Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

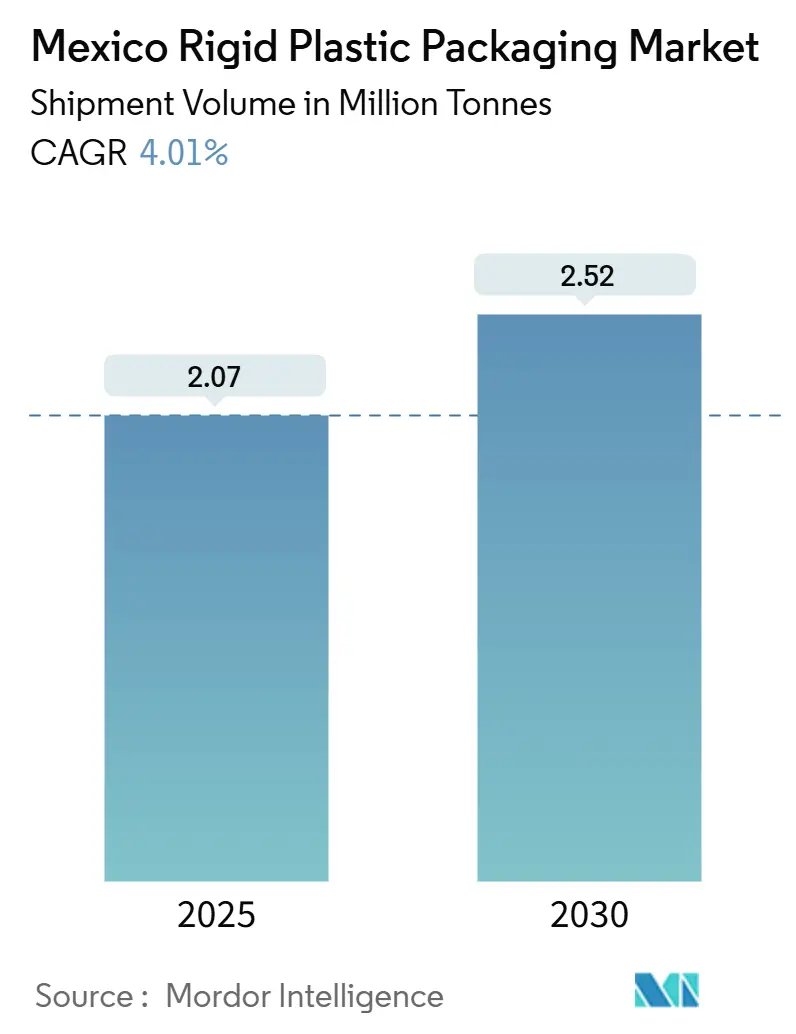

| Market Volume (2025) | 2.07 Million tonnes |

| Market Volume (2030) | 2.52 Million tonnes |

| Growth Rate (2025 - 2030) | 4.01% CAGR |

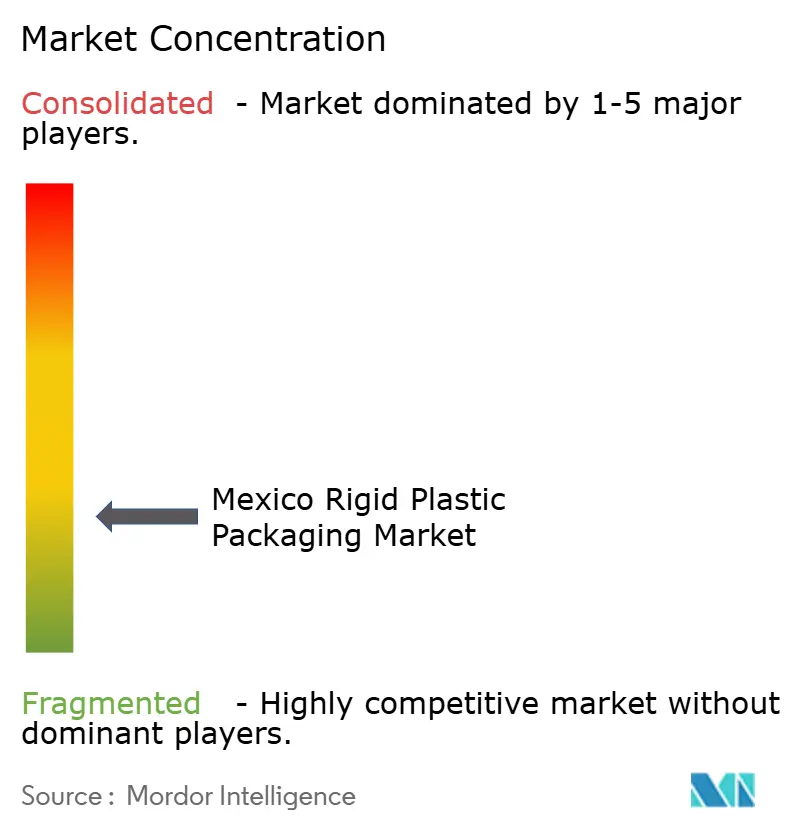

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Rigid Plastic Packaging Market Analysis by Mordor Intelligence

The Mexico rigid plastic packaging market size stood at 2.07 million tonnes in 2025 and is projected to reach 2.52 million tonnes by 2030, advancing at a 4.01% CAGR throughout the forecast period. Accelerated bottled-water consumption, strong nearshoring inflows, and resilient food exports underpin steady volume expansion, while substitution away from glass and metal containers further enlarges addressable demand. Lower resin costs relative to competing materials and the country’s developed recycling infrastructure support competitive production economics, whereas localized manufacturing clusters minimize logistics outlays. Regulatory momentum around circular-economy goals motivates brand owners to specify higher recycled-content packs, thereby stimulating investment in advanced sorting, washing, and extrusion assets. Nevertheless, state-level single-use levies and rPET feedstock tightness temper growth potential, keeping the price–volume equation finely balanced.

