| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 7.49 Billion |

| Market Size (2030) | USD 9.81 Billion |

| CAGR (2025 - 2030) | 5.53 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Mexico Rigid Packaging Market Analysis

The Mexico Rigid Packaging Market size is estimated at USD 7.49 billion in 2025, and is expected to reach USD 9.81 billion by 2030, at a CAGR of 5.53% during the forecast period (2025-2030).

Mexico's rigid packaging industry is experiencing robust growth driven by increasing industrialization and evolving consumer preferences. The country's industrial production demonstrated strong momentum with a 3.1% year-on-year increase in May 2023, while manufacturing output registered an impressive 5.6% growth during the same period. This industrial expansion has created substantial opportunities for industrial packaging solutions across various sectors, particularly in food and beverage packaging where local manufacturing capabilities are being strengthened. The packaging sector has emerged as a cornerstone of Mexico's plastics industry, accounting for 47% of market demand, with a significant portion dedicated to food and beverage applications.

The glass packaging segment is witnessing significant investments and capacity expansions to meet growing demand. In the first quarter of 2022, while glass production increased by 7%, demand surged by 11%, indicating a strong market pull for glass packaging solutions. This trend has prompted major investments in the sector, exemplified by Saverglass's USD 116 million investment in June 2022 to double capacity at its Guadalajara facility, enabling the production of 200 million bottles annually in various colors. Similarly, Grupo Modelo announced a USD 154 million investment to expand its glass production facility in Tierra Blanca, demonstrating the industry's commitment to expanding domestic manufacturing capabilities.

The e-commerce boom has revolutionized packaging requirements in Mexico, with the sector reaching a value of 401 billion pesos (USD 19.54 billion) in 2022. This digital transformation has significantly influenced rigid packaging designs and specifications, particularly in areas of protective packaging and sustainable solutions. The rapid growth of online retail has created new demands for innovative rigid plastic packaging solutions that can withstand the rigors of e-commerce logistics while maintaining product integrity and environmental consciousness.

The industry is witnessing substantial consolidation through strategic acquisitions and partnerships aimed at expanding manufacturing capabilities and market reach. Notable examples include Pretium Packaging's acquisition of Grupo Edit, enhancing its capability to produce various rigid packaging products including bottles, carafes, and thin-wall containers. This trend of strategic consolidation is reshaping the competitive landscape while bringing advanced technologies and improved production efficiencies to the Mexican market. The focus on local manufacturing capabilities has become increasingly important as companies seek to optimize supply chains and reduce dependence on imports.

Mexico Rigid Packaging Market Trends

Growing Demand from Packaging Food and Industrial Sector

The Mexican food industry has experienced substantial growth, driven by the establishment of the North American Free Trade Agreement (NAFTA) and the evolution of its retail model. According to the National Institute of Statistics and Geography (INEGI), the country hosts 217,245 economic units dedicated to food and beverage manufacturing and processing, including manufacturing plants, offices, and distribution centers. The sector's robustness is further evidenced by the engagement of 9.3 million people in agricultural and fish product transformation, with the food processing industry alone employing more than 800,000 workers. This extensive workforce and infrastructure demonstrate the sector's significant demand for rigid packaging solutions across the value chain.

The Mexican processed food industry maintains strong domestic integration, with approximately 90% of its supplies sourced locally, including essential packaging materials such as plastic, glass, and tinplate. The growing demand for protein-rich food products has emerged as a crucial driver for rigid food packaging solutions, as the country continues to boost domestic meat production. This growth is supported by several key factors, including vertical integration of farms, substantial investments in biosecurity measures, improvements in production chain efficiency, and enhanced operational effectiveness. These developments have created a robust ecosystem for local food production, subsequently driving the demand for various packaging solutions to maintain product quality and safety throughout the supply chain.

