Micro LED Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

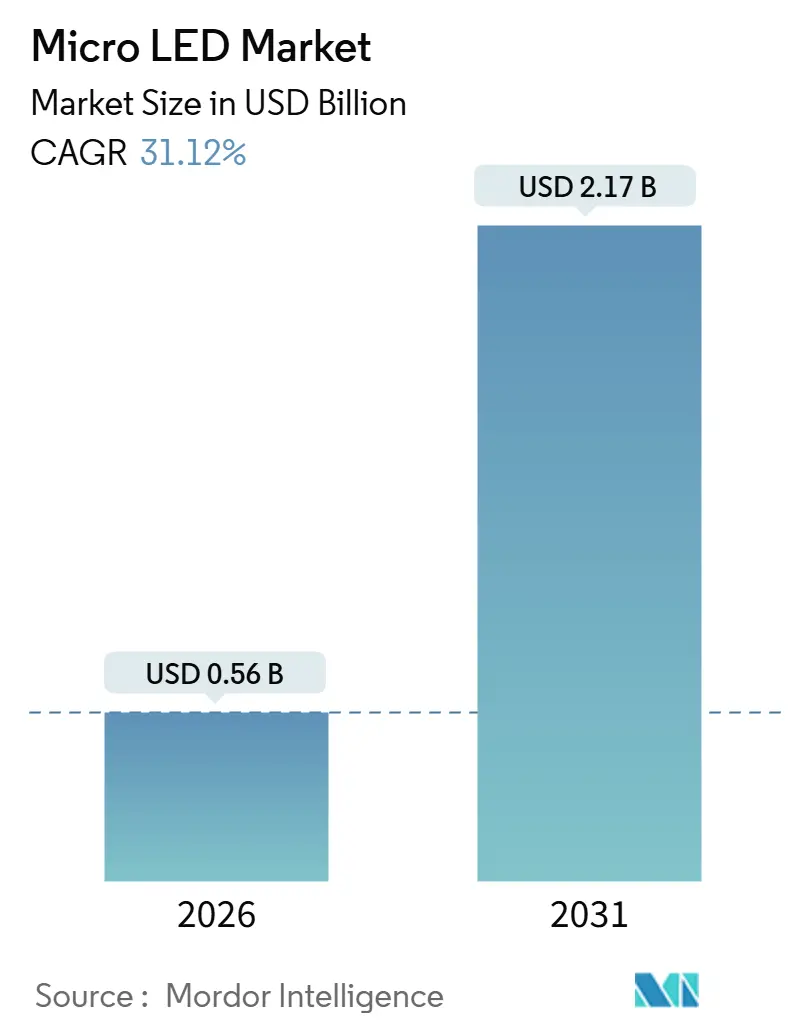

| Market Size (2026) | USD 0.56 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 31.12% CAGR |

| Fastest Growing Market | Middle East |

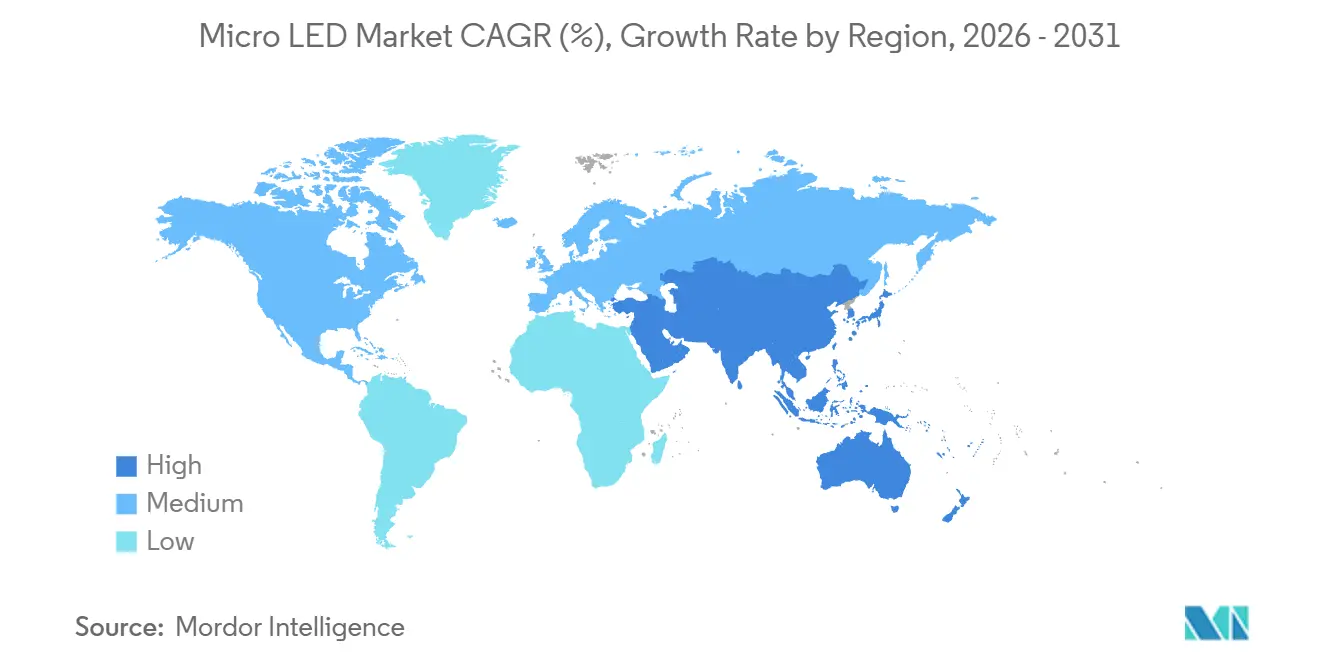

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro LED Market Analysis by Mordor Intelligence

The Micro LED Market size is estimated at USD 0.56 billion in 2026, and is expected to reach USD 2.17 billion by 2031, at a CAGR of 31.12% during the forecast period (2026-2031). Surging capital re-allocation from OLED and mini-LED toward micro-scale epitaxy, together with defense procurement of ultra-bright head-up displays, underpins this expansion. Pilot lines in Taiwan, China, and South Korea are resolving the historic mass-transfer yield bottleneck, while quantum-dot color conversion trims epitaxial complexity and accelerates time-to-yield. Wearables remain the gateway use-case, yet near-eye augmented-reality devices-where 3,000+ PPI density is mandatory-are pacing the revenue curve. Fine-pitch digital signage is also scaling quickly as transparent modules replace static LED billboards in high-footfall retail corridors across Gulf Cooperation Council cities and East Asia. In parallel, healthcare theaters and robotic-surgery suites are adopting daylight-readable micro-LED monitors to reduce heat dissipation and improve color fidelity during minimally invasive procedures.

Key Report Takeaways

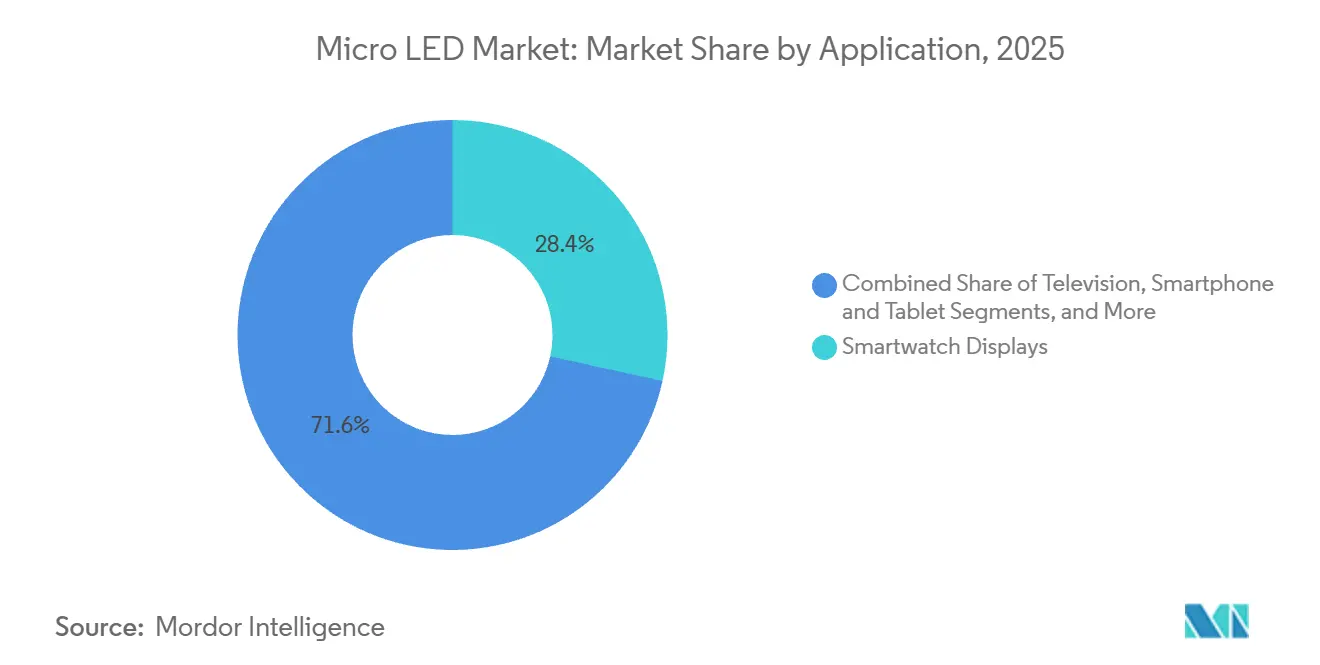

- By application, smartwatch displays led with 28.43% revenue share in 2025, near-to-eye devices (AR/VR) are forecast to expand at a 32.61% CAGR through 2031.

