| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 159.75 Billion |

| Market Size (2030) | USD 190.10 Billion |

| CAGR (2025 - 2030) | 3.54 % |

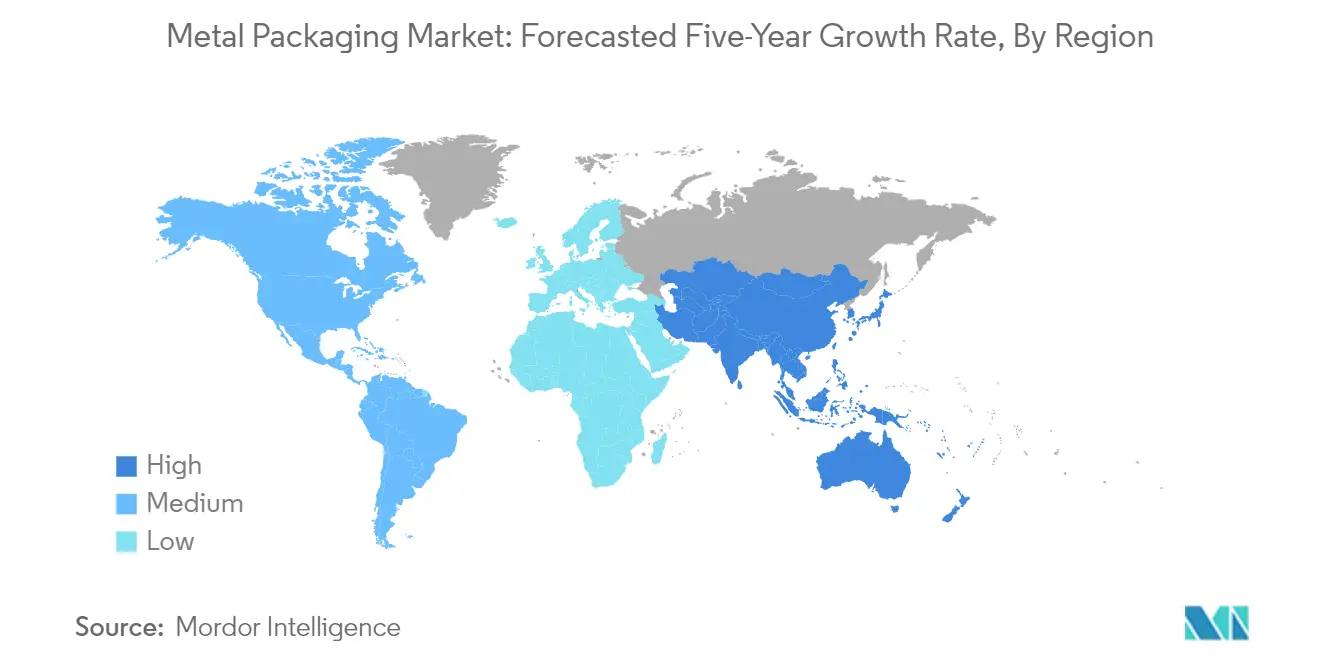

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Metal Packaging Market Analysis

The Metal Packaging Market size is worth USD 159.75 Billion in 2025, growing at an 3.54% CAGR and is forecast to hit USD 190.10 Billion by 2030.

The metal packaging industry is experiencing a significant transformation driven by sustainability initiatives and technological advancements. According to recent data from Metal Packaging Europe, 78.5% of steel packaging and 73% of aluminum beverage cans are recycled in Europe as of January 2024, highlighting the industry's commitment to circular economy principles. Major manufacturers are investing in innovative recycling technologies and sustainable production methods, with companies like Beiersdorf announcing in September 2023 that all European NIVEA aerosol deodorant cans will contain a minimum of 50% recycled aluminum. This shift towards sustainable practices is reshaping the industry landscape while creating new opportunities for metal packaging companies to differentiate their offerings.

