Metal Finishing Chemical Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

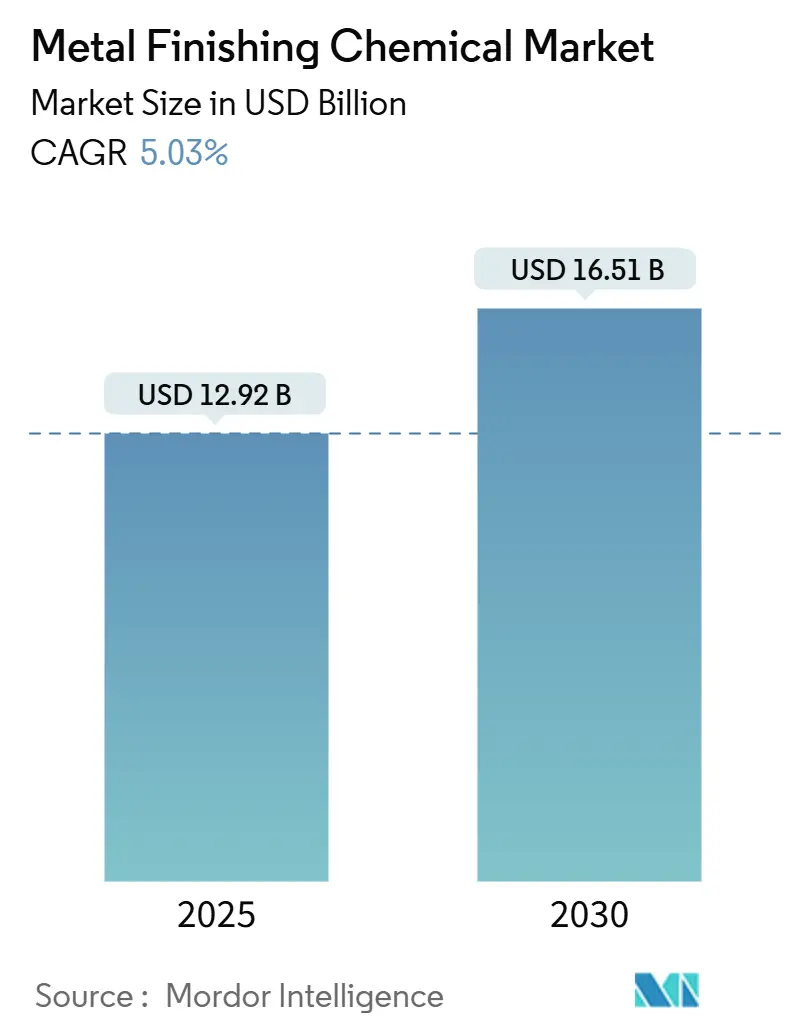

| Market Size (2025) | USD 12.92 Billion |

| Market Size (2030) | USD 16.51 Billion |

| Growth Rate (2025 - 2030) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Metal Finishing Chemical Market Analysis by Mordor Intelligence

The metal finishing chemical market size reached USD 12.92 billion in 2025 and is forecast to climb to USD 16.51 billion by 2030, advancing at a 5.03% CAGR. The metal finishing chemical market is expanding because advanced plating, anodizing, and conversion-coat chemistries enable precision that mechanical finishing cannot match. Growth pivots on four themes: electric-vehicle lightweighting that favors aluminum-intensive architectures, electronics miniaturization requiring sub-micrometer deposit control, aerospace mandates that shift chemistries away from PFAS and hexavalent chromium, and reshoring programs that shorten supply chains for surface-treatment consumables.

Key Report Takeaways

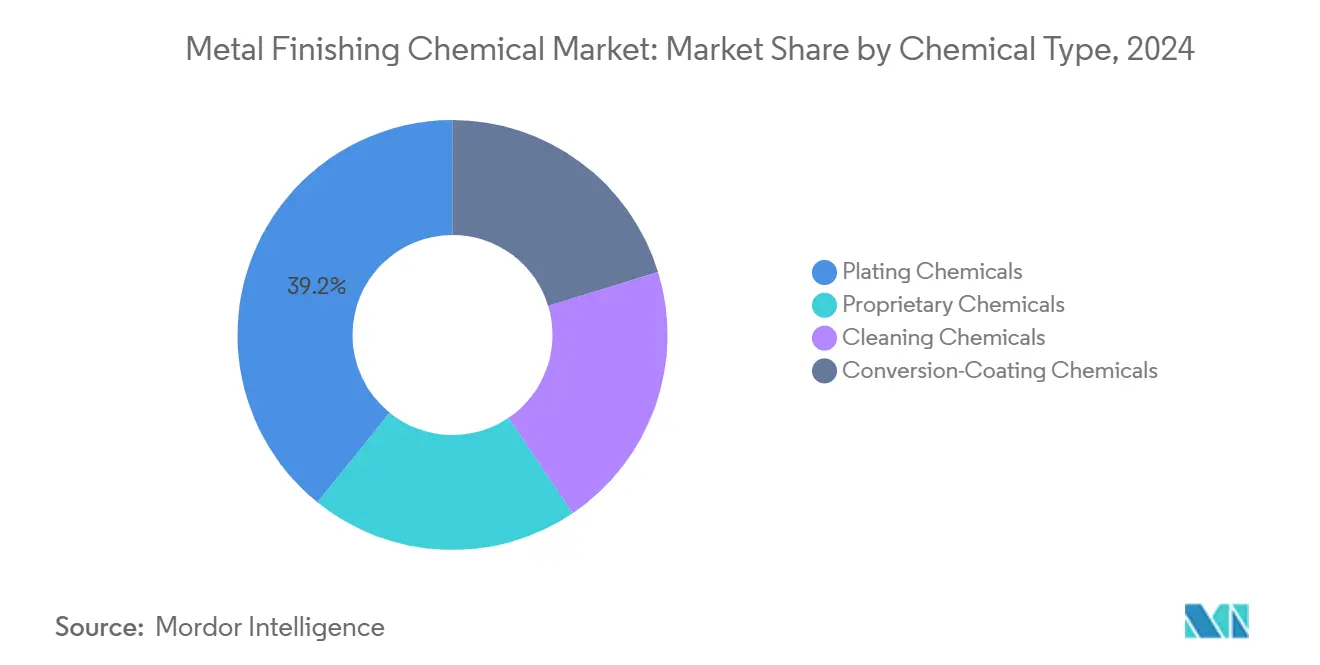

- By chemical type, plating chemicals led with 39.18% of the metal finishing chemical market share in 2024; cleaning chemicals are projected to grow at a 6.18% CAGR to 2030.

- By material, aluminum processing accounted for a 31.26% share of the metal finishing chemical market size in 2024, while nickel is set to expand at 6.42% between 2025-2030.

- By process, electroplating held 42.19% of the metal finishing chemical market in 2024 and is forecast to rise at a 7.09% CAGR through 2030.

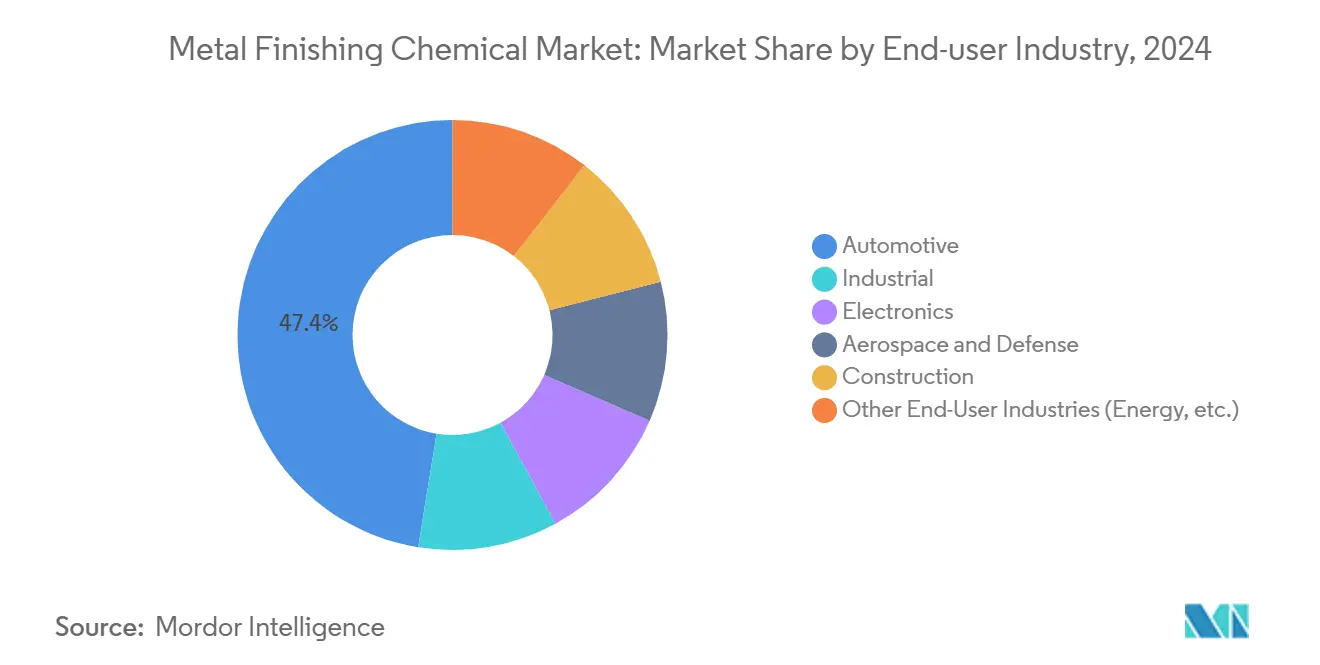

- By end-user, automotive dominated with 47.44% revenue share in 2024; electronics is the fastest-growing segment at 6.81% CAGR.