- By end-use industry, consumer electronics accounted for 40.12% of the Micro LED market share in 2025, while the healthcare sector is projected to grow at a 33.37% CAGR through 2031.

- By panel size, panels smaller than 10 inches accounted for a 46.78% share of the Micro LED market size in 2025; these panels are expected to advance at a 32.83% CAGR through 2031.

- By pixel pitch, fine-pitch panels with a pitch of under 1.5 mm commanded 51.36% of the revenue in 2025 and are expanding at a 33.46% CAGR.

- By technology, RGB full-color architectures accounted for 78.67% shipments in 2025 and are growing at a 35.79% CAGR.

- By component, epitaxial wafers accounted for a 34.28% revenue share in 2025; the Driver IC segment is expected to rise at a 34.23% CAGR through 2031.

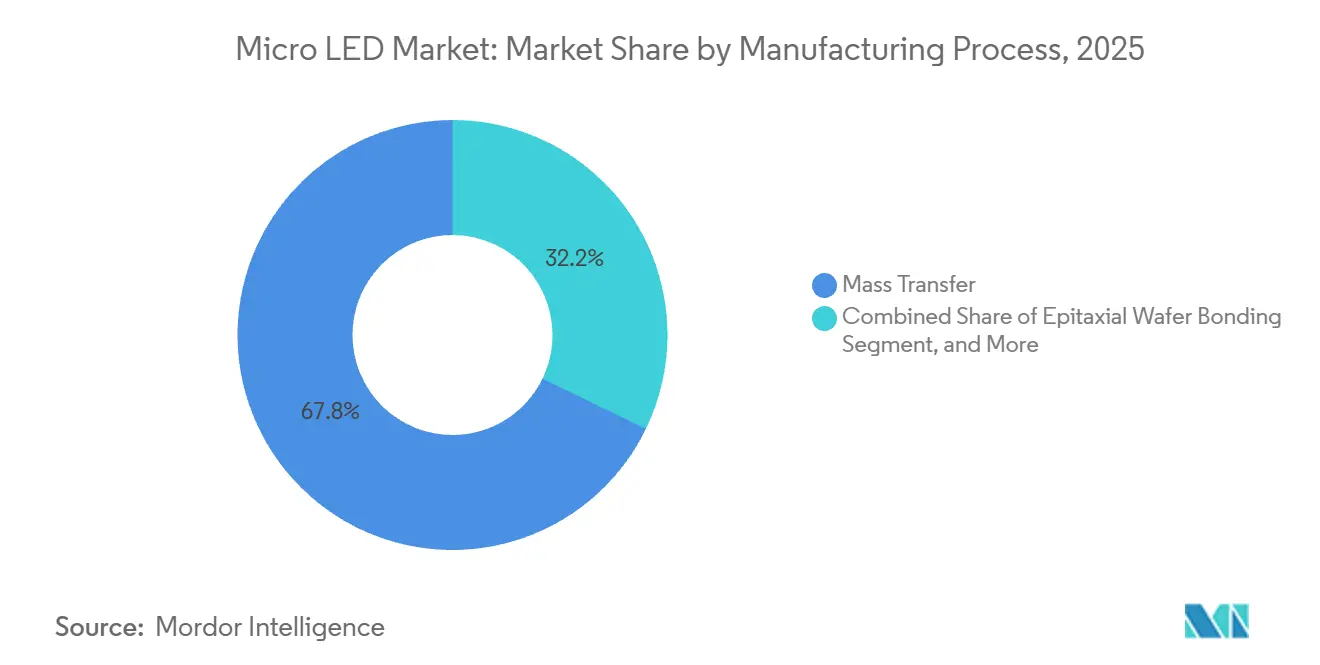

- By manufacturing process, mass transfer covered 67.81% of output in 2025; hybrid bonding is projected to climb at a 32.19% CAGR to 2031.

- By offering, display modules dominated with 71.24% revenue share in 2025; lighting modules are on track for a 32.04% CAGR through 2031.

