Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

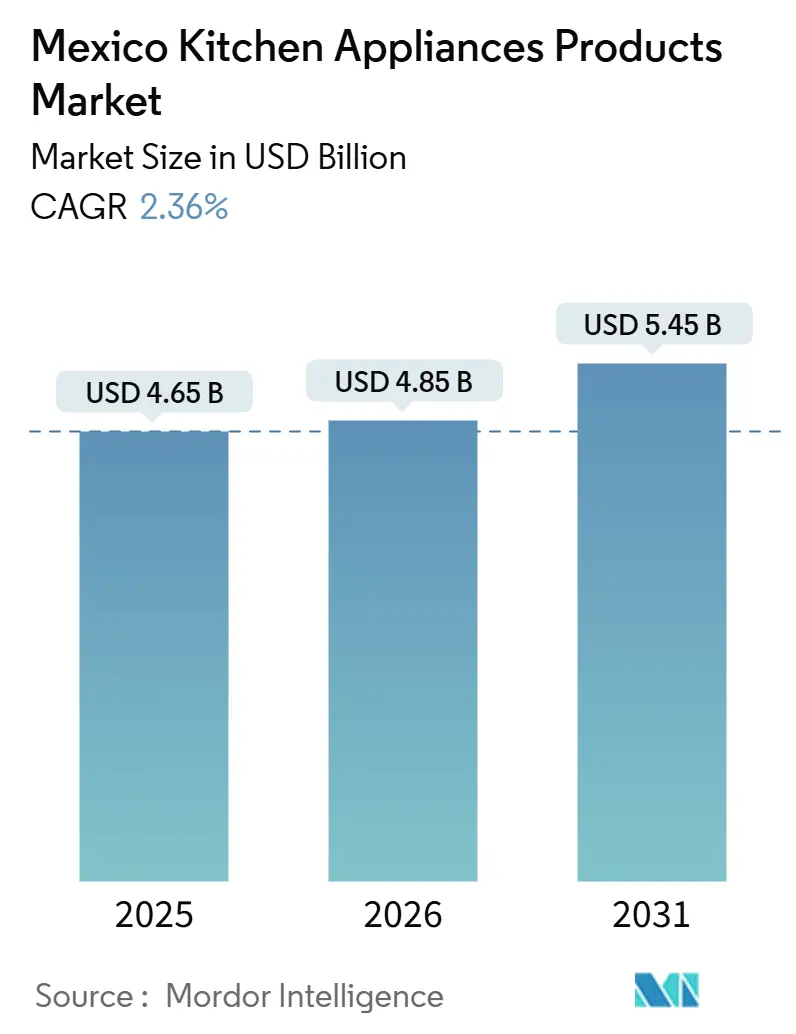

| Base Year Market Size (2025) | USD 4.65 Billion |

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 5.45 Billion |

| Growth Rate (2026 - 2031) | 2.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Kitchen Appliances Products Market Analysis by Mordor Intelligence

The Mexico Kitchen Appliances Products market size is expected to increase from USD 4.65 billion in 2025 to USD 4.85 billion in 2026 and reach USD 5.45 billion by 2031, growing at a CAGR of 2.36% over 2026-2031. Beneath the measured growth rate, regulatory replacement cycles and localized manufacturing are reshaping category mix and price ladders, while distribution is tilting toward omnichannel formats that use credit-led conversion and faster delivery to broaden access. Energy-efficiency mandates under NOM-015 have tightened refrigerator performance thresholds and catalyzed structured replacement, which informs competitive strategy around inverter technology, warranty signaling, and in-country testing capabilities. Retail finance ecosystems that serve informal workers keep demand resilient during price shocks, while tariff uncertainty encourages leading brands to deepen local content and hedge cross-border exposure through capacity and procurement choices. Regionally, Central Mexico remains the revenue anchor due to dense urbanization and mature retail networks, yet Northern Mexico sets the fastest growth curve as nearshoring, wage gains, and hot-climate usage support higher-cycling categories.

Key Report Takeaways

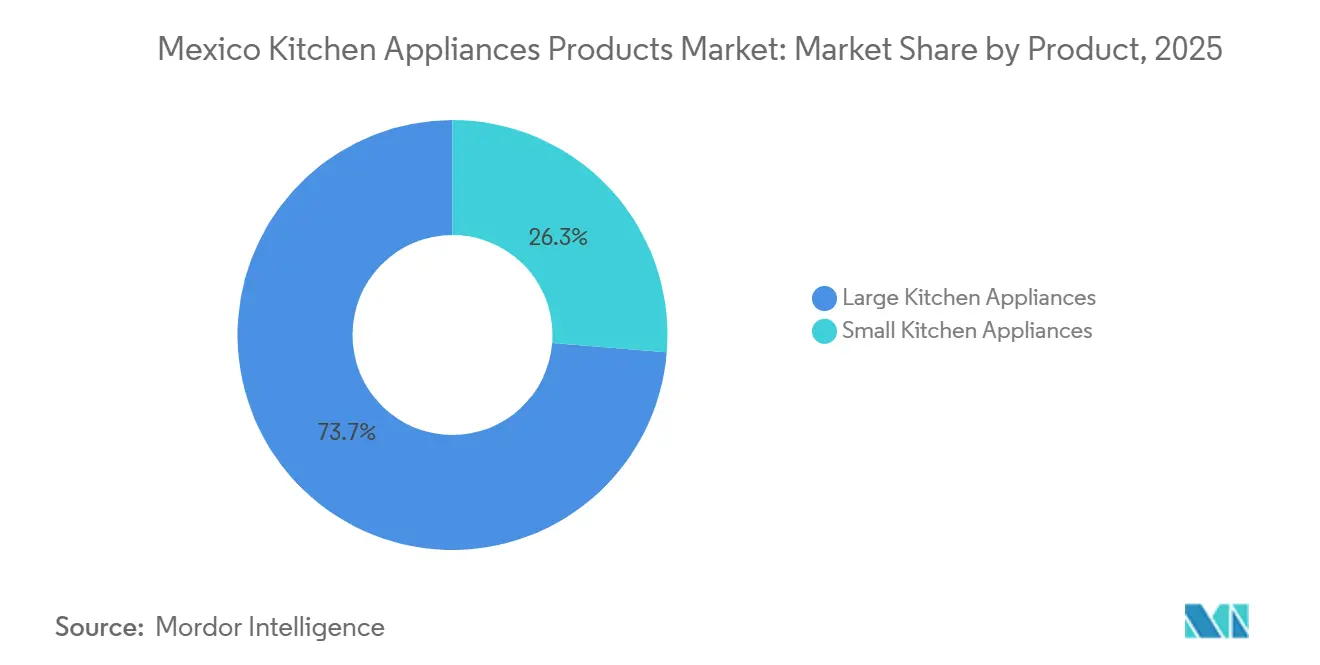

- By product, large kitchen appliances held 73.72% revenue share in 2025, while small kitchen appliances are projected to grow at a 3.45% CAGR through 2031, driven by innovation and product lifecycles. Small kitchen appliances are expected to outpace the overall category during this period.

- By end user, residential accounted for 86.25% of the 2025 volume, while commercial deployments are forecast to expand at a 3.71% CAGR on hotel pipelines and QSR rollout. This growth is supported by capacity additions in tourist corridors and institutional kitchens.

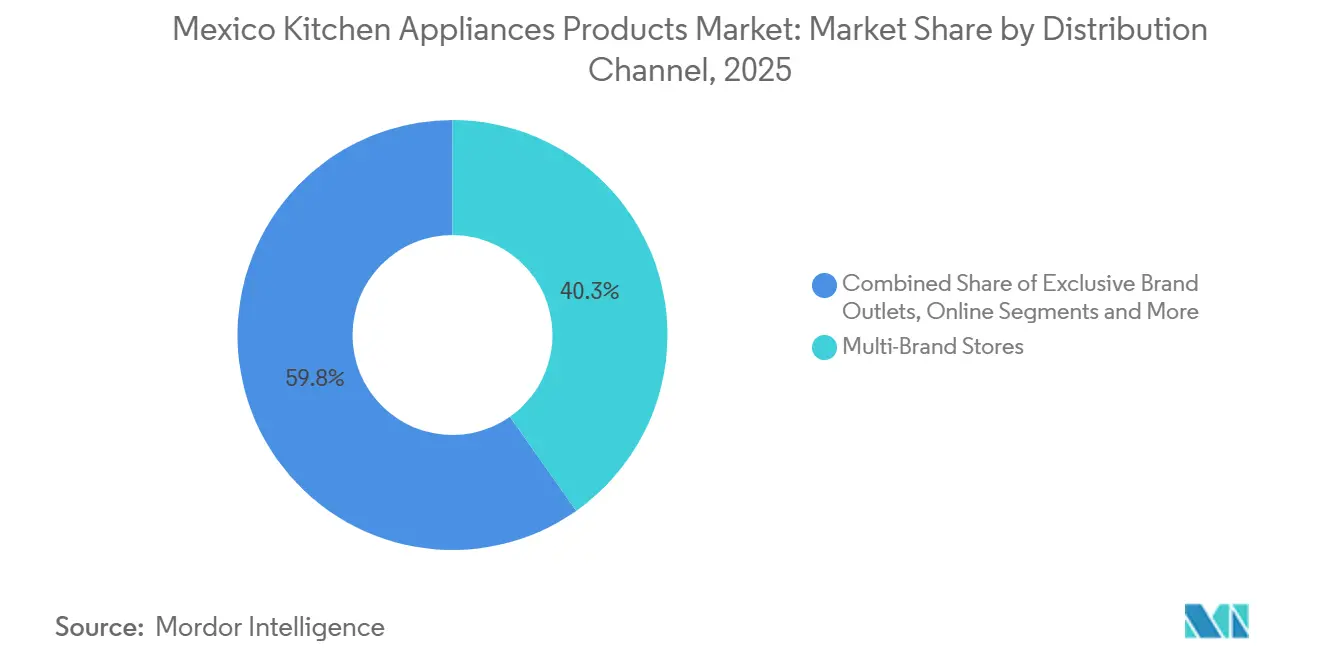

- By distribution channel, multi-brand stores led with 40.25% share in 2025, while online channels are projected to post a 4.21% CAGR as logistics and BNPL improve conversion. Multi-brand stores benefit from captive credit and immediate possession in nationwide chains.

- By geography, Central Mexico held 42.71% of 2025 sales, while Northern Mexico is projected to record a 4.18% CAGR, setting the fastest regional pace through 2031. This growth is driven by nearshoring-led payrolls and manufacturing-linked multipliers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Kitchen Appliances Products Market Trends and Insights

Drivers Impact Analysis

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Refrigeration replacement bolstered by NOM-015 efficiency labeling | +0.5% | National, concentrated in Central and Northern urban cores | Medium term (2-4 years) |

| Omnichannel retail and e-commerce scale-up improves access and pricing | +0.4% | Urban centers nationwide, particularly Northern and Central Mexico | Short term (≤ 2 years) |

| Nearshoring-fueled OEM capacity and local model availability | +0.3% | Northern manufacturing corridors, including Nuevo León, Coahuila, Chihuahua | Long term (≥ 4 years) |

| Water-scarcity hot zones push adoption of water- and energy-saving formats | +0.2% | Northern Mexico, including Monterrey metro, Chihuahua, Sonora | Medium term (2-4 years) |

| Rising DAC tariff exposure heightens consumer focus on efficient appliances | +0.3% | National, with early gains in hot-climate states in Tariff 1C–1F zones | Short term (≤ 2 years) |

| Retail credit proliferation expands addressable demand | +0.8% | National, with spillover to urban informal workers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Refrigeration Replacement Bolstered by NOM-015 Efficiency Labeling

NOM-015-ENER-2018 sets formula-based annual energy consumption limits for refrigerators and freezers sold in Mexico, a threshold that tightened performance expectations compared to the prior edition and directly spurs replacement of the aging installed base. The regulation improves energy outcomes and magnifies the value proposition of inverter compressors and superior efficiency badges, which retailers highlight in marketing to quantify lifetime savings in peso terms for heat-prone metros. Structured testing and certification through accredited laboratories add predictability to product launches for incumbents with in-country labs, which compresses approval cycles relative to smaller importers and shortens time to shelf in mass retail[1]Intertek, “Norma Oficial Mexicana (NOM) Certification for Mexico,” Intertek, intertek.com . Retail finance partners pair NOM-compliant SKUs with months-without-interest offers, which lower upfront barriers and make the total cost of ownership salient for mid-tier households that weigh energy bills against installments. Replacement momentum concentrates in urban cores where electricity usage patterns and DAC risk are front of mind, reinforcing the regulatory pull on refrigerator upgrades through 2031.

Omnichannel Retail and E-Commerce Scale-Up Improves Access and Pricing

Mexico’s omnichannel reset is shifting appliance discovery and conversion across marketplaces, retail sites, and in-store kiosks that extend catalog depth while preserving branch-based credit approvals for informal workers. Hot Sale 2024 showed how comparison-led shopping can reframe pricing power, as small kitchen appliances gained traction through promotional events organized by AMVO and highlighted cross-retailer price transparency[2]AMVO, “México 2025: ¿Cómo liderará el ecommerce con innovación, IA y sostenibilidad en el mercado digital de América Latina?,” AMVO, blog.amvo.org.mx . Retailers are fusing credit and e-commerce workflows so buyers can apply for financing, schedule delivery, and confirm installation windows in a single journey, which lifts conversion for bulky goods that historically required in-person interactions. Large-format chains embed showroom kiosks to let rural customers order SKUs unavailable locally, then rely on improved last-mile logistics to meet delivery expectations that mimic urban standards. Over the forecast horizon, channel boundaries will blur as brands scale direct-to-consumer sites while retaining wholesale exposure, and this hybrid path will balance margin mix with reach in the Mexico Kitchen Appliances Products market.

Nearshoring-Fueled OEM Capacity and Local Model Availability

New investments across Northern Mexico are anchoring refrigerator capacity that aligns with NOM-015 performance requirements and shortens lead times into U.S. border markets, strengthening regional content strategies under USMCA rules. Whirlpool’s capacity expansions in Coahuila and Guanajuato support premium formats, including French-door and side-by-side models, while reducing logistics costs to key distribution hubs in Central and Northern corridors[3]GP Construcción, “Whirlpool Plant Expansion in Ramos Arizpe,” GP Construcción, gpconstruccion.com.mx . Mabe’s record 2025–2027 program prioritizes local supply chains and research on compact formats for space-constrained apartments, a choice that targets urban demographics in Mexico City and Guadalajara. Added capacity enables model proliferation tailored to Mexican preferences, including refrigerator sizes that fit smaller kitchens and cooking options that align with local fuel mixes and safety norms under NOM-003. Nearshoring also disciplines inventory cycles and mitigates port congestion risk, which stabilizes shelf availability and supports consistent promotions across peak retail events in the Mexico Kitchen Appliances Products market.

Water-Scarcity Hot Zones Push Adoption of Water- and Energy-Saving Formats

Northern states contend with periodic water stress that reframes certain appliances from convenience items into conservation tools, which strengthens the case for efficient dishwashers and low-flow configurations in residential and hospitality settings. Hotel and QSR procurement in tourist corridors also favors efficient small appliances and compact dishwashers, linking conservation goals with predictable total-cost-of-ownership outcomes in high-utilization environments. Manufacturers are localizing designs and tuning feature sets for water- and energy-saving performance, and these moves align product narratives with municipal conservation messaging in drought-prone zones. Because format adoption faces cultural and infrastructure barriers, financing and installation services are increasingly packaged to reduce friction at the point of upgrade in cities that saw previous water crises. This dynamic sustains long-run potential for efficient models even as short-run uptake remains gradual, and it reinforces how resource constraints shape category mix in the Mexico Kitchen Appliances Products market.

Restraints Impact Analysis

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Very low dishwasher penetration and cultural habits constrain adoption | -0.4% | National, entrenched in middle- and low-income segments | Long term (≥ 4 years) |

| Fragmented small appliances intensify price competition | -0.4% | National, eroding margins in countertop-appliance SKUs | Short term (≤ 2 years) |

| NOM-003/NOM-001 certification costs prolong time-to-market for importers | -0.3% | National, impacting Asian OEMs and gray-market entrants | Medium term (2-4 years) |

| Household electricity cost shocks curb high-wattage usage | -0.3% | National, acute in regions that exceed subsidized caps | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Very Low Dishwasher Penetration and Cultural Habits Constrain Adoption

Dishwasher ownership remains low across Mexican households due to long-standing cultural habits around hand washing and the lack of under-counter plumbing in a high share of existing housing stock, dynamics that limit addressable demand in the near term. Even where water scarcity strengthens the case for efficient dishwashers, upfront costs and installation complexity can deter first-time buyers despite overall conservation benefits compared to manual washing. Manufacturers that produce compact formats and promote installation services gain traction in select metros, but the national curve reflects gradual adoption rather than rapid category lift. Retail financing helps some households spread the cost, although credit programs tend to favor large appliances with broader usage and clearer monthly-savings narratives. The result is a slow-burn market where education, plumbing retrofits, and water-tariff alignment will be needed to unlock faster growth in the Mexico Kitchen Appliances Products market over the long term.

Fragmented Small Appliances Intensify Price Competition

Countertop appliances attract many independent brands that list through online marketplaces, which intensifies price competition and compresses margins in SKUs like air fryers, blenders, and kettles. Product cycles move quickly and promotional events elevate algorithm-driven price matching, making it harder for incumbents to preserve premium spreads without strong brand equity or differentiated features. As entry barriers are low relative to large appliances, new SKUs can launch rapidly, and this cycle allows fast followers to imitate features and undercut prices in short windows. Retailers respond with private-label lines and exclusive bundles, which keep average selling prices in check while making premiumization sporadic and event-driven rather than steady. These pressures sustain tactical promotions and inventory rotation but restrain the pace of value accretion in the small appliance mix of the Mexico Kitchen Appliances Products market through 2031.

Segment Analysis

By Product: Premium Formats and Inverter Tech Lift Lifecycle Value

Large kitchen appliances accounted for 73.72% of revenue in 2025, while small kitchen appliances tracked a 3.45% CAGR through 2031 and extended their outperformance against the overall growth trend. Refrigerator upgrades concentrate in urban centers where high-usage conditions and regulatory thresholds under NOM-015 elevate the rationale for efficient formats and inverter compressors. Premium French-door and side-by-side models continue to gain share in Northern metros where larger households and hotter climates shape capacity needs, while compact top-mount units remain relevant in space-constrained apartments in Central corridors. Warranty signaling and in-country testing capabilities help incumbents coordinate launches around major retail windows, which anchors share in the Mexico Kitchen Appliances Products market at the high end of large appliances. For small appliances, innovation cycles and online promotion support faster category churn that can elevate product discovery and trial without heavy installation dependencies in the Mexican kitchen Appliances Products industry.

Dishwashers face a slower climb due to cultural habits and installation challenges, yet water-scarcity narratives keep interest alive where conservation is a household priority in hot and dry regions. Range hoods and built-in cooktops grow in line with higher-income urban retrofits, a niche shaped by new home completions and kitchen renovations rather than mass-market replacement cycles. Certification under NOM-003 adds structured, predictable testing and documentation steps for new product launches and deters uncertified entries, which supports a floor for safety and reliability in mass retail. Countertop ovens and electric kettles are adjusting to updated standby-power expectations that encourage re-engineering of power management and extend development timelines, while brands time releases to match retail events. As category roles diverge between large and small formats, the Mexico Kitchen Appliances Products market aligns its product ladder to distinct lifecycles and promotional calendars that can sustain steady upgrade activity across the forecast horizon.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: QSR Expansion and Hotel Retrofits Propel Commercial Uptake

Residential users absorbed 86.25% of volume in 2025, while commercial end users are projected to grow at 3.71% CAGR through 2031 on hotel additions and foodservice expansion in tourism corridors. Hospitality procurement cycles are lumpy and tied to occupancy and new-room pipelines, which create bursts of demand for compact refrigerators, microwaves, and coffee makers, along with maintenance-linked refresh programs for older inventories. Quick-service operators emphasize durability and serviceability in appliances to maximize uptime, a requirement that benefits industrial-grade designs tuned for heavy daily use across high-traffic locations. Nearshoring-related industrial parks add cafeteria installations to the project pipeline and support steady orders for ranges, walk-in refrigeration, and high-cycle dishwashing equipment in Northern states. This mixed commercial demand profile complements stable residential replacement and creates new routes to market in the Mexico Kitchen Appliances Products market that run parallel to retail channels and brand-direct sales.

Residential demand remains tied to replacement of pre-standard units and new household formation in large metros, with efficiency labels and retail financing improving acceptance of premium step-ups in major appliances. Informal income patterns and utility-bill seasonality shape purchase timing, and retailers respond with calendarized promotions and installment offers that smooth upgrades during peak demand months. Regional disparities matter because Northern payrolls and hotter climates support a higher cadence of refrigeration and cooling upgrades than in cooler or lower-income regions, which magnifies geographic spread in growth outcomes. As commercial growth accelerates from a small base and residential replacement continues steadily, the Mexico Kitchen Appliances Products industry aligns feature roadmaps to both heavy-duty use cases and home energy-savings narratives, serving distinct value pools with shared component platforms where possible. These dynamics will shape sell-in patterns and promotional planning through 2031, reinforcing a two-speed end-user mix within the Mexico Kitchen Appliances Products market.

By Distribution Channel: Last-Mile Logistics and BNPL Redraw Channel Economics

Multi-brand stores held 40.25% of distribution in 2025 and continue to benefit from credit underwriting and immediate possession, while online channels are projected to post a 4.21% CAGR through 2031 on logistics speed and checkout financing integration. Retailers deploy in-store kiosks that allow rural shoppers to order extended assortments, a hybrid that binds brick-and-mortar trust with e-commerce assortment reach for bulky appliances. Marketplaces and retail sites use promotional events to jumpstart discovery for small appliances, and association-led campaigns like Hot Sale mobilize cross-channel traffic and competitive pricing. Credit-laddering and months-without-interest offers at checkout anchor conversion for big-ticket items online, bringing digital journeys closer to in-person branch experiences in terms of affordability. As documentation for NOM labels is integrated into product listings, online sellers align with physical-store standards, which supports safety and quality consistency in the Mexico Kitchen Appliances Products market, regardless of channel.

Exclusive brand outlets maintain a small overall share but play an outsized role in premium refrigerators and integrated kitchen packages, where consultative selling and same-day installation services reinforce willingness to pay for feature-rich units. B2B routes support hotel and restaurant fit-outs through project-based procurement and installation, and these volumes bypass conventional retail price ladders and align with service-level agreements that prioritize uptime. Cash-at-delivery options persist in secondary cities to convert unbanked buyers, while marketplace protections and returns handling elevate confidence for large-goods purchases that once were strictly in-store. Over time, the Mexico Kitchen Appliances Products market will reflect a more balanced mix as multi-brand chains match delivery speeds and online retailers deepen credit coverage, shaping a competitive steady state around convenience, financing, and post-sale service quality. Within this convergence, the Mexico Kitchen Appliances Products industry expects higher attach rates for installation and extended warranties, an adjacent revenue stream that scales well in both online and offline environments.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Central Mexico held 42.71% of 2025 kitchen-appliance sales, reflecting dense urbanization, mature retail footprints, and strong omnichannel fulfillment across the Mexico City and Guadalajara metros. The region’s growth moderates as ownership rates in core categories approach saturation, and replacement cycles orient toward premium upgrades with better energy performance and larger capacities in refrigerators and ranges. Flagship department stores and same-day marketplace logistics reinforce a service expectation benchmark that is now propagating to tier-two cities, balancing convenience with assortments that include premium and compact formats. The Mexico Kitchen Appliances Products market in Central corridors will lean on regulatory-led replacement and premium step-ups, including connected features and improved food preservation, to sustain value growth through 2031. As incumbents deploy in-country labs and faster test loops, inventory turnover remains predictable and aligned with key promotional calendars in the region’s most competitive retail nodes.

Northern Mexico records the fastest trajectory with a 4.18% projected CAGR, reflecting nearshoring-driven payrolls, hotter climates that elevate cooling and refrigeration usage, and the proximity of OEM capacity in Nuevo León and Coahuila. Large-format refrigerators with inverter compressors resonate in heat-prone metros where seasonality in electricity usage raises the profile of energy savings and drives premium acceptance within household budgets. New industrial parks, cross-border logistics, and wage effects support cafeteria installations and commercial kitchen demand, a base that amplifies regional growth beyond residential replacement alone. The Mexico Kitchen Appliances Products market benefits from capacity risk hedging as brands align production schedules to regional demand curves and reduce stockout risk during summer peaks in the North. Over time, proximity to suppliers and a more skilled labor pool should lower fulfillment volatility, helping the region sustain its edge on growth and product availability.

Southern Mexico is smaller by value but sees episodic acceleration tied to tourism infrastructure in Quintana Roo and Yucatán and to agro-processing facilities that require reliable, efficient refrigeration. Urban cores adopt omnichannel standards quickly, but rural peripheries still favor informal channels and refurbished units, which tempers the impact of premiumization and complicates warranty enforcement. As e-commerce platforms improve trust signals and expand cash-on-delivery options, formal channels should gradually gain share in secondary cities where online assortment broadens choice and reduces travel time for large purchases. The Mexico Kitchen Appliances Products market will continue to show a two-speed pattern in the South, as tourism-linked commercial upgrades climb and residential upgrades follow income and credit access improvements in urban clusters. These geographic contrasts underline how national-level figures blend mature replacement in the Center, capacity-fueled growth in the North, and tourism-driven procurement in parts of the South through the forecast period.

Competitive Landscape

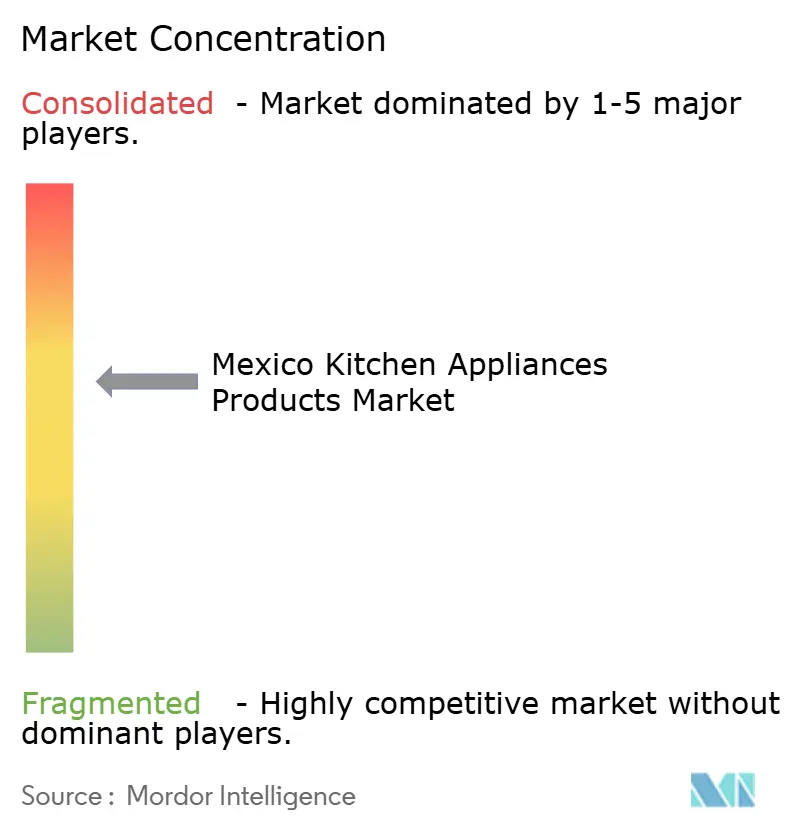

The Mexico Kitchen Appliances Products market exhibits mid-level consolidation, with Mabe, Whirlpool, LG, Samsung, and Electrolux, a top-five group that collectively represents two-thirds of revenue and sets the tone in major appliances. Incumbents leverage in-country testing, regulatory alignment, and warranty signaling to protect share in core categories like refrigerators and ranges, while small-appliance niches stay fragmented as independent brands exploit marketplace reach. Mabe’s 2025–2027 investment program underscores a long-term bet on local content and multi-category scaling in fifteen Mexican factories, which positions it to absorb regulatory shifts and logistics disruptions with greater resilience than import-centric rivals. Whirlpool’s footprint in Coahuila and Guanajuato advances premium-capacity refrigerators and shortens supply lines to Central distribution nodes, a shift that reduces transport costs and improves response time to promotional windows. BSH’s new refrigerator plant in Monterrey expands high-efficiency model availability domestically and complements North American export flows, highlighting how nearshoring reinforces product availability across price bands in Mexico.

Premium differentiation centers on energy performance, capacity, and connected features that support remote diagnostics and faster service resolution, while retailers showcase these benefits through dedicated brand spaces and bundled installation services. Samsung’s technician training initiatives deepen service capabilities for connected ecosystems and reinforce after-sales support, a factor that influences brand choice for high-end refrigerators and built-in appliances in metros with strong tech adoption[4]Samsung Global Newsroom, “Around the World (Feb 2025),” Samsung, news.samsung.com. At the same time, certification stringency discourages gray imports and strengthens the relative positioning of compliant brands that maintain full documentation online and in-store, a requirement that online sellers now integrate into product pages. As tariffs and trade policy remain a consideration, leading brands pursue flexible production planning and supplier diversification to insulate Mexico-bound SKUs, which supports steadier delivery cycles and pricing continuity in mass retail. These moves indicate that operational agility and regulatory fluency will be critical to sustaining share gains in the Mexico Kitchen Appliances Products market through 2031.

White-space opportunities remain in water-saving dishwashers for drought-prone metros, mid-priced built-in configurations for urban retrofits, and D2C kitchen bundles that unify financing, delivery, installation, and service into one offer. Retailers increasingly link credit pre-approval to upgrade prompts, a practice that encourages basket expansion when customers become eligible for higher installment thresholds, thereby reinforcing closed-loop ecosystems. As the competitive field balances consolidation in large appliances and fragmentation in small appliances, incumbents will continue to use reliability, service, and certified performance as pillars, while challengers exploit online discovery and price transparency to win episodic share in the Mexico Kitchen Appliances Products market. Over time, quality enforcement by PROFECO and the normalization of labeling online reduce information asymmetry for buyers, which should reward durable energy performance and clear service propositions across price tiers. This environment supports steady value creation for brands that align product roadmaps with Mexico’s resource realities, urban housing formats, and evolving channel economics in the Mexico Kitchen Appliances Products industry.

Mexico Kitchen Appliances Products Industry Leaders

LG Electronics

Electrolux AB

Samsung Electronics

Whirlpool Corporation

Mabe

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Samsung Electronics Mexico was recognized in ESG rankings and opened an air-conditioning training center in Santa Catarina, Monterrey, to certify technicians for Samsung HVAC systems and SmartThings integration, strengthening the service backbone for connected appliances.

- March 2025: Mabe confirmed a USD 668 million investment program for 2025–2027 to expand multi-category production across its Mexican factories, focusing on refrigerators, ranges, and dishwashers, while deepening local supply chains to strengthen resilience against tariff risks

- August 2024: BSH Home Appliances inaugurated a USD 260 million refrigerator factory in Monterrey, Nuevo León, with an initial 300,000-unit annual capacity focused on high-efficiency French-door bottom-mount models and on-site photovoltaic power integration

Mexico Kitchen Appliances Products Market Report Scope

Kitchen Appliances means appliances generally found in consumers' kitchens, such as refrigerators, stoves, dishwashers, washing machines, tumble dryers, and microwave ovens. A complete background analysis of the Mexico Kitchen Appliances Products Industry, which includes an assessment of the national accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and a market overview, is covered in the report. Mexico's Kitchen Appliances Market is segmented by product type (Food Preparation Appliances, Small Cooking Appliances, Large Kitchen Appliances, and other kitchen appliances), by distribution channel (Specialist retailers, E-commerce, Supermarkets and Hypermarkets, Department Stores, and other distribution channels). The report offers market size and forecasts for the Mexico Kitchen Appliances Market in value (USD Million) for all the above segments.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| Northern Mexico |

| Central Mexico |

| Southern Mexico |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | Northern Mexico | |

| Central Mexico | ||

| Southern Mexico | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size and growth outlook for the Mexico Kitchen Appliances Products market through 2031?

The market size is expected to increase from USD 4.65 billion in 2025 to USD 4.85 billion in 2026 and reach USD 5.45 billion by 2031, growing at a CAGR of 2.36% over 2026-2031

Which product categories are leading and which are growing the fastest in Mexico Kitchen Appliances Products?

Large appliances lead with 73.72% of 2025 revenue, while small appliances are projected to grow at 3.45% CAGR through 2031 as innovation cycles and online promotion accelerate adoption.

How do Mexico’s NOM standards affect appliance purchases and upgrades?

NOM-015 and NOM-003 set efficiency and electrical safety baselines that shape refrigerator upgrades and standardize product labeling, which helps consumers compare options and supports steady replacement.

Which regions in Mexico are driving future demand for kitchen appliances?

Central Mexico holds the largest 2025 share due to urbanization and retail density, while Northern Mexico is expected to grow fastest at a 4.18% CAGR on nearshoring, hotter climates, and capacity proximity.

How is retail credit influencing appliance sales in Mexico Kitchen Appliances Products?

Captive credit and months-without-interest terms expand access for informal workers and shift focus from sticker price to monthly payments, which improves conversion, especially for big-ticket refrigerators and ranges.

What competitive strategies are leaders using in the Mexico Kitchen Appliances Products market?

Leading brands combine in-country testing, warranty signaling, and localized production with omnichannel partnerships and service training to protect share, while smaller players leverage marketplaces and promotions to win episodic gains.