The industry is witnessing substantial technological innovations in manufacturing processes and material development. In February 2023, Ardagh Metal Packaging's strategic acquisition of digital can printer NOMOQ demonstrated the industry's push toward advanced printing technologies and customization capabilities. These technological advancements are enabling manufacturers to offer more sophisticated metal container solutions while improving production efficiency and reducing environmental impact. The integration of smart technologies and digital printing solutions is revolutionizing the way metal packaging is produced and customized for various applications.

Global consumption patterns continue to drive market expansion, with the beverage sector leading the demand. Current data indicates that worldwide beer and soda consumption utilizes approximately 180 billion aluminum packaging annually, equivalent to 6,700 cans every second. This tremendous volume is further exemplified by Red Bull's performance, which sold 12.10 billion cans in 2023, marking an increase from 11.60 billion the previous year. The industry is responding to this demand by investing in capacity expansion and innovative beverage can solutions that cater to changing consumer preferences.

The metal packaging sector is experiencing significant consolidation and strategic partnerships aimed at strengthening market positions and enhancing technological capabilities. In September 2023, Novelis Inc. established a landmark partnership with Ball Corporation to supply aluminum sheets for Ball's can manufacturing facilities, demonstrating the industry's focus on securing sustainable supply chains. These collaborations are driving innovation in lightweight materials, enhanced coating technologies, and improved recycling processes. The industry is also witnessing increased investment in research and development to create more sustainable and cost-effective aerosol packaging solutions while maintaining the inherent benefits of metal packaging such as durability, preservation qualities, and infinite recyclability.

Metal Packaging Market Trends

Growing Demand for Metal Drums and IBCs for Liquid Transportation

The increasing demand for metal drums and Intermediate Bulk Containers (IBCs) is primarily driven by their exceptional durability and protection capabilities in liquid transportation. Metal containers, particularly those composed of steel and aluminum, provide superior durability and protection, making them the preferred containers for industries that prioritize product integrity. The packaging of industrial lubricants, oils, and fluids has undergone significant changes over the years due to fluctuations in material availability and rising costs, while packaging components and functional design advancements have contributed to this evolution. Additionally, sustainability has become an increasingly critical aspect of lubricant packaging as the industry prioritizes environmentally responsible practices.

Steel drums are particularly valued for their effectiveness in storing low-viscosity fluids and hazardous chemicals used in the oil industry, offering advantages over plastic alternatives. These containers operate effectively across wide ranges of temperature, humidity, and pressure while preserving structural integrity in the presence of heat and flame without leaking or spilling. Steel drums in the retrieving type offer optimal protection against high-temperature fire when used in conjunction with an effective fire suppression system. Some lubricants naturally absorb moisture from the air, and some plastics have notable air permeability rates, making the storage of these lubricants in plastic containers challenging since the absorbed moisture may shorten the fluid's useful life.

Understand The Key Trends Shaping This Market

Download PDF

Innovation in Metal Packaging for Storage of Hazardous Materials

Metal packaging has emerged as an ideal solution for hazardous material storage due to its durability and resistance against external forces. Metal drums provide superior protection from impact puncture and are resistant to ultraviolet (UV) radiation, making them suitable for outdoor storage. Manufacturers of such material packaging provide various solutions for hazardous chemicals such as IBCs and drums, with continuous innovation driving improvements in safety and efficiency. The risk of spillage, explosion, and corrosion is reduced due to the efficient encapsulation of chemical products, while hazardous material packaging offers a protective solution extensively used in the chemical and pharmaceutical industries.

According to Royal Chemical, steel storage containers demonstrate superior durability with a lifespan of many years, offering more suitable hygienic properties than other options and being highly preferred for all shipping types, including air, sea, and rail. In March 2023, SCHÜTZ Container Systems expanded its steel drum plant in Houston, USA, to produce open-head steel drums, adding billions more cans annually to existing capacity. Additionally, in January 2023, Nestlé launched the DRS packaging with stainless steel in Germany, integrating with the Deposit Return Scheme, demonstrating the industry's commitment to innovation and sustainability in hazardous material storage solutions.

