MENA Wealth Management Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

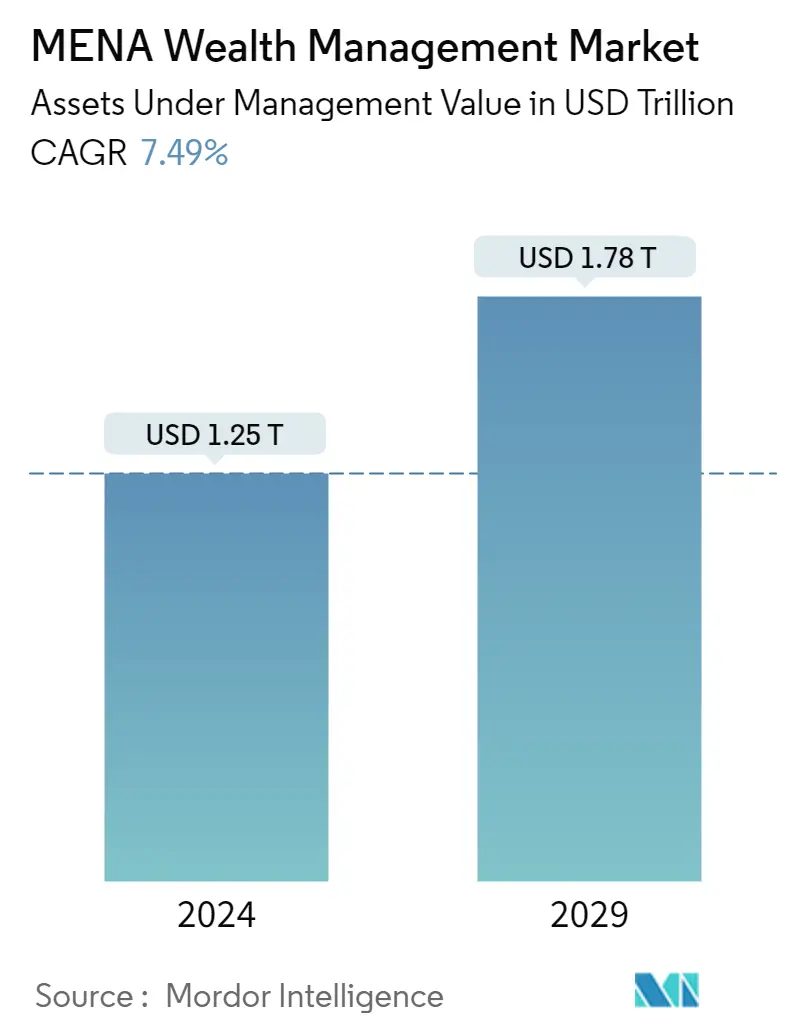

| Market Size (2024) | USD 1.25 Trillion |

| Market Size (2029) | USD 1.78 Trillion |

| CAGR (2024 - 2029) | 7.49 % |

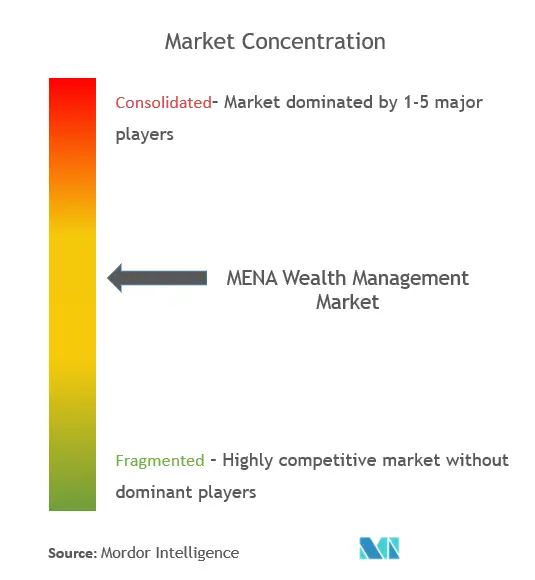

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

MENA Wealth Management Market Analysis

The MENA Wealth Management Market size in terms of assets under management value is expected to grow from USD 1.25 trillion in 2024 to USD 1.78 trillion by 2029, at a CAGR of 7.49% during the forecast period (2024-2029).

The wealth management industry in the MENA region is growing and coming on the path of sustainability as clients are more likely to reevaluate and move their assets during major life events. In the Middle East & North Africa (MENA) region, most clients move their money when starting a new business or when buying a house, and more than half of clients reconsider their asset management when inheriting or receiving money.

Countries in the Levant and North Africa region were ahead of the GCC while establishing their financial markets. The AuM growth in the region is primarily attributed to an increase in Sovereign Wealth Funds (SWF) assets, mainly due to strong capital market performances. Many SWFs had high equity exposure in developing and emerging markets, faring well as the financial landscape regained a degree of pre-pandemic stability. Further, another main driver of AuM growth was retail investors.

MENA Wealth management market is projected to grow through the potential for sizeable progress within private markets, especially for firms that can successfully enter the retail market, systematically use data and analytics to enhance decision-making and integrate meaningful ESG metrics. During COVID-19, the Wealth management industry faced a drastic downfall in the MENA region as the whole globe faced a challenging situation. Now, the asset management industry is coming out of the crisis with notable changes. Although the operating environment continues to change, the growth recorded during the pandemic implies further development as countries like Saudi Arabia, UAE, Egypt, and other countries continue reemerging, with many opportunities.

MENA Wealth Management Market Trends

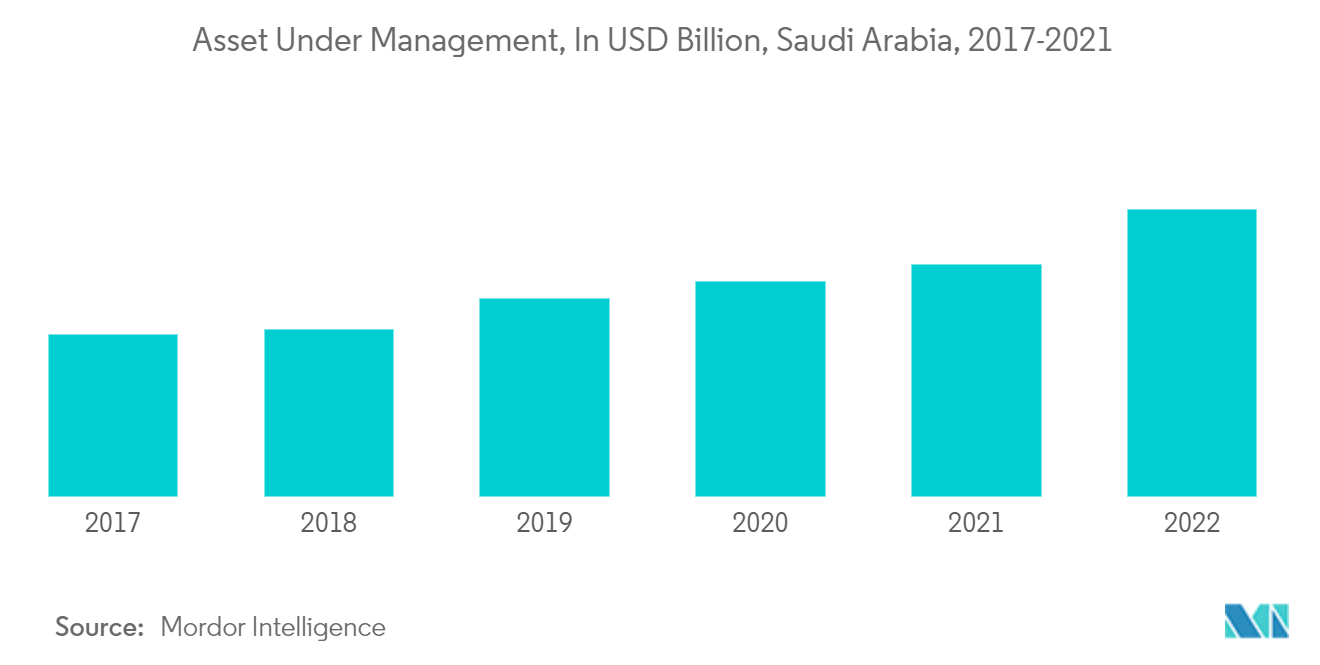

Saudi Arabia Asset Under Management Trend Shows Growth in Wealth Management Industry on MENA Region

Saudi Arabia has raised tens of billions of dollars in sovereign issuances in the past five years (after nearly a decade without public debt issuances). Public debt issuance increased by nearly 50 percent in recent years. While non-government debt issuance increased by more than 250 percent compared to the previous year. Over the past three years, the CMA has released numerous regulations covering the establishment of new corporate vehicles. The IPO process and foreign investment in Saudi Arabia have promised a complete revamp of existing financial services regulations.

Saudi Arabia is home to the largest investment funds in the Gulf Cooperation Council (GCC). Funds and asset managers have been gradually diversifying from primarily real estate investments into other parts of the economy, with a particular focus on venture capital and private equity, as these sectors are being supported by the CMA, PIF (directly and through its fund of funds established under the name of Jada), Sanabil Investments, the Saudi Venture Capital Company (a government-owned venture capital investment firm), the Ministry of Commerce, the Ministry of Investment, the Ministry of Labour, Social Development Bank, the Small and Medium Enterprise Authority (SMEA), the Saudi Technology Development and Investment Company (TAQNIA) and other government institutions.

