Market Size of MENA Wealth Management Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

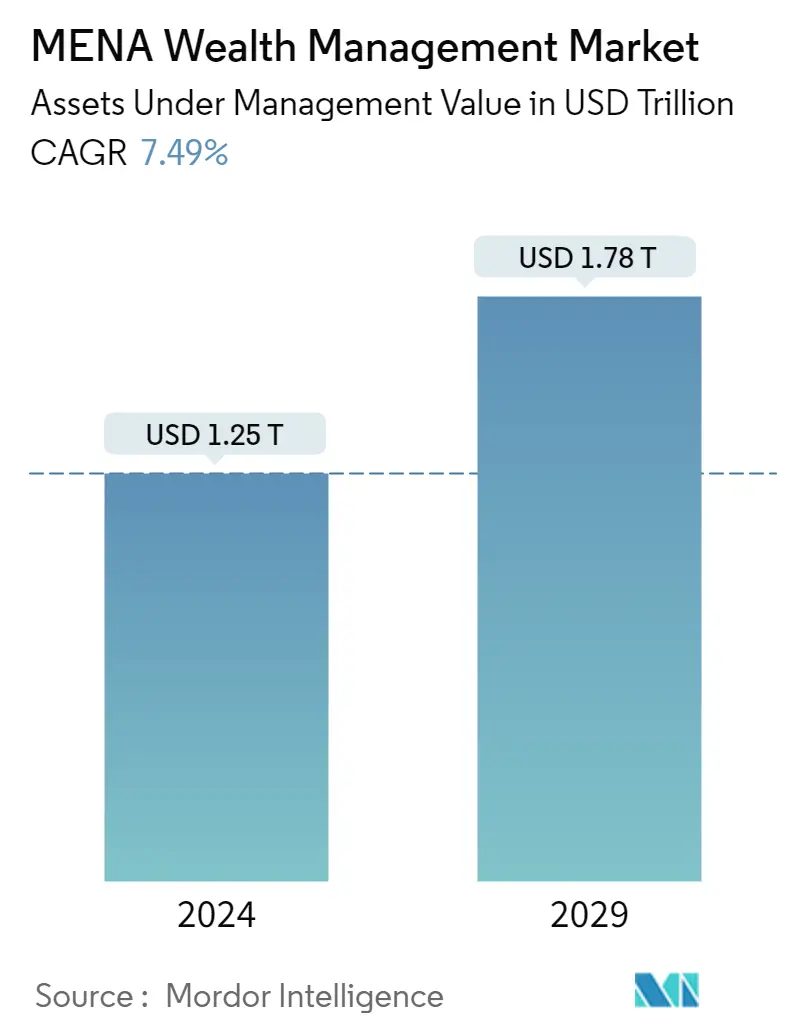

| Market Size (2024) | USD 1.25 Trillion |

| Market Size (2029) | USD 1.78 Trillion |

| CAGR (2024 - 2029) | 7.49 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

MENA Wealth Management Market Analysis

The MENA Wealth Management Market size in terms of assets under management value is expected to grow from USD 1.25 trillion in 2024 to USD 1.78 trillion by 2029, at a CAGR of 7.49% during the forecast period (2024-2029).

The wealth management industry in the MENA region is growing and coming on the path of sustainability as clients are more likely to reevaluate and move their assets during major life events. In the Middle East & North Africa (MENA) region, most clients move their money when starting a new business or when buying a house, and more than half of clients reconsider their asset management when inheriting or receiving money.

Countries in the Levant and North Africa region were ahead of the GCC while establishing their financial markets. The AuM growth in the region is primarily attributed to an increase in Sovereign Wealth Funds (SWF) assets, mainly due to strong capital market performances. Many SWFs had high equity exposure in developing and emerging markets, faring well as the financial landscape regained a degree of pre-pandemic stability. Further, another main driver of AuM growth was retail investors.

MENA Wealth management market is projected to grow through the potential for sizeable progress within private markets, especially for firms that can successfully enter the retail market, systematically use data and analytics to enhance decision-making and integrate meaningful ESG metrics. During COVID-19, the Wealth management industry faced a drastic downfall in the MENA region as the whole globe faced a challenging situation. Now, the asset management industry is coming out of the crisis with notable changes. Although the operating environment continues to change, the growth recorded during the pandemic implies further development as countries like Saudi Arabia, UAE, Egypt, and other countries continue reemerging, with many opportunities.

MENA Wealth Management Industry Segmentation

Wealth management is a type of financial Advisory service. A wealth advisor often works with wealthy people to develop a personalized investment plan to assist them in managing their assets. Additionally, thorough financial counseling, tax advice, estate planning, and even legal support are typically included in wealth management. A complete background analysis of the MENA Wealth Management Market, including the assessment of the economy, market overview, market size estimation for critical segments and emerging trends in the market, market dynamics, and key company profiles, are covered in the report. The MENA Wealth Management Market is segmented by client type (HNWI, Retail/ Individuals, Mass Affluent, and others), by provider (Private Bankers, Fintech Advisors, Family Offices, and others), and by geography (Saudi Arabia, Algeria, Egypt, United Arab Emirates, and Other Countries).

| By Client Type | |

| HNWIs | |

| Retail/ Individuals | |

| Mass Affluents | |

| Other Client Types |

| By Provider Type | |

| Private Bankers | |

| Fintech Advisors | |

| Family Offices | |

| Other Provider Types |

| By Geography | |

| Saudi Arabia | |

| Algeria | |

| Egypt | |

| United Arab Emirates | |

| Rest of MENA Region |

MENA Wealth Management Market Size Summary

The MENA wealth management market is experiencing significant growth, driven by a combination of factors including the reevaluation of asset management during major life events and the expansion of sovereign wealth funds. The region's financial markets, particularly in the Levant and North Africa, have historically been ahead of the Gulf Cooperation Council (GCC) countries. The growth in assets under management (AuM) is largely attributed to strong capital market performances and increased equity exposure in developing markets. Retail investors are also playing a crucial role in this expansion. The market is poised for further growth through advancements in private markets and the integration of data analytics and ESG metrics, despite the challenges posed by the COVID-19 pandemic.

Saudi Arabia stands out in the GCC with its substantial investment funds and a shift towards diversifying investments beyond real estate into venture capital and private equity. This shift is supported by various government institutions and regulatory changes aimed at revamping financial services. The adoption of technologies like artificial intelligence and robotic process automation is enhancing client experiences, while FinTech innovations are reshaping the market landscape. The competitive environment in the MENA region is marked by significant players such as NCB Capital and Emirates NBD Asset Management, with recent developments like strategic partnerships and bond issuances further strengthening their market positions.

MENA Wealth Management Market Size - Table of Contents

-

1. MARKET INSIGHTS AND DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Adoption of New Age Digital Platforms by Millenials

-

1.2.2 Increasing HNWI in MENA Region

-

-

1.3 Market Restraints

-

1.3.1 Increased Cyber-Security Risks

-

-

1.4 Technological Advancement Shaping the Wealth Management Landscape in the Region

-

1.4.1 Insights on Digital Platform and New Age Fintechs Adoption Levels across the Value Chain Wealth Management in the Region

-

1.4.2 Insights on Robo Advisors and the other applications of Artificial Intelligence techniques in Wealth Management Industry

-

-

1.5 Porter's Five Forces Analysis

-

1.5.1 Bargaining Power of Suppliers

-

1.5.2 Bargaining Power of Buyers/ Consumers

-

1.5.3 Threat of New Entrants

-

1.5.4 Threat of Substitute Product

-

1.5.5 Intensity of Competitive Rivalry

-

-

1.6 Government Policies and Regulations Impacting the Wealth Management Industry of MENA Region

-

1.7 Insights into Alternative Assets Considered for Financial Planning By Wealth Managers in the Region

-

1.8 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Client Type

-

2.1.1 HNWIs

-

2.1.2 Retail/ Individuals

-

2.1.3 Mass Affluents

-

2.1.4 Other Client Types

-

-

2.2 By Provider Type

-

2.2.1 Private Bankers

-

2.2.2 Fintech Advisors

-

2.2.3 Family Offices

-

2.2.4 Other Provider Types

-

-

2.3 By Geography

-

2.3.1 Saudi Arabia

-

2.3.2 Algeria

-

2.3.3 Egypt

-

2.3.4 United Arab Emirates

-

2.3.5 Rest of MENA Region

-

-

MENA Wealth Management Market Size FAQs

How big is the MENA Wealth Management Market?

The MENA Wealth Management Market size is expected to reach USD 1.25 trillion in 2024 and grow at a CAGR of 7.49% to reach USD 1.78 trillion by 2029.

What is the current MENA Wealth Management Market size?

In 2024, the MENA Wealth Management Market size is expected to reach USD 1.25 trillion.