Metal Bonding Adhesives Market Size

| Study Period | 2019 - 2029 |

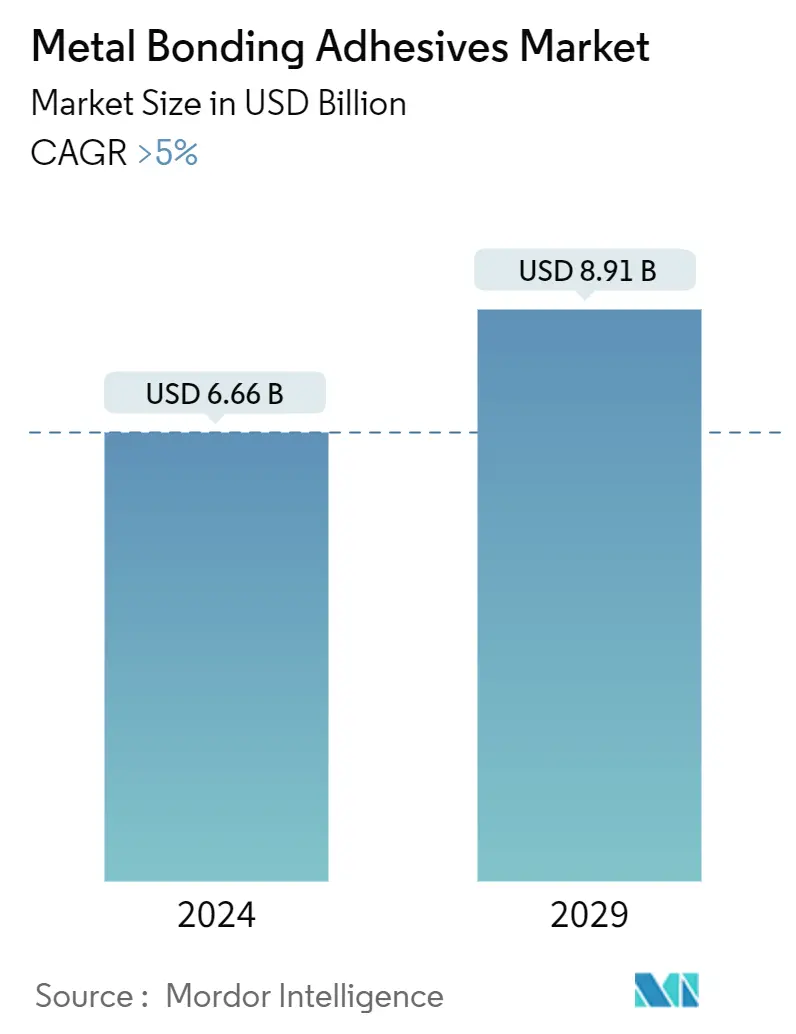

| Market Size (2024) | USD 6.66 Billion |

| Market Size (2029) | USD 8.91 Billion |

| CAGR (2024 - 2029) | > 5.00 % |

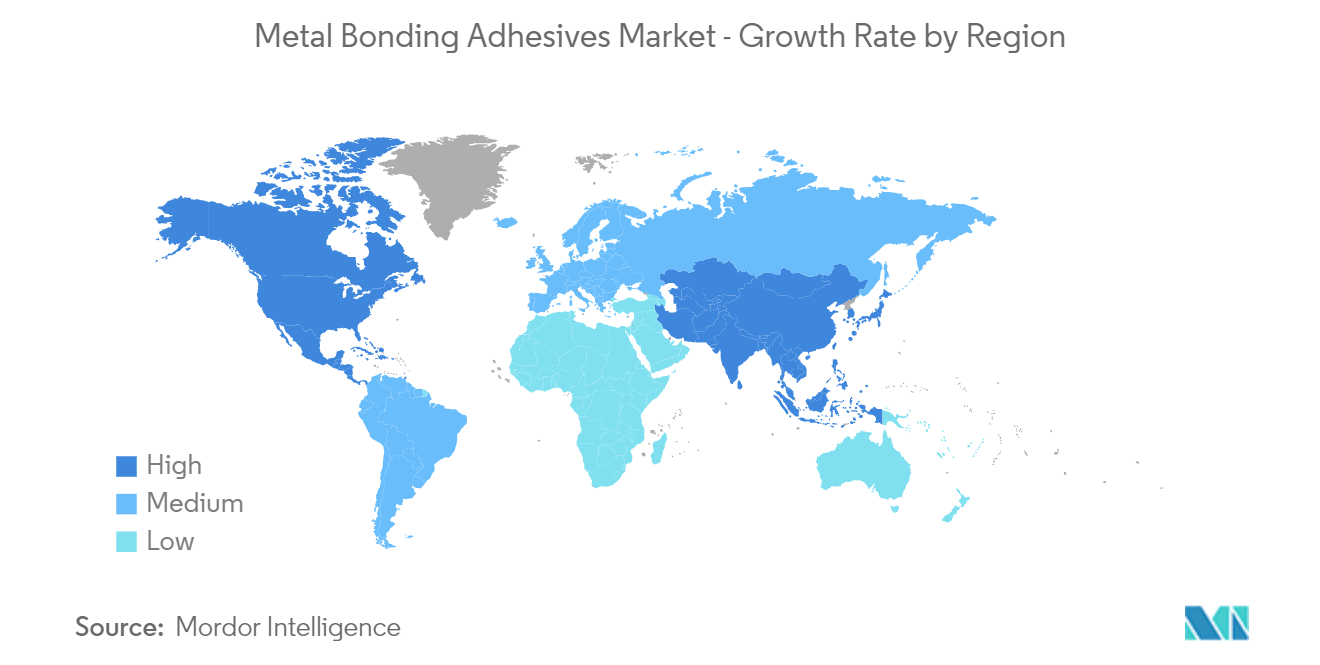

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

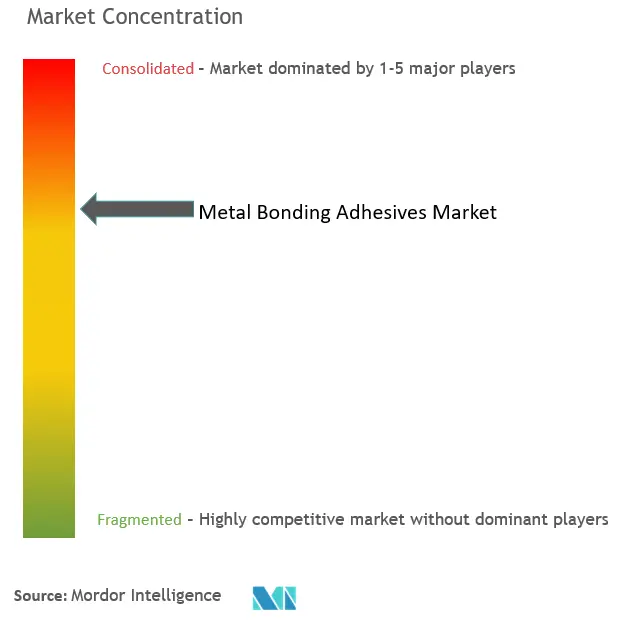

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Metal Bonding Adhesives Market Analysis

The Metal Bonding Adhesives Market size is estimated at USD 6.66 billion in 2024, and is expected to reach USD 8.91 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the metal bonding adhesive market by disrupting the supply chain, causing production to slow down and shut down and an economic downturn. While the initial impact of COVID-19 was negative, the market appears to be on a recovery path during the forecast period.

- Major factors driving the market studied are growing demand from the automotive and transportation industry.

- On the flip side, volatility in raw material prices, due to the rising geopolitical tensions between various nations is hindering the growth of the market.

- Innovation and development of bio-based adhesives to open new opportunities for the market.

- The Asia-Pacific region represents the largest market, and it is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries, such as China, India, and Japan.

Metal Bonding Adhesives Market Trends

Growing Demand from the Automotive and Transportation Industry

- Metal bonding adhesives are widely used in the automotive and transportation industry by OEMs for fabricating chassis, automotive exteriors, panel bonding, frames, and reinforcement of the passenger, as well as heavy vehicles segment. Exterior panels and panel bonding are among the top applications in the automotive segment.

- Furthermore, in the aerospace industry, metal bonding adhesives are specifically designed for maximum durability, high strength, and toughness with temperature resistance designed for their operating environment.

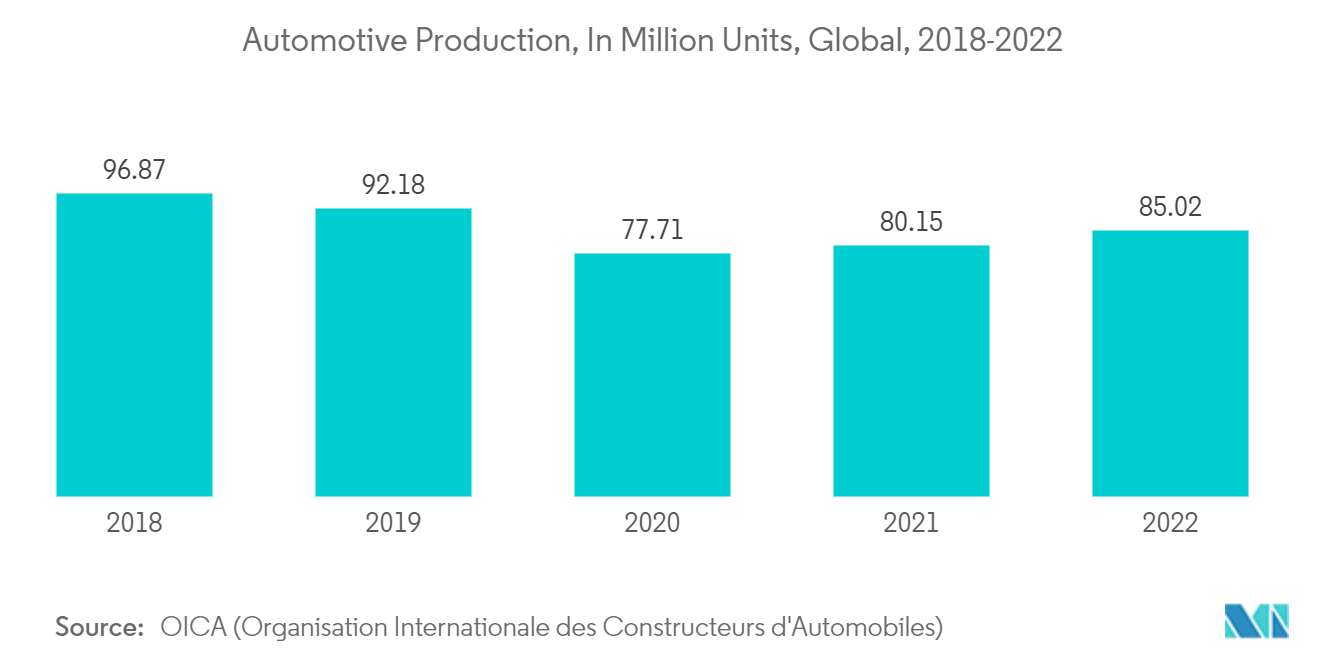

- According to the Organisation Internationale des Constructeurs d’Automobiles (OICA), in 2022, around 85.01 million vehicles were produced across the globe, witnessing a growth rate of 5.99% compared to 80.205 million vehicles in 2021, thereby indicating an increased demand for metal hoses from the automotive industry. In 2022, around 60 million passenger cars were manufactured worldwide, up nearly 7.35% compared to 2021.

- The Asia-Pacific is home to some of the world’s most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the Boeing Commercial Outlook 2023-2042, the demand for new commercial jets by 2042 is expected to reach 42,595 units, valued at USD 8 trillion. The global fleet will nearly double to 48,600 jets by 2042, expanding by 3.5% annually. Airlines will replace about half of the global fleet with new, more fuel-efficient models.

- North America accounts for the largest share with 9,250 deliveries, followed byEurasia and China, with the total deliveries of new airplanes estimated to be 9,645 units by 2042, indicating rising demand from the industry.

- In China, Airbus announced plans in March 2023 to expand production of its best-selling A320 single-aisle jet and boost sales. China is one of the largest markets for European airline manufacturers, and this expansion is expected to significantly grow the metal bonding adhesives market as these adhesives are used in weight reduction and improving strength and fatigue resistance experienced by the aircraft structures.

- Over the forecast period, increasing demand and production of automotive vehicles and aircrafts are likely to drive the market.

The Asia-Pacific Region to Dominate the Market

- The Asia-Pacific metal bonding adhesives market is anticipated to witness significant and fastest growth, owing to the growing demand for technologically advanced consumer electronics and automobile production in China, which holds a significant market share.

- In addition, the relocation of manufacturing hubs due to the accessibility of cost-effective raw materials and labor in India, Thailand, Indonesia, and China, coupled with increasing investments by multinationals in the industrial and electronics sectors and growing competition among market players to hold a manufacturing base in the Asia-Pacific, is the central aspect stimulating the increasing demand for metal bonding adhesives in the region.

- The Chinese automotive manufacturing industry is the largest in the world. The industry witnessed a slight growth in 2022, wherein production and sales increased. A similar trend continued in 2021, with production witnessing a 3% incline in 2022. According to the China Association of Automobile Manufacturers (CAAM), automotive production is expected to grow in the future, with companies like BYD, SAIC Motors, and more increasing their automotive production sales in the fuel-run and electric vehicles segment.

- According to the China Association of Automobile Manufacturers, Chinese automakers are anticipated to report sales of approximately 9.4 million electric vehicles and hybrids in the previous year, up from 6.9 million in 2022. The association further projects a continued increase in sales for 2024, reaching 11.5 million units.

- For Example, China's automotive giant BYD sold over 3 million battery-powered cars in 2023, of which both batteries and gasoline power 1.6 million fully electric vehicles and another 1.4 million hybrids. Together, that is a 62 percent increase over 2022. BYD is also making money, tripling its profit to USD 1.5 billion in the first half of last year, according to BYD.

- According to India Today, 4,108,000 cars were sold in the domestic market in 2023. This was the first time during a calendar year that over 4 million units were sold in the country. In 2022, the industry witnessed sales of 3,792,000 units. In India, major automotive manufacturers, like Maruti, Hyundai, Tata, Honda, and Mahindra, have shut down their production owing to the unsold stock. This is expected to have a substantial negative impact on India's automotive production in the near future.

- China has one of the largest healthcare sectors in the world. Under the 13th Five-Year Plan, the Government of China prioritized health and innovation, which is expected to increase investments in the medical device manufacturing sector during the forecast period. Additionally, due to the COVID-19 outbreak, investment in the healthcare sector has been gradually growing in the country.

- Metal bonding adhesives play a crucial role in modern construction, offering numerous advantages over traditional joining methods like welding, riveting, or bolting.

- China's growth is also fueled by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China’s construction sector is expected to maintain a 6% share of the country’s GDP going into 2025.

- As per Invest India, the construction industry in India is expected to reach USD 1.4 Trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in Indian Construction Sectors.

- Furthermore, South Korean builders' overseas building orders have surpassed 30 billion US dollars for the third consecutive year in 2022, owing to strong demand from Asia, North America, and the Pacific Ocean regions.

- Hence, owing to the factors mentioned above, the demand for metal bonding adhesives in the country has been on the rapid rise in the region.

Metal Bonding Adhesives Industry Overview

The Metal Bonding Adhesives market is partially consolidated in nature. The major players (not in any particular order) include Henkel AG & Co. KGaA, 3M, H.B. Fuller Company., Arkema and Sika AG, among others.

Metal Bonding Adhesives Market Leaders

-

3M

-

H.B. Fuller Company

-

Henkel AG & Co. KGaA

-

Sika AG

-

Arkema

*Disclaimer: Major Players sorted in no particular order

Metal Bonding Adhesives Market News

November 2023: Saint-Gobain launched a new tape product line with technology to enhance the automotive assembly. Norbord Z2000 Acrylic Tape Series is a durable, long-lasting adhesion for automotive exterior bonding on complex surfaces.

October 2023: Saint-Gobain launched a completely new thermal management production line in Kolo, Poland. This facility specializes in thermally conductive silicone gasketing foams- especially for EV battery and powertrain system applications.

January 2023: Shurtape Technologies LLC announces the release of Duck Pro by Shurtape BR Code Scannable Solutions, powered by the BitRip app. Developed in partnership with Nastro Technologies, a tech startup specializing in asset tracking technology, the two companies began developing the product line together in August 2022 after merging their respective expertise in industrial adhesive applications and asset tracking technology.

Metal Bonding Adhesives Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand from the Automotive and Transportation Industry

4.1.2 Increased Consumption from Construction and Infrastructure Sector

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Regulatory Policies

4.2.2 Sustainability Concerns

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size In Value)

5.1 Resin Type

5.1.1 Acrylic

5.1.2 Epoxy

5.1.3 Polyurethane

5.1.4 Silicone

5.1.5 Other Resin Types (Bio-Based Resins, Hybrid, etc.)

5.2 Application

5.2.1 Automotive and Transportation

5.2.2 Aerospace and Defense

5.2.3 Electrical and Electronics

5.2.4 Industrial Assembly

5.2.5 Construction and Infrastructure

5.2.6 Other Applications (Marine, Medical, etc.)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 NORDIC

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Nigeria

5.3.5.4 Qatar

5.3.5.5 Egypt

5.3.5.6 UAE

5.3.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 Arkema

6.4.3 Ashland

6.4.4 Avery Dennison Corporation

6.4.5 Beardow Adams

6.4.6 DELO Industrie Klebstoffe GmbH & Co. KGaA5

6.4.7 Dow

6.4.8 DuPont

6.4.9 H.B. Fuller Company

6.4.10 Henkel AG & Co. KgaA

6.4.11 Huntsman International LLC

6.4.12 Hexion

6.4.13 ITW Performance Polymers (Illinois Tool Works Inc.)

6.4.14 Parker Hannifin Corp (Lord Corporation)

6.4.15 Parson Adhesives Inc.

6.4.16 Sika AG

6.4.17 Solvay

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Innovation and Development of Bio-based Adhesives

7.2 Shifting Focus Towards Adhesive Bonding for Composite Materials

Metal Bonding Adhesives Industry Segmentation

Metal bonding adhesives are high-performance adhesives or chemicals used to join or connect two or more metal surfaces together with a bond that is strong and flexible enough to resist separation when subjected to movements, stress, high temperatures, and other adverse conditions.

The metal bonding adhesives market is segmented by resin type, application, and geography. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resin types (bio-based resins, hybrid, etc.). By application, the market is segmented into automotive and transportation, aerospace and defense, electrical and electronics, industrial assembly, construction and infrastructure, and other applications (marine, medical, etc.). The report also covers the market size and forecasts for the metal bonding adhesives market in 27 countries across major regions.

For each segment, the market sizing and forecasts have been done based on value (USD).

| Resin Type | |

| Acrylic | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resin Types (Bio-Based Resins, Hybrid, etc.) |

| Application | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Electrical and Electronics | |

| Industrial Assembly | |

| Construction and Infrastructure | |

| Other Applications (Marine, Medical, etc.) |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Metal Bonding Adhesives Market Research FAQs

How big is the Metal Bonding Adhesives Market?

The Metal Bonding Adhesives Market size is expected to reach USD 6.66 billion in 2024 and grow at a CAGR of greater than 5% to reach USD 8.91 billion by 2029.

What is the current Metal Bonding Adhesives Market size?

In 2024, the Metal Bonding Adhesives Market size is expected to reach USD 6.66 billion.

Who are the key players in Metal Bonding Adhesives Market?

3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG and Arkema are the major companies operating in the Metal Bonding Adhesives Market.

Which is the fastest growing region in Metal Bonding Adhesives Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Metal Bonding Adhesives Market?

In 2024, the Asia Pacific accounts for the largest market share in Metal Bonding Adhesives Market.

What years does this Metal Bonding Adhesives Market cover, and what was the market size in 2023?

In 2023, the Metal Bonding Adhesives Market size was estimated at USD 6.33 billion. The report covers the Metal Bonding Adhesives Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Metal Bonding Adhesives Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Metal Bonding Adhesives Industry Report

Statistics for the 2024 Metal Bonding Adhesives market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Metal Bonding Adhesives analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Metal Bonding Adhesives Market Report Snapshots