Market Size of Metal Implants and Medical Alloys Industry

| Study Period | 2019 - 2029 |

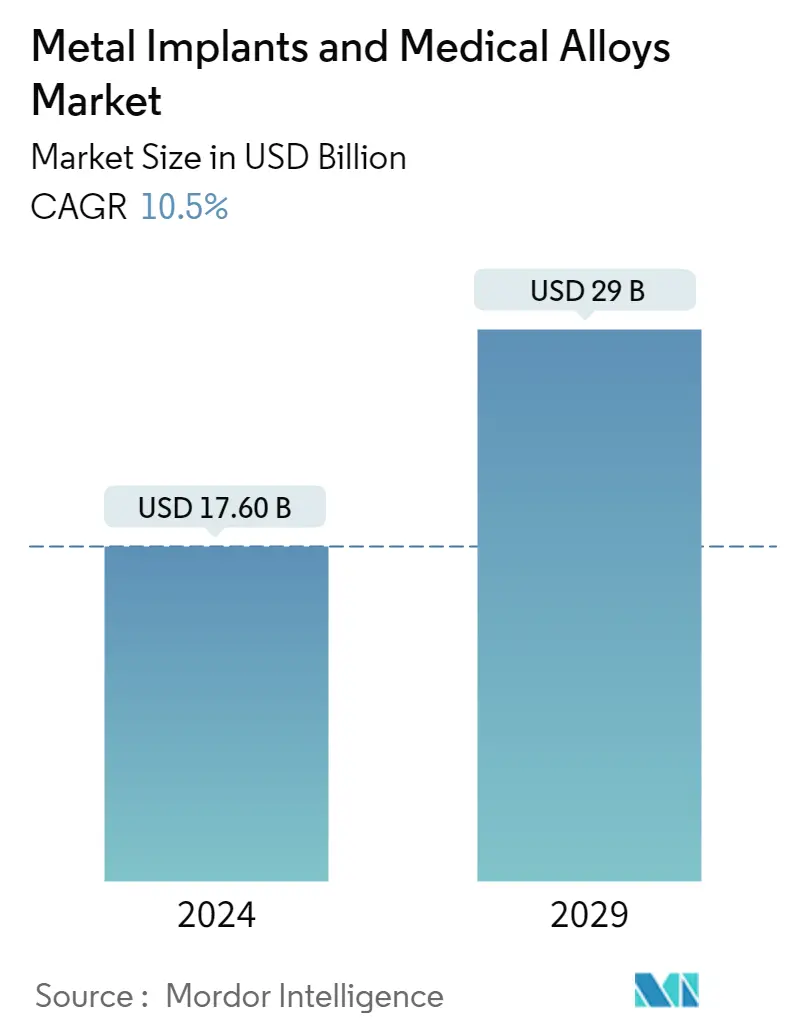

| Market Size (2024) | USD 17.60 Billion |

| Market Size (2029) | USD 29.00 Billion |

| CAGR (2024 - 2029) | 10.50 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Metal Implants and Medical Alloys Market Analysis

The Metal Implants and Medical Alloys Market size is estimated at USD 17.60 billion in 2024, and is expected to reach USD 29 billion by 2029, growing at a CAGR of 10.5% during the forecast period (2024-2029).

The emergence of the COVID-19 pandemic impacted the growth of the metal implants market, as the healthcare industry is still coping with the massive disruption in the supply chain. As a result, a massive shortage is still being experienced in medical devices in various countries. For instance, the study published International Dental Journal in April 2022 suggested that the number of outpatients decreased, and the proportion of emergency cases increased during the epidemic period.

Additionally, according to a study published in the British Journal of Surgery, in May 2021, based on 12 weeks of major hospital services disruption due to COVID-19, approximately 28.4 million elective surgeries worldwide will be canceled or postponed by 2020. Thus, the decline in surgical procedures and outpatient services hampered the market growth during the COVID-19 pandemic. However, since the restrictions were lifted, the industry has been recovering well. Over the last two years, the market recovery has been led by the high prevalence of orthopedic diseases, new product launches, and increased demand for metal implants and medical alloys.

The rising prevalence of degenerative joint diseases and the growing geriatric population are driving the growth of metal implants and the medical alloys market. For instance, according to the study published in Rheumatology International in May 2021, between 1980 and 2019, there were 460 cases of RA per 100,000 people worldwide, and people over the age of 60 will account for more than 20% of the world's population by 2050 which means the number of osteoarthritis sufferers will reach 130 million. The growing prevalence of arthritis and the increasing burden of arthritis conditions will increase the requirement for metal implants and medical alloys and hence are expected to boost the market growth.

