| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 218.02 Billion |

| Market Size (2030) | USD 381.82 Billion |

| CAGR (2025 - 2030) | 11.86 % |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

In Aerospace And Defense Market Major Players")

In Aerospace And Defense Market Size")

Mergers And Acquisitions (M&A) In Aerospace And Defense Market Analysis

The Mergers And Acquisitions In Aerospace And Defense Market size is estimated at USD 218.02 billion in 2025, and is expected to reach USD 381.82 billion by 2030, at a CAGR of 11.86% during the forecast period (2025-2030).

The aerospace and defense mergers and acquisitions landscape has undergone significant transformation, shifting away from traditional megamergers focused on cost savings toward strategic acquisitions aimed at product innovation and global market expansion. This evolution reflects broader industry trends, with Lazard's Aerospace and Defense Investment Banking Group reporting 148 M&A transactions announced as of May 2022. The industry's strategic focus has particularly intensified on supply chain resilience and technological advancement, with companies increasingly pursuing targeted acquisitions to secure critical capabilities and minimize disruption risks.

The market dynamics are being reshaped by the growing influence of private equity firms in aerospace M&A activities. Private equity transactions in the United States alone totaled USD 19.3 billion by the end of June 2022, demonstrating the sector's attractiveness to institutional investors. These investors are adopting more innovative approaches to capital deployment, including longer-term investment horizons, particularly in areas experiencing rapid technological advancement and market disruption. This trend is fostering a more diverse and competitive M&A environment, with private equity firms playing a crucial role in industry consolidation and technological innovation.

Cross-border transactions have emerged as a significant trend in the aerospace and defense mergers and acquisitions landscape, with US companies engaging in transactions worth USD 1.2 billion in the first half of 2022. Notable transactions include Airbus Helicopters' acquisition of German-based ZF Luftfahrttechnik in January 2023, strengthening their position in helicopter dynamic components and MRO services. These international deals reflect a broader industry strategy to enhance global market presence, access new technologies, and strengthen supply chain resilience across different geographical regions.

The industry is witnessing a strategic shift toward smaller, technology-focused acquisitions aimed at enhancing capabilities in emerging technologies and digital transformation. This trend is exemplified by recent transactions such as Abu Dhabi's ADQ combining four aviation companies to create a global firm with assets of USD 2.6 billion in October 2022, focusing on integrated maintenance, repair, and overhaul services. Companies are increasingly prioritizing acquisitions that provide access to advanced technologies in areas such as autonomous systems, artificial intelligence, and cybersecurity, reflecting the industry's evolution toward more sophisticated and digitally-enabled solutions. This strategic focus is indicative of the growing aerospace and defense market size and its potential for future growth.

Mergers And Acquisitions (M&A) In Aerospace And Defense Market Trends

Growing Focus of Aerospace and Defense OEMs on Business Expansion through Mergers and Acquisitions

The aerospace companies and defense sector has witnessed a significant transformation in its approach to aerospace acquisitions, shifting from traditional megamergers focused on cost savings to strategic acquisitions aimed at expanding product portfolios and global market presence. This evolution is evident in recent major aerospace and defense transactions, such as BAE Systems PLC's acquisition of Ball Aerospace for USD 5.5 billion in February 2024, which significantly enhanced their space and defense capabilities through the new Space and Mission Systems division. Similarly, Parker-Hannifin Corporation's acquisition of Meggitt PLC for approximately GBP 6.3 billion has enabled the expansion of their aerospace portfolio with advanced defense and aerospace technologies, demonstrating the industry's focus on technological advancement through strategic acquisitions.

The industry has also witnessed a surge in strategic mergers aimed at innovation and market expansion, as exemplified by the March 2024 merger between XTI Aircraft Company and Inpixon to form XTI Aerospace Inc., focusing on revolutionary private air transportation solutions. This trend extends to specialized technological acquisitions, as demonstrated by THALES's USD 1.1 billion acquisition of Cobham Aerospace Communications in February 2024, which aims to advance connected cockpit technologies. These strategic moves reflect the industry's shift towards acquiring smaller players with niche capabilities to enhance technological expertise and reduce supplier dependence, ultimately strengthening their competitive position in the global market.

Understand The Key Trends Shaping This Market

Download PDF

Governmental Policies Encouraging Growth in the Market Studied

Government initiatives worldwide are actively reshaping the aerospace and defense industry landscape by implementing policies that promote domestic manufacturing capabilities and international collaboration. In response to rising global tensions and supply chain vulnerabilities, democratic governments are introducing comprehensive policies to strengthen national defense manufacturing capabilities, particularly focusing on Tier 2 and 3 suppliers rather than just OEMs. These policies have led to increased opportunities for cross-border industrial cooperation, especially in Europe, where common security concerns have fostered greater collaboration among nations in defense manufacturing and technology development.

The impact of governmental support is particularly evident in emerging markets, where policies are being formulated to encourage foreign defense manufacturers to collaborate with local companies and establish subsidiaries. For instance, the Indian government has implemented policies to promote the indigenization of defense production, resulting in the approval of 45 companies/joint ventures operating in the defense sector with foreign OEMs. These initiatives are complemented by various governments' focus on forming strategic alliances to accelerate technological advancement and economic growth, while simultaneously addressing supply chain vulnerabilities through policies that encourage shorter, more resilient supply chains and stronger national capabilities in defense manufacturing.

Segment Analysis: Sector

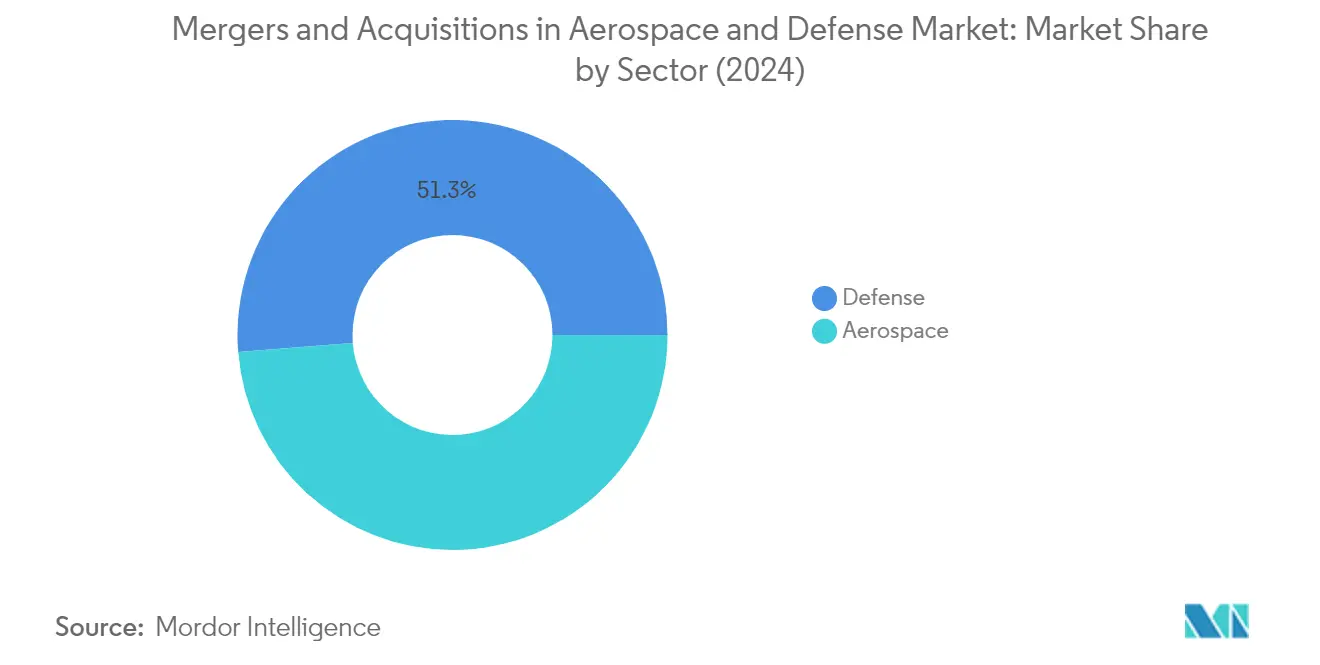

Defense Segment in Mergers and Acquisitions (M&A) in Aerospace and Defense Market

The defense segment continues to dominate the global aerospace and defense M&A market, holding approximately 51% market share in 2024. This significant market position is driven by increasing cross-border conflicts, rising terrorism concerns, and growing political disputes among neighboring countries, which have led to an enhanced focus on strengthening defense capabilities worldwide. The segment's prominence is further reinforced by substantial defense budget allocations from major powers and the strategic importance of acquisition in the defense industry. Key players in the defense sector are actively pursuing M&A in defense to expand their technological capabilities, particularly in areas such as unmanned systems, cybersecurity, and advanced weapons systems. The defense segment's robust performance is also supported by governmental policies encouraging domestic defense manufacturing capabilities and the consolidation of defense industrial bases across major markets.

Aerospace Segment in Mergers and Acquisitions (M&A) in Aerospace and Defense Market

The aerospace segment is demonstrating remarkable growth momentum in the M&A landscape, with an anticipated growth rate of approximately 14% during the forecast period 2024-2029. This accelerated growth is primarily driven by the increasing focus of aerospace companies on acquiring start-ups and innovative technology firms to enhance their product portfolios and technological capabilities. The segment's growth is further fueled by the rising demand for commercial aviation, the expansion of maintenance, repair, and overhaul (MRO) capabilities, and the growing emphasis on sustainable aviation technologies. Strategic mergers in aerospace in the aerospace sector are increasingly targeting companies specializing in electric propulsion, advanced materials, and digital technologies, reflecting the industry's shift towards more sustainable and technologically advanced solutions. The segment is also witnessing significant M&A activity in the space technology domain, as companies seek to capitalize on the growing commercial space market opportunities. This reflects the overall expansion of the aerospace and defense market size.

Mergers And Acquisitions (M&A) In Aerospace And Defense Market Geography Segment Analysis

Mergers and Acquisitions in the Aerospace and Defense Market in North America

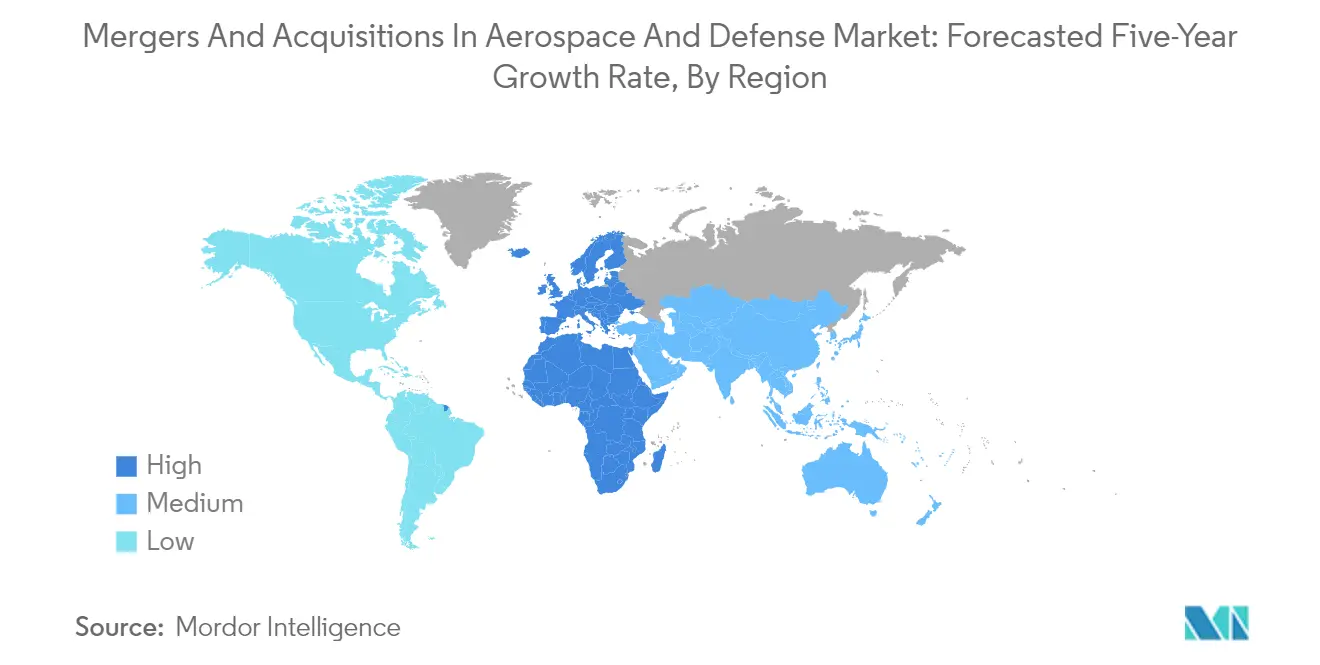

North America continues to dominate the global aerospace and defense market size, commanding approximately 63% of the global market share in 2024. The region's prominence is largely attributed to the presence of major aerospace OEMs and their extensive supplier networks across the United States and Canada. The mature and fragmented nature of the A&D sector in this region has created an environment where several global and regional players actively pursue aerospace mergers and acquisitions. The focus has notably shifted from megamergers towards targeted acquisitions that deliver new products and technological capabilities. The region's robust defense infrastructure and continuous technological advancement initiatives have made it particularly attractive for tier suppliers looking to penetrate the market through aerospace and defense M&A activities. The presence of stringent regulatory frameworks and sophisticated financial markets further facilitates structured deal-making processes. Additionally, the strong emphasis on supply chain sustainability and adaptation to geopolitical changes has made M&A an essential tool for industrial transformation in the region.

Mergers and Acquisitions in the Aerospace and Defense Market in Europe

The European aerospace and defense M&A market has demonstrated remarkable resilience and growth, achieving an approximate 15% annual growth rate from 2019 to 2024. The region's M&A landscape is characterized by a well-established aviation and defense sector, supported by the presence of industry giants like Airbus SE, BAE Systems, and Thales. The European market has witnessed a strategic transformation in recent years, with companies increasingly focusing on consolidating supplier bases to enhance operational efficiency. The region's unique political and economic framework, particularly within the European Union, has created opportunities for cross-border collaborations and strategic partnerships. The presence of advanced research and development capabilities, coupled with strong governmental support for defense modernization initiatives, has made European companies attractive targets for strategic acquisitions. The market has also seen increased activity in emerging sectors such as space technology, drone systems, and cybersecurity, driving further aerospace M&A deals.

Mergers and Acquisitions in the Aerospace and Defense Market in Asia-Pacific

The Asia-Pacific region represents one of the most dynamic markets for aerospace and defense M&A activities, with a projected growth rate of approximately 12% from 2024 to 2029. The region's M&A landscape is characterized by increasing investments in both civil aviation and defense sectors, driven by rising air passenger traffic and growing defense modernization programs. The market dynamics are shaped by the presence of emerging economic powerhouses like China and India, which are actively pursuing self-reliance in aerospace and defense capabilities. The region's strategic importance in global trade and security has attracted significant attention from international players looking to establish or expand their presence through strategic acquisitions. Local companies are increasingly seeking partnerships and acquisitions to enhance their technological capabilities and expand their market presence. The trend towards indigenous development of aerospace and defense capabilities has created numerous opportunities for technology-focused acquisitions and strategic partnerships.

Mergers and Acquisitions in the Aerospace and Defense Market in Latin America

The Latin American aerospace and defense M&A market exhibits significant potential for growth, driven by increasing modernization efforts in both civil aviation and military sectors. The region's market dynamics are characterized by a growing focus on enhancing domestic aerospace and defense capabilities through strategic partnerships and acquisitions. Countries like Brazil, Mexico, and Chile are leading the transformation by actively pursuing policies that encourage technology transfer and industrial cooperation through M&A activities. The market has witnessed increased interest from international players looking to establish regional manufacturing and maintenance capabilities. The growing emphasis on developing indigenous aerospace and defense capabilities has created opportunities for strategic acquisitions, particularly in areas such as aircraft maintenance, repair, and overhaul (MRO) services. The region's evolving regulatory environment and increasing defense budgets have created favorable conditions for defense mergers.

Mergers and Acquisitions in the Aerospace and Defense Market in the Middle East & Africa

The Middle East and African region presents unique opportunities in the aerospace and defense M&A landscape, driven by ambitious modernization programs and an increasing focus on developing indigenous capabilities. The market is characterized by significant investments in aviation infrastructure and defense modernization, particularly in Gulf Cooperation Council (GCC) countries. The region's strategic position and growing emphasis on diversifying economies beyond traditional sectors have created favorable conditions for M&A activities. Countries are actively pursuing partnerships and acquisitions to enhance their technological capabilities and develop local aerospace and defense industries. The market has witnessed increased interest in areas such as maintenance, repair, and overhaul (MRO) facilities, defense electronics, and unmanned systems. The growing focus on localization of manufacturing and maintenance capabilities has created opportunities for strategic acquisitions and joint ventures.

Get Analysis on Important Geographic Markets

Download PDF

Mergers And Acquisitions (M&A) In Aerospace And Defense Industry Overview

Top Companies in Mergers and Acquisitions in Aerospace and Defense Market

The market is dominated by major players including Boeing Company, Raytheon Technologies, Airbus SE, General Electric, Safran SA, BAE Systems, Parker Hannifin, L3Harris Technologies, Leonardo SpA, and Thales. These aerospace companies are actively pursuing innovation through strategic acquisitions of smaller technology-focused firms, particularly in areas like unmanned systems, cybersecurity, and advanced materials. The industry leaders are demonstrating operational agility by streamlining their supply chains and integrating acquired capabilities into their existing portfolios. Companies are increasingly focusing on cross-border acquisitions to expand their global footprint and access new markets, particularly in the Asia-Pacific and Middle East regions. Strategic moves include vertical integration through the acquisition of key suppliers, investment in emerging technologies like autonomous systems and artificial intelligence, and expansion of MRO capabilities through targeted acquisitions of specialized service providers.

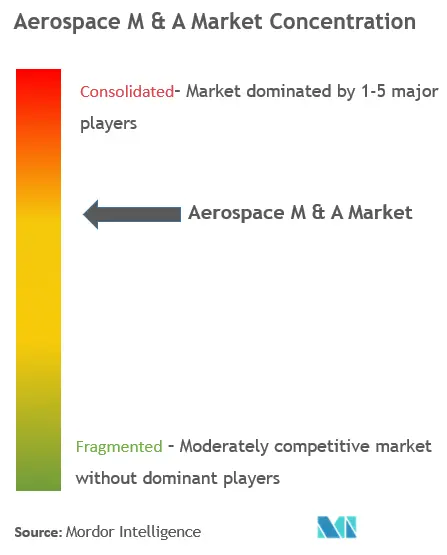

Market Consolidation Drives Industry Evolution and Growth

The aerospace and defense M&A landscape is characterized by a mix of global conglomerates and specialized players, with the major conglomerates holding significant market share through their diverse portfolios and extensive geographic presence. The market structure shows a high degree of consolidation at the top tier, with several large players dominating the global landscape, while the middle and lower tiers remain relatively fragmented with numerous specialized companies focusing on specific technologies or regional markets. The industry is witnessing a shift from megamergers focused on cost savings to strategic acquisitions aimed at acquiring new capabilities and technologies, particularly in emerging areas like unmanned systems, cybersecurity, and advanced materials.

The M&A activity in the sector is increasingly being shaped by geopolitical factors, supply chain considerations, and technological advancement needs. Companies are adopting more aggressive acquisition strategies to gain major contracts and increase their market presence, with a particular focus on acquiring smaller players with niche capabilities. Private equity firms are playing an increasingly important role in the market, bringing new perspectives and longer-term investment horizons to the industry. The market is also seeing a trend towards cross-sector collaborations, where traditional aerospace and defense companies are acquiring or partnering with technology firms to enhance their digital capabilities and innovation potential. The role of aerospace and defense M&A advisory services is becoming crucial in navigating these complex transactions.

Innovation and Agility Key to Future Success

For incumbent players to maintain and increase their market share, the focus needs to be on strategic capability acquisition and technological innovation. Companies must develop robust strategies for identifying and integrating smaller, innovative firms while maintaining operational efficiency and customer relationships. Success factors include the ability to navigate complex regulatory environments, maintain strong relationships with government customers, and effectively manage supply chain risks. Companies need to balance between organic growth and strategic acquisitions, while also investing in research and development to stay ahead of technological curves.

For contenders looking to gain ground, the key lies in developing specialized capabilities and establishing strong positions in emerging technology areas. These companies need to focus on building strong intellectual property portfolios and developing unique value propositions that address specific market needs or technological gaps. Success will depend on the ability to form strategic partnerships, maintain operational flexibility, and demonstrate clear value differentiation. Companies must also consider the increasing importance of environmental sustainability and digital transformation in their growth strategies, while being prepared to adapt to evolving regulatory requirements and changing customer preferences in both commercial and defense sectors. The presence of a defense industry M&A advisor can significantly aid in these strategic endeavors.

Mergers And Acquisitions (M&A) In Aerospace And Defense Market Leaders

-

Parker Hannifin Corporation

-

The Boeing Company

-

Airbus SE

-

RTX Corporation

-

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Mergers And Acquisitions (M&A) In Aerospace And Defense Market News

March 2024: Airbus Defence and Space acquired Infodas, a German cybersecurity company that provides IT solutions for the public sector's defense and critical infrastructure elements. The acquisition deal is expected to be finalized before Q4-2024.

March 2024: Spirit AeroSystems Holdings Inc. announced that it was engaged in talks with Boeing regarding Boeing's potential acquisition of Spirit AeroSystems. Spirit AeroSystems manufactures aerostructures for commercial aircraft, defense platforms, and business and regional jets.

Aerospace Mergers and Acquisitions Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Sector

- 5.1.1 Aerospace

- 5.1.2 Defense

-

5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Latin America

- 5.2.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles*

- 6.1.1 The Boeing Company

- 6.1.2 RTX Corporation

- 6.1.3 Airbus SE

- 6.1.4 General Electric Company

- 6.1.5 Safran SA

- 6.1.6 BAE Systems PLC

- 6.1.7 Parker Hannifin Corporation

- 6.1.8 L3Harris Technologies Inc.

- 6.1.9 Leonardo SpA

- 6.1.10 THALES

- 6.1.11 Elbit Systems Ltd

- 6.1.12 Rolls-Royce PLC

- 6.1.13 Honeywell International Inc.

- 6.1.14 Rheinmetall AG

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Mergers And Acquisitions (M&A) In Aerospace And Defense Industry Segmentation

Mergers and acquisitions (M&A) in the aerospace and defense (A&D) sector have emerged as a commercially viable business strategy as they help the participants enhance their technological know-how while mitigating the risks associated with technological disruptions. Moreover, mergers and acquisitions facilitate the sustenance of both firms and, in most cases, help the major players to foster comparatively faster growth than their competitors.

The aerospace mergers and acquisitions market is segmented based on sector and geography. By sector, the market is segmented by aerospace and defense. The report also covers the market sizes and forecasts in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Sector | Aerospace |

| Defense | |

| Geography | North America |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Aerospace Mergers and Acquisitions Market Research FAQs

How big is the Mergers And Acquisitions In Aerospace And Defense Market?

The Mergers And Acquisitions In Aerospace And Defense Market size is expected to reach USD 218.02 billion in 2025 and grow at a CAGR of 11.86% to reach USD 381.82 billion by 2030.

What is the current Mergers And Acquisitions In Aerospace And Defense Market size?

In 2025, the Mergers And Acquisitions In Aerospace And Defense Market size is expected to reach USD 218.02 billion.

Who are the key players in Mergers And Acquisitions In Aerospace And Defense Market?

Parker Hannifin Corporation, The Boeing Company, Airbus SE, RTX Corporation and Safran SA are the major companies operating in the Mergers And Acquisitions In Aerospace And Defense Market.

Which is the fastest growing region in Mergers And Acquisitions In Aerospace And Defense Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Mergers And Acquisitions In Aerospace And Defense Market?

In 2025, the North America accounts for the largest market share in Mergers And Acquisitions In Aerospace And Defense Market.

What years does this Mergers And Acquisitions In Aerospace And Defense Market cover, and what was the market size in 2024?

In 2024, the Mergers And Acquisitions In Aerospace And Defense Market size was estimated at USD 192.16 billion. The report covers the Mergers And Acquisitions In Aerospace And Defense Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Mergers And Acquisitions In Aerospace And Defense Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Mergers And Acquisitions (M&A) In Aerospace And Defense Market Research

Mordor Intelligence delivers comprehensive insights into the dynamic world of aerospace and defense M&A. We leverage our extensive experience in tracking aerospace mergers and acquisitions across global markets. Our analysis covers major aerospace companies and their strategic moves. This includes everything from Boeing mergers to Airbus acquisitions. We provide a detailed examination of aerospace and defense market size and growth trajectories. The report thoroughly examines defense industry acquisition patterns and aerospace M&A deals. It offers strategic insights into both completed and potential transactions.

Stakeholders gain access to detailed defense industry merger report data through an easy-to-download PDF format. This format features an in-depth analysis of aerospace and defense transactions and emerging trends. Our research encompasses defense M&A activities, aerospace acquisitions, and strategic developments across the sector. This is supported by comprehensive mergers and acquisitions dataset analysis. The report proves invaluable for industry leaders, investors, and strategists. It helps them understand aerospace and defense mergers and acquisitions dynamics, with particular attention to defense industry M&A advisory perspectives and future growth opportunities.