Growing Demand for Aerosol Cans Across End-use Industries

The aerosol can segment holds a substantial share in the metal packaging industry, with these containers using compressed gas to propel products in spray or mist form. The demand for aerosol cans has been growing steadily due to the increasing demand for convenience products, as they can contain products and propellants under pressure that can be dispensed as spray, mist, or foam. Standard products include insecticides, cooking sprays, solvents, and paints, with most aerosol cans made of recyclable steel or aluminum that can be efficiently handled as scrap metal, offering easy-to-use and cost-effective packaging solutions.

Recent innovations and sustainability initiatives have further driven market growth. For instance, in January 2023, Ball Corporation launched a new lightweight aerosol can designed to reduce its carbon footprint, with internal life cycle analysis reporting that the new cans carry a 50% lower carbon footprint than standard cans. Additionally, according to AEROBAL (Aluminium Aerosol Container Manufacturers), its members' output of aluminum aerosols increased by 5.5% during the first half of 2022 to reach 3 billion units, with end-use segments such as pharmaceuticals, hairspray, household products, and deodorants showing significant growth rates of 9%, 34%, 15%, and 1.2% respectively.

High Demand for Beverage Cans for Alcoholic Beverages Mainly Beer

The beverage industry has witnessed a significant shift toward metal can packaging, particularly in the alcoholic beverages sector, driven by consumer preferences and sustainability considerations. According to The World Counts data, the world's beer and soda consumption uses approximately 180 billion aluminum beverage cans annually, equivalent to 6,700 cans every second, enough to go around the planet every 17 hours. This tremendous volume reflects the growing preference for metal can packaging in the beverage industry, particularly for alcoholic beverages like beer, which benefit from the superior preservation properties and convenience of aluminum cans.

Recent industry developments further demonstrate this trend's strength. In May 2023, Jack Daniel's introduced its iconic Jack Daniel's & Coca-Cola cocktail for the first time in the United States as a ready-to-drink (RTD) premixed cocktail option in 12-oz beverage cans. Additionally, Red Bull, one of the most popular beverage brands in the United States, controlling about 39.5% of the market, reported sales of 12.10 billion cans in 2023, surpassing the previous year's count of approximately 11.60 billion. These developments highlight the growing consumer acceptance and industry adoption of metal can packaging for both alcoholic and non-alcoholic beverages, driven by factors such as convenience, sustainability, and product protection.

Segment Analysis: By Material

Aluminum Segment in Metal Cans Market

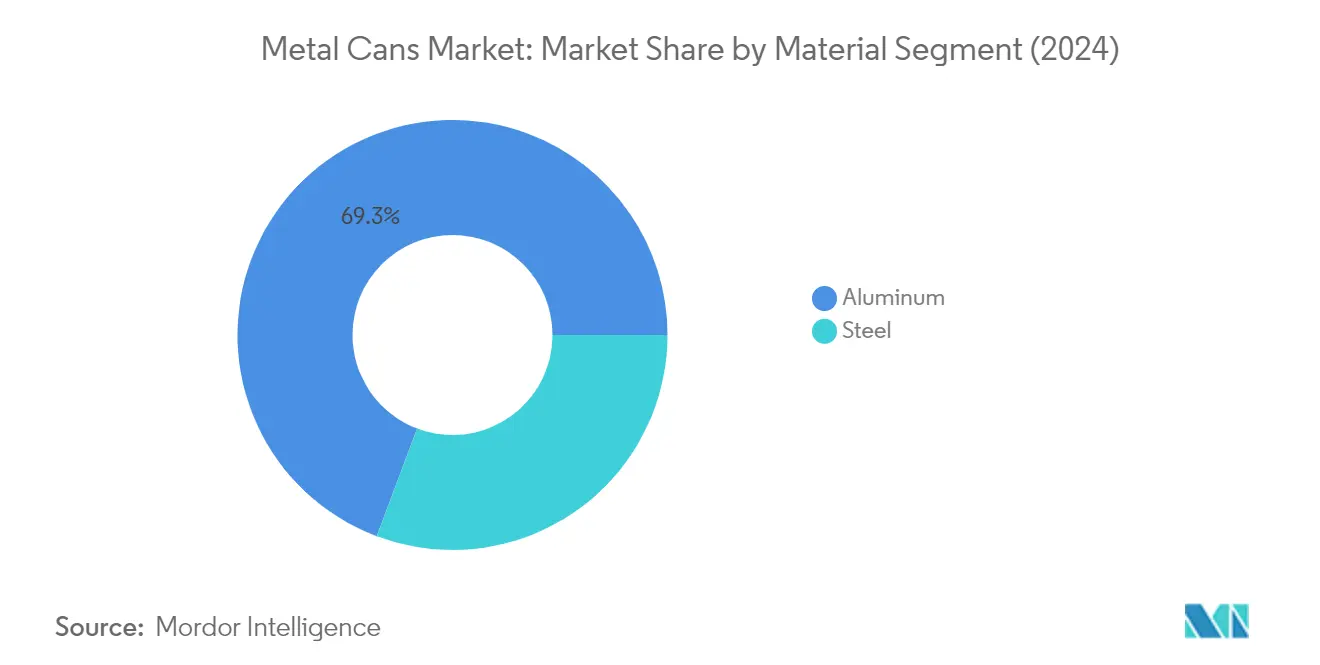

The aluminum packaging segment dominates the metal cans market, commanding approximately 69% market share in 2024, driven by its superior properties in preserving product quality and extending shelf life. Aluminum packaging offers long-term food quality preservation benefits and nearly 100% protection against light, oxygen, moisture, and other contaminants. The material's rust and corrosion-resistant properties provide one of the longest shelf lives of any metal packaging option. The segment is experiencing robust growth with a projected growth rate of around 4% from 2024-2029, primarily due to increasing applications in the food and beverage industry, where both manufacturers and consumers recognize the benefits of aluminum packaging. Companies are investing heavily in aluminum can manufacturing facilities and recycling infrastructure to meet the growing demand, particularly in the beverage can sector where aluminum cans are becoming increasingly popular for both alcoholic and non-alcoholic drinks.

Steel Segment in Metal Cans Market

The steel packaging segment maintains a significant presence in the metal cans market, particularly in food packaging applications where its barrier properties and durability are highly valued. Steel packaging provides 100% barrier protection and is among the most tamper-evident metal container materials, keeping products safe from light exposure, oxidation, extreme temperature changes, and contamination. These materials effectively protect the product's flavor, appearance, and quality throughout the supply chain from factory to consumer. Steel's relatively higher thermal conductivity allows canned beverages to cool faster and more efficiently than glass and plastic bottles. The material's ability to be placed on pallets and stacked high without damaging the package or contents has made it particularly popular in industrial and bulk packaging applications, reducing storage and transportation costs while maintaining product integrity.

Segment Analysis: By Product

2-Piece Segment in Metal Cans Market

The 2-piece segment dominates the global metal cans market, commanding approximately 66% of the total market share in 2024. This significant market position is primarily driven by the segment's superior advantages in terms of manufacturing efficiency and product quality. The 2-piece cans have been gaining substantial momentum in recent years as they are increasingly replacing three-piece cans to reduce environmental pollution created by the extra material required by the latter. The body of these cans does not have any side seams, and there is no seam from the top to the bottom of the can, making them tightly close with less raw material consumption. The growing environmental awareness across the globe has led businesses to gravitate toward 2-piece metal packaging, as they offer enhanced sustainability benefits while maintaining structural integrity.

3-Piece Segment in Metal Cans Market

The 3-piece segment continues to maintain its presence in the metal cans market, offering specific advantages for certain applications despite the growing popularity of 2-piece cans. These cans are particularly valued in applications where customization and flexibility in can sizes are required. The 3-piece construction method allows manufacturers to produce cans of varying heights using the same diameter tooling, providing cost-effective solutions for diverse packaging needs. The segment maintains its relevance in specialized applications such as industrial packaging, certain food products, and aerosol cans where the traditional 3-piece construction offers specific advantages in terms of production flexibility and customization capabilities.

Segment Analysis: By End-User

Chemicals and Petrochemicals Segment in Industrial Metal Packaging Market

The chemicals and petrochemicals segment dominates the industrial metal packaging market, commanding approximately 33% of the total market share in 2024. This significant market position is attributed to the sector's extensive use of metal container solutions for storing and transporting various chemical products safely. The segment's prominence is driven by stringent safety regulations requiring robust packaging solutions for hazardous materials, the growing chemical manufacturing sector globally, and the increasing demand for secure transportation of chemical products. Metal packaging's inherent properties, such as durability, chemical resistance, and ability to withstand extreme conditions, make it particularly suitable for chemical and petrochemical applications, further solidifying its position as the leading end-user segment in the market.

Food and Beverage Segment in Industrial Metal Packaging Market

The food and beverage segment is emerging as the fastest-growing end-user segment in the industrial metal packaging market, projected to grow at approximately 3.4% during 2024-2029. This growth is primarily driven by the increasing demand for sustainable packaging solutions, growing awareness about food safety, and the rising preference for metal food packaging in the beverage industry. The segment's expansion is further supported by innovations in metal packaging technology, including advanced coating solutions and improved barrier properties that enhance product shelf life. Additionally, the growing trend towards ready-to-eat foods and beverages, coupled with the rising adoption of metal food packaging in emerging economies, continues to fuel the segment's growth trajectory.

Remaining Segments in Industrial Metal Packaging Market End-User Segmentation

The industrial metal packaging market encompasses several other significant end-user segments, including lubricants, grease, and oils; pharmaceuticals; paints, coatings, and varnishes; and other miscellaneous applications. The lubricants, grease, and oils segment benefits from the automotive and industrial machinery sectors' growth, while the pharmaceutical segment is driven by stringent quality requirements and the need for contamination-free packaging. The paints, coatings, and varnishes segment relies on metal packaging for its durability and chemical resistance properties. Each of these segments contributes uniquely to the market's diversity and overall growth, with specific requirements driving innovation and development in metal packaging solutions.

Metal Packaging Market Geography Segment Analysis

Metal Packaging Market in North America

The North American metal packaging market demonstrates robust development across various sectors, particularly in industrial packaging and metal cans. The United States and Canada form the core markets in this region, with each country showing distinct growth patterns influenced by their industrial base and consumer preferences. The region's metal packaging market is characterized by significant technological advancements in packaging solutions, a strong emphasis on sustainability initiatives, and increasing demand from key end-user industries such as food and beverage, chemicals, and automotive sectors.

Metal Packaging Market in United States

The United States dominates the North American metal packaging industry, driven by its extensive industrial base and sophisticated packaging requirements. Consumer preferences, such as small size and multi-pack packaging formats, contribute significantly to market growth. The country's focus on sustainability and recyclability has made metal packaging a preferred choice for various industries. The United States accounts for approximately 85% of the North American metal packaging market in 2024, reflecting its position as the region's primary market driver. The market benefits from continuous innovations in packaging design, a strong presence of major manufacturers, and growing demand from the beverage and industrial sectors.

Metal Packaging Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 3% during 2024-2029. The country's metal packaging sector is experiencing significant expansion driven by increasing industrial activities and growing environmental consciousness. Canada's market growth is supported by strong government initiatives promoting sustainable packaging solutions, rising demand from the food and beverage industry, and expanding industrial applications. The country's focus on innovative packaging solutions and increasing adoption of metal packaging in various end-user industries continues to drive market expansion.