Furthermore, growing technological advancement in metal implants is expected to support the growth of the market. For instance, in March 2022, Stryker presented a new implant material, the Klassic Knee implant with Aurum Technology, at Utah-based Total Joint Orthopedics Inc. (TJO). Aurum, a revolutionary implant coating method, is being unveiled to the orthopedic community at the American Academy of Orthopaedic Surgeons (AAOS). Thus, all the above-mentioned factors are expected to boost the market growth over the forest period. However, the high cost of the implant and regulatory issues may restrain the market growth over the forest period.

Metal Implants and Medical Alloys Industry Segmentation

As per the scope of the report, the metal implant is a device that is used to replace a biological structure that has been damaged due to cartilage disorders, trauma, or bone disorders. The metal implants and medical alloys market is segmented by type (cobalt chrome, stainless steel, titanium, and other types), application (orthopedic, dental, spinal fusion, craniofacial, stent, others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above-mentioned segments.

| By Type | |

| Cobalt Chrome | |

| Stainless Steel | |

| Titanium | |

| Other Types |

| By Application | |

| Orthopedic | |

| Dental | |

| Spinal Fusion | |

| Craniofacial | |

| Stent | |

| Other Applications |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Metal Implants and Medical Alloys Market Size Summary

The metal implants and medical alloys market is poised for significant growth over the forecast period, driven by the increasing prevalence of orthopedic diseases and the expanding geriatric population. The market is recovering from the disruptions caused by the COVID-19 pandemic, which had previously led to a decline in surgical procedures and outpatient services. The recovery is supported by new product launches and technological advancements in implant materials, such as Stryker's Klassic Knee implant with Aurum Technology. Despite challenges like high costs and regulatory issues, the market is expected to benefit from the rising demand for metal implants in orthopedic and dental applications, fueled by the growing burden of degenerative joint diseases and dental problems among the elderly.

North America is anticipated to hold a significant share of the global market, driven by the increasing geriatric population and the high prevalence of chronic diseases. The region's market growth is further supported by ongoing research and development activities, such as the approval of 3D-printed medical implants in Canada. Key market players, including Carpenter Technology Corporation, Royal DSM, and Johnson Matthey PLC, are actively contributing to the competitive landscape. The market's expansion is also bolstered by product innovations, such as OssDsign's patient-specific cranial implant and OSSIOfiber's intelligent bone regeneration technology, which are expected to enhance patient outcomes and drive adoption.

Metal Implants and Medical Alloys Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Growing Elderly Population Increases the Prevalence of Orthopedic Disorders

-

1.2.2 Technologically Advanced Metal Implant Products

-

-

1.3 Market Restraints

-

1.3.1 High Cost of Implants

-

1.3.2 Regulatory Issues for the Approval of Products

-

-

1.4 Porter's Five Force Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD Million)

-

2.1 By Type

-

2.1.1 Cobalt Chrome

-

2.1.2 Stainless Steel

-

2.1.3 Titanium

-

2.1.4 Other Types

-

-

2.2 By Application

-

2.2.1 Orthopedic

-

2.2.2 Dental

-

2.2.3 Spinal Fusion

-

2.2.4 Craniofacial

-

2.2.5 Stent

-

2.2.6 Other Applications

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

2.3.2.4 Italy

-

2.3.2.5 Spain

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 Australia

-

2.3.3.5 South Korea

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Middle East and Africa

-

2.3.4.1 GCC

-

2.3.4.2 South Africa

-

2.3.4.3 Rest of Middle East and Africa

-

-

2.3.5 South America

-

2.3.5.1 Brazil

-

2.3.5.2 Argentina

-

2.3.5.3 Rest of South America

-

-

-

Metal Implants and Medical Alloys Market Size FAQs

How big is the Metal Implants and Medical Alloys Market?

The Metal Implants and Medical Alloys Market size is expected to reach USD 17.60 billion in 2024 and grow at a CAGR of 10.5% to reach USD 29.00 billion by 2029.

What is the current Metal Implants and Medical Alloys Market size?

In 2024, the Metal Implants and Medical Alloys Market size is expected to reach USD 17.60 billion.