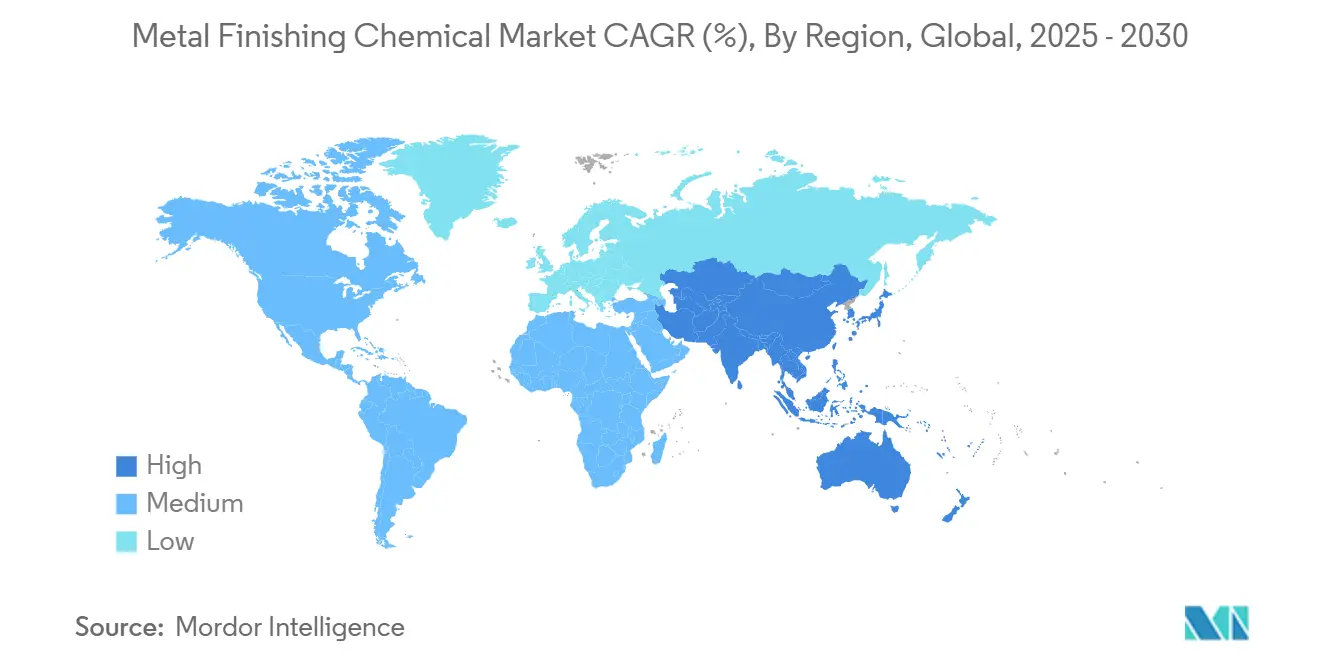

- By geography, Asia-Pacific captured 53.78% of the metal finishing chemical market in 2024 and is advancing at a 7.17% CAGR to 2030.

Global Metal Finishing Chemical Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV lightweighting shifts need higher-performance plating chemistries | +1.2% | Global, with a concentration in China, Europe, and North America | Medium term (2-4 years) |

| Electronics miniaturization requires ultra-thin deposit accuracy | +0.9% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Aerospace OEM PFAS-free mandates accelerate conversion-coat demand | +0.7% | North America and the EU, expanding to global aerospace hubs | Long term (≥ 4 years) |

| Reshoring of metal parts boosts localized chemical demand | +0.5% | North America, with selective European markets | Medium term (2-4 years) |

| Green hydrogen electrolyzer build-out needs specialty nickel baths | +0.4% | EU leading, followed by North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Lightweighting Shifts Needing Higher-Performance Plating Chemistries

Electric-vehicle platforms rely on aluminum and mixed-metal architectures that demand corrosion-resistant conversion coats capable of bonding to recycled alloys. Honda’s USD 15 billion Canadian EV complex and BMW’s battery expansion in Mexico illustrate production realignment that lifts regional chemical demand. Specialized anodizing systems maintain coating integrity on secondary aluminum while complying with weight-reduction goals. At the same time, composite housings such as ARRK Group’s carbon-fiber gearbox shells displace some metal parts, yet hybrid metal-composite interfaces still require niche plating chemistries to mitigate galvanic risk. Continuous model refresh cycles through 2030 support sustained uptake of premium plating formulations, positioning the metal finishing chemical market for steady volume and margin expansion.

Electronics Miniaturization Requiring Ultra-Thin Deposit Accuracy

Shrinking semiconductor nodes have moved interconnect pitches below 10 µm, pushing electroplating baths to deliver sub-100 nm uniformity across wafers. Horizontal wafer-level systems improve through-silicon-via filling, while pulse plating cuts void formation. Cobalt replaces copper in some layers for better electromigration resistance, demanding new additives that stabilize bath chemistry. AI-enabled sensors feed machine-learning models to predict thickness deviations in real time, cutting scrap and reagent use. Fab capital outlays track node migrations, so each lithography transition injects new demand into the metal finishing chemical market for high-purity additives and real-time control packages.

Aerospace OEM PFAS-Free Mandates Accelerate Conversion-Coat Demand

Aerospace primes have moved to eliminate hexavalent chromium and PFAS across airframes. The F-35 program’s switch to chrome-free primers set a precedent for other fleets. Oerlikon’s Balinit C PVD coating gained Airbus approval as a hard-chrome alternative, demonstrating that multi-layer vapor coatings can meet adhesion and fatigue requirements. Fluorozirconate-based anodizing passes 3,000-hour salt-spray tests, validating performance while lowering hazardous-waste costs. Certification cycles are lengthy, but once approved, the chemistries displace legacy baths fleet-wide, adding durable revenue to the metal finishing chemical market.

Reshoring of Metal Parts Boosts Localized Chemical Demand

North American reshoring accelerates as OEMs trade cost for resilience; Metal Solutions Holdings is aggregating 2,000 fabricators to supply local aerospace and defense programs. The U.S. Department of Defense funds finishing-sector upskilling, signaling policy support for domestic capacity. Shorter logistics chains give regional chemical suppliers an edge through rapid onsite service, a factor that strengthens pricing power in the metal finishing chemical market. Consolidated job shops also pool capital to install automated lines that require consistent, high-purity chemistries, raising average spend per line.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of high-performance plastics in e-mobility | -0.8% | Global, with early adoption in European and North American EV markets | Short term (≤ 2 years) |

| 3D-printed net-shape metals lower post-finish chemical volumes | -0.6% | APAC manufacturing hubs, expanding to North America and Europe | Medium term (2-4 years) |

| Tight PFAS and Cr VI bans raise reformulation compliance costs | -0.4% | EU leading, North America following, gradual APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of High-Performance Plastics in E-Mobility

Engineers substitute carbon-fiber and glass-fiber composites for aluminum brackets and housings, trimming 30% weight without post-plating steps. Plastics can integrate decorative texture during molding, erasing the need for chemical etches or electroless plating. Covestro’s low-carbon polycarbonate cuts VOCs and meets thermal-shock standards, reinforcing non-metal adoption. As plastic penetration widens, the addressable portion of the metal finishing chemical market tied to exterior trim and under-hood brackets contracts, pressuring legacy chemistries.

3D-Printed Net-Shape Metals Lower Post-Finish Chemical Volumes

Laser powder bed fusion delivers titanium and Inconel parts with surface roughness under 6 µm; cavitation-abrasive finishing removes alpha-case layers mechanically, bypassing acid dips. Wire-arc additive manufacturing yields near-net-shape components that need only light polishing. Machine-learning algorithms refine scan paths, reducing porosity and eliminating the need for heavy post-plate corrosion barriers. As aerospace and medical buyers qualify printed parts, chemical consumption per unit declines, limiting upside for some metal finishing chemical market segments.

Segment Analysis

By Chemical Type: Demand Diversifies Beyond Traditional Plating

Plating chemicals held a 39.18% share of the metal finishing chemical market in 2024, driven by their indispensable role in electrodeposition for automotive trim, semiconductor bumps, and aerospace fasteners. Cleaning chemicals, although smaller, are the fastest-growing at 6.18% CAGR because chip fabs mandate particle-free substrates before copper damascene steps. Degreasers employing bio-based surfactants meet stringent resistivity thresholds, and hydrogen peroxide blends replace solvent cleaners to cut greenhouse-gas footprints. Proprietary blends now comprise multilayer additive packages that fine-tune deposit brightness and tensile stress for niche alloy systems. Chrome-free conversion-coat solutions capture aerospace share as qualification programs conclude, redirecting revenue from legacy hexavalent products into safer alternatives.

Note: Segment shares of all individual segments available upon report purchase

By Materials: Nickel Gains Momentum Amid Aluminum Dominance

Aluminum finishing products commanded 31.26% of the metal finishing chemical market in 2024, buoyed by EV battery-tray production and architectural cladding demand. Multi-stage anodizing baths yield pore structures suited for dye uptake, expanding decorative options. Yet nickel baths are advancing fastest at 6.42% CAGR as electrolyzer plates and battery current collectors proliferate[1]World Platinum Investment Council Analysts, “Hydrogen Economy to Lift Platinum and Nickel Demand,” World Platinum Investment Council, wpic.org. High-pH sulfamate systems allow thick nickel deposits with low internal stress, critical for hydrogen-evolution efficiency. Copper plating remains steady in printed-circuit fabrication, while zinc-nickel alloys displace cadmium in aerospace hardware.

By Process: Electroplating Retains Dual Supremacy

Electroplating claimed 42.19% of the metal finishing chemical market share in 2024 and posts a 7.09% growth outlook, reflecting its adaptability to everything from micro-bump copper pillars to heavy hard-chrome builds. Automated racks with vision-guided loading squeeze takt times and heighten bath throughput. AI-based predictive dosing halves additive over-use, strengthening environmental compliance. Anodizing grows modestly as architectural projects favor colored finishes, whereas thermal-spray systems fill wear-resistant niches with ceramic-metal blends.

Pulse-reverse power supplies in electroplating reduce porosity in high-aspect-ratio trenches, enabling semiconductor metallization down to 5 nm nodes. Digital twin models simulate ion transport, optimizing throwing power before plant trials. These technology upgrades underpin the process segment’s leadership and deepen customer reliance on advanced formulations, cementing revenues throughout the metal finishing chemical market.

By End-User Industry: Electronics Challenges Automotive Supremacy

Automotive applications delivered 47.44% of 2024 revenue as decorative chrome and zinc-nickel corrosion barriers remained standard. Yet electric drivetrains shift demand toward copper busbar plating and aluminum battery cases, altering chemistry mixes. Electronics is accelerating at 6.81% CAGR as AI chips and advanced packaging ramp volumes that need ultra-pure copper and cobalt electrolytes. Aerospace keeps premium pricing because flight-critical hardware requires high-reliability coatings audited by OEMs.

Industrial machinery and construction contribute a steady baseline demand for galvanized and phosphate finishes, while renewable-energy infrastructure, wind-turbine gearboxes, and hydrogen electrolyzers open high-value niches. As each sector’s requirements diverge, suppliers segment portfolios, supporting multi-application growth across the metal finishing chemical market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated with 53.78% revenue share in 2024, and the metal finishing chemical market size here is rising 7.17% annually. China’s EV build-out, India’s specialty chemical expansion, and South Korea’s chip-foundry investments fuel volume gains. Government incentives for localized semiconductor supply chains spur high-purity plating demand, giving regional suppliers scale advantages.

North America benefits from the Infrastructure Investment and Jobs Act funding and reshoring. U.S. cast-metal demand is projected at USD 37.5 billion by 2032, supporting downstream finishing needs[2]American Foundry Society, “U.S. Metalcasting Forecast,” Castingsource, castingsource.com . Canada’s EV projects and Mexico’s contract manufacturing hubs multiply cross-border chemical flows. Shorter transport routes and on-site technical support strengthen supplier relationships, raising margins within the metal finishing chemical market.

Europe faces strict REACH revisions that ban PFAS and tighten chromium VI allowances. Compliance pressures add cost but also stimulate innovation. DuPont’s chrome-free etchants and ammonia-free plastic metallization lines gain traction, while German tier-ones pilot zirconate sealer systems. Eastern Europe captures capacity migrating from higher-cost Western plants, enlarging its finish-chemical consumption base. As regulators reward sustainable chemistries, premium offerings secure share across the metal finishing chemical market.

Competitive Landscape

The market remains highly consolidated. Technology leadership hinges on developing PFAS-free cleaners and chrome-free conversion coats that match legacy performance. AI-enabled bath monitoring differentiates suppliers able to furnish data dashboards to OEM quality teams. Start-ups focus on hydrogen electrolyzer nickel baths, targeting a premium niche underserved by multinationals.

Metal Finishing Chemical Industry Leaders

-

BASF

-

Dow

-

Henkel AG & Co. KGaA

-

MacDermid Alpha Electronics Solutions

-

MKS Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MKS Inc. (Atotech) opened a Derio, Spain facility, expanding General Metal Finishing capacity and local technical support across Iberia and Southern Europe.

- April 2025: Quaker Houghton acquired Dipsol Chemicals Co., Ltd. for about JPY 23 billion (USD 153 million), adding plating solutions and USD 82 million in revenue in Asia-Pacific.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the metal finishing chemical market as all proprietary or commodity formulations that clean, plate, or convert metallic surfaces, ranging from aqueous degreasers and acid pickles to electroless nickel baths and chromate-free conversion coatings, applied during OEM production and aftermarket refurbishment across automotive, electronics, industrial machinery, aerospace, and construction parts.

Scope exclusion: Equipment such as plating lines, spray booths, or vibratory finishers is not valued inside this chemical market.

Segmentation Overview

- By Chemical Type

- Plating Chemicals

- Proprietary Chemicals

- Cleaning Chemicals

- Conversion-Coating Chemicals

- By Materials

- Aluminum

- Copper

- Zinc

- Nickel

- Chromium

- Other Materials

- By Process

- Anodizing

- Carbonizing

- Electroplating

- Polishing

- Plating

- Thermal or Plasma Spray Coating

- Other Process (Laser, Magnetic-Abrasive, etc.)

- By End-user Industry

- Automotive

- Industrial

- Electronics

- Aerospace and Defense

- Construction

- Other End-User Industries (Energy, etc.)

- By Geography

- Asia-Pacifc

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacifc

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi-structured interviews and surveys with plating job shops, automotive tier-ones, electronics fabricators, and chemical formulators across Asia-Pacific, North America, and Europe allowed us to gauge average bath life, replenishment rates, and regional price spreads. Expert feedback challenged early cost assumptions, leading us to recalibrate cleaning chemical penetration in high-throughput PCB fabrication lines.

Desk Research

Mordor analysts first mapped supply-side footprints through trade data from UN Comtrade, EPA and ECHA substance registers, and industry association briefs such as NASF and the International Electronics Manufacturing Initiative. Company 10-Ks, investor decks, and patent families accessed via Questel helped us link brand portfolios to end-use volumes, while Dow Jones Factiva newsfeeds captured capacity additions or price adjustments in real time. Government statistics on light vehicle builds (OICA), printed circuit board output (IPC), and aircraft deliveries (FAA) anchored demand proxies. The sources cited above illustrate, not exhaust, the wider set reviewed for context, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with production statistics, automobile units, multilayer board square meters, and fabricated metal shipments, which are then converted into chemical demand pools using consumption coefficients validated through supplier roll-ups and channel checks (our light bottom-up pass). Key variables include plating line uptime, average film thickness specs, share of trivalent chromium adoption, and regulatory timelines for PFAS substitution; each series is forecast through multivariate regression blended with scenario analysis for legislation shocks. Where supplier-level data remained opaque, gap factors were assigned and back-tested against historical invoice samples shared confidentially by respondents.

Data Validation & Update Cycle

Outputs pass a two-step analyst review: variance flags versus past editions or external indicators trigger deeper dives, and anomalies are discussed again with industry contacts before sign-off. Reports refresh yearly, with interim tweaks when material events, mergers, plant outages, or policy bans shift the baseline; a fresh pass is executed just before client delivery.

Why Mordor's Metal Finishing Chemical Baseline Commands Reliability

Published estimates often differ because firms pick unique scopes, price points, and refresh cadences.

Below we benchmark current year values and spotlight the research gaps driving divergence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.92 B | Mordor Intelligence | - |

| USD 13.52 B | Global Consultancy A | Uses 2017 base, applies straight-line growth, excludes aftermarket chemical reuse credits |

| USD 13.87 B | Industry Association B | Mixes metal surface treatment fluids with heat treatment salts, inflating totals |

| USD 13.21 B | Trade Journal C | Relies on supplier list prices without adjusting for regional duty rebates |

The comparison shows that when scope creep, outdated baselines, or unvetted price assumptions slip in, totals swing by up to a billion dollars. Mordor's disciplined variable selection, annual refresh, and dual-path validation deliver a balanced, transparent baseline that decision-makers can retrace and reproduce confidently.

Key Questions Answered in the Report

What is the current value of the metal finishing chemical market?

The metal finishing chemical market size is USD 12.92 billion in 2025, with a CAGR of 5.03% toward 2030.

Which chemical type leads the market?

Plating chemicals hold the largest share at 39.18%, reflecting their critical role in electrodeposition across industries.

Why is Asia-Pacific dominant in metal finishing chemicals?

Asia-Pacific hosts the bulk of global electronics and EV production, capturing 53.78% of 2024 revenue and growing 7.17% annually.

How are regulations influencing product development?

Stricter PFAS and chromium VI bans in Europe and North America push suppliers to develop chrome-free conversion coats and fluorine-free cleaners without sacrificing performance.

Which material segment is growing fastest?

Nickel finishes are advancing at 6.42% CAGR due to hydrogen electrolyzer plates and battery collectors that need high-integrity nickel deposits.

Page last updated on: