Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

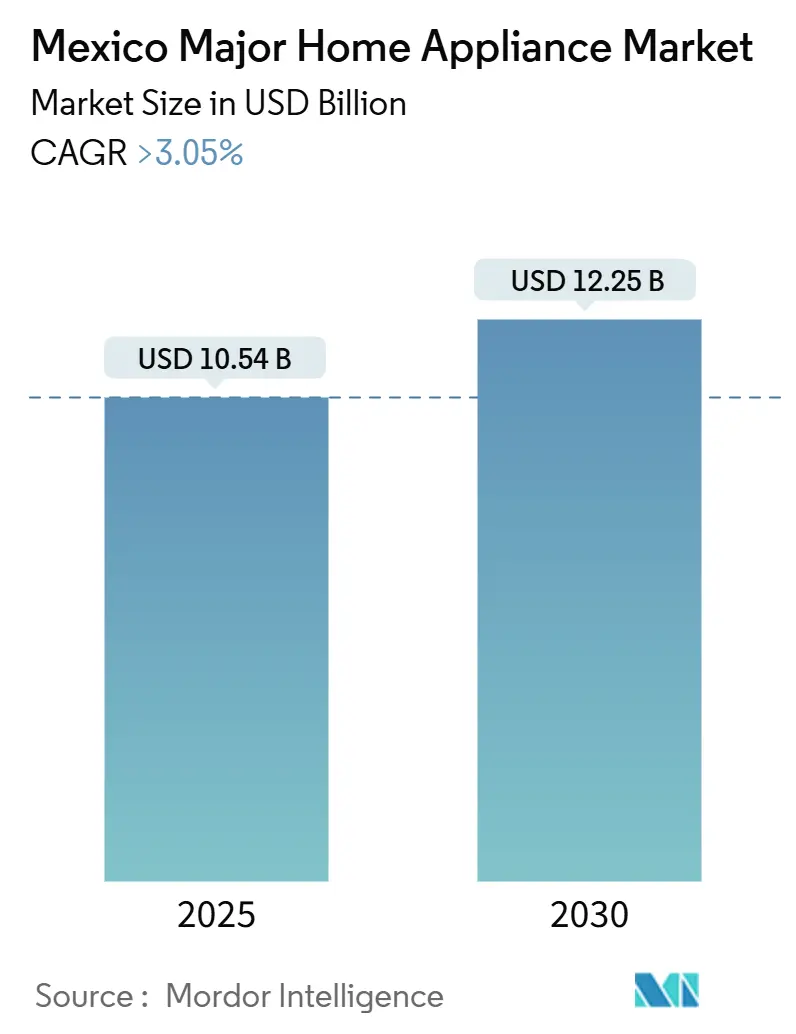

| Market Size (2025) | USD 10.54 Billion |

| Market Size (2030) | USD 12.25 Billion |

| Growth Rate (2025 - 2030) | 3.05% CAGR |

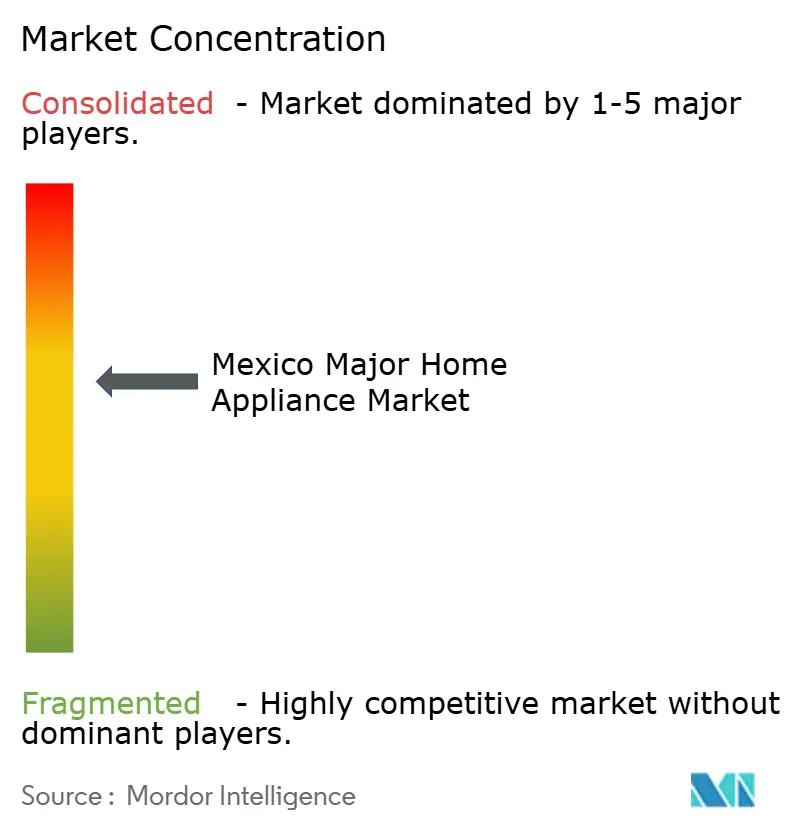

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Major Home Appliance Market Analysis by Mordor Intelligence

The Mexico major home appliances market is valued at USD 10.54 billion in 2025 and is forecast to climb to USD 12.25 billion by 2030, advancing at a 3.05% CAGR over the period. Persistent near-shoring inflows, totalling more than USD 1.2 billion during 2024-2025, underpin this steady expansion even as national GDP growth cools to an expected 1.0% in 2025. Demand resilience is strongest in the refrigerator and washing-machine categories, where energy-efficiency upgrades and evolving hygiene norms spur replacement intent. Multi-brand retailers retain the largest channel footprint, yet rapid online adoption is reshaping price discovery, inventory planning, and last-mile logistics. Regionally, Northern Mexico captures the lion’s share of sales thanks to concentrated manufacturing activity, higher wages, and hot-climate cooling needs, while Southern states deliver the fastest growth as infrastructure projects accelerate urbanization. Competitive intensity is set to rise because tariff uncertainty is prompting some global brands to weigh partial output shifts to the United States, even as domestic champion Mabe commits record local investment.