Metal Packaging Market in Europe

The European metal packaging market showcases a diverse landscape across multiple countries, each contributing uniquely to the region's overall market dynamics. The market encompasses major economies, including the United Kingdom, Germany, France, Italy, Spain, and the Benelux region, with each country demonstrating distinct growth patterns and market characteristics. The region's metal packaging market is driven by strong environmental regulations, an increasing focus on sustainable packaging solutions, and growing demand from various end-user industries.

Metal Packaging Market in United Kingdom

The United Kingdom stands as the largest metal packaging market in Europe, characterized by its advanced manufacturing capabilities and strong focus on sustainable packaging solutions. The country's market is driven by robust demand from the food and beverage sector, industrial applications, and growing environmental consciousness among consumers. The United Kingdom holds approximately 25% of the European metal packaging market share in 2024, establishing its position as a key player in the region's packaging industry.

Metal Packaging Market in Italy

Italy emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 4% during 2024-2029. The country's metal packaging industry is experiencing significant expansion driven by increasing industrial activities, growing demand from the food and beverage sector, and rising adoption of sustainable packaging solutions. Italy's market demonstrates strong potential for growth, supported by technological advancements in packaging manufacturing and increasing environmental awareness among consumers.

Metal Packaging Market in Asia-Pacific

The Asia-Pacific metal packaging market represents a dynamic and rapidly evolving landscape, encompassing major economies such as China, India, and Japan. The region's market is characterized by increasing industrialization, a growing urban population, and rising demand for packaged products. Each country in the region contributes uniquely to the market's growth, driven by their respective industrial developments and consumer preferences.

Metal Packaging Market in China

China dominates the Asia-Pacific metal packaging market, establishing itself as the region's largest market. The country's market leadership is driven by its extensive manufacturing base, robust industrial sector, and growing demand from various end-user industries. China's metal packaging industry benefits from continuous technological advancements, increasing adoption of sustainable packaging solutions, and strong government support for industrial development.

Metal Packaging Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, demonstrating remarkable growth potential in the metal packaging sector. The country's market expansion is driven by rapid industrialization, increasing urbanization, and growing demand from various end-user industries. India's metal packaging industry benefits from government initiatives promoting manufacturing activities, rising environmental consciousness, and increasing adoption of modern packaging solutions.

Metal Packaging Market in Latin America

The Latin American metal packaging market demonstrates significant potential across Argentina, Brazil, and Mexico. The region's market is characterized by increasing industrial activities, growing urbanization, and rising demand for sustainable packaging solutions. Brazil emerges as the largest market in the region, while Mexico shows the fastest growth rate, driven by its expanding industrial base and increasing foreign investments in manufacturing sectors.

Metal Packaging Market in Middle East & Africa

The Middle East & Africa metal packaging market encompasses diverse economies, including the United Arab Emirates, Saudi Arabia, and South Africa. The region's market is driven by increasing industrialization, growing demand from the oil and gas sector, and rising adoption of modern packaging solutions. Saudi Arabia represents the largest market in the region, while the United Arab Emirates demonstrates the fastest growth rate, supported by its robust industrial development and strategic location as a major trading hub.

Get Analysis on Important Geographic Markets

Download PDF

Metal Packaging Industry Overview

Top Companies in Metal Packaging Market

The metal packaging market features established global leaders like Ball Corporation, Crown Holdings, Ardagh Metal Packaging, Silgan Holdings, and CCL Container, who are driving innovation across the industry. These metal packaging companies are increasingly focused on developing sustainable packaging solutions, including lightweight designs and enhanced recyclability features to address growing environmental concerns. Strategic investments in advanced manufacturing facilities and digital technologies are enabling improved production efficiency and quality control. Market leaders are expanding their geographical presence through greenfield investments and strategic acquisitions, particularly in emerging markets across Asia-Pacific and Latin America. Product innovation efforts are centered on developing smart packaging solutions, enhanced barrier properties, and improved convenience features like easy-open ends and resealable closures, while operational agility is being achieved through automation and Industry 4.0 initiatives.

Consolidated Market with Strong Regional Players

The metal packaging industry exhibits a relatively consolidated structure dominated by large multinational corporations with integrated operations spanning multiple regions and product segments. These major players possess significant advantages in terms of economies of scale, technological capabilities, and established relationships with key customers in the beverage can, food, and industrial sectors. Regional specialists maintain strong positions in specific market segments or geographical areas by leveraging their local knowledge, customer relationships, and specialized product offerings. The market has witnessed ongoing consolidation through strategic acquisitions, particularly in emerging markets where global players seek to establish or strengthen their presence.

The competitive dynamics are characterized by a mix of global conglomerates and specialized manufacturers, with the former typically leading in beverage can and food packaging, while the latter often focus on industrial packaging segments. Merger and acquisition activity remains robust, driven by the need to achieve operational synergies, expand product portfolios, and enter new geographical markets. Companies are increasingly pursuing vertical integration strategies to secure raw material supply and enhance control over the value chain, while also investing in recycling infrastructure to support circular economy initiatives.

Innovation and Sustainability Drive Future Success

Success in the metal packaging industry increasingly depends on companies' ability to align with sustainability trends while maintaining cost competitiveness and operational efficiency. Incumbent players must focus on developing innovative solutions that address environmental concerns while meeting evolving customer requirements for convenience and functionality. Investment in research and development capabilities, particularly in areas such as material science and smart packaging technologies, will be crucial for maintaining competitive advantage. Companies must also strengthen their recycling infrastructure and circular economy initiatives to address growing regulatory pressure and consumer awareness regarding environmental impact.

Market contenders can gain ground by focusing on specialized market segments or geographical regions where they can build strong customer relationships and differentiate through customized solutions. Success factors include developing efficient distribution networks, investing in advanced manufacturing capabilities, and building strategic partnerships across the value chain. The industry faces increasing pressure from alternative packaging materials, particularly in certain end-use segments, necessitating continuous innovation in product design and functionality. Regulatory requirements regarding recycling content and environmental impact are becoming more stringent, making sustainability initiatives and compliance capabilities critical success factors for all market participants.

Metal Packaging Market Leaders

-

Ardagh Metal Packaging SA (Ardagh Group SA)

-

Ball Corporation

-

Crown Holdings, Inc.

-

Can-Pack S.A.

-

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Metal Packaging Market News

- July 2024: AkzoNobel launched Securshield 500, a new range of metal packaging coatings for the food can manufacturing industry. This next-generation product line is free from bisphenols (BPXni*) and PVC, supporting the metal packaging industry's transition toward more sustainable solutions. The introduction of Securshield 500 demonstrates AkzoNobel's commitment to developing environmentally friendly alternatives for food packaging manufacturers.

- February 2024: Hart Print, a subsidiary of Ardagh Metal Packaging that digitally prints aluminum cans, expanded its presence in the United States by opening its third production facility in Maryland. To meet the region's demand, the company aims to increase its annual printing capacity by at least 100 million cans.

- October 2023: Ball Aluminum Cups and Denver Arts & Venues announced the installation of a reverse vending machine, RVM, in Red Rocks Amphitheatre's Top Plaza to improve aluminum recycling at the venue. RVM aims to increase recycling rates at Red Rocks and inform consumers about the benefits of using aluminum.

Metal Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Geopolitical Scenario on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price Offered by Canned Food and Beverage

-

5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions

6. MARKET SEGMENTATION

-

6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

-

6.2 By Product Type

- 6.2.1 Cans

- 6.2.1.1 Food Cans

- 6.2.1.2 Beverage Cans

- 6.2.1.3 Aerosol Cans

- 6.2.2 Bulk Containers

- 6.2.3 Shipping Barrels and Drums

- 6.2.4 Caps and Closures

-

6.3 By End-user Industry

- 6.3.1 Beverage

- 6.3.2 Food

- 6.3.3 Cosmetics and Personal Care

- 6.3.4 Household

- 6.3.5 Paints and Varnishes

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Italy

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 South Korea

- 6.4.3.5 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Argentina

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

- 7.1.2 Ball Corporation

- 7.1.3 Crown Holdings Inc.

- 7.1.4 CANPACK SA (CANPACK Group)

- 7.1.5 Silgan Holdings Inc.

- 7.1.6 Greif Inc.

- 7.1.7 TUBEX Packaging GmbH

- 7.1.8 Mauser Packaging Solutions

- 7.1.9 Nampak Limited

- 7.1.10 Colep Packaging

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia-Pacific'. Rest of Europe, Rest of Asia-Pacific, Rest of Latin America, and Rest of Middle East and Africa countries are considered in the final report.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Metal Packaging Industry Segmentation

Metal packaging is a long-lasting industrial and consumer packaging solution comprised mostly of two key materials, i.e., steel and aluminum. The scope of the metal packaging market is limited to B2B demand. Steel and aluminum packages have outstanding qualities like durability, flexibility, and cost-effectiveness, providing various advantages over other packaging solutions for specific industrial applications. Aluminum is a reasonably simple metal to sterilize for use in packaging. Due to its superior barrier protection and strength, it is an excellent choice for packing materials.

The metal packaging market is segmented by material type (steel and aluminum), product type (cans [food cans, beverage cans, and aerosol cans], bulk containers, shipping barrels and drums, caps and closures, and other product types), end-user industry (beverage, food, cosmetic and personal care, household, paints and varnishes, and other end-user industries), and Geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Spain, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material Type | Aluminum | ||

| Steel | |||

| By Product Type | Cans | Food Cans | |

| Beverage Cans | |||

| Aerosol Cans | |||

| Bulk Containers | |||

| Shipping Barrels and Drums | |||

| Caps and Closures | |||

| By End-user Industry | Beverage | ||

| Food | |||

| Cosmetics and Personal Care | |||

| Household | |||

| Paints and Varnishes | |||

| By Geography*** | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Asia | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Latin America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

Need A Different Region or Segment?

Customize Now

Metal Packaging Market Research FAQs

How big is the Metal Packaging Market?

The Metal Packaging Market size is worth USD 159.75 billion in 2025, growing at an 3.54% CAGR and is forecast to hit USD 190.10 billion by 2030.

What is the current Metal Packaging Market size?

In 2025, the Metal Packaging Market size is expected to reach USD 159.75 billion.

Which is the fastest growing region in Metal Packaging Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Metal Packaging Market?

In 2025, the Asia Pacific accounts for the largest market share in Metal Packaging Market.

What years does this Metal Packaging Market cover, and what was the market size in 2024?

In 2024, the Metal Packaging Market size was estimated at USD 154.09 billion. The report covers the Metal Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Metal Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Metal Packaging Market Research

Mordor Intelligence provides a comprehensive analysis of the metal packaging market. We leverage extensive expertise in industrial metal packaging research and consulting. Our detailed report examines the full range of metal container solutions, including metal tubes, metal cans, and metal drums. The analysis covers crucial segments such as food cans, beverage cans, and aerosol packaging. It also explores innovations in metal bottles and metal caps. Our research methodology includes both tinplate packaging and aluminum packaging sectors. Detailed insights are available in an easy-to-read report PDF format for download.

The report offers stakeholders vital intelligence on metal packaging market trends and emerging opportunities across the steel packaging industry. We provide an in-depth analysis of metal closures, metal jars, and rigid metal packaging segments. This supports strategic decision-making for manufacturers, suppliers, and investors. The study examines industrial metal containers and metal food packaging applications, while tracking developments in tin packaging technologies. Our comprehensive coverage of the metal packaging industry includes detailed analysis of beverage can markets and aluminum packaging industry dynamics. This ensures stakeholders gain actionable insights for sustainable growth strategies.