Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

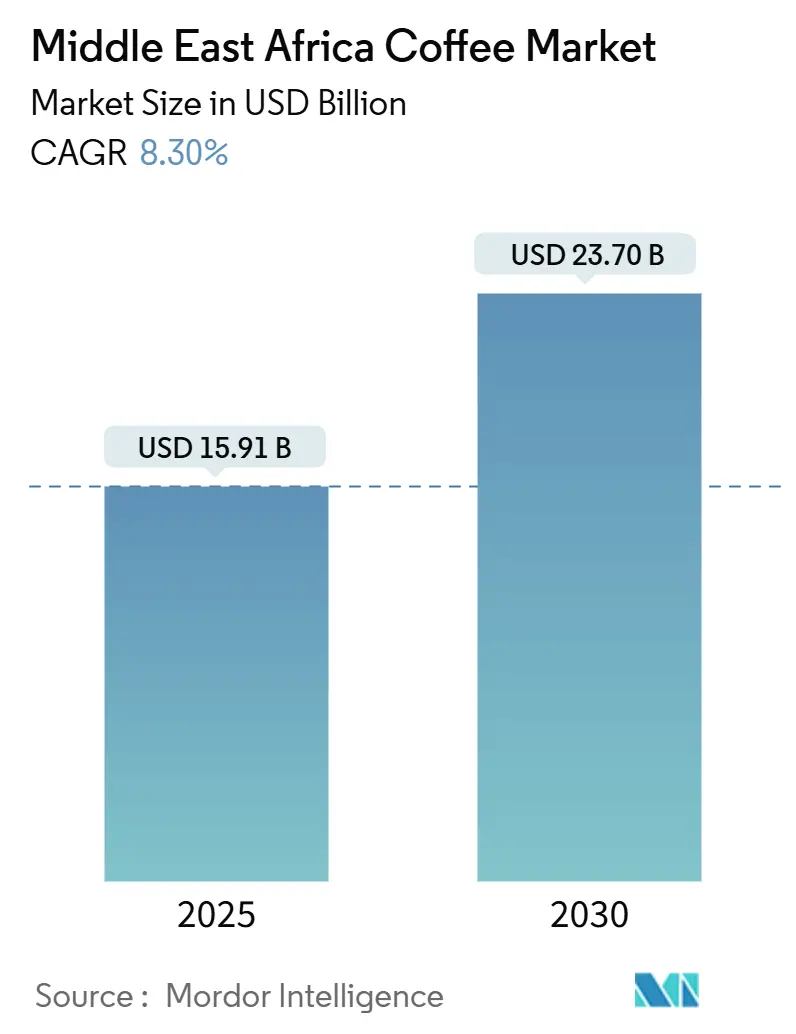

| Market Size (2025) | USD 15.91 Billion |

| Market Size (2030) | USD 23.70 Billion |

| Growth Rate (2025 - 2030) | 8.30% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East Africa Coffee Market Analysis by Mordor Intelligence

By 2030, the coffee market in the Middle East and Africa is expected to grow from USD 15.91 billion in 2025 to USD 23.70 billion, registering a CAGR of 8.30% during the forecast period. This growth is driven by factors such as increasing urbanization, higher disposable incomes, and the growing trend of visiting cafés as part of daily social activities. Global coffee roasters are focusing on localization by launching Arabic-language marketing campaigns and introducing Ramadan-specific flavors to cater to regional preferences. At the same time, local players are strengthening their supply chains by securing green coffee beans from key producers like Ethiopia and Kenya. Additionally, Gulf governments are investing in logistics hubs to reduce delivery times for fresh-roasted coffee, which supports the demand for premium products in high-income areas. The competitive landscape is becoming more intense as franchise agreements expand and specialty cafés attract mall visitors who previously frequented international fast-food chains.

Key Report Takeaways

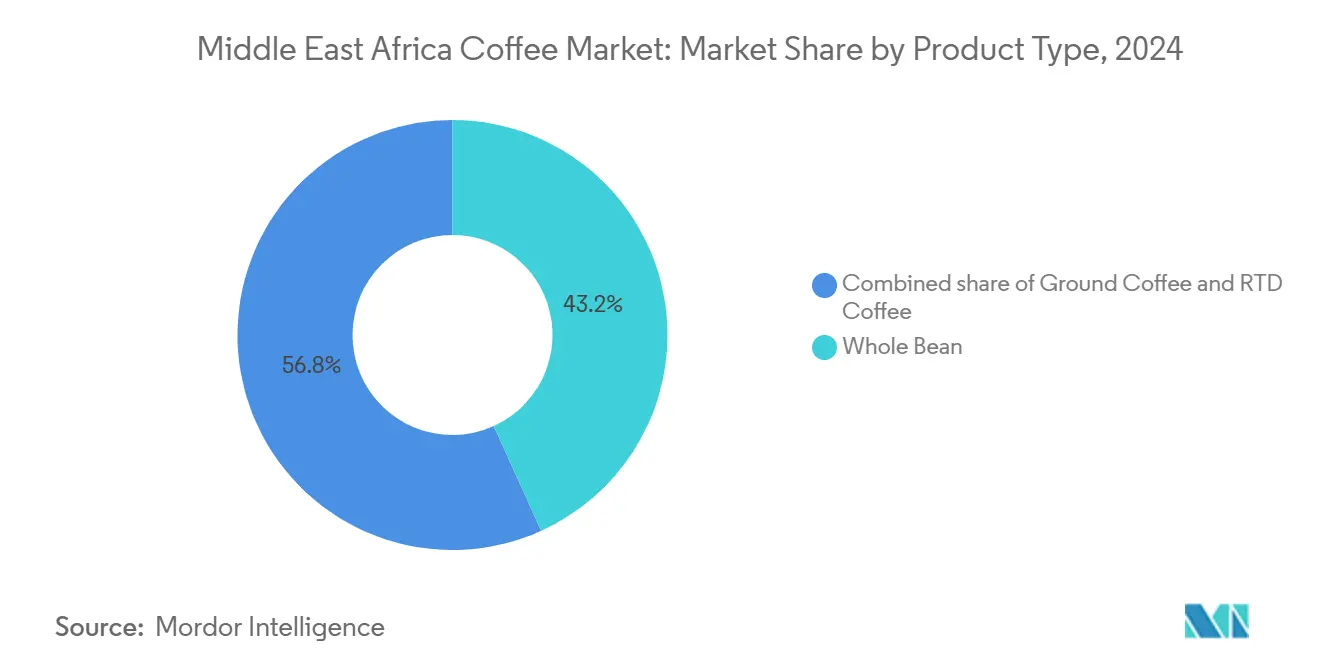

- By product type, Whole Bean coffee led with 43.22% of the Middle East Africa coffee market share in 2024, whereas Ready-to-Drink coffee is on track to post the fastest 8.34% CAGR through 2030.

- By category, Conventional formats commanded 79.31% revenue share in 2024; Specialty coffee is projected to grow at a 9.44% CAGR to 2030.

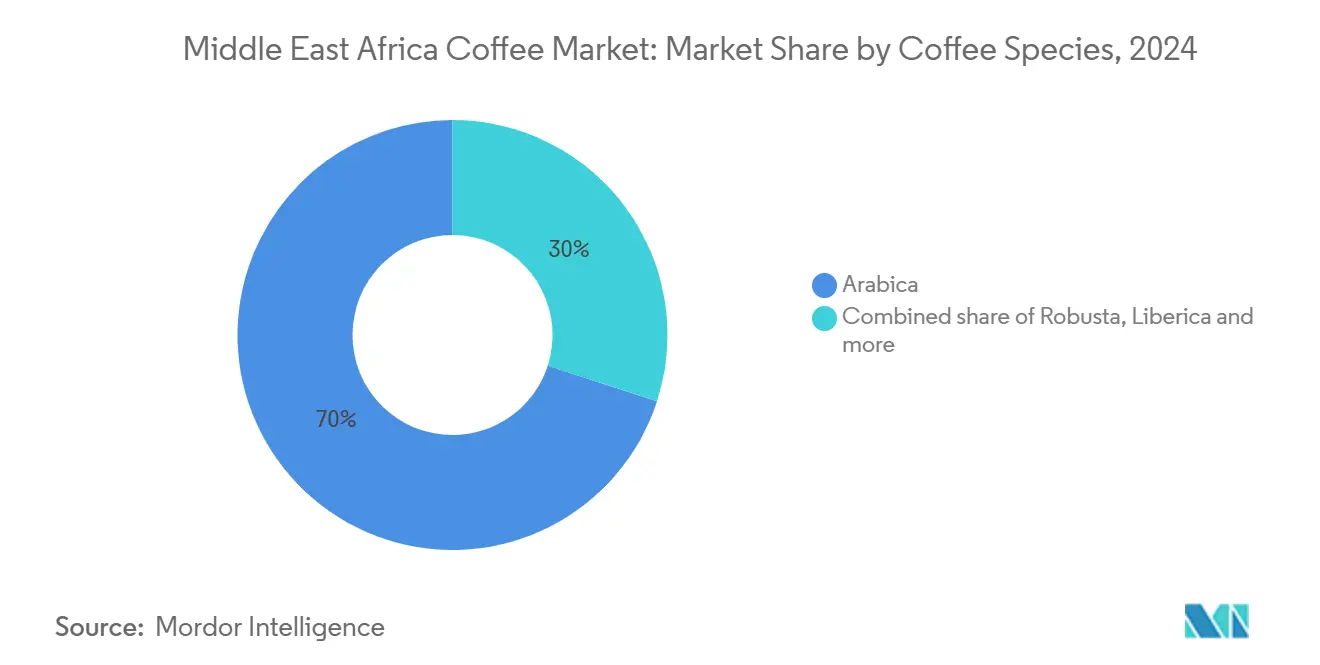

- By coffee species, Arabica dominated 70.01% of 2024 volume, while Liberica is forecast to register a 7.89% CAGR over the same period.

- By distribution channel, Off-Trade accounted for 69.42% of 2024 value, yet On-Trade is forecast to expand at a 9.23% CAGR to 2030 as store openings accelerate.

Middle East Africa Coffee Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep cultural and social role of coffee | +1.5% | Turkey, Saudi Arabia, UAE, Ethiopia | Long term (≥ 4 years) |

| Rapid urbanization and lifestyle shifts | +1.2% | Saudi Arabia, UAE, Egypt, Nigeria, South Africa | Medium term (2-4 years) |

| Expansion of café culture and specialty coffee shops | +1.1% | UAE, Saudi Arabia, Turkey, South Africa | Medium term (2-4 years) |

| Premiumisation and single-origin positioning | +0.9% | UAE, Saudi Arabia, Kuwait, Turkey | Short term (≤ 2 years) |

| Growth in coffee house stores fueling market demand | +0.8% | Middle East core, spill-over to North Africa | Medium term (2-4 years) |

| Innovation in coffee brewing methods | +0.6% | Global, early adoption in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rapid Urbanization and Lifestyle Shifts

In Saudi Arabia and the United Arab Emirates, urban populations have surpassed 85%, leading to the emergence of densely packed clusters of young, digitally-savvy consumers. For these consumers, coffee has evolved from a mere beverage to a symbol of social currency. This shift is evident in the surge of specialty cafés sprouting up in Riyadh's King Abdullah Financial District and Dubai's Design District. World Bank data reveals that 43% of Egypt's populace resides in urban locales, hinting at a burgeoning appetite for affordable instant and ready-to-drink coffee options tailored for the on-the-go commuter[1]World Bank, "Urban Population Data.", data.worldbank.org. Similarly, in Nigeria's Lagos and Abuja, trends mirror those of their Middle Eastern counterparts. Local roasters, such as Bunna Bet Ethiopia, are making inroads, catering to both expatriate communities and the aspirational middle class. As urbanization condenses meal times, grab-and-go coffee has begun to replace traditional tea breaks. This shift has paved the way for Nestlé's September 2024 debut of Nescafé Ready-to-Drink in Saudi Arabia, UAE, Egypt, and Iraq, all under the catchy "Bikeifi" campaign. With rising incomes, widespread smartphone use, and the omnipresence of delivery apps, it's clear that urbanization will continue to drive volume growth, even if per-capita consumption levels off in the more established Gulf markets.

Expansion of Café Culture and Specialty Coffee Shops

Third-wave coffee culture has grown beyond Western cities, with Dubai, Riyadh, and Istanbul now hosting international barista championships and single-origin coffee tasting events that attract regional buyers and roasters. In 2024, Black Sheep Coffee announced plans to open 250 stores across the Middle East and Africa. These stores will be located in busy malls and business districts, offering premium espresso drinks and co-working spaces. Costa Coffee has partnered with Saudi Arabia's Jazean Group to open 100 stores. This partnership uses Jazean's expertise in real estate and cultural knowledge to handle zoning laws and labor-nationalization requirements effectively. Ethiopia's specialty coffee industry is shifting from exporting commodities to building branded retail. Nordic Approach's project in Yirgacheffe connects small farmers directly with European roasters, bypassing the Ethiopian Commodity Exchange and ensuring farmers earn higher premiums that previously went to middlemen. The trend of cafés serving as workspaces, driven by remote work policies, is increasing customer visit durations and repeat visits. This change supports higher rents and attracts institutional investors, showing strong confidence in the sector's growth potential.

Premiumisation and Single-Origin Positioning

Affluent consumers in the Gulf Cooperation Council states are willing to pay 3 to 5 times the commodity price for traceable, single-origin lots that carry narratives of terroir and farmer welfare. This willingness is reshaping procurement strategies; roasters now bypass traditional exporters to contract directly with cooperatives in Ethiopia's Sidamo and Yirgacheffe regions. Lavazza's 2024 introduction of the Tibali brewing system, designed for premium whole-bean coffee, targets this segment by offering barista-quality extraction in home and small-office settings. Kenya's Agriculture and Food Authority reformed its auction system in 2024 to allow direct sales, enabling specialty buyers to secure AA and Peaberry grades without intermediary markups, a move that lifted farmgate prices by an estimated 15%[2]Agriculture and Food Authority Kenya, "Kenya Coffee Auction Reform." agricultureauthority.go.ke. Saudi Arabia's DMCC Coffee Centre, which expanded its storage and grading facilities in 2024, is positioning Dubai as a re-export hub for African specialty lots destined for Asian and European markets, capturing logistics and blending margins that previously accrued to European ports.

Growth in Coffee House Stores Fueling Market Demand

In February 2025, Starbucks revealed plans to open 500 new stores across the Middle East over the next five years. This marks the largest expansion by a single brand in the region, surpassing previous efforts and reflecting the company’s confidence in rising demand. Starbucks operates in the region through the Alshaya Group, which currently manages over 1,300 stores. Alshaya has effectively adapted to local preferences by introducing offerings like date-flavored lattes during Ramadan and providing gender-segregated seating in conservative markets. Regional competitors are also expanding their presence. In February 2024, the Saudi Coffee Company, owned by the Public Investment Fund, signed nine agreements to secure coffee supply, enhance roasting facilities, and open branded outlets to compete with international chains. The increasing number of coffee shops is influencing social habits. More stores are encouraging coffee consumption among groups like women and younger people, who now see cafés as acceptable places to socialize. Franchising is also lowering barriers for local entrepreneurs. Inspire Brands and Caffè Nero are seeking master franchisees in Egypt, Morocco, and Nigeria, aiming to gain an advantage by entering these markets early as infrastructure and consumer awareness improve.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitute beverages and functional drinks | -0.7% | Saudi Arabia, UAE, Egypt, Turkey | Medium term (2-4 years) |

| Supply-chain and logistics bottlenecks | -0.5% | Ethiopia, Uganda, Tanzania, Kenya | Short term (≤ 2 years) |

| Health concerns over caffeine and sugar | -0.4% | Saudi Arabia, UAE, Kuwait, Bahrain | Short term (≤ 2 years) |

| Detrimental impact of coffee pods and capsules on the environment | -0.3% | UAE, Saudi Arabia, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Caffeine and Sugar

Public health campaigns in the Middle East are driving changes in sugar-sweetened beverages. The World Health Organization's Eastern Mediterranean office reports that 4 out of 8 countries in the region, including Saudi Arabia, have introduced taxes on these beverages. Saudi Arabia's tax reduced consumption by 19%. To comply with regulations and attract health-conscious consumers, brands are reformulating products. For example, Nestlé's Nescafé Ready-to-Drink line, launched in September 2024, now includes reduced-sugar options. Caffeine content is also under scrutiny, especially for pregnant women and adolescents, leading retailers in the UAE and Kuwait to add advisory labels on high-caffeine products. Functional beverages like matcha lattes and turmeric teas are gaining popularity, replacing coffee on premium grocery shelves as consumers seek wellness benefits. Decaffeinated and half-caff options are also growing, with decaf now accounting for 5% to 8% of specialty coffee sales in Gulf markets, up from negligible levels three years ago. Stricter labeling rules and public health messaging are expected to push coffee brands to invest more in reformulation and consumer education to maintain market share.

Detrimental Impact of Coffee Pods and Capsules on the Environment

Single-serve coffee pods and capsules create significant plastic and aluminum waste, which municipal systems in the Middle East and Africa struggle to manage. Recycling rates in countries like the UAE and South Africa are often below 10%, prompting discussions on extended producer responsibility schemes. Brands like Nespresso and Lavazza have introduced take-back programs in some markets, but participation remains low due to logistical challenges and consumer indifference. The European Union's circular-economy standards are influencing the region, as multinational brands adopt compostable or recyclable capsule designs to streamline supply chains. Washington State's 2024 compostable products report has also impacted global standards, pushing brands to prepare for stricter regulations. Younger consumers in urban Gulf markets are increasingly vocal about sustainability, with social media campaigns criticizing capsule waste. This has led some cafés to replace pod-based machines with traditional espresso equipment. The shift has opened opportunities for reusable capsules and whole-bean formats, which specialty roasters promote as environmentally friendly and high-quality. The future depends on whether governments enforce deposit-return schemes or bans and if brands can expand recycling infrastructure to match capsule sales growth.

Segment Analysis

By Product Type: Whole Bean Anchors Tradition, RTD Captures Convenience

In 2024, Whole Bean coffee held 43.22% of the market, driven by Turkey's traditional cezve brewing and the UAE's demand for premium single-origin beans. Specialty roasters like RAW Coffee Company and Ludlow Coffee Group cater to UAE consumers willing to pay USD 20 to USD 40 per kilogram for traceable Ethiopian and Kenyan beans. Lavazza's launch of the Tibali brewing system in 2024, designed for whole-bean extraction, highlights its appeal to affluent consumers valuing flavor complexity. Turkey's annual per-capita coffee consumption, currently 1 to 1.2 kilograms, is expected to double to 2 kilograms by 2030, fueled by younger consumers exploring espresso-based drinks. While urbanization and time constraints may shift preferences toward pre-ground and instant coffee, Whole Bean's association with authenticity ensures a loyal customer base.

Ready-to-Drink coffee is projected to grow at a CAGR of 8.34% through 2030, the fastest among product types, as millennials in Saudi Arabia, Egypt, and the UAE embrace convenient, on-the-go formats. Ground Coffee, Instant Coffee, and Coffee Pods and Capsules occupy a middle ground. Instant Coffee benefits from affordability and long shelf life in price-sensitive markets like Egypt and Nigeria, while Coffee Pods and Capsules face challenges from environmental concerns and limited machine penetration outside Gulf Cooperation Council states. Nescafé's May 2024 launch of Espresso Concentrate, a liquid format for foodservice, addresses labor shortages in cafés and restaurants. RTD coffee's growth depends on expanding cold-chain infrastructure in North and Sub-Saharan Africa and managing sugar-tax regulations without compromising taste or margins.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Conventional Dominates, Specialty Surges

In 2024, conventional coffee accounted for 79.31% of the market, driven by the popularity of mass-market instant and ground coffee formats. These products cater to price-sensitive households in countries like Egypt, Nigeria, Morocco, and rural Turkey. Brands such as Nescafé, Jacobs, and local competitors utilize economies of scale to offer 100-gram jars priced affordably between USD 2 and USD 3. This pricing strategy positions coffee as an accessible daily necessity rather than a premium product. The segment's stronghold is further supported by institutional demand from hotels, restaurants, and offices, where cost efficiency and consistency take precedence over factors like origin or quality scores. However, the growth of this segment is slowing as urban consumers increasingly shift to specialty coffee options, and younger generations move away from the instant-coffee preferences of older demographics.

Specialty coffee is projected to grow at a robust 9.44% CAGR through 2030, making it the fastest-growing category. This growth is fueled by the expansion of third-wave coffee roasters in cities such as Riyadh, Dubai, Istanbul, and Johannesburg. These roasters focus on direct-trade Ethiopian and Kenyan coffee, which commands premiums of 200% to 400% over standard commodity coffee. The retail sector is also adapting to this trend, with UAE hypermarkets dedicating entire aisles to single-origin coffee products. Additionally, Saudi Arabia's DMCC Coffee Centre expanded its grading and storage facilities in 2024, aiming to establish Dubai as a key re-export hub for African specialty coffee. The future growth of this category will depend on the ability of roasters to implement scalable traceability systems that meet consumer expectations and on the resilience of disposable incomes in Gulf markets amid fluctuating oil prices.

By Coffee Species: Arabica Leads, Liberica Emerges

In 2024, Arabica coffee led the market with a 70.01% share, driven by its dominance in Ethiopian and Kenyan exports and its popularity among Gulf consumers who prefer its smooth, less bitter taste. Ethiopia's 2024/25 harvest is projected at 8.5 million bags, primarily Arabica. A new policy introduced in April 2024 allows direct foreign purchases, expected to channel premium lots to Middle Eastern roasters seeking unique offerings. Similarly, Kenya's 2024 auction reforms, enabling direct sales, have strengthened Arabica's position by allowing buyers to secure high-quality grades at better prices. Arabica's share is expected to remain steady due to strong consumer preferences and proximity to East African origins. However, Robusta's affordability and higher caffeine content make it competitive in instant-coffee blends and cost-sensitive markets.

Liberica coffee is forecast to grow at a 7.89% CAGR through 2030, the fastest among all species. Its low-acidity, fruity profile appeals to health-conscious consumers looking for alternatives to high-caffeine options. While primarily cultivated in the Philippines and Malaysia, trials in Uganda and Tanzania are exploring its potential in African soils, which could reduce import reliance. Specialty cafés in Dubai and Riyadh are introducing Liberica single-origin pour-overs, positioning it as a premium, exotic choice for adventurous consumers. Robusta, favored for its solubility and cost advantage, remains dominant in instant-coffee production. Uganda's 2024/25 Robusta harvest is projected at 6.87 million bags, largely destined for European and Asian instant-coffee manufacturers. The market reflects a balance between Robusta's high yield and resilience and the growing demand for premium Arabica and niche varieties like Liberica.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Off-Trade Holds Share, On-Trade Accelerates

In 2024, Off-Trade channels seized 69.42% of the market share, propelled by supermarkets, hypermarkets, and convenience stores. These outlets, known for their diverse selections and competitive pricing, have become the go-to spots for both instant and ground coffee. In the Gulf retail scene, Carrefour, Lulu Hypermarket, and Spinneys lead the pack. They skillfully leverage private-label products to offer prices that undercut branded counterparts, appealing to the budget-conscious shopper. Meanwhile, online retail is making significant inroads, especially in the UAE and Saudi Arabia. Platforms like Noon and Amazon.ae are not just selling products; they're introducing subscription models, ensuring steady revenue streams and allowing brands to sidestep the traditional challenges of shelf-space negotiations. Specialty stores, from boutique roasters to gourmet grocers, are tapping into the premium market. While their share in the Off-Trade segment is currently modest, it's on an upward trajectory as consumers increasingly value curated selections and transparency about product origins. Other Off-Trade avenues—like petrol stations, kiosks, and vending machines—offer quick purchase options for ready-to-drink and single-serve formats. However, their overall contribution remains limited, primarily concentrated in bustling urban areas.

Forecasts predict On-Trade channels will expand at a 9.23% CAGR through 2030, outpacing Off-Trade's anticipated 7.8% growth, thanks to the rising popularity of experiential retail and café culture. In a strategic move, Costa Coffee has teamed up with Saudi Arabia's Jazean Group, eyeing the operation of 100 stores. This collaboration harnesses local real-estate insights and cultural nuances, ensuring smooth navigation through zoning laws and labor-nationalization mandates. Black Sheep Coffee, not to be outdone, unveiled its ambitious plan in 2024 to roll out 250 stores across the Middle East and Africa. Their focus is on high-traffic malls and bustling business districts, offering premium espresso drinks alongside co-working spaces. The On-Trade channel's expansion is further bolstered by hotels, restaurants, and corporate cafeterias. These establishments are not just upgrading their equipment but are also refining their menus to align with heightened quality expectations. A testament to this trend is Nescafé's May 2024 introduction of Espresso Concentrate, designed specifically for this segment, promising barista-quality extraction with reduced labor demands. However, the future of this channel hinges on several factors: real-estate costs, the availability of labor, and the ability of café operators to maintain foot traffic in an era of normalized remote work and heightened scrutiny on discretionary spending.

Geography Analysis

The United Arab Emirates and Saudi Arabia dominate coffee consumption in the Middle East, driven by high incomes, expatriates with daily coffee habits, and government diversification efforts focused on hospitality and retail. The UAE's coffee market emphasizes premium offerings, with Dubai's specialty cafés rivaling European cities. In Saudi Arabia, Vision 2030 is fueling café growth, highlighted by Costa Coffee's partnership with Jazean Group to open 100 stores and Saudi Coffee Company's nine agreements signed in February 2024. These initiatives aim to boost local value-chain margins and reduce import reliance. In Turkey, traditional Turkish coffee remains popular in rural areas and among older demographics, while urban millennials in cities like Istanbul, Ankara, and Izmir increasingly prefer espresso-based drinks. Turkey's strategic location also makes it a key re-export hub for instant coffee to Central Asia.

South Africa leads Sub-Saharan Africa in coffee consumption, supported by strong retail infrastructure, a growing middle class, and a coffee culture rooted in European colonial history. Johannesburg and Cape Town have thriving specialty café scenes, and local roasters are sourcing from Zambia and Malawi to reduce reliance on East African imports. In North Africa, Egypt and Morocco are the largest markets, with instant and ground coffee dominating due to price sensitivity. Egypt's urban population, projected to reach 60 million by 2030, is driving demand for ready-to-drink and single-serve products. Ethiopia and Kenya, major coffee producers, are also emerging as consumers. Ethiopia's April 2024 policy change allowing direct foreign purchases aims to retain more specialty coffee locally, while Kenya's auction reforms are increasing farmgate prices and enabling smallholder investments in processing.

Other Middle Eastern and African markets, including Algeria, Tunisia, Kuwait, Bahrain, Oman, Uganda, Tanzania, and Ghana, show varied coffee consumption patterns. Algeria and Tunisia have French-inspired café cultures but face foreign-exchange challenges limiting premium imports. Kuwait, Bahrain, and Oman follow UAE and Saudi trends on a smaller scale, driven by expatriates and international café franchises. Uganda and Tanzania focus on production, with Uganda's 2024/25 Robusta harvest projected at 6.87 million bags, mostly exported to Europe and Asia for instant coffee[3]USDA Foreign Agricultural Service, "Coffee: World Markets and Trade", fas.usda.gov. However, urbanization is boosting domestic consumption, with local roasters targeting middle-income households with affordable ground coffee. The 2024 European Union Deforestation Regulation is pressuring Ugandan and Tanzanian exporters to adopt traceability systems, increasing costs for smallholders and potentially shifting supply to less-regulated markets in the Middle East and Asia.

Competitive Landscape

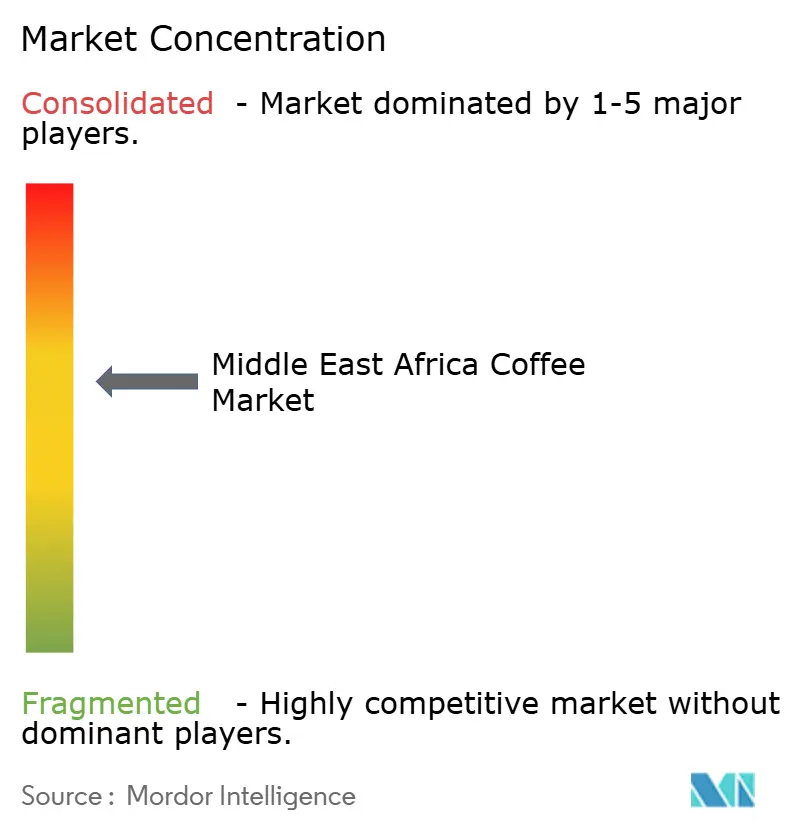

The Middle East Africa coffee market is moderately consolidated, with global brands and strong regional roasters shaping competition in key areas. Multinational companies use their scale, sourcing networks, and premium positioning to maintain visibility in modern retail. Key players in the market include Nestlé SA, JDE Peet’s N.V., Starbucks Corporation, Luigi Lavazza S.p.A., and Strauss Group Ltd. On the other hand, regional players focus on local tastes and flexible pricing to build loyalty in traditional trade. While specialty cafés and micro-roasters bring variety, their market share remains small compared to larger players. In East Africa, vertical integration in supply chains helps producers and exporters improve quality control and traceability.

North Africa and Sub-Saharan markets offer growth opportunities, as coffee consumption per person is still below 1 kilogram annually. Brands that can handle challenges like currency fluctuations, import tariffs, and fragmented distribution networks could gain a first-mover advantage. Technology is playing a bigger role, especially in supply-chain traceability. For example, JDE Peet's has introduced blockchain pilots to verify coffee origins and meet the European Union Deforestation Regulation. Smaller roasters lack such capabilities, which could lead to a shift in market share toward compliant companies.

New players are also entering the market. Saudi Coffee Company, supported by the Public Investment Fund, signed nine partnership agreements in February 2024 to secure supply and expand domestic roasting. This positions the company as a vertically integrated competitor to global brands. Additionally, Ethiopian and Kenyan cooperatives are bypassing traditional exporters by directly working with Gulf roasters. Policy changes allowing direct foreign buying and auction system reforms enable this shift, which challenges established traders and creates opportunities for roasters willing to invest in direct relationships with producers.

Middle East Africa Coffee Industry Leaders

-

Nestlé SA

-

JDE Peet’s N.V.

-

Starbucks Corporation

-

Luigi Lavazza S.p.A.

-

Strauss Group Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Douwe Egberts introduced its D.E. Excellent capsule range in South Africa, targeting the growing demand for premium at-home coffee experiences. According to the company, this product launch highlights the evolving market and manufacturers' responsiveness to consumer preferences.

- September 2024: Juan Valdez, a prominent Colombian coffee brand, opened a new store in Ankara's Kızılay district, marking the occasion with a special event. This highlights how leading coffee companies utilize flagship store openings and experiential marketing to attract consumer interest.

- August 2024: Barns Café opened its first branch in Egypt, located in the City Stars Mall in Cairo. The outlet offers a wide range of Barns’ signature brews and carefully crafted beverages, aiming to provide a premium coffee experience for visitors.

- July 2024: Moldova’s Tucano Coffee launched its first Turkish outlet at Istanbul’s Tuzla Port shopping center, highlighting the appeal of Turkey’s urban coffee market and the rising demand for diverse, globally inspired café experiences.

Middle East Africa Coffee Market Report Scope

Cold Brew Coffee, Iced coffee are covered as segments by Soft Drink Type. Aseptic packages, Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Qatar, Saudi Arabia, United Arab Emirates are covered as segments by Country.

By Product Type

| Whole Bean |

| Ground Coffee |

| Instant Coffee |

| Coffee Pods and Capsules |

| RTD Coffee |

By Category

| Conventional Coffee |

| Specialty |

By Coffee Species

| Arabica |

| Robusta |

| Liberica |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/ Grocery Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Off-trade Channels |

By Country

| United Arab Emirates |

| South Africa |

| Saudi Arabia |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Whole Bean | |

| Ground Coffee | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| RTD Coffee | ||

| By Category | Conventional Coffee | |

| Specialty | ||

| By Coffee Species | Arabica | |

| Robusta | ||

| Liberica | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/ Grocery Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Off-trade Channels | ||

| By Country | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms

Get More Details On Research Methodology

Download PDF