Key Report Takeaways

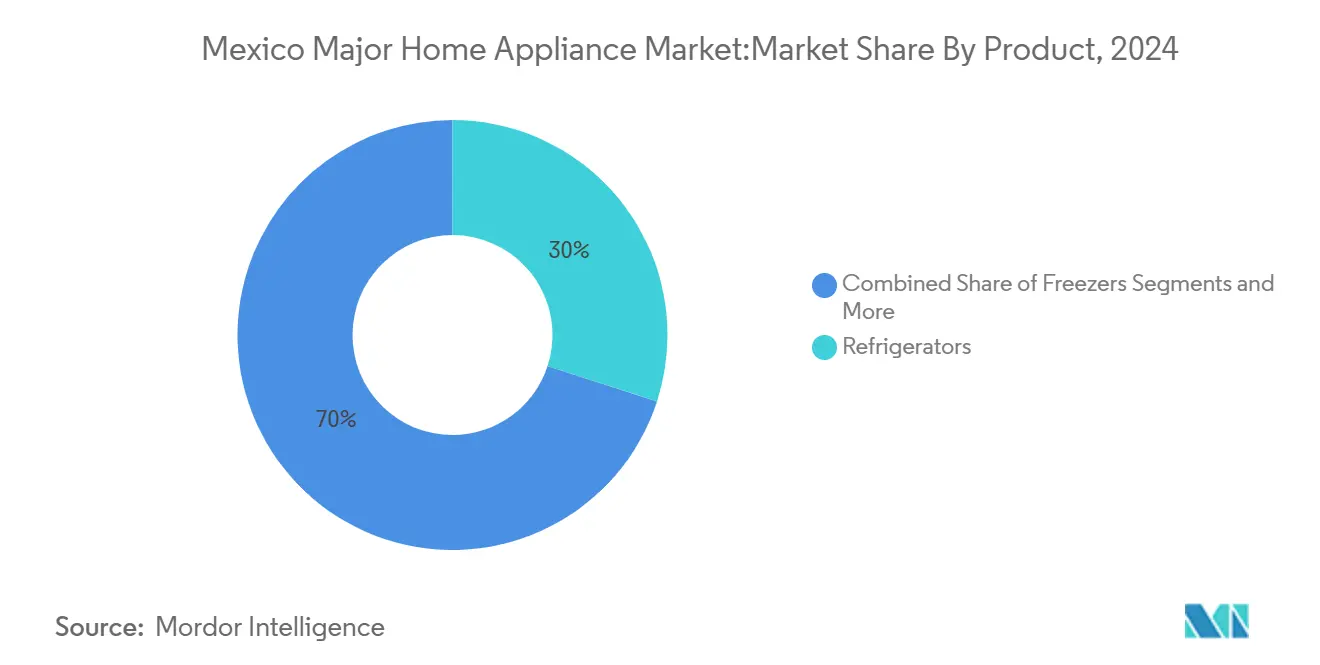

- By product, refrigerators led with 30% of the Mexico major home appliances market share in 2024, whereas washing machines record the highest projected CAGR at 3.4% through 2030.

- By distribution channel, multi-brand stores held 35% of the Mexico major home appliances market size in 2024, while online retail is growing at a 6.2% CAGR during the forecast window.

- By geography, Northern Mexico accounted for 45% of the Mexico major home appliances market size in 2024 and Southern Mexico is set to expand at a 4.6% CAGR to 2030.

Mexico Major Home Appliance Market Trends and Insights

Drivers Impact Analysis

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income and middle-class expansion | +0.8% | Central and Northern Mexico, spillover to urban Southern areas | Medium term (2-4 years) |

| Urbanization and housing projects pipeline | +0.6% | National; early gains in Mexico City, Monterrey, Guadalajara | Long term (≥4 years) |

| Energy-efficiency regulations driving replacement | +0.5% | National; strongest in high-consumption Northern states | Short term (≤2 years) |

| Omnichannel retail and e-commerce boom | +0.4% | Urban centers nationwide; peak in Northern and Central Mexico | Medium term (2-4 years) |

| Near-shoring of appliance manufacturing | +0.3% | Northern manufacturing corridors | Long term (≥4 years) |

| Rapid uptake of smart and inverter models | +0.2% | Urban affluent segments in Northern and Central Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Middle-Class Expansion

Northern and Central states continue to post wage gains as manufacturing payrolls swell, sustaining appliance outlays even while GDP growth eases to 0.9% in Q4 2024. Consumer surveys reveal that 70% of households prefer cutting volumes rather than trading down to cheaper brands, signalling enduring loyalty to value-oriented labels [1]McKinsey & Company, “Mexican Consumers: Loyalty under Pressure,” mckinsey.com. Middle-class clusters in Monterrey, Saltillo, and Ciudad Juárez channel pay increases toward premium refrigerators and inverter air conditioners, promising lower running costs.

Urbanization and Housing Projects Pipeline

Federal housing programs and a construction sector that Deloitte estimates will grow 6.0 % in 2025 are opening fresh demand nodes across Tier-II cities. Quintana Roo, Yucatán and Campeche show the fastest household formation rates as road, rail and tourism investments deepen the urban footprint. Appliance makers see first-time buyers moving directly from open-flame cooking to induction stoves. Academic work indicates that appliance energy use grows in tandem with urban migration, with refrigerators and washing machines displaying the steepest penetration curves. Yet, delayed housing completions intermittently curb sell-in volumes, pushing manufacturers to run variable production schedules.

Energy-Efficiency Regulations Driving Replacement

The NOM-015-ENER-2002 update obliges new refrigerators to be 30% more efficient than earlier models, accelerating scrappage of outdated stock [2]National Institute of Electricity and Clean Energy, “NOM-015-ENER-2002 Compliance Guide,” ineel.mx. Programs run by CONUEE and FIDE subsidize swaps, and studies in Mexicali show that switching oversized air conditioners can slash household consumption by 32%. As electricity tariffs creep up, marketing that quantifies peso savings resonates with cost-sensitive segments. Producers that secure yellow-label certification gain shelf primacy in large retailers and online filters, supporting price discipline.