- By region, Asia Pacific led with 66.42% revenue share in 2025; Middle East is poised to expand at a 32.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro LED Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Apple and Samsung Roadmaps for Micro-LED Wearables Accelerating Small-Display Demand | +6.2% | Global, Early Focus in North America and East Asia | Medium Term (2–4 Years) |

| Transparent and Flexible Retail Signage Uptake in Gulf Cooperation Council Countries and East Asia | +4.8% | Middle East and East Asia | Short Term (≤ 2 Years) |

| Defense-Grade Micro-Displays Funded by United States and EU Governments | +5.1% | North America and Europe | Medium Term (2–4 Years) |

| Taiwanese Mini-LED Cost Decline Enabling Pilot Micro-LED Lines | +7.3% | Global, Manufacturing in Taiwan | Long Term (≥ 4 Years) |

| European Automotive Sun-Readability Norms Boosting Micro-LED HUD Integration | +3.9% | Europe and Spillover Markets | Long Term (≥ 4 Years) |

| Quantum-Dot Color-Conversion Efficiency Breakthroughs Reducing Manufacturing Steps | +5.4% | Global | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Apple and Samsung Roadmaps For Micro-LED Wearables Accelerating Small-Display Demand

Samsung’s CES 2025 concept smartwatch features a peak luminance of roughly 4,000 nits, quadrupling the luminance of today’s OLED wearables and confirming outdoor readability targets. Apple’s canceled watch project shifts micro-LED R&D toward near-eye AR glasses at its Santa Clara campus. Meta has locked in Plessey’s full GaN-on-Si capacity for late-2025 smart glasses, while JBD mass-produces monochrome and RGB panels for tier-one headset OEMs. Collectively, these roadmaps pivot demand from wrist-worn to sub-1-inch microdisplays requiring 3,000 PPI, a density OLED struggles to achieve at viable yield. Their trajectories signal that the micro LED market will diversify across multiple wearable form factors over the next four years.

Transparent and Flexible Retail Signage Uptake In Gulf Cooperation Council Countries and East Asia

Storefront and airport installations in Saudi Arabia, the United Arab Emirates, Tokyo, and Shanghai are deploying modules that deliver 70-85% transparency once pixels are off, maintaining sightlines while broadcasting video content. LG Display and BOE publicized prototypes under 5 mm thick that wrap around curved glass, addressing architectural mandates for glass façades in new smart-city districts. The region’s extreme ambient light-exceeding 100,000 lux-renders transparent OLED solutions unreadable outdoors, giving micro LED an intrinsic performance moat. Regulatory zoning that favors sightline preservation further accelerates uptake, making retail signage an early-scale driver of fine-pitch panels in the micro LED market.

Defense-Grade Micro-Displays Funded By United States and EU Governments

A U.S. Army contract awarded to Kopin in April 2025 defines full-color micro-LED requirements for head-mounted fire-control optics. DARPA’s LUMOS program finances heterogeneous integration of compound-semiconductor emitters with silicon photonics for compact optical systems. These initiatives seek 10,000+ nit daytime readability, −40 °C to +85 °C operation, and elimination of scan-line artifacts, benchmarks that OLED cannot reach. The resulting specifications flow down to commercial AR devices, anchoring a defense-to-consumer technology transfer that enlarges total addressable demand in the micro LED market.

Taiwanese Mini-LED Cost Decline Enabling Pilot Micro-LED Lines

Shared tooling from mature mini-LED fabs cuts incremental capex for micro-LED pilot lines. PlayNitride’s USD 19 million Kunshan site expands epitaxial capacity within mainland China and forecasts a consumer television cost inflection point by 2027. Ennostar divested Kfes Lighting to redeploy USD 30 million into a six-inch epi-wafer expansion, indicating a strategic exit from the commodity lighting market. AU Optronics plans the world’s largest dedicated micro-LED line for mass production in 2025, leveraging its thin-film-transistor expertise to integrate active-matrix backplanes. Collectively, Taiwanese moves reduce per-panel cost curves and unlock broader deployment of micro-scale dies, lifting the global micro LED market growth trajectory.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mass-Transfer Yield Below 60% for Sub-10 µm LEDs Beyond 4-Inch Wafers | −5.7% | Global, Acute in North America and Europe | Short Term (≤ 2 Years) |

| Non-Standardized Automotive Qualification Protocols | −2.9% | Global, Fragmentation in Asia Pacific and South America | Medium Term (2–4 Years) |

| GaN-on-Si Wafer Supply Concentration in Asia | −2.1% | Global Risk Centered in Taiwan, China, and Japan | Long Term (≥ 4 Years) |

| More Than USD 600 Million Capex Limiting Expansion in South America and Africa | −3.4% | South America and Africa | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Mass-Transfer Yield Below 60 % For Sub-10 µm LEDs Beyond 4-Inch Wafers

Nature’s September 2025 review confirms sidewall recombination and Auger effects erode yields once pixel pitch falls below 10 µm. Sub-5 µm LEDs demanded by AR microdisplays face catastrophic die loss during pick-and-place or laser lift-off transfer, limiting their commercial viability. PlayNitride’s March 2025 chip-on-carrier study improved yields but still documented industrial-scale gaps. High-PPI microdisplays in North America and Europe, therefore, remain expensive, slowing consumer adoption and subtracting momentum from the micro LED market until hybrid bonding or other wafer-level processes mature.

Non-Standardized Automotive Qualification Protocols

UNECE Regulations 112, 123, and 148 govern photometric limits but omit accelerated aging profiles or vibration thresholds tailored to micro-LED bonding interfaces.[1]European Union, “Regulation No 123 Uniform Provisions Concerning Adaptive Front-Lighting Systems,” eur-lex.europa.eu Each OEM imposes proprietary sequences, which inflate validation costs and stretch the time-to-market to 24 months or more. Asia Pacific and South America show the widest divergence, forcing suppliers into repetitive test loops that dilute engineering bandwidth. The resulting delay tempers penetration of micro-LED head-up displays and instrument clusters in an otherwise lucrative automotive channel.

Segment Analysis

By Application: Near-To-Eye Devices Drive Miniaturization

Near-to-eye devices expanded at a 32.61% CAGR through 2031, outpacing all other uses as Apple, Meta, and defense integrators align roadmaps to sub-1-inch microdisplays with 3,000 PPI densities. The micro LED market size for near-to-eye devices is projected to compound as AR headsets transition from monochrome prototypes to full-color, sunlight-readable optics. Smartwatch displays, which commanded 28.43% of 2025 revenue, remain the largest shipped volume, yet will concede growth ranking to AR eyewear. Television adoption lags due to die-count economics; a 100-inch panel still requires about 25 million dies. Monitors and laptops carve a middle path, tapping micro LED for medical imaging and HDR content grading where OLED burn-in risks are unacceptable.

The application bifurcation gives rise to two parallel supply chains. Wearable vendors favor hybrid bonding for sub-10 µm alignment accuracy, whereas large-format signage continues to use elastomer-stamp mass transfer at a 50 µm pitch. Medical theaters form a third niche, purchasing USD 10,000-plus diagnostic displays that justify micro-LED premiums and leverage zero-motion-blur characteristics for robotic surgery. This segmentation diversity cushions revenue volatility and sustains multi-node innovation across the micro LED market.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare Outpaces Consumer Electronics Growth

Consumer electronics accounted for 40.12% of 2025 revenue, driven by premium televisions, gaming monitors, and smartwatches. Yet, healthcare will post the fastest 33.37% CAGR, propelled by surgical suites that demand 10,000-nit luminance with minimal heat rise over multi-hour procedures. Diagnostic radiology workstations also benefit from micro-LED’s 1,000,000:1 contrast ratio, which enhances grayscale discernment in bright rooms. Automotive OEMs, driven by UNECE sun-readability thresholds, accelerate the integration of head-up displays once qualification hurdles are cleared, while the aerospace and defense supply streams grow on U.S. and EU contracts for ruggedized micro-displays.[2]United Nations Economic Commission for Europe, “Regulation No 148 – Light-Signalling Devices,” unece.org

Consumer electronics growth moderates as OLED retains smartphone dominance and mini-LED undercuts cost in mid-size monitors. Conversely, healthcare budgets can absorb USD 10,000 unit pricing due to multi-year depreciation schedules, yielding margins that offset the micro-LED yield penalty. Automotive programs offer similar resilience-the segment commands USD 500-1,000 per vehicle once validated, ensuring durable revenue once qualification protocols converge. Defense projects tolerate even higher pricing, creating a layered opportunity ladder within the micro LED market.

By Panel Size: Sub-10-Inch Units Dominate Wearable Demand

Sub-10-inch panels captured 46.78% of 2025 revenue and are expected to maintain a 32.83% CAGR, as smartwatches, AR glasses, and head-up displays prioritize compactness and battery life. The micro LED market size for sub-10-inch products will therefore expand the fastest, driven by pixel densities that are impossible for legacy technologies. Medium panels (10-50 inches) appeal to high-brightness monitors and laptop workstations, yet must compete with mature mini-LED backlights. Panels beyond 50 inches remain luxury items priced above USD 100,000, confining adoption to flagship commercial signage.

Micro-scale emissive architecture, especially when it comes to devices, favors those where every gram and milliamp counts. JBD’s sub-5 µm pixel pitch achieves 3,000 PPI, enabling uninterrupted AR overlays in daylight. Large-format units, by contrast, still face prohibitive die-counts and sub-60% yields, delaying mainstream television adoption until 2028-2030. The resulting size stratification reinforces dual tooling strategies across the micro LED market.

By Pixel Pitch: Fine-Pitch Captures Over Half Of Revenue

Fine-pitch modules with pitches below 1.5 mm accounted for 51.36% of 2025 revenue and are growing at a 33.46% CAGR. Digital signage in GCC retail districts adopts a sub-1 mm pitch to meet new municipal resolution rules, while automotive HUDs require a sub-0.5 mm pitch for crisp windshield projections. Standard pitch (1.5-2.5 mm) serves outdoor billboards viewed beyond three meters, and large pitch above 2.5 mm is losing ground to higher-resolution alternatives.

Demand for immersive signage and head-up displays will keep fine-pitch micro LED as the revenue anchor of the micro LED market. Standard pitch persists where cost trumps resolution, yet even stadium displays increasingly specify 4K or higher, nudging buyers toward finer grids. Large pitch shrinks as cities legislate minimum pixel density, further tilting the share toward fine-pitch assemblies.

Note: Segment shares of all individual segments available upon report purchase

By Technology: RGB Full-Color Leads On Quantum-Dot Breakthroughs

RGB full-color architectures accounted for 78.67% of 2025 shipments and achieved a 35.79% CAGR, driven by cadmium-free quantum dots that reached a 38% photon-conversion efficiency.[3]Li et al., “Color-Conversion Displays: Current Status and Future Outlook,” nature.com Using blue micro-LED arrays and patterned quantum dots circumvents the low efficiency of native red LEDs, reducing epitaxial steps and stabilizing color uniformity. Monochrome displays maintain a niche in defense and industrial optics where green-only emission is sufficient, and power budgets are tight.

Structural advantages drive the adoption of full-color technology across premium televisions, AR glasses, and automotive clusters, cementing its lead within the micro LED market. Research into ligand engineering and dielectric screening aims to suppress Auger recombination at excitation densities of 1–10 W cm⁻², typical of near-eye applications, ensuring that quantum-dot conversion retains headroom for brightness scaling.

By Component: Driver ICs Gain Share As Adaptive Brightness Becomes Mandatory

Epitaxial wafers supplied 34.28% of 2025 revenue, yet driver ICs now post the fastest 34.23% CAGR. Active-matrix micro-LED panels require per-pixel dimming, temperature compensation, and real-time current sensing to satisfy UNECE Regulation 123 failure-signal mandates. Adaptive brightness algorithms also lower power draw in battery-constrained AR glasses, shifting the bill of materials weight toward driver silicon.

The micro LED market share for driver IC vendors rises as panel makers integrate thin-film transistors, high-speed serializers, and fault-monitor circuitry onto glass or silicon backplanes. Inspection and repair tooling, although smaller in revenue, remains essential for yields exceeding 60% and will continue to receive investment from display fabs pursuing defect-free bonding.

By Manufacturing Process: Hybrid Bonding Gains Ground On Throughput Advantages

Hybrid bonding posts a 32.19% CAGR as wafer-to-wafer alignment achieves sub-5 µm accuracy and halves thermal resistance relative to epoxy adhesives. A Nature paper from March 2025, co-authored by PlayNitride, logged 99.5% yields on six-inch wafers via chip-on-carrier hybridization. Mass transfer still controlled 67.81% of 2025 revenue, thanks to the installed elastomer-stamp capacity for signage and televisions. Epitaxial wafer bonding stays niche, constrained by supply-chain lock-in.

Hybrid bonding’s thermal advantages prove indispensable for microdisplays operating above 1 W cm⁻², where even minute temperature rises induce color shift. Mass transfer remains viable for 50 µm-pitch modules where throughput per hour is paramount. This dual-track processing landscape characterizes the manufacturing nucleus of the micro LED market.

Note: Segment shares of all individual segments available upon report purchase

By Offering: Display Modules Dominate As Lighting Lags

Display modules accounted for 71.24% of 2025 revenue and are expected to grow at a 32.04% CAGR. Their dominance reflects the micro-LED’s local-dimming and infinite-contrast traits, which directly translate into premium price points for televisions, smartwatches, and head-up displays. Lighting modules trail because mini-LEDs and conventional LEDs generally deliver superior lumens per dollar in general illumination.

Regulatory photometric ceilings in automotive lighting (UNECE Regulation 148) do not demand pixel-level control, diluting the micro-LED value proposition. Market adoption will therefore concentrate on high-impact display formats until chip costs drop below USD 0.05 per lumen, a milestone forecast for 2028-2030. In the interim, display companies capture the bulk of economic rent within the micro LED market.

Geography Analysis

Asia Pacific generated 66.42% of 2025 revenue and remains the manufacturing backbone for epitaxial wafers, TFT backplanes, and mass-transfer tooling. China’s BOE and Tianma leverage government incentives to scale gaming monitors and automotive clusters, while Taiwan’s PlayNitride and Epistar extend six-inch epi-wafer lines. South Korea’s Samsung and LG Display concentrate on modular televisions and transparent glass prototypes showcased at CES 2025. The region’s vertically integrated supply chain ensures faster iteration cycles and cost degression, reinforcing its economic gravity inside the micro LED market.

The Middle East is projected to chart the fastest 32.21% CAGR, as Saudi Arabia’s NEOM project and Dubai’s retail corridors install transparent micro-LED façades readable under 100,000 lux of desert daylight. Sovereign wealth funding offsets capex hurdles and accelerates full-scale pilot deployments. Regulatory codes favor glass-first architecture, creating a predictable pull for transparency-enabled signage that OLED cannot satisfy.

North America’s growth centers on defense and AR wearables. U.S. Army and DARPA contracts finance performance matrices that serve as de facto standards for commercial glasses. Apple’s Santa Clara lab continues developing sub-1-inch microdisplays after ending its watch program, anchoring domestic R&D spending and seeding a specialized micro-LED competency cluster. Europe advances through automotive OEM demand for sun-readable HUDs, leveraging UNECE conformity as a conversion catalyst. South America and Africa trail due to USD 600 million fab cost thresholds and absent local epi-wafer sources, confining them to imported modules and tempering their contribution to the global micro LED market.

Competitive Landscape

The micro LED market exhibits moderate fragmentation. Samsung, Sony, LG Display, BOE, and AU Optronics collectively control a roughly 45–50% share, relying on vertical integration across epitaxial growth, TFT backplanes, and final assembly. Samsung’s “The Wall Luxury” and LG’s transparent prototypes illustrate incumbent strategies to dominate large-format and specialty niches. BOE and AU Optronics similarly leverage scale to bid for gaming monitor and automotive dash contracts.

Specialist challengers fill performance gaps. VueReal’s solid-print transfer technique claims 99.99% yield for sub-5 µm dies, positioning the firm to supply AR microdisplays. Plessey’s exclusive supply deal with Meta locks the social-media giant into GaN-on-Si roadmaps through 2027. Aledia’s nanowire architecture aims to achieve higher red LED efficiency on eight-inch wafers, potentially disrupting conventional planar designs.

Failure stories temper exuberance. Rohinni’s 2024 closure, despite USD 50 million in funding, underscores capital intensity and yield risks. The lesson sharpens investor due diligence, favoring players with proven mass-transfer or hybrid bonding proficiency. Looking forward, automotive qualification consolidation and hybrid bonding maturation will likely sort contenders from pretenders, gradually concentrating revenue share among the best-capitalized and technologically diversified firms.

Micro LED Industry Leaders

Samsung Electronics Co. Ltd.

Sony Corporation

LG Display Co. Ltd.

BOE Technology Group Co. Ltd.

AU Optronics Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Applied Materials introduced a production-ready hybrid-bonding tool targeting six-inch GaN wafers, slated for customer qualification in Q1 2026.

- July 2025: PlayNitride invested USD 19 million to open a Kunshan micro-LED facility, expanding epi-wafer supply for mainland Chinese panel makers.

- July 2025: Ennostar divested Kfes Lighting, redeploying USD 30 million into six-inch epi-wafer lines dedicated to micro-LED display applications.

- April 2025: Kopin won a U.S. Army contract to define performance matrices for soldier-worn micro-LED head-up displays.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the micro-LED market as revenue generated from selling fully fabricated micro light-emitting diode chips, display modules, and lighting engines in which each diode's active area is typically below 100 µm and driven individually through active or passive matrices. The assessment spans consumer electronics, automotive, industrial, healthcare, aerospace, retail signage, and other end-use channels and tracks value in US dollars from 2019 through 2030.

Scope Exclusion: mini-LED back-lit LCD panels, conventional LED signage above 300 µm chip size, and any prototype volumes not entering commercial billing are omitted.

Segmentation Overview

- By Application

- Smartwatch

- Near-to-Eye Devices (AR/VR)

- Television

- Smartphone and Tablet

- Monitor and Laptop

- Head-up Display

- Digital Signage

- Micro-Projector

- Medical and Surgical Displays

- Industrial Inspection Panels

- By End Use Industry

- Consumer Electronics

- Automotive

- Aerospace and Defense

- Healthcare

- Advertising and Retail

- Industrial and Manufacturing

- Others End Use Industries

- By Panel Size

- Less than 10-inch (Small and Micro-Displays)

- 10- to 50-inch (Medium)

- Above 50-inch (Large)

- By Pixel Pitch

- Fine Pitch (Less than 1.5 mm)

- Standard (1.5 – 2.5 mm)

- Large (Above 2.5 mm)

- By Technology (Color)

- RGB Full-Color

- Monochrome

- By Component

- Epitaxial Wafers

- Backplanes

- Driver ICs

- Transfer and Bonding Equipment

- Inspection and Repair Tools

- By Manufacturing Process

- Mass Transfer

- Epitaxial Wafer Bonding

- Hybrid Bonding

- By Offering

- Display Modules

- Lighting Modules

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview wafer equipment engineers in Taiwan and South Korea, procurement leads at wearables and EV OEMs across North America, Europe, and China, and display architects from specialty integrators. These discussions validate cost learning rates, realistic yield ramps, and channel mark-ups, filling information gaps that static documents cannot cover.

Desk Research

We start with structured desk work that gathers trade codes for epitaxial wafers from UN Comtrade, shipment disclosures from display makers filed with the U.S. SEC, and production indices from sources such as the International Display Manufacturing Association, OECD STAN, and Korea's KITA export dashboard. Power-efficiency benchmarks, patent family counts, and design-win announcements are mined through Questel, Dow Jones Factiva, and D&B Hoovers to detect inflection points in yield and cost curves.

Macro calibrators, consumer device sell-in data from IDC releases, automotive cockpit penetration ratios published by ACEA, and national energy-saving incentive rolls anchor addressable demand before we layer technology-specific adoption factors. The desk list shown is illustrative; numerous other open and subscription sources support data collection, validation, and clarification.

Market-Sizing & Forecasting

Our top-down model reconstructs spend by mapping micro-LED die output, average transfer yield, and blended selling price across nine core applications, which are then cross-checked with bottom-up rollups from sampled supplier revenues and channel checks. Key variables include premium smartwatch shipments, AR/VR headset launches, wafer starts per month, transfer equipment throughput, regulatory brightness caps, and historical ASP erosion. A multivariate regression ties these drivers to observed market value; scenario analysis adjusts for breakthrough mass-transfer yields or deferred consumer upgrades.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst audits, and senior sign-off. We re-run the model annually and reopen it mid-cycle if a material event, such as a major fab capacity addition, triggers our re-contact protocol, ensuring clients always receive the freshest view.

Why Mordor's Micro LED Baseline Earns Confidence

Buyers often see diverging numbers because firms choose different technology cut-offs, adoption curves, and currency treatments. We spell out scope, apply only invoiced shipments, and refresh the model every twelve months, which limits drift.

Key gap drivers versus other publishers include their inclusion of mini-LED backlights, reliance on management targets rather than audited sales, and the use of OLED price proxies that inflate revenue.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.42 bn (2025) | Mordor Intelligence | - |

| USD 0.82 bn (2024) | Global Consultancy A | Bundles mini-LED LCD backlights and counts announced, not shipped, volumes |

| USD 1.05 bn (2024) | Trade Journal B | Converts retail tag to market value and retains modules above 300 µm chip size |

| USD 0.80 bn (2024) | Industry Association C | Uses prototype output and limited regional coverage |

Taken together, the comparison shows that our disciplined scoping, variable selection, and refresh cadence deliver a balanced, transparent baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

How fast is the micro LED market expected to grow to 2031?

The market is forecast to increase from USD 0.56 billion in 2026 to USD 2.17 billion by 2031, registering a 31.12% CAGR.

Which application segment shows the highest growth potential?

Near-to-eye devices for AR and VR lead with a 32.61% CAGR as headsets demand ultra-bright, high-PPI microdisplays.

Why are driver ICs gaining a larger revenue share?

Integrated driver ICs are essential for per-pixel dimming, adaptive brightness and UNECE fault-signal compliance, driving a 34.23% CAGR.

Which region dominates manufacturing and revenue?

Asia Pacific holds more than 66% of 2025 revenue, backed by vertically integrated supply chains in Taiwan, China, South Korea and Japan.

What is the main technical barrier to mass adoption?

Sub-10 µm mass-transfer yields remain below 60%, raising costs for high-density panels and delaying widespread AR headset rollout.

How does micro-LED compare with OLED in outdoor visibility?

Micro-LED achieves 4,000–10,000 nits peak brightness versus typical OLED peaks under 1,500 nits, ensuring superior readability in direct sunlight.