Understand The Key Trends Shaping This Market

Download PDF

The Manufacturing and Allied Sectors are Expected to Rebound and Contribute to the Market Demand in Mexico

The manufacturing sector in Mexico demonstrates strong potential for growth, particularly in rigid packaging applications, as evidenced by significant investments in production capacity and recycling infrastructure. A notable example is the strategic partnership between Alpla and Coca-Cola FEMSA, which resulted in a USD 60 million investment in a PET recycling plant in South Mexico, with an annual capacity of 50,000 tons of reusable PET material. This investment not only addresses the growing demand for sustainable packaging solutions but also strengthens the manufacturing capabilities in the region, creating additional opportunities for industrial packaging applications across various industrial sectors.

The industrial sector's commitment to sustainable practices and technological advancement is further demonstrated through various manufacturing initiatives and expansions. The country's strategic geographical location and trade agreements have made it an attractive destination for manufacturing operations, particularly in sectors such as automotive, aerospace, and consumer goods. These industries require specialized rigid plastic packaging solutions for both component protection during manufacturing and final product distribution. The manufacturing sector's growth is supported by improvements in industrial production data, as reported by the National Institute of Statistics and Geography, indicating a positive trajectory for rigid container demand across manufacturing applications.

Segment Analysis: By Packaging Material

Rigid Plastic Segment in Mexico Rigid Packaging Market

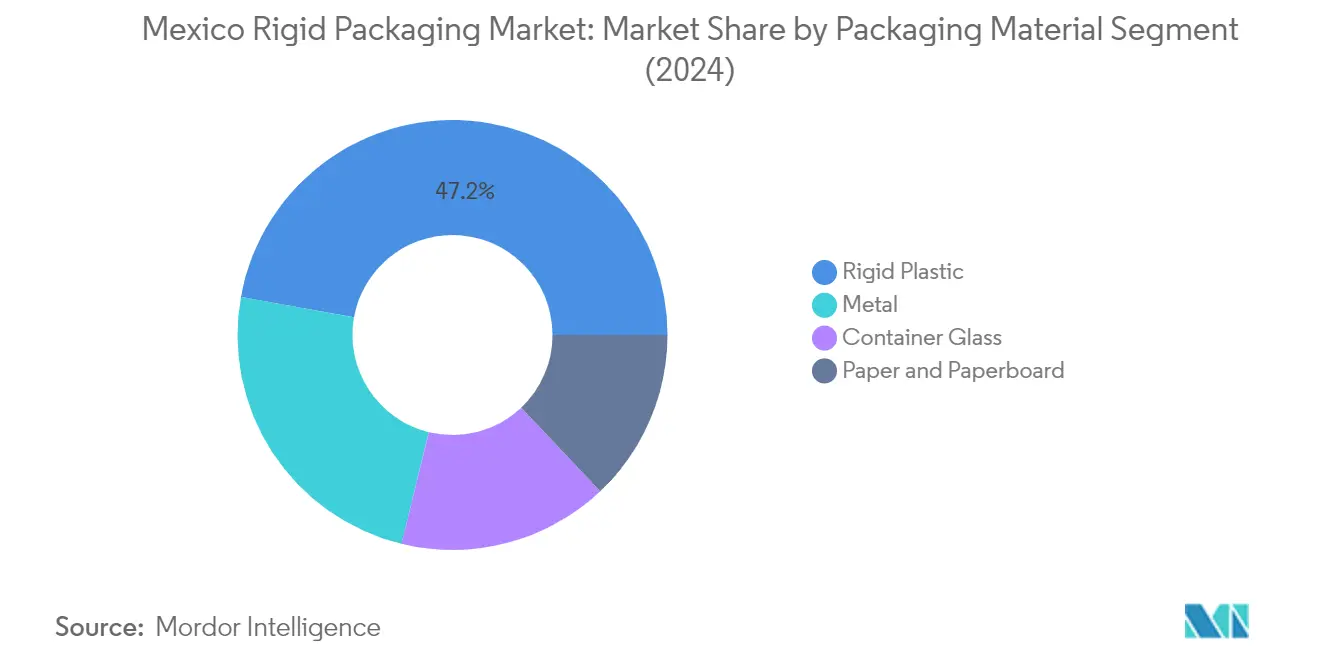

The rigid plastic packaging segment dominates the Mexico rigid packaging market, commanding approximately 47% market share in 2024. This significant market position is driven by the segment's extensive applications across the food, beverage, pharmaceutical, and personal care industries. The segment's growth is supported by the increasing adoption of PET and HDPE polymers, which have expanded plastic bottling applications. The rugged and robust nature of rigid container plastic bottles, particularly their resistance to leaks and bursts, makes them ideal for preserving contents and protecting shipping containers. Mexico's position as one of the most advanced countries in Latin America regarding PET recycling further strengthens this segment's dominance, with manufacturers increasingly focusing on sustainable and eco-friendly packaging solutions.

Paper and Paperboard Segment in Mexico Rigid Packaging Market

The paper and paperboard segment is emerging as the fastest-growing segment in the Mexico rigid packaging market, with a projected growth rate of approximately 8% during 2024-2029. This remarkable growth is driven by increasing consumer awareness about environmental sustainability and the rising demand for eco-friendly packaging solutions. The segment's expansion is further supported by the growing e-commerce sector and the subsequent need for corrugated packaging solutions. The versatility of paper and paperboard packaging, ranging from folding cartons to corrugated boxes, makes it particularly attractive for various end-use industries. Additionally, technological advancements in paper-based packaging manufacturing and the development of innovative, sustainable solutions are contributing to the segment's accelerated growth trajectory.

Remaining Segments in Mexico Rigid Packaging Market

The metal packaging and glass packaging segments continue to play crucial roles in the Mexico rigid packaging market. The metal packaging segment maintains its significance in the food and beverage industry, particularly for canned products and aerosol packaging, benefiting from its superior barrier properties and recyclability. The container glass segment serves premium markets, especially in beverages and pharmaceuticals, leveraging its inherent qualities of preservation and premium appearance. Both segments are experiencing technological advancements in manufacturing processes and increasing focus on sustainability initiatives, including improved recycling programs and lightweight solutions, which contribute to their continued relevance in the market.

Segment Analysis: By End-User Industry

Food Segment in Mexico Rigid Packaging Market

The food segment continues to dominate the Mexico rigid packaging market, holding approximately 34% market share in 2024. This significant market position is driven by the growing demand for processed and packaged foods, changing dietary habits, and increasing urbanization in Mexico. The country's robust food processing industry, with over 217,000 economic units including manufacturing plants and distribution centers, has been a key driver for rigid box and other rigid packaging solutions. The segment's growth is further supported by Mexico's position as a major participant in international agricultural trade, with substantial exports of packaged food products requiring various rigid packaging solutions including corrugated boxes, glass containers, and plastic packaging. The food industry's emphasis on food safety, extended shelf life, and sustainable packaging solutions has also contributed to the segment's dominance in the rigid packaging market.

Beverage Segment in Mexico Rigid Packaging Market

The beverage segment is emerging as the fastest-growing sector in Mexico's rigid packaging market, projected to grow at approximately 7% during 2024-2029. This growth is primarily driven by Mexico's position as one of the world's largest consumers of soft drinks and alcoholic beverages. The segment's expansion is fueled by the increasing popularity of premium beverages, craft beers, and specialty drinks that require high-quality glass packaging solutions. The rising demand for sustainable and recyclable packaging in the beverage industry, particularly for glass and aluminum containers, is also contributing to this growth. Additionally, the segment is benefiting from innovations in rigid packaging designs, including lightweight solutions and enhanced barrier properties, which are essential for maintaining beverage quality and extending shelf life.

Remaining Segments in Mexico Rigid Packaging Market

The other segments in Mexico's rigid packaging market, including healthcare and pharmaceutical, beauty and personal care, industrial, and other end-user industries, each play vital roles in shaping the market landscape. The healthcare and pharmaceutical segment is driven by stringent packaging requirements and the growing pharmaceutical manufacturing sector in Mexico, where blister packaging is often utilized. The beauty and personal care segment is influenced by changing consumer preferences and the increasing demand for premium packaging solutions. The industrial segment continues to grow with the expansion of manufacturing activities and cross-border trade. These segments collectively contribute to the market's diversity and innovation, particularly in areas such as sustainable packaging solutions, smart packaging technologies, and customized packaging designs.

Mexico Rigid Packaging Industry Overview

Top Companies in Mexico Rigid Packaging Market

The rigid packaging market in Mexico is characterized by continuous innovation and strategic expansion by key players like Amcor, Berry Global, Smurfit Kappa, and domestic players like Vitro and BioPappel. Companies are increasingly focusing on sustainable packaging solutions, with significant investments in recycling facilities and eco-friendly material development. The market witnesses active collaboration between global and local players to enhance production capabilities and meet growing demand across various end-user industries. Operational agility is demonstrated through the establishment of new manufacturing facilities, particularly in industrial hubs near the US border, capitalizing on nearshoring opportunities. Strategic moves include vertical integration, particularly in recycling operations, while product innovation centers on developing lightweight, recyclable rigid packaging solutions that maintain structural integrity while reducing material usage.

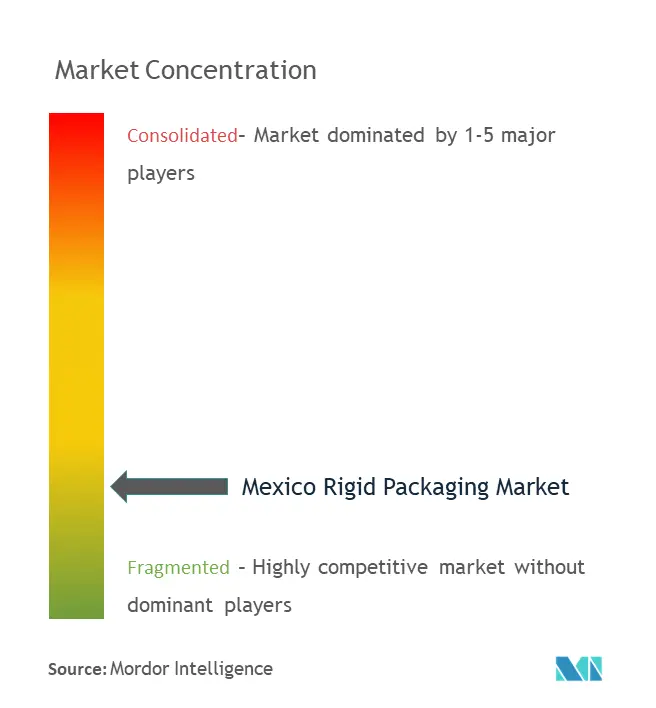

Consolidated Market with Strong Regional Players

The Mexican rigid packaging landscape represents a mix of global conglomerates and specialized regional manufacturers, with a notable presence of family-owned businesses, particularly in the glass packaging and corrugated packaging segments. The market structure is moderately consolidated in certain segments like glass packaging and metal packaging, while remaining relatively fragmented in plastic packaging and corrugated boxes. Major global players have strengthened their position through strategic acquisitions of local manufacturers, enabling them to expand their production capabilities and distribution networks across Mexico's key industrial regions.

The market demonstrates active merger and acquisition activity, particularly in the plastic packaging segment, where global players seek to establish stronger footholds in the growing Mexican market. Companies are increasingly pursuing vertical integration strategies, especially in recycling operations, to secure raw material supply and meet sustainability goals. Local players maintain competitive advantages through their established distribution networks, long-standing customer relationships, and deep understanding of regional market dynamics, while global players leverage their technological expertise and economies of scale.

Innovation and Sustainability Drive Future Success

Success in the Mexican industrial packaging market increasingly depends on companies' ability to balance sustainability initiatives with cost-effective solutions. Market leaders are investing heavily in research and development to create innovative packaging solutions that meet both environmental regulations and customer demands. The high concentration of end-users in the food and beverage sector necessitates strong relationships with key customers and the ability to provide customized solutions. Companies must also navigate the growing substitution threat from flexible packaging alternatives while maintaining competitive pricing strategies.

Future market share gains will likely depend on companies' ability to establish efficient recycling infrastructure and develop circular economy solutions. Regulatory compliance, particularly regarding plastic usage and recycling requirements, will become increasingly important for maintaining market position. Contenders can gain ground by focusing on niche markets, developing specialized packaging solutions for specific industries, and establishing strategic partnerships with key end-users. Success will also depend on companies' ability to optimize their supply chains, leverage digital technologies for production efficiency, and maintain strong relationships with raw material suppliers.

Mexico Rigid Packaging Market Leaders

-

Coexpan S.A.

-

AptarGroup, Inc.

-

Grupo Gondi

-

Envases Group

-

Vitro S.A.B. de CV

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Mexico Rigid Packaging Market News

- June 2022 - Smurfit Kappa has announced an investment of USD 23.5 Million (EUR 21.9 Million) to upgrade its sheet plant in Nuevo Laredo in Northeast Mexico. This investment is aimed at making the plant more sustainable, including installing a new corrugator.

- June 2022 - Saverglass is to double capacity at its Guadalajara, Mexico, production facility and increase its decoration capability. The USD 116 million investment will include a 200,000 tonnes-a-year furnace capable of manufacturing 200 million bottles in three colors: extra-white, antique green, and dark yellow. The 30 hectares plant expansion will allow Saverglass to preserve the quality and regularity of production for its customers.

- May 2022 - Ball Corp. and Manna Capital Partners of Louisville, Kentucky, partnered to build and run a recycled-content aluminum can sheet rolling mill and melt shop in Los Lunas, New Mexico. The company reports that Ball, based in Westminster, Colorado, will sign a long-term supply arrangement and also plans to take a minority equity stake in the mill.

- February 2022 - US-based metal packaging producer Crown Holdings secured Aluminum Stewardship Initiative (ASI) certification for its beverage and could begin operations in Mexico. ASI's Performance Standard certification represents that the business is verified for the responsible manufacturing, obtaining, and managing of aluminum.

Mexico Rigid Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Prodcuts

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Demand From Packaging Food And Industrial Sector

- 5.1.2 The Manufacturing And Allied Sectors Are Expected To Rebound And Contribute To The Market Demand In Mexico

-

5.2 Market Challenge

- 5.2.1 Stringent Regulations Coupled With Strong Competition From Flexible-based Products

- 5.3 Market Opportunities

- 5.4 Impact of COVID-19 on Mexico Rigid Packaging Market

- 5.5 Role of Reusability and Recyclability in Rigid Packaging Market

6. MARKET SEGMENTATION

-

6.1 By Packaging Material Type

- 6.1.1 Paper and Paperboard

- 6.1.2 Container Glass

- 6.1.3 Metal

- 6.1.4 Rigid Plastic (Bottles, Containers, Caps and Closures, Bulk-based products)

-

6.2 By End-User Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare and Pharmaceutical

- 6.2.4 Beauty and Personal Care

- 6.2.5 Industrial

- 6.2.6 Other End-User Industries

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles - Flexible Plastic Vendors

- 7.1.1 Altopro Inc.

- 7.1.2 Transcontinental Inc.

- 7.1.3 Amcor PLC

- 7.1.4 Printpack

- 7.1.5 UFlex Limited

- 7.1.6 Huhtamaki Oyj

- 7.1.7 Mondi PLC

- 7.1.8 Coexpan

- 7.1.9 Constantia Flexibles

- 7.1.10 FLAIR Flexible Packaging Corp.

-

7.2 Company Profiles - Rigid Plastic Vendors

- 7.2.1 Amcor Rigid Packaging Mexico

- 7.2.2 Grupo Phoenix

- 7.2.3 Aptar Group Inc.

- 7.2.4 GREIF Inc.

- 7.2.5 ALPLA Mexico S.A. de C.V. (ALPLA GROUP)

- 7.2.6 Berry Global Inc.

- 7.2.7 Winpak Ltd

- 7.2.8 Sonoco Mexico Products Company

- 7.2.9 COEXPAN S.A. (Coexpan México, S.A. de C.V.)

- 7.2.10 Monoflo International

-

7.3 Company Profiles - Carton and Corrugated Box Vendors

- 7.3.1 Smurfit Kappa

- 7.3.2 International Paper Company

- 7.3.3 Westrock Company

- 7.3.4 Tri-Wall Limited

- 7.3.5 Copamex, S.A. de C.V.

- 7.3.6 Graphic Packaging International, LLC

- 7.3.7 Edelmann GmbH

- 7.3.8 Grupo Gondi

- 7.3.9 Papeles Y Conversiones De Mexico

- 7.3.10 Biopappel

-

7.4 Company Profiles - Foam and Metal Can Vendors

- 7.4.1 Ball Corporation

- 7.4.2 Crown Holdings, Inc.

- 7.4.3 Mauser Packaging Solutions

- 7.4.4 CCL Container

- 7.4.5 KB Foam Inc

- 7.4.6 Sealed Air Corporation

- 7.4.7 Madison Polymeric Engineering, Inc

- 7.4.8 Sonoco Mexico Products Company

- 7.4.9 ALLTUB Group

- 7.4.10 Envases Group

-

7.5 Company Profiles - Container Glass Vendors

- 7.5.1 Schott AG

- 7.5.2 Corning Incorporated

- 7.5.3 Vitro S.A.B. de CV

- 7.5.4 Vidrio Formas S.A. de C.V.

- 7.5.5 Fevisa

- 7.5.6 Gerresheimer AG

- 7.5.7 O-I Glass, Inc.

- 7.5.8 Saverglass Group

- 7.5.9 Jocoglass

- 7.5.10 Fusion y Formas

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Mexico Rigid Packaging Industry Segmentation

The study on Mexico's Rigid packaging market tracks demand for the major packaging format types such as rigid plastic containers, paper and paperboard, container glass, and metal cans, along with corresponding end-user industry verticals demand and revenue accrued from the sales of these rigid packaging products.

The Market is primarily segmented based on packaging material (rigid plastic containers, paper and paperboard, container glass and metal cans), end-user ( food, beverage, industrial, healthcare and pharmaceutical, and others). The market estimates are adjusted based on the assessment of the impact of COVID-19 on the market. The scope of the study is limited to Mexico Region only.

| By Packaging Material Type | Paper and Paperboard |

| Container Glass | |

| Metal | |

| Rigid Plastic (Bottles, Containers, Caps and Closures, Bulk-based products) | |

| By End-User Industry | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Beauty and Personal Care | |

| Industrial | |

| Other End-User Industries |

Need A Different Region or Segment?

Customize Now

Mexico Rigid Packaging Market Research FAQs

How big is the Mexico Rigid Packaging Market?

The Mexico Rigid Packaging Market size is expected to reach USD 7.49 billion in 2025 and grow at a CAGR of 5.53% to reach USD 9.81 billion by 2030.

What is the current Mexico Rigid Packaging Market size?

In 2025, the Mexico Rigid Packaging Market size is expected to reach USD 7.49 billion.

Who are the key players in Mexico Rigid Packaging Market?

Coexpan S.A., AptarGroup, Inc., Grupo Gondi, Envases Group and Vitro S.A.B. de CV are the major companies operating in the Mexico Rigid Packaging Market.

What years does this Mexico Rigid Packaging Market cover, and what was the market size in 2024?

In 2024, the Mexico Rigid Packaging Market size was estimated at USD 7.08 billion. The report covers the Mexico Rigid Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Mexico Rigid Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Mexico Rigid Packaging Market Research

Mordor Intelligence provides a comprehensive analysis of the rigid packaging industry, drawing on decades of expertise in industrial packaging research. Our extensive coverage includes various segments such as blister packaging, glass packaging, and metal packaging solutions. The analysis details developments in thermoformed packaging technologies and innovations in rigid plastic packaging. This information offers stakeholders crucial insights into rigid container and rigid box manufacturing trends.

This detailed report, available as an easy-to-download PDF, offers an in-depth examination of rigid plastic container developments and rigid food packaging applications. Stakeholders gain valuable insights into innovations in rigid tray design, rigid bottle manufacturing processes, and corrugated packaging solutions. The analysis covers emerging trends in hard packaging technologies and rigid industrial packaging applications. It is supported by extensive data on rigid food packaging demand patterns. Our research methodology ensures actionable intelligence for industry participants seeking to optimize their market strategies.