Key Report Takeaways

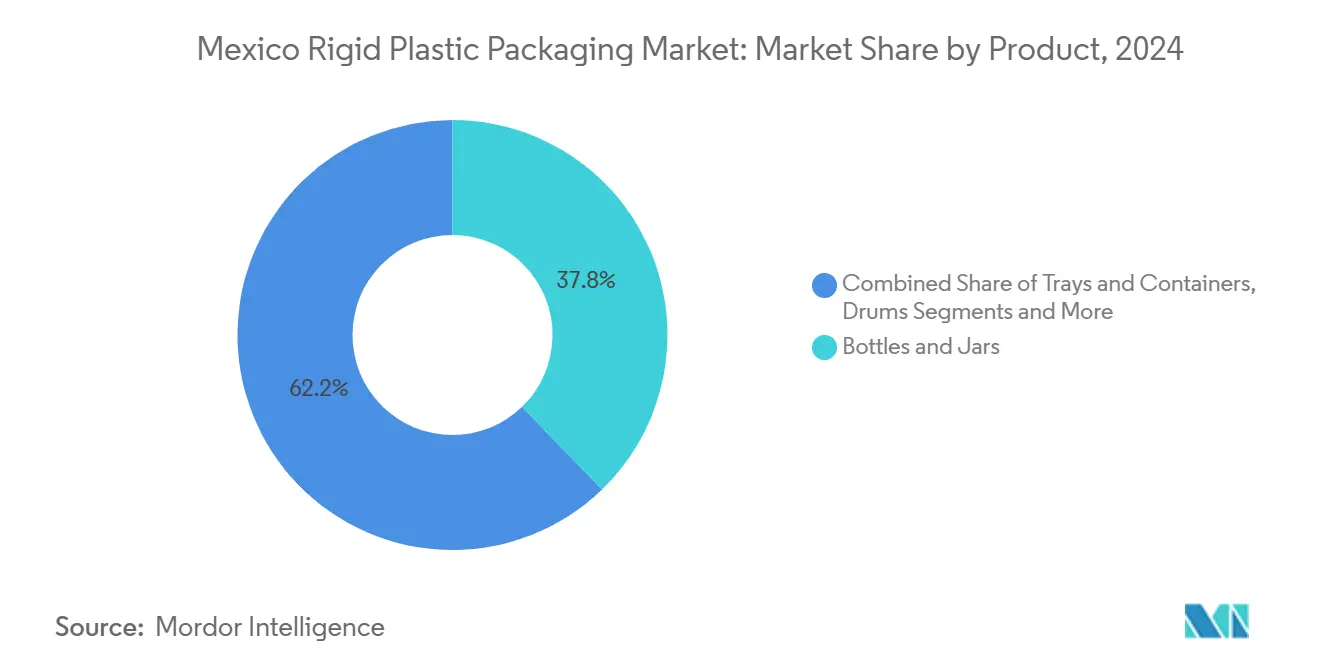

- By product, bottles and jars captured 37.76% of the Mexico rigid plastic packaging market share in 2024.

- By material, the Mexico rigid plastic packaging market size for polyethylene is projected to grow at a 5.16% CAGR between 2025 to 2030.

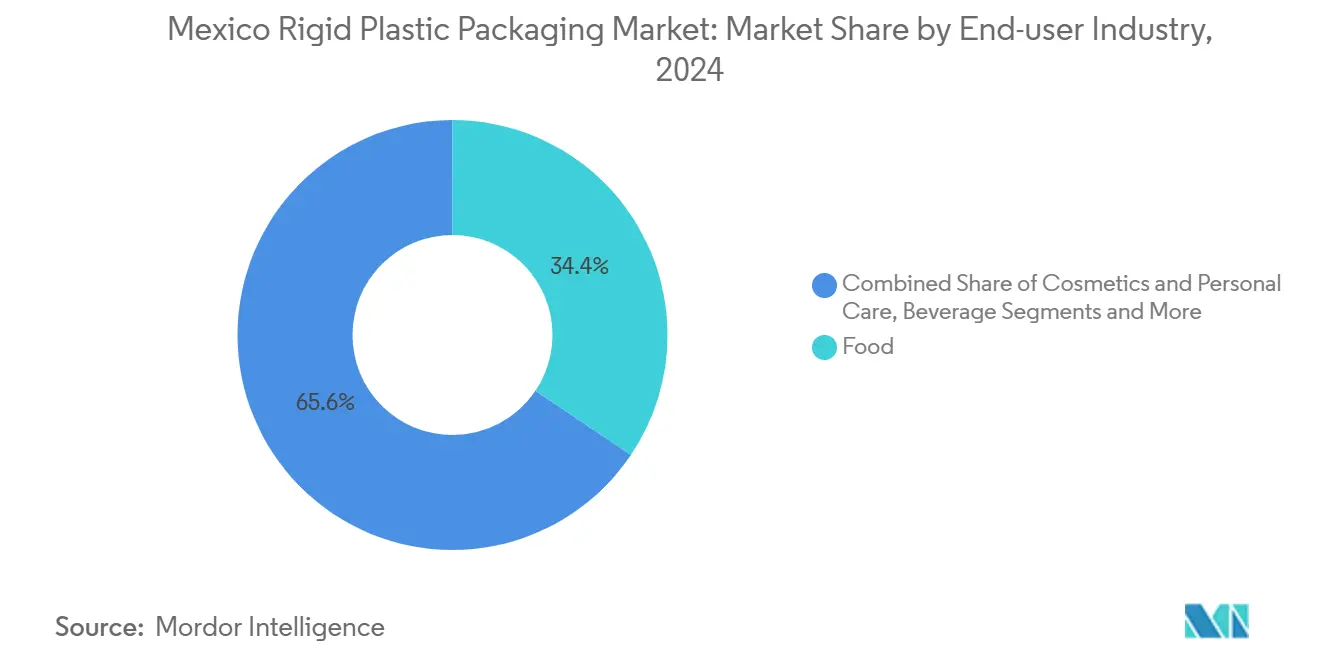

- By end-user industry, food captured 34.42% of the Mexico rigid plastic packaging market share in 2024.

Mexico Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bottled-water and carbonated-soft-drink uptake | +1.2% | Nationwide urban centers | Short term (≤ 2 years) |

| Manufacturing nearshoring rebound | +0.9% | Northern border and Bajío | Medium term (2–4 years) |

| Food-export packaging requirements | +0.7% | Pacific agricultural states | Medium term (2–4 years) |

| Glass/metal-to-plastic substitution | +0.5% | Countrywide | Long term (≥ 4 years) |

| Pre-emptive tethered-cap adoption | +0.3% | National, anticipating regulatory alignment | Short term (≤ 2 years) |

| E-grocery boom requiring sturdy packs | +0.4% | Metropolitan areas, expanding to secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Bottled-Water and CSD Consumption

Mexico retains the world’s highest per-capita bottled-water intake at 234 liters and maintains strong carbonated-soft-drink preferences, a pairing that produces reliable PET bottle volumes even during macro-economic softness. Federal health-risk standards enforced by COFEPRIS favor converters with certified hygienic operations, creating barriers to informal entrants. A 56% PET recycling rate achieved by PetStar demonstrates the closed-loop potential that increasingly influences brand procurement decisions. Bottled water’s role as a substitute for municipal supply makes demand comparatively inelastic, safeguarding baseline throughput for resin producers and molders.

Manufacturing Nearshoring Rebound

United States–Mexico-Canada Agreement (USMCA) certainty, coupled with supply-chain realignment out of Asia, delivered 10.63 million ft² of new industrial-space absorption around Monterrey in 2024, clustering electronics, appliance, and automotive plants that consume trays, component totes, and IBCs. Nuevo León alone hosts 79 industrial parks, enabling converters to run high-utilization lines while servicing diverse customers within a two-hour drive radius. Chinese tier-1 auto suppliers’ USD 7.06 billion cumulative investments since 2019 continue to spawn demand for protective battery housings and under-hood part packaging that must meet stringent OEM specifications.

Food-Export Packaging Demand

Mexico’s status as a major produce exporter to North America requires rigid containers that safeguard avocado and berry shipments through multi-modal transit and varied climates. ISO 22000 and FSSC 22000 certifications have become selection criteria among export-oriented packers, favoring suppliers with robust quality-assurance systems. The General Law of Adequate and Sustainable Food, effective April 2024, enforces prominent nutrition panels, driving adoption of high-clarity resins and superior printing surfaces.

Glass/Metal-to-Plastic Substitution

Lightweight plastic designs lower freight emissions and costs versus glass, a crucial factor given elevated diesel prices. Blow-mold advancements now realize thin-wall bottles retaining top-load strength, allowing beverage and sauce brands to migrate away from heavier formats. Plastic’s compatibility with recycled content supports corporate sustainability pledges, while integrated supply chains such as ALPLA’s 32 Mexican plants yield speed-to-market advantages.[1]ALPLA, “Company Fact Sheet,” alpla.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and disposal concerns | -0.8% | Urban municipalities | Medium term (2–4 years) |

| State-level single-use-plastic taxes | -0.6% | State-specific implementation, varying enforcement | Short term (≤ 2 years) |

| rPET feedstock supply volatility | -0.4% | National, affecting recycling-dependent operations | Short term (≤ 2 years) |

| Resin-plant water-scarcity curbs | -0.3% | Northern states, industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental and Disposal Concerns

Municipal waste is projected to escalate from 44 million tonnes in 2025 to 65 million tonnes by 2030, amplifying public scrutiny of single-use plastics. State-level bans and fees add compliance costs and necessitate portfolio tweaks, with 69% of surveyed stakeholders doubting industry readiness for circular-economy execution. Extended-Producer-Responsibility frameworks under discussion could force converters to internalize collection and recycling expenses, nudging some buyers toward refill systems or alternate substrates.

rPET Feedstock Supply Volatility

Recycled PET availability tightens whenever informal collection networks are disrupted by commodity-price swings, prompting price spikes that erode converter margins. Although PLANETA’s 50,000 tonne annual facility and IMER’s capacity expansions boost domestic output, demand continues to outstrip supply during peak beverage seasonality. Converters, therefore, maintain parallel virgin-resin sourcing, exposing them to foreign-exchange fluctuations and import duties.

Segment Analysis

By Product: Bottles and Jars Sustain Dual Leadership

Bottles and jars controlled 37.76% of the Mexico rigid plastic packaging market in 2024 and are forecast to grow at 5.28% through 2030, a rare concurrence of scale and momentum that underpins the overall Mexico rigid plastic packaging market size expansion. High beverage throughput, growing condiment exports, and personal-care premiumization all reinforce demand for PET and PE containers.

Trays and lidded containers capture e-grocery and ready-meal uptake, aided by rising electric-vehicle last-mile fleets that expand chilled-chain coverage. UN-rated drums and IBCs serve chemicals and agro-inputs moving across the US border, while molded pallets gain favor inside automated warehouses. Lightweighting programs implemented by multinational soft-drink bottlers cut resin per unit but increase total units shipped, sustaining feedstock volumes for blow molders.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: PE Dominance, PET Outpaces

Polyethylene retained 33.72% of Mexico's rigid plastic packaging market share in 2024, buoyed by its versatility across closures, bottles, and industrial pails. However, PET leads growth at a 5.16% CAGR, underpinned by robust bottle-to-bottle recycling infrastructure and brand recycled-content targets, reinforcing the Mexico rigid plastic packaging market size trajectory.

Polypropylene benefits from automotive interior-component streams requiring scratch-resistant binning, whereas PVC confines itself to niche construction fittings that demand rigidity and chemical resistance. Polystyrene endures regulatory pressure but survives in protective appliance packaging where cushioning performance and mold-cost economics still prevail. Engineering resins such as ABS and PC capture value in medical-device trays and electronics caddies produced within clustered maquiladora facilities.

By End-user Industry: Food Maintains Scale, Industrial Accelerates

Food processors absorbed 34.42% of the Mexico rigid plastic packaging market size in 2024, relying on multilayer tubs, spice jars, and beverage bottles that meet COFEPRIS food-contact criteria. Label legislation from 2024 encourages high-resolution graphics and tamper-evident closures, driving incremental value addition.

Industrial demand rises at a 4.78% CAGR, reflecting battery, semiconductor, and appliance factories seeking returnable totes, component reels, and chemical containers. Pharmaceutical and medical-device assemblers select class-7-compliant blister trays and vials, while cosmetics brands deploy PET jars and PP closures with premium aesthetics to serve a growing middle-income consumer base.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Northern border states dominate the Mexico rigid plastic packaging market thanks to proximity to U.S. customers and USD-denominated cross-border flows. Nuevo León’s USD 66.458 billion export tally and dense park network concentrate converters near resin suppliers and high-volume end-users.[2]Secretaría de Economía, “Industry and Regional Profiles,” datamexico.org

The Bajío corridor, responsible for 50% of national vehicle output, generates demand for grease-resistant component trays, heavy-duty drums, and dunnage. Guanajuato’s MXN 32.540 million soap-and-toiletry output feeds PET and PP bottle lines, while cafés and beverage fillers around Querétaro spur cap-and-closure orders.

Central Mexico, anchored by the Mexico City metropolitan area, serves 30 million consumers and a vast food-service sector that absorbs sauce bottles, dairy tubs, and takeaway clamshells. Pacific coastal states specialize in produce export packs, vented harvest crates, and high-clarity berry punnets aligned with port logistics to the U.S. West Coast and Asia. Water-scarce northern municipalities encourage the adoption of closed-loop process-water systems among resin producers, marginally elevating capital intensity for new pelletizing lines.

Competitive Landscape

The Mexico rigid plastic packaging market features moderate fragmentation: the top five suppliers account for roughly 45% of installed capacity, leaving scope for regional specialists. Multinationals such as ALPLA, Amcor, and Aptar leverage integrated design-to-recycling models, while domestic groups like Plastiex and Envases Universales excel in customized short-run work for local brands.

Recent capital allocations emphasize recycled-content capability: ALPLA’s PET wash line expansions and Coca-Cola FEMSA’s USD investment in PLANETA signal commitment to closed loops. Acquisition activity persists. ALPLA lifted its stake in the Taba joint venture in February 2025 to secure blow-molding volume in central Mexico.[3]ALPLA, “ALPLA Strengthens Mexican Presence,” alpla.com

Innovation differentiators include tethered caps that anticipate potential nationwide mandates, barrier coatings for hot-fill sauces, and RFID-embedded pallets enabling asset tracking in automated warehouses. Automation rollouts, particularly in high-cavitation closure cells, push productivity gains that smaller rivals struggle to replicate.

Mexico Rigid Plastic Packaging Industry Leaders

-

Amcor plc

-

ALPLA México SA de CV

-

Greif Inc.

-

Sonoco México

-

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Sonoco committed USD 30 million to boost adhesives and sealants tube output by 100 million units annually across three Mexican plants.

- February 2025: ALPLA acquired additional shares in its Taba joint venture to enlarge food-grade bottle capacity.

- January 2025: SEMARNAT activated the Environmental Electronic Platform (VEA), obliging manufacturers to submit permits digitally and monitor official inboxes twice weekly.

- December 2024: Toppan finalized the USD 1.8 billion purchase of Sonoco’s thermoformed-packaging assets, strengthening barrier-tray offerings for Mexican protein processors.

Mexico Rigid Plastic Packaging Market Report Scope

The study tracks the demand for rigid plastic packaging materials across various end-user industries, such as food, foodservice, beverages, healthcare, personal care, cosmetics, industrial, building and construction, and automotive. Rigid plastics can be of different grades and different material combinations based on the type of product being packed, like polyethylene, polypropylene, polyvinyl chloride, polyethylene terephthalate, and bio-plastics.

The Mexican rigid plastic packaging market is segmented by resin type (polyethylene (PE) (low-density polyethylene (LDPE) & linear low-density polyethylene (LLDPE) and high-density polyethylene (HDPE)), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), and other resin types), product type (bottles and jars, trays and containers, caps and closures, intermediate bulk containers (IBCs), drums, pallets, and other product types), and end-user industry (food (candy & confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products), foodservice, beverages, healthcare, cosmetics and personal care, industrial, building and construction, automotive, and other end-user industries). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

By Product

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Pallets |

| Other Products |

By Material

| Polyethylene (PE) |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP) |

| Polystyrene (PS) and Expanded PS (EPS) |

| Polyvinyl Chloride (PVC) |

| Other Materials |

By End-user Industry

| Food |

| Beverage |

| Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Building and Construction |

| Automotive |

| Other End-user Industries |

| By Product | Bottles and Jars |

| Trays and Containers | |

| Caps and Closures | |

| Intermediate Bulk Containers (IBCs) | |

| Drums | |

| Pallets | |

| Other Products | |

| By Material | Polyethylene (PE) |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP) | |

| Polystyrene (PS) and Expanded PS (EPS) | |

| Polyvinyl Chloride (PVC) | |

| Other Materials | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Building and Construction | |

| Automotive | |

| Other End-user Industries |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Mexico rigid plastic packaging market in 2025?

The market handles 2.07 million tonnes of rigid plastic packs in 2025, with output forecast to reach 2.52 million tonnes by 2030.

Which product type leads demand?

Bottles and jars dominate with 37.76% market share in 2024 and grow the quickest at a 5.28% CAGR.

What material is gaining the most traction?

PET exhibits the fastest 5.16% CAGR, buoyed by strong recycling infrastructure and brand sustainability targets.

How is nearshoring influencing packaging demand?

Industrial relocation to northern and Bajío corridors fuels orders for component trays, drums and IBCs, adding +0.9% to forecast CAGR.

What environmental regulations affect rigid plastic packaging in Mexico?

State-level single-use levies, the 2024 food-labeling law and SEMARNAT’s new digital permitting platform all shape compliance obligations and cost structures.

Page last updated on: