Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

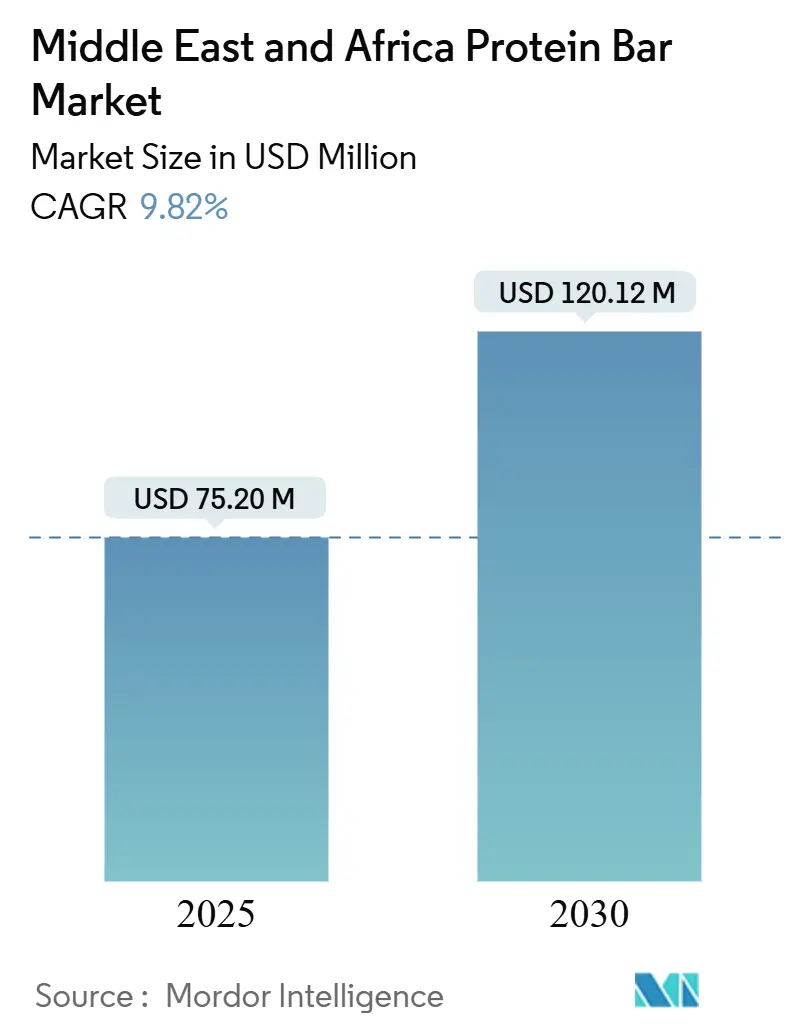

| Market Size (2025) | USD 75.20 Million |

| Market Size (2030) | USD 120.12 Million |

| Growth Rate (2025 - 2030) | 9.82% CAGR |

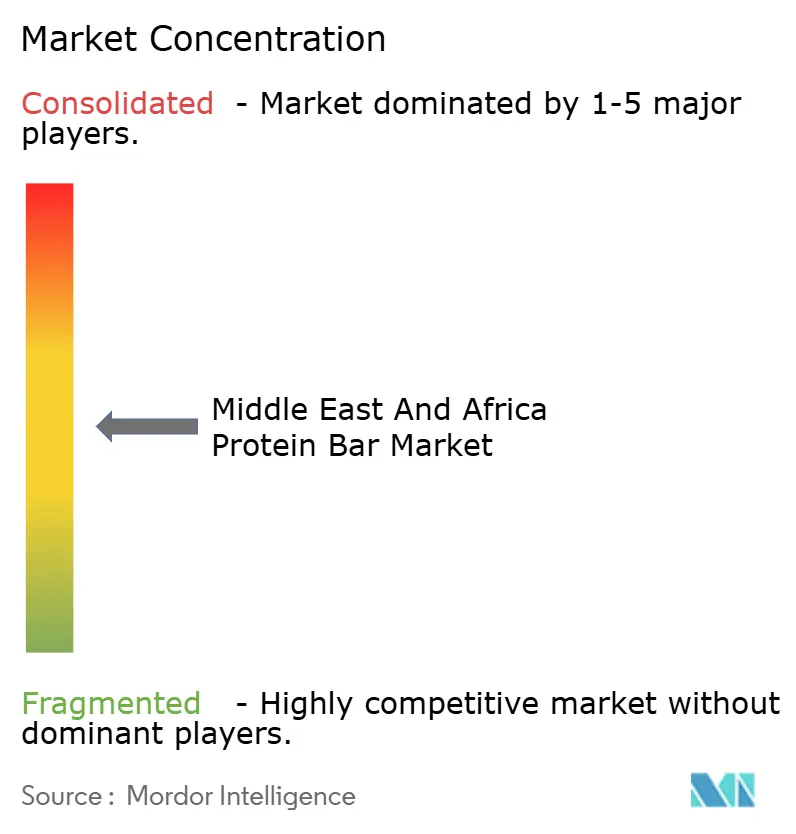

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Protein Bar Market Analysis by Mordor Intelligence

The Middle East and Africa protein bar market size is estimated to be USD 75.20 million in 2025 and is projected to reach USD 120.12 million by 2030, registering a robust 9.82% CAGR. The current growth wave is shaped by higher disposable incomes, rapid urbanization, and intensified government action on obesity, all of which expand the consumer base for portable protein snacks. Investment momentum is further fueled by regulatory frameworks that now classify protein bars as functional foods, simplifying import approvals and enabling faster product launches under the Saudi Food and Drug Authority’s hygiene and labeling standards. Regional manufacturers leverage Western flavor formats while integrating local ingredients such as dates and pistachios, creating compelling value propositions that resonate with both expatriate and native consumer segments. Consolidation among multinational confectionery giants adds marketing muscle to the category, yet mid-sized local brands still find space to differentiate through clean-label claims, halal certifications, and plant-forward recipes. Growing e-commerce penetration, especially in the Gulf Cooperation Council (GCC), enhances category visibility and offers a low-entry cost route for new labels targeting lifestyle-oriented millennials.

Key Report Takeaways

- By protein type, animal protein held 64.23% of the Middle East and Africa protein bar market share in 2024, while plant protein is forecast to expand at an 11.22% CAGR through 2030.

- By flavor type, chocolate-based variants led with 46.76% revenue share in 2024; fruit-based bars are projected to grow at a 10.88% CAGR to 2030.

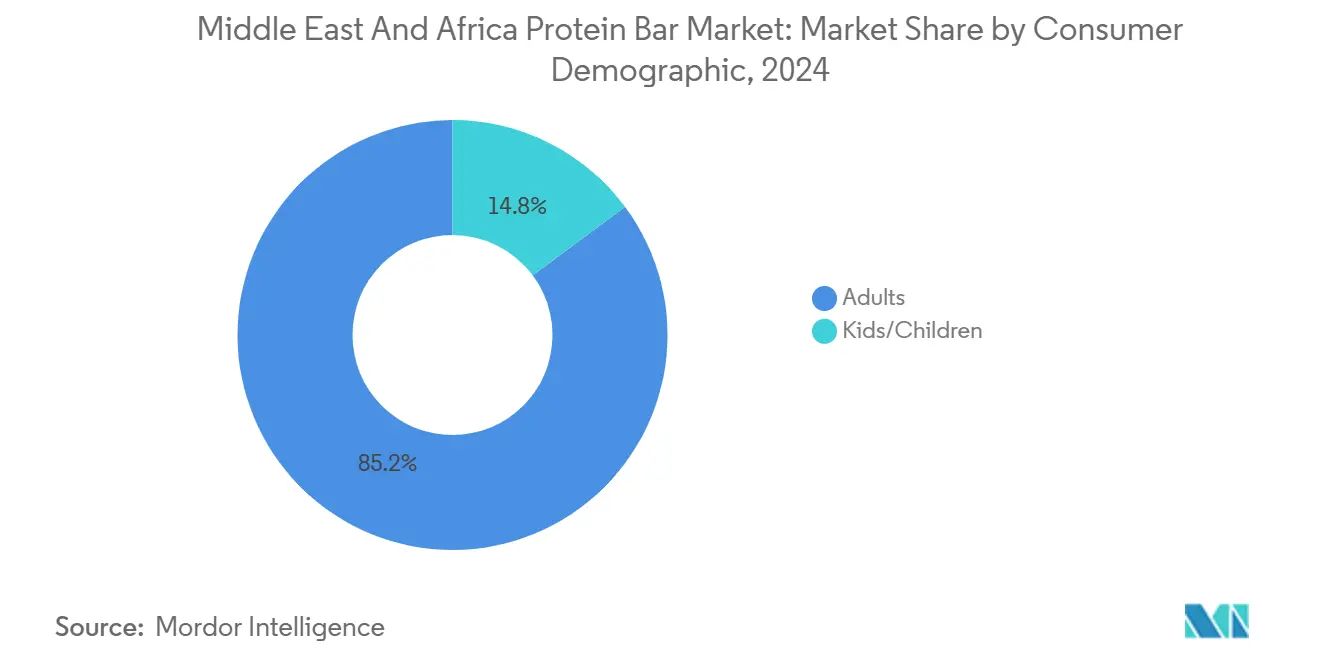

- By consumer demographic, adults accounted for 85.17% of sales in 2024, while children’s products are advancing at an 11.64% CAGR through 2030.

- By distribution channel, supermarkets/hypermarkets captured 65.41% share of the Middle East and Africa protein bar market in 2024, whereas online retail is recording an 11.37% CAGR through 2030.

- By country, Saudi Arabia commanded 29.85% of 2024 revenue; the United Arab Emirates is on track for the fastest growth at a 10.33% CAGR to 2030.

Middle East And Africa Protein Bar Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in sports/fitness culture | +2.1% | GCC core, spill-over to North Africa | Medium term (2-4 years) |

| Rising health-and-wellness consciousness | +2.8% | Regiona, strongest in United Arab Emirates and Saudi Arabia | Long term (≥ 4 years) |

| Government-led obesity reduction programmes | +1.9% | Saudi Arabia, United Arab Emirates, Egypt primary focus | Medium term (2-4 years) |

| Product innovation and flavor diversity | +1.7% | Regional with premium positioning in GCC | Short term (≤ 2 years) |

| Consumer prioritization of clean label and functional claims | +1.4% | United Arab Emirates, Saudi Arabia, urban centers across Middle East and Africa | Long term (≥ 4 years) |

| Influence of western and expat trends | +1.2% | GCC markets, expatriate communities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in sports/fitness culture

Rising health consciousness and physical activity levels are transforming protein consumption patterns, with government initiatives implementing wellness programs beyond athletic communities. Saudi Arabia's Vision 2030 promotes physical activity, with GASTAT data indicating that in 2024, 58.5% of individuals aged 18 and above engage in 150 minutes or more of weekly physical activity, while 18.7% of children and adolescents aged 5-17 meet the daily 60-minute activity requirement [1]Source: General Authority for Statistics (GASTAT), "General Authority for Statistics Announces Physical Activity Statistics for Saudi Arabia in 2024", mos.gov.sa. The UAE's National Program for Happiness and Wellbeing incorporates fitness metrics into quality-of-life indicators, supporting the shift toward active lifestyles. This government support increases demand for convenient protein solutions, including protein bars that meet active lifestyle requirements. The growth of fitness facilities, including boutique gyms and women-focused centers, along with corporate wellness programs in urban areas, creates opportunities for premium nutritional products. The adoption of sports nutrition in daily wellness routines has expanded protein bar consumption beyond athletes to health-conscious consumers. Companies like Barebells and Quest Nutrition are responding by developing products for this broader consumer base. The combination of fitness culture growth, government policies, and improved infrastructure continues to increase protein bar demand in the Middle East and Africa market.

Rising health-and-wellness consciousness

Rising obesity rates and increasing health awareness are driving significant changes in consumer behavior across the Middle East and Africa. The region faces an obesity crisis, with the growing prevalence of diabetes emphasizing the critical need for effective dietary management. This combination of medical necessity and enhanced consumer education is fueling sustainable market growth, unaffected by typical economic fluctuations. Protein-dense snacks are gaining clinical endorsement from healthcare providers and nutritionists, strengthening the perception of protein bars as health-promoting products. These endorsements support the premium positioning of protein bars, aligning with a market that is shifting from awareness to proactive nutritional decision-making. The alarming obesity rates in certain Middle Eastern countries further highlight the importance of protein bars in promoting healthier dietary habits. Companies like Barebells are leveraging this trend by offering convenient, nutrient-rich protein bars that appeal to health-conscious consumers. Consequently, the growing focus on health and wellness is driving structural expansion in the MEA protein bar market, positioning it as a critical solution for addressing diet-related diseases and improving public health outcomes.

Government-led obesity‐reduction programmes

Regulatory support through government health initiatives provides opportunities for functional nutrition products, including protein bars, while creating restrictions for traditional confectionery items. Saudi Arabia's Vision 2030 includes health transformation programs focused on reducing obesity through better nutrition choices. In September 2024, the Ministry of Health and Prevention (MoHAP) collaborated with Novo Nordisk Pharma Gulf to introduce a national scientific guide for obesity management and weight control, which forms part of the country's National Strategy for Preventing and Managing Non-communicable Diseases [2]Source: Ministry of Health and Prevention (MoHAP), "Ministry of Health and Prevention: Combating Obesity is a Strategic Health Priority, Overseen by a Highly Skilled National Team", mohap.gov.ae. The regulatory frameworks implement policies such as sugar taxes and mandatory caloric labeling that limit traditional snack consumption. These regulations benefit protein bar manufacturers who provide nutritious alternatives, creating a competitive advantage. Government health objectives support product innovation and premium positioning, as demonstrated by companies like Optimum Nutrition, which focuses on clinical validation and health benefits for MEA consumers. The combination of public health policies and business strategies is transforming snacking preferences and increasing protein bar adoption across urban and semi-urban areas in the MEA region.

Influence of western and expat trends

Western and expatriate trends are significantly shaping consumer preferences in the Middle East and Africa, particularly in urban areas with large expatriate populations. For instance, in Kuwait, non-Kuwaiti residents account for 68.3% of the total population, according to the Public Authority for Civil Information, highlighting a substantial expatriate presence [3]Source: Indian Frontliners Association, "68.6% of Kuwait's Population, Which is Close to 5 Million, are Expatriates", iflkuwait.com. This demographic drives demand for Western-style health and fitness products, including protein bars, as they bring their nutritional preferences and consumption habits. These consumers typically seek convenient, protein-rich snacks that align with active lifestyles and wellness-focused diets, fueling local market growth. Western brands such as Clif, Optimum Nutrition, Quest Nutrition, and Barebells have effectively leveraged this trend by offering familiar, high-quality protein bars that appeal to both expatriates and health-conscious locals. The expatriate influence fosters market diversification, encouraging the introduction of a wider range of flavors, formulations, and premium positioning. Additionally, these trends are driving retail innovation, supporting expansion in modern grocery outlets, specialty health stores, and online channels, thereby creating a robust distribution network catering to diverse preferences. This cross-cultural nutrition adoption is progressively integrating into everyday consumer behavior, transforming protein bars from niche athletic supplements into mainstream wellness staples across the MEA region.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus traditional snacks | -1.8% | Price-sensitive markets: Egypt, Morocco, Nigeria, rural areas | Short term (≤ 2 years) |

| Low product awareness in underdeveloped regions | -1.3% | Rural areas across Middle East and Africa, secondary cities, Sub-Saharan Africa | Medium term (2-4 years) |

| Regulatory and import/labeling barriers | -1.1% | Cross-border trade corridors, emerging markets with evolving frameworks | Medium term (2-4 years) |

| Short shelf life and storage challenges | -0.9% | Hot climate regions, limited cold chain infrastructure areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium price versus traditional snacks

Price sensitivity in emerging markets significantly limits the adoption of protein bars, as many consumers in the Middle East and Africa prioritize essential goods over functional nutrition when managing limited household budgets. This is particularly evident in price-volatile economies such as Egypt and Morocco, where purchasing decisions are closely tied to immediate affordability. The substantial cost difference between protein bars and traditional snacks, such as biscuits, local pastries, and fried street foods, reinforces this limitation, leading to the perception of protein bars as discretionary or "treat" items rather than everyday staples. Economic volatility further amplifies risk aversion, with consumers carefully evaluating functional benefits like satiety, protein content, and perceived health outcomes against the short-term appeal of cheaper, more familiar alternatives. This dynamic underscores the importance of strategic pricing strategies, including entry-sized SKUs and mixed promotional bundles, alongside clear value communication that translates premium positioning into tangible nutritional benefits. Successful brands are increasingly shifting from simple shelf-price comparisons to a "value-per-gram of protein" approach. This strategy demonstrates that, on a protein-yield basis, a protein bar can outperform multiple low-cost snacks while also supporting weight management or fitness goals. International players in the region, such as locally distributed MyProtein bars, often emphasize this narrative by highlighting high protein content and targeted functionality to justify higher unit prices. However, this approach must be carefully balanced to avoid alienating mass-market consumers. Localized messaging that connects protein density and prolonged satiety to budget-conscious household decision-making is essential. Over time, consistent consumer education on value-per-gram protein and associated health benefits may gradually reduce price resistance. However, until then, the premium pricing of protein bars compared to traditional snacks will remain a structural barrier to category penetration in the Middle East and Africa protein bar market.

Low product awareness in underdeveloped regions

Low product awareness in underdeveloped regions across the Middle East and Africa continues to impede the expansion of the protein bar market. Limited consumer education on the nutritional benefits of protein, including its role in satiety, muscle maintenance, and overall health, results in traditional staples dominating purchasing decisions in secondary cities and rural areas. These regions often lack exposure to sports nutrition culture and modern health trends, which are critical drivers of protein bar adoption in urban centers. This perception of protein bars as unfamiliar or unnecessary products is further compounded by weak distribution infrastructure, which creates physical access barriers in areas where supermarkets, pharmacies, and specialty health outlets are sparse. As a result, even interested consumers face challenges in trialing or repurchasing protein bars. Consequently, modern protein nutrition remains concentrated in urbanized markets such as the United Arab Emirates, Saudi Arabia, and South Africa, leaving significant geographic areas underpenetrated despite rising health concerns. Addressing this issue requires targeted educational initiatives to equip healthcare providers and fitness professionals with practical protein knowledge, leveraging their trusted status to reframe protein bars as functional and legitimate options. Integrating protein education into government health and nutrition programs, such as school nutrition campaigns or non-communicable disease (NCD) strategies, offers a cost-effective way to align public health objectives with market development. Brands can collaborate with local stakeholders to pilot awareness and sampling programs, linking familiar confectionery brands with enhanced protein functionality. Over time, a combination of education, improved distribution, and community-based advocacy will be essential to overcoming low product awareness and driving market growth.

Segment Analysis

By Protein Type: Plant Alternatives Accelerate Despite Animal Dominance

In 2024, animal protein formulations hold a dominant 64.23% share of the protein bar market in the Middle East and Africa. This dominance is primarily driven by consumer demand for whey and casein proteins, recognized for their complete amino acid profiles essential for muscle building and recovery. However, plant protein alternatives are experiencing significant growth, with a projected CAGR of 11.22% through 2030. This growth is driven by increasing awareness of sustainability and dietary restrictions, such as lactose intolerance and veganism, which are expanding the consumer base. Protein type segmentation highlights a strategic opportunity in hybrid protein bars. These products combine animal and plant proteins, delivering nutritional completeness while addressing environmental concerns, thereby appealing to a more conscientious market.

Advancements in plant protein technology, particularly high-moisture extrusion processing, have resolved traditional challenges related to texture and flavor, significantly increasing consumer acceptance in the MEA market. Chickpea and pea protein isolates, in particular, align with regional dietary preferences for legumes, enhancing protein density and market appeal. Additionally, regulatory bodies across the region are facilitating plant protein innovation by streamlining approvals for novel sources and functional foods, creating opportunities for product development. Brands such as MyProtein are leveraging these advancements to introduce plant-forward bars tailored to health-conscious consumers in the MEA region, effectively capitalizing on the intersection of tradition, innovation, and sustainability within the evolving protein bar market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Flavor Type: Fruit Innovation Challenges Chocolate Leadership

In 2024, chocolate-based formulations dominate the market, capturing a significant 46.76% share. This dominance is attributed to their widespread consumer appeal, driven by the universal popularity of chocolate as a flavor and its strong association with indulgence. Additionally, chocolate-based products have successfully positioned themselves as functional nutrition solutions, appealing to health-conscious consumers seeking a balance between taste and nutritional benefits. On the other hand, fruit-based alternatives are emerging as the fastest-growing segment, recording an impressive 10.88% CAGR. This growth reflects a shift in consumer preferences toward products perceived as natural and wholesome. The inclusion of fruit flavors not only aligns with the demand for clean-label ingredients but also provides opportunities for vitamin fortification, enabling brands to differentiate themselves by offering benefits that extend beyond basic protein delivery. Furthermore, the flavor segmentation landscape highlights significant potential for integrating regional taste preferences. For instance, flavors such as date, fig, and pomegranate have gained strong traction among Middle Eastern consumers, showcasing the importance of tailoring offerings to specific cultural and regional demands.

Nut and seed-based flavors hold their ground in the market, yet present differentiation avenues through the incorporation of indigenous ingredients. Formulations like pistachio, almond, and sesame not only align with regional agricultural strengths but also cater to evolving consumer tastes. Savory and herbal flavors are carving out a niche, expanding the market's horizons beyond the traditional sweet realm. This is especially true for adult consumers, who are increasingly seeking sophisticated profiles that enhance their professional dining experiences. Advanced flavor masking technologies are tackling the age-old challenge of plant protein bitterness. This innovation paves the way for a broader flavor exploration, bolstering market segmentation strategies that cater to a diverse demographic spectrum.

By Consumer Demographic: Adult Dominance with Accelerating Youth Adoption

In 2024, adult consumers in the Middle East and Africa hold a commanding 85.17% share of the protein bar market, driven by their strong purchasing power and increasing focus on health and wellness. This segment, primarily comprising professionals and fitness enthusiasts, demonstrates a clear preference for premium protein products. Their purchasing behavior is further influenced by workplace wellness programs and strategic collaborations with fitness facilities, which integrate protein nutrition into comprehensive lifestyle improvement initiatives. The stability of this demographic provides a solid foundation for sustained market growth and fosters opportunities for product innovation. Concurrently, the children's segment is experiencing significant growth, with a projected CAGR of 11.64% through 2030. This growth is fueled by targeted educational campaigns and the development of reformulated protein bars designed to align with children's taste preferences, thereby making nutritional products more appealing to younger consumers.

The increasing emphasis on pediatric nutrition highlights the critical role of protein in supporting growth and development, a perspective reinforced by endorsements from healthcare professionals. This trend is driving the expansion of the children's segment and creating opportunities for brands to implement differentiated life-stage marketing strategies. By addressing the needs of both adult and child consumers and leveraging family-oriented marketing approaches, companies can capitalize on household purchasing patterns to maximize market penetration. For instance, Clif Bar has effectively adopted this strategy by offering tailored protein bar solutions that cater to diverse age groups, meeting the evolving nutritional demands across the MEA region. This strategic demographic segmentation not only accelerates growth within individual consumer segments but also promotes synergistic market expansion through integrated family health and wellness initiatives.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Digital Disruption Accelerates Traditional Retail Evolution

In 2024, supermarkets/hypermarkets retain a commanding 65.41% market share, highlighting their entrenched position as the preferred shopping destinations for consumers. This dominance is attributed to well-established consumer shopping behaviors and retailer-driven category management strategies that prioritize protein nutrition within health and wellness sections. On the other hand, online retail channels are experiencing rapid growth, emerging as the fastest-growing distribution segment with a robust 11.37% CAGR. This growth trajectory is propelled by significant investments in e-commerce infrastructure and the increasing adoption of digital payment systems across MEA markets. The ongoing evolution of distribution channels presents lucrative opportunities for businesses to adopt omnichannel strategies, effectively integrating the physical retail experience with the convenience and accessibility of digital platforms to meet diverse consumer demands.

Specialty stores and convenience channels play complementary yet critical roles in driving market development. Specialty retailers differentiate themselves by offering expert consultations and in-depth product education, catering to consumers seeking informed purchasing decisions. Conversely, convenience stores capitalize on impulse buying behaviors, aligning their offerings with the fast-paced, on-the-go consumption patterns of modern consumers. Additionally, the integration of subscription-based delivery models is transforming customer engagement strategies. These models not only enhance customer retention by fostering long-term relationships but also create predictable revenue streams for businesses. By leveraging automated replenishment systems, companies can reduce customer acquisition costs while ensuring consistent product availability. Furthermore, digital transformation initiatives across traditional retail channels, such as the implementation of click-and-collect services and mobile payment solutions, are reshaping the retail landscape. These advancements blur the lines between traditional and digital channels, enabling businesses to expand their market reach and cater to a broader spectrum of consumer segments.

Geography Analysis

Saudi Arabia's dominant position, with a 29.85% market share in 2024, underscores the kingdom's robust consumer spending power and its comprehensive health transformation initiatives under Vision 2030. These initiatives focus on reducing obesity and enhancing nutrition across the population. The regulatory framework, led by the Saudi Food and Drug Authority, facilitates functional food innovation through guidelines on food hygiene, import controls, and product classification, creating favorable conditions for international brand entry and local manufacturing growth. In 2024, Agthia Group's launch of a protein manufacturing facility in Saudi Arabia highlights growing corporate confidence in local production capabilities and supply chain optimization. Furthermore, the kingdom's young demographic and increasing fitness facility penetration drive sustained demand, supporting premium positioning strategies for protein nutrition products.

The United Arab Emirates is the fastest-growing market, with a projected CAGR of 10.33% through 2030. This growth is driven by its cosmopolitan expatriate population and government initiatives that integrate wellness metrics into broader quality-of-life programs. Dubai Municipality's health supplement guidelines provide clear regulatory pathways for functional food products while ensuring consumer safety, strengthening market confidence. The United Arab Emirates's advanced e-commerce infrastructure and high digital payment adoption rates enable the development of online retail channels. Local startups have successfully launched functional beverages addressing regional hydration and nutrition needs. The combination of regulatory support, infrastructure advancements, and consumer sophistication positions the United Arab Emirates as a strategic entry point for international protein nutrition brands.

Egypt, Nigeria, Morocco, and Turkey present diverse market development opportunities, each with unique regulatory environments and consumer preferences requiring tailored entry strategies. Egypt's high obesity prevalence creates an urgent need for dietary intervention solutions, while its large population offers significant scale opportunities for well-positioned products. Nigeria's demographic trends and urbanization indicate long-term potential, despite current infrastructure challenges and price sensitivity. Morocco benefits from investments in premium snacking infrastructure, reflecting local market confidence and production capability growth. Turkey's strategic geographic location and established food processing industry provide opportunities for developing regional distribution hubs to support broader Middle East And Africa market expansion strategies.

Competitive Landscape

The protein bar market in the Middle East and Africa (MEA) is characterized by moderate fragmentation, with a mix of local and international players competing to meet diverse consumer preferences. Gulf countries tend to favor premium nutrition products, while broader African markets prioritize affordable functional snacks. This variation in demand creates opportunities for innovative companies to introduce differentiated offerings, particularly those utilizing unique ingredient profiles. For instance, brands incorporating high-quality plant proteins, such as ALOHA, or dairy-derived whey from Glanbia Nutritionals, can address both taste and performance requirements. Emerging players that adapt formulations to local dietary needs and preferences can effectively capture niche segments, demonstrating how fragmentation fosters innovation.

Meanwhile, established brands are actively consolidating their market presence through strategic initiatives. Companies like Mars' KIND Protein Bars and Quest Nutrition are expanding their distribution networks and enhancing production capabilities to meet the rising demand across the region. These efforts streamline supply chains and ensure consistent product availability in both modern retail and e-commerce channels, where consumer penetration is growing rapidly. By scaling operations, leading players gain a competitive advantage in pricing, making it challenging for smaller competitors to compete without similar infrastructure. This consolidation trend underscores how established companies enhance their market position while fostering overall category growth.

The competitive dynamics in the MEA protein bar market are shaped by the balance between fragmentation and consolidation. Moderate fragmentation allows new entrants to drive innovation, particularly when supported by ingredient brands like Beneo’s functional fiber or Arla Foods Ingredients’ whey peptides, which enhance nutritional value. At the same time, consolidation by major players stabilizes the market, creating consistent quality and trust benchmarks for consumers. Successful entrants align their product development with emerging health trends, such as clean-label formulations and plant-based proteins, while leveraging insights from the distribution strengths of larger competitors. Together, innovation and strategic expansion define competition and growth in this market.

Middle East And Africa Protein Bar Industry Leaders

-

Simply Good Foods Company

-

Mondelēz International, Inc.

-

Vitamin Well Group

-

Kellanova

-

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: MaxiNutrition launched its Pistachio Waffle Protein Bar, combining indulgence with purpose. Inspired by Dubai's chocolate trend, the company developed a bar designed to align with fitness goals without compromising taste. Each bar contained 15g of premium protein to support muscle growth and recovery. With no artificial colors or flavors, the product emphasized clean, trusted ingredients. Whether used pre- or post-workout, or as a smart snack during the day, the bar seamlessly fits into consumers' routines.

- April 2024: FULFIL Chocolate Protein Bars, a global leader in the nutritious snacking market, launched in South Africa and became available at Spar Stores and Clicks outlets nationwide. The bars offered a strategic combination of low sugar, high protein, and nine essential vitamins. Consumers could choose from four flavors: Salted Caramel, Peanut and Caramel, Hazelnut Whip, and Chocolate Brownie.

- January 2024: Shastowitz's food division entered the sports nutrition market, launching a new brand named "TODAY" in Israel. The initial product offerings under the brand were innovative protein bars featuring an impressive protein-to-calorie ratio of 1:10. These bars, designed for both men and women, served as an ideal recovery snack post-workout and a flavorful treat throughout the day. Flavors included salted caramel, cookie cream, cinnamon pie, chocolate, and banana chocolate chips.

Middle East And Africa Protein Bar Market Report Scope

The Middle-East and African protein bar market is segmented by distribution channel into supermarkets/hypermarkets, convenience stores, specialist retail stores, online stores, and other distribution channels. Additionally, the study provides an analysis of the protein bar market in the emerging and established markets across the region, including South Africa, Saudi Arabia, and Rest of Middle-East and Africa.

By Protein Type

| Animal Protein |

| Plant Protein |

By Flavor Type

| Chocolate-based |

| Fruit-based |

| Nut/Seed-based |

| Others (Savory/Herbal flavors, Exotic and Dessert-inspired) |

By Consumer Demographic

| Adults |

| Kids/Children |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Protein Type | Animal Protein |

| Plant Protein | |

| By Flavor Type | Chocolate-based |

| Fruit-based | |

| Nut/Seed-based | |

| Others (Savory/Herbal flavors, Exotic and Dessert-inspired) | |

| By Consumer Demographic | Adults |

| Kids/Children | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Country | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Middle East and Africa protein bar market?

The market is valued at USD 75.20 million in 2025 and is set to reach USD 120.12 million by 2030.

Which country leads regional sales?

Saudi Arabia holds the largest share at 29.85% of 2024 revenue, supported by high consumer spending and pro-fitness policies.

What protein type is gaining the most traction?

Plant-based bars are expanding at an 11.22% CAGR owing to sustainability appeals and lactose-free positioning.

How fast is online retail growing in the region?

Online sales are registering an 11.37% CAGR, driven by high smartphone usage and widespread digital payment adoption.

Page last updated on: