flydubai’s USD 190 million facility at Dubai World Central opened extra narrow-body bays that turn aircraft in 6 to 8 hours, keeping schedule disruptions low. Safran’s Casablanca LEAP shop mirrors this model for North-African LCCs, allowing operators to avoid ferry flights to Europe. Variable-cost maintenance plans, component pooling, and pay-by-the-hour contracts align with the LCC's cash-flow profile and redirect heavy-check revenue to regional hubs. The short booking horizons characteristic of LCCs benefit providers able to guarantee overnight returns, raising line-service volume across the GCC and North Africa.

Increasing Adoption of OEM Power-by-the-Hour Service Agreements

Emirates extended Rolls-Royce TotalCare to Trent 900 engines, Qatar Airways activated Honeywell GoldCare for its GEnx fleets, and Ethiopian Airlines operates CFM56 powerplants on a flight-hour basis. These agreements incorporate real-time engine-health feeds that predict unscheduled removals 30 to 60 days ahead, reducing revenue disruptions for airlines and allowing OEMs to stage parts at satellite stores. Independent MROs lacking data pipelines risk losing high-value engine work unless they become licensed channel partners. Operators value the budget certainty that PBH structures provide, evidenced by multi-year coverage clauses exceeding 15 years on widebody fleets. OEMs convert digital insights into lifecycle parts sales, increasing overall aftermarket penetration.

Defense Localization Initiatives Supporting Domestic Engine MRO Capabilities

Saudi Arabia’s GAMI targets 50% in-country sustainment by 2030, while the UAE’s AMMROC operates a 1.2 million sq ft complex in Al Ain, capable of civil-spec non-destructive testing and thrust measurement. Turkey’s Eskişehir base overhauls F-110 engines alongside civil-rated CFM56 units, facilitating skill transfers. Military capital budgets fund tooling, clean rooms, and certified test cells that are underutilized during peacetime, freeing capacity for civil customers. Widebody carriers secure overflow slots in these facilities, benefiting from defense-grade quality control.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled maintenance technicians and retention challenges | -0.9% | Africa, emerging Middle East hubs | Short term (≤ 2 years) |

| Geopolitical instability affecting engine parts and material supply chains | -0.7% | Red Sea corridor, customs-intensive African markets | Short term (≤ 2 years) |

| Limited harmonisation of Part-145 maintenance standards across Africa | -0.6% | Multiple African CAAs, non-EASA territories | Medium term (2–4 years) |

| Extended customs clearance timelines for engine components in non-GCC markets | -0.5% | West and Central Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Maintenance Technicians and Retention Challenges

Boeing projects that Africa will require 22,000 new licensed technicians by 2042, yet current regional training pipelines graduate fewer than 500 engineers annually.[3]Aviation Week Network, “Technician Shortage Looms Over Global MRO,” aviationweek.com Gulf shops compete directly with their host airlines for EASA Part-66 and FAA-licensed talent, driving up base salaries by double digits and compressing MRO operating margins. Visa requirements and housing costs further constrain expatriate hiring, while poaching between carriers raises staff turnover rates above 15% in UAE free zones, and delays in workforce scale-up risk underutilizing new hangars, such as Joramco’s five-line expansion in Amman. The talent gap lowers adequate capacity, subtracting 0.9 percentage points from forecast CAGR across the aircraft MRO market.

Geopolitical Instability Disrupting Engine-Parts and Material Supply Chains

Red Sea shipping attacks in late 2024 extended voyage times around the Cape of Good Hope by 10 to 14 days, inflating freight costs for engine rotables and standard parts kits. African operators face additional customs clearance of up to three weeks owing to manual inspection regimes and non-harmonized tariffs. Airlines are stockpiling high-value components, including landing gear, avionics, and APUs, to hedge against delays, thereby tying up working capital that would otherwise be used to finance fleet expansion. Smaller MROs without bonded warehouses incur higher demurrage fees and lose AOG business to larger providers with pre-cleared parts inventories.

Segment Analysis

By MRO Type: Line Maintenance Gains Momentum

Engine work represented the single-largest pool, capturing 37.02% of the aircraft MRO market share in 2025. Yet line maintenance, buoyed by on-wing borescope inspections and mobile repairs, is projected to outpace every other segment at a 6.05% CAGR to 2031. The aircraft MRO market size attributable to line services reached USD 2.94 billion in 2025 and is forecast to reach USD 4.19 billion by 2031, aided by GCC LCC fleets that prioritize rapid turnarounds. Providers invest in portable test cells, engine wash rigs, and mobile borescope suites to shrink downtime windows, with GE Aerospace and Lufthansa Technik leading deployment across Dubai and Doha hubs. High-cycle narrowbody fleets amplify demand for A-checks and corrective tasks, incentivizing MROs to base technicians across airport ramps rather than in hangar bays.

Line maintenance growth cascades through component provisioning; mobile engine teams often flag accessory gearbox leaks, bleed-valve failures, and minor hot-section distress that need immediate spares. Safran Landing Systems’ forthcoming East Africa office aims to provide predictive parts supply for landing gear interventions. Continuous line activity compresses shop-visit intervals, prompting providers to balance throughput against resource strain. Engine MRO remains capital-intensive; CFM56 and LEAP complete overhauls range from USD 2 to 4 million per shop visit. Therefore, operators will continue to assign deep maintenance to facilities with certified test cells and OEM licenses. These structural differences ensure both segments coexist, each anchoring distinct value pools within the aircraft MRO market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Aviation: Commercial Demand Dominates, Military Works Accelerate

Commercial aviation drove 64.72% of the 2025 value, underpinned by expanding A320neo and 737 MAX fleets, and is on track to maintain a 6.63% CAGR to 2031. Narrowbody engines, such as the LEAP-1A and CFM56-7B, require performance restoration every 6,000-8,000 flight cycles, generating predictable shop workloads. Emirates Engineering’s USD 950 million facility handles wide-body checks on A380 and 777 aircraft, while Ethiopian MRO operates a 100,000-pound-thrust cell for GEnx-1B testing, positioning both as hubs for regional third-party work. General aviation and business-jet activity, although smaller in volume, carries premium per-aircraft yields, tempting providers to add Gulfstream and Bombardier approvals.

Military workstreams, which were historically sent overseas, are localizing at a rapid pace. Saudi Arabia’s GE90 module program and AMMROC’s all-type authorization for UH-60, C-130, and F-110 engines redirect spending from Europe to the Gulf. The aircraft MRO market size aligned with military fleets is expected to rise from USD 3.85 billion in 2025 to USD 5.74 billion by 2031. Dual-use platforms, such as the C-130 Hercules and Airbus C295, allow defense shops to cross-sell capacity during peacetime lulls. Meanwhile, helicopter MRO, particularly for the AW139 and S-92 rotorcraft, adds a recurrent workload of dynamic-component overhauls. UAV sustainment is embryonic but growing: Boeing subsidiary Insitu opened a UAS center in Abu Dhabi for ScanEagle and Integrator platforms, indicating future diversification within the aircraft MRO market.

By Maintenance Provider Type: OEM-Affiliated Shops Scale Fastest

In-house airline organizations controlled 46.02% of the aircraft MRO market share in 2025, leveraging captive fleets and proximity to their home base for competitive slot allocation. Emirates Engineering, Saudia Technic, and Ethiopian MRO collectively managed over 4 million labor hours in 2024, while also pursuing third-party revenue to offset overhead. Yet OEM-affiliated networks are scaling at a 6.7% CAGR, fueled by data-rich service plans and engine health analytics. Lufthansa Technik’s AVIATAR integrates real-time aircraft data with job-card scheduling to cut turnaround times by up to 15%, enticing carriers to shift heavy checks under bundled agreements. GE Aerospace operates two On-Wing Support stations that now encompass LEAP and soon GE9X quick-turn lines, cementing its footprint across the aircraft MRO market.

Independent third-party providers, Joramco, Turkish Technic, and Sanad, bridge capability gaps with flexible slot offerings and multi-OEM coverage. Joramco’s Hangar 7 adds five narrowbody lines, pushing its parallel capacity to 22 aircraft, while Turkish Technic signed multiyear redelivery checks for IndiGo’s A320neos, underscoring the appetite for cost-efficient overhauls. Channel-partner agreements enable independents to maintain relevance: Sanad became the first non-OEM LEAP MRO in the SAMENA region, thereby strengthening its share of the aircraft MRO market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Middle East generated 68.01% of 2025 revenue within the aircraft MRO market, driven by hub operations in Dubai, Doha, and Riyadh, which service more than 1,400 engines across 30 airlines. Emirates Engineering’s widebody docks handle A380 and 777 overhauls, while flydubai’s USD 190 million hangar focuses on rapid narrow-body throughput. Saudi localization programs are enhancing in-country value capture, exemplified by Saudia Technic’s partnership with Air France-KLM, which assigns at least 50% of GE90 module work to Jeddah shops. Qatar Airways’ forthcoming HGT1700 APU facility, the first in the MENA region, expands the region’s component skill set and adds capacity for Airbus A350 operators.

Africa, although smaller today, is expected to grow at the fastest rate, with a 6.95% CAGR, increasing from USD 3.49 billion in 2025 to nearly USD 5.22 billion by 2031. Ethiopian Airlines, EgyptAir, Kenya Airways, Royal Air Maroc, and SAA Technical formed an AFRAA consortium to pool procurement and develop joint engine test cells, aiming to slash foreign MRO outlay. Ethiopia’s Addis Ababa hub already processes CFM56, LEAP, and GEnx engines, while EgyptAir’s Helwan facility is expanding to support Russian-origin helicopters and C295 transports under defense agreements. Nigeria's plans to host Boeing-certified shops in Lagos and Abuja could convert USD 200 million of annual overseas spending into domestic value capture. However, success hinges on customs modernization and a stable power supply.

Competitive Landscape

Three operating archetypes shape competition in the aircraft MRO market. Gulf hubs, such as Emirates Engineering, Abu Dhabi Aviation, and Saudia Technic (SAEI), pursue scale economics by integrating widebody docks, engine test cells, and component shops under a single campus to service intercontinental traffic. African carriers, recognizing the limited individual fleet scale, collaborate through AFRAA to pool resources, including tooling, approvals, and purchasing power, to narrow the cost gap with Gulf competitors. Defense-driven facilities in Saudi Arabia, the UAE, and Turkey utilize localization mandates to amortize military investments across commercial work, particularly on dual-use C-130 and helicopter platforms.

Technology integration differentiates providers. Lufthansa Technik’s AVIATAR, GE Aerospace’s FlightPulse, and Rolls-Royce’s Engine Health Management provide actionable analytics that cut unplanned removals and optimize parts inventories. Blockchain parts tracking is piloted in business aviation, though commercial uptake remains tentative. Regulatory scope governs addressable markets; dual EASA/FAA approvals unlock cross-border opportunities, while single-authority shops remain tied to domestic fleets. Consequently, top providers balance the breadth of certification with capacity specialization to sustain their pricing power.

Middle East And Africa Aircraft MRO Industry Leaders

Emirates Engineering

Abu Dhabi Aviation

EDGE Group PJSC

Joramco

Saudia Technic (SAEI)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Emirates and GAMECO signed multi-year agreements to extend heavy maintenance support for Airbus A380 and Boeing 777 fleets, ensuring continued operational efficiency and compliance with technical standards.

- November 2025: Air Arabia and Lufthansa Technik signed a long-term agreement for comprehensive MRO services of CFM56-5B engines, supporting the operational efficiency of Air Arabia's 43 Airbus A320ceo aircraft.

- April 2025: AJW Group secured a long-term PBH support program with FlySafair, covering 30 B737NG aircraft. The agreement includes PBH coverage, pool access, and repair management, ensuring streamlined maintenance operations and sustained efficiency for the South African operator’s expanding fleet.

Middle East And Africa Aircraft MRO Market Report Scope

Aircraft MRO includes tasks performed to ensure the continuing airworthiness of an aircraft and its parts. MRO service providers perform overhaul, inspection, replacement, defect rectification, and the embodiment of modifications, in compliance with airworthiness directives and repair.

The market is segmented by MRO type, aviation, maintenance provider type, and geography. By MRO type, the market is segmented into airframe MRO, engine MRO, component and modifications MRO, and line maintenance. By aviation, the market is classified as commercial aviation, military aviation, general aviation, and Unmanned Aerial Vehicles (UAVs). The scope of the study for the UAVs is limited to military applications only. By maintenance provider type, the market is categorized into airline in-house MRO, independent third-party MRO, and OEM-affiliated MRO. The report also offers the market size and forecasts for the Middle East and African countries. The market sizing and forecasts have been provided in value (USD) for all the above segments.

By MRO Type

| Airframe MRO |

| Engine MRO |

| Component and Modifications MRO |

| Line Maintenance |

By Aviation

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Vehicles |

By Maintenance Provider Type

| Airline In-house MRO |

| Independent Third-Party MRO |

| OEM-Affiliated MRO |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Rest of Middle East | |

| Africa | Sourth Africa |

| Egypt | |

| Rest of Africa |

| By MRO Type | Airframe MRO | |

| Engine MRO | ||

| Component and Modifications MRO | ||

| Line Maintenance | ||

| By Aviation | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Combat | |

| Transport | ||

| Special Mission | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Commercial Helicopters | ||

| Unmanned Aerial Vehicles | ||

| By Maintenance Provider Type | Airline In-house MRO | |

| Independent Third-Party MRO | ||

| OEM-Affiliated MRO | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Sourth Africa | |

| Egypt | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Middle East and Africa aircraft MRO market in 2026?

The aircraft MRO market size stands at USD 11.57 billion in 2026 and is forecast to reach USD 15.05 billion by 2031.

Which MRO segment is growing the fastest in the region?

Line maintenance is projected to expand at a 6.05% CAGR through 2031, driven by on-wing repairs and mobile service teams.

Why are OEM-affiliated MRO providers gaining share?

They embed predictive analytics and power-by-the-hour contracts, enabling data-driven scheduling and risk transfer that appeal to airlines seeking cost visibility.

What challenges are constraining regional MRO growth?

Technician shortages and geopolitical supply chain disruptions increase turnaround times and raise working capital requirements for operators.

Which country is investing most heavily in defense-related MRO localization?

Saudi Arabia, through GAMI’s 50% localization mandate and major expansions at AMMROC and Saudia Technic, leads regional defense MRO investments.