Omnichannel Retail and E-Commerce Boom

AMVO’s HOT SALE 2024 campaign demonstrated robust shopper engagement with big-ticket appliances, legitimizing digital carts for high-value goods [3]Asociación Mexicana de Venta Online (AMVO), “Estudio de Venta Online en México 2024,” amvo.org.mx. Coppel’s MX$14.2 billion capex plan adds 100 stores and logistics hubs, while its BanCoppel arm extends credit to first-time buyers. Pure-play e-commerce platforms use zero-interest installments to lure traffic from informal street markets. Retailers still keep cash-on-delivery and in-store pickup alive to bridge the trust deficit among the 55% of workers in informal employment who lack formal banking.

Restraints Impact Analysis

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation and peso volatility pressure | -0.7% | National; most acute in low-income Southern and rural areas | Short term (≤2 years) |

| Informal market and grey imports | -0.4% | Border zones and urban informal settlements | Medium term (2-4 years) |

| Rising electricity tariff uncertainty | -0.3% | Northern high-consumption states and industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation and Peso Volatility Pressure on Affordability

Rising prices squeeze household budgets, leaving less money for big-ticket appliances. A softer peso then pushes up the cost of imported parts and finished units, so manufacturers have to walk a fine line between raising prices and keeping their profits intact. EY polls show 55% of consumers curbing spending to essentials during inflation spikes, dampening discretionary appliance upgrades. Flexible-term credit and buy-now-pay-later offers arise as mitigation levers, but rural budgets still fall short of the installment threshold for many major devices. "Rural households face significant constraints with average per capita incomes of 1,842.56 pesos (USD 92-102) per month as of Q4 2024, with 50.7% of rural workers in labor poverty, limiting discretionary spending on major appliances

Informal Market and Grey Imports Erode Branded Sales

With over half of Mexican workers earning their living in the informal sector—an activity that also produces almost one-quarter of the nation’s output—many appliances move through unofficial channels rather than established stores, taking business away from well-known brands. To stem the resulting tax losses, the government will broaden reference-price rules for imports in May 2025; importers that declare values below those benchmarks will have to post financial guarantees, a move designed to discourage under-pricing. The Economy Ministry will impose reference pricing and guarantee deposits from May 2025, aiming to stamp out under-invoiced imports, yet enforcement gaps linger in high-traffic crossings. Formal retailers must therefore balance competitive ticket prices against service differentiation to protect their share.

Segment Analysis

By Product: Refrigerators Lead Market Share

Refrigerators commanded 30% of the Mexico major home appliances market share in 2024 and remain the volume anchor for manufacturers. Roughly 80% of households own at least one unit, and replacement programs stimulated by NOM-015-ENER-2002 promise to save 4.7 TWh each year if older models are fully retired. The Mexico major home appliances market size for refrigerators is forecast to extend steadily as urban living propels multi-door formats, while rural penetration estates drift toward basic top-freezer units. Mabe, Whirlpoo,l and LG stay top of mind due to entrenched factory presence and after-sales reach. Mid-tier consumers weigh upfront penalties against lifetime energy savings highlighted on the yellow label.

Washing machines trail in installed base yet outpace other categories with a 3.4% CAGR through 2030. Urban migration heightens focus on hygiene and time savings versus manual washing. Smart front loaders with inverter motors gain share in cities, whereas twin-tub models hold ground among price-sensitive buyers. Air conditioners post the sharpest seasonal spikes in northern deserts where oversized legacy units inflate power bills, creating swap-out opportunities for inverter splits. Ovens, freezers and dishwashers capture niche gains tied to lifestyle shifts in dual-income households and rising fast-food aversion.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Multi-Brand Stores Dominate

Multi-brand stores retained 35% of the Mexico major home appliances market in 2024, leveraging broad assortments and credit underwriting to attract walk-in traffic. Chains such as Coppel, Liverpool and Elektra use loyalty plans and lay-away options to deepen engagement. Ecommerce, however, registers the swiftest climb at a 6.2% CAGR thanks to HOT SALE campaigns and nationwide free-shipping thresholds. The Mexico major home appliances market size sold online is still small but scales quickly as mobile penetration enables price comparisons and influencer reviews.

Retailers invest in dark stores, regional fulfilment nodes and last-mile fleets to compress delivery windows. Exclusive brand outlets operate mainly in high-income metros, offering immersive showrooms and bundled installation that justify premium pricing. Traditional mom-and-pop and catalogue sales linger in remote towns, though limited SKU depth and cash dependency restrict basket growth. Informal cash stalls remain a persistent wildcard, often trading refurbished or smuggled stock.

Geography Analysis

Northern Mexico booked 45% of 2024 revenue, reflecting its status as an export manufacturing heartland and beneficiary of near-shoring inflows topping USD 1.2 billion. Whirlpool’s Ramos Arizpe expansion alone lifts capacity by 300,000 French-door units yearly, while LG’s USD 100 million Reynosa project broadens cooking ranges. High desert temperatures also push cooling appliance spend, with households in Mexicali using 8,193 kWh annually, far above the national mean. Yet tariff risk has Samsung and LG drafting U.S. plant contingencies, underscoring geopolitical fragility.

Central Mexico forms the second-largest cluster, anchored by Mexico City and Guadalajara. Dense urbanization, diversified industry, and 6.0% construction growth yield steady appliance demand despite economic slowdowns. Efficient-appliance rebates gain stronger acceptance here than in any other region, helped by greater electricity-bill awareness and advanced retail networks. The Mexico major home appliances market benefits further from robust transport corridors that trim logistics costs in the populous Bajío.

Southern Mexico delivers the most dynamic outlook at a 4.6% CAGR through 2030 as public infrastructure lifts connectivity and tourism expands income in Quintana Roo and Yucatán. Nevertheless, average rural incomes of USD 44,325 limit discretionary spending, and informal cash sales dominate. Manufacturers targeting the region pair low-ticket top-freezer refrigerators with micro-credit programs and mobile service vans to overcome sparse dealership density. Over time, improved grid stability and broader 4G rollout are expected to unlock latent demand for smart and inverter appliances.

Competitive Landscape

The Mexico major home appliances market sits in a mid-consolidated state where the top five brands capture around two-thirds of revenue. Domestic leader Mabe has reaffirmed its long-term play with a record USD 668 million spending pledge that scales local plants and sharpens R&D. Whirlpool, LG, Samsung and BSH follow close, each hedging tariff exposure through flexible sourcing. The market rewards those synchronizing cost-competitive Mexican assembly with North American design inputs and omnichannel reach.

Tech differentiation is rising fast. Panasonic’s OASYS HVAC platform promises energy cuts above 50% and signals a pivot toward connected ecosystems rather than isolated devices. Samsung’s joint venture with Lennox focuses on VRF systems and ductless splits adapted for North American codes, offering Mexican plants an export springboard. While feature-rich products pull margins upward, informal cash markets continue to test price ceilings, forcing firms to tier portfolios carefully.

Supply-chain realignment is another battleground. Component localization deepens as resin, compressor and control-board suppliers establish plants near Monterrey and Saltillo to shrink lead times. Simultaneously, proposed U.S. tariffs inject planning insecurity; LG and Samsung have publicly weighed incremental Tennessee capacity as a hedge. Such moves would thin Mexico’s content share on certain SKUs, yet strong domestic demand ensures baseline throughput for existing facilities.

Mexico Major Home Appliance Industry Leaders

-

Whirlpool (+Mabe brand JV)

-

LG Electronics

-

Samsung Electronics

-

Mabe (own brand)

-

Electrolux (incl. Frigidaire)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Mabe confirmed a USD 668 million program to scale multi-category production across its Mexican network.

- March 2025: LG earmarked USD 100 million for Reynosa output expansion while drafting contingency relocation plans to Tennessee if 25% tariffs materialize.

- February 2025: Daikin Applied’s Alliance Air unit began constructing a USD 121 million Tijuana plant set to employ 1,000 workers and target data-center cooling demand.

- February 2025: Whirlpool’s Horizon and Plastics plants achieved silver World Class Manufacturing certification, extending lean and safety gains.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the Mexico major home appliance market as the revenue generated from the sale of new, factory-built "white goods" that perform core household tasks, including refrigerators, standalone freezers, washing machines, dishwashers, cooking ovens (inclusive of microwave and combi units), and room air-conditioners, delivered to residential and small commercial users within Mexico in a given year.

Scope Exclusions: Small countertop devices, spare parts, HVAC chillers, and used or refurbished units are outside the study.

Segmentation Overview

- By Product

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Northern Mexico

- Central Mexico

- Southern Mexico

Detailed Research Methodology and Data Validation

Primary Research

We interview appliance makers, component suppliers, national retailers, and logistics specialists across Northern, Central, and Southern Mexico. These discussions confirm penetration rates, warranty return ratios, and typical replacement cycles, helping us refine the desk-derived assumptions and triangulate the final model.

Desk Research

Our analysts start with publicly available macro and trade sources such as INEGI household expenditure surveys, Banco de México retail sales indices, UN Comtrade import-export codes 8418 and 8450, CANIETI production releases, and energy-efficiency regulations NOM-015 and NOM-003. Company filings, investor decks, and reputable press are mined to track average selling prices and brand channel strategies. Paid repositories like D&B Hoovers and Dow Jones Factiva assist us in checking manufacturer revenue splits and shipment narratives. The secondary sources cited above are illustrative; many additional references were consulted for validation and clarification.

Market-Sizing & Forecasting

A top-down construct begins with official production, import, and export data to recreate national supply, which is then filtered through estimated domestic sell-through and average selling prices. Select bottom-up checkpoints, including sampled retailer volumes and manufacturer revenue parses, anchor the totals. Key variables include household formation growth, urban electricity tariff trends, replacement cycle length, e-commerce share in durable goods, peso-dollar movements, and enforcement of energy-efficiency norms. Multivariate regression, informed by these drivers and consensus signals from expert calls, projects demand through 2030. Where bottom-up data are spotty, gaps are filled using benchmark price-volume pairs from similar states and years.

Data Validation & Update Cycle

Outputs pass anomaly checks, variance analyses, and multi-analyst peer reviews before sign-off. Reports refresh every twelve months, with mid-cycle revisions triggered by events such as tariff shifts or major plant closures. A final pre-delivery pass ensures clients receive the latest calibrated view.

Why Mordor's Mexico Major Home Appliance Baseline Commands Reliability

Published estimates often differ; definitions, base years, and modeling shortcuts vary, which confuses decision-makers.

Key gap drivers include scope mismatch (some studies fold small devices or exclude built-in air-conditioners), reliance on single-year customs totals without replacement-cycle corrections, older base-year anchoring, and infrequent updates that miss peso volatility. Mordor's disciplined mix of current-year field insight, clearly stated product boundaries, and annual refresh cadence mitigates those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.54 B (2025) | Mordor Intelligence | |

| USD 10.32 B (2024) | Regional Consultancy A | Narrower product mix; air-conditioners excluded |

| USD 11.24 B (2023) | Global Consultancy B | Older base year and customs-only top-down build |

These contrasts show that Mordor Intelligence delivers a balanced, transparent baseline rooted in up-to-date variables and repeatable steps, giving stakeholders a dependable foundation for strategy and investment decisions.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Mexico major home appliances market?

The market stands at USD 10.54 billion in 2025 and is projected to reach USD 12.25 billion by 2030.

Which product category leads sales?

Refrigerators lead with 30% of 2024 revenue, underscoring their essential role in Mexican households.

Which region shows the fastest growth?

Southern Mexico posts the quickest expansion at a 4.6% CAGR through 2030, propelled by infrastructure and tourism development.

How are energy-efficiency rules affecting demand?

NOM-015-ENER-2002 and CONUEE rebate programs are accelerating replacement of older appliances, boosting sales of high-efficiency models that cut household power bills.

Why are manufacturers expanding capacity in Mexico?

Near-shoring strategies and USMCA trade benefits encourage global brands to invest over USD 1.2 billion in 2024-2025 to serve both domestic and North American demand.

Which distribution channel is expanding the quickest for appliance sales in Mexico?

Online retail is the fastest-growing channel, advancing at a 6.2% CAGR as consumers embrace e-commerce platforms and omnichannel services.

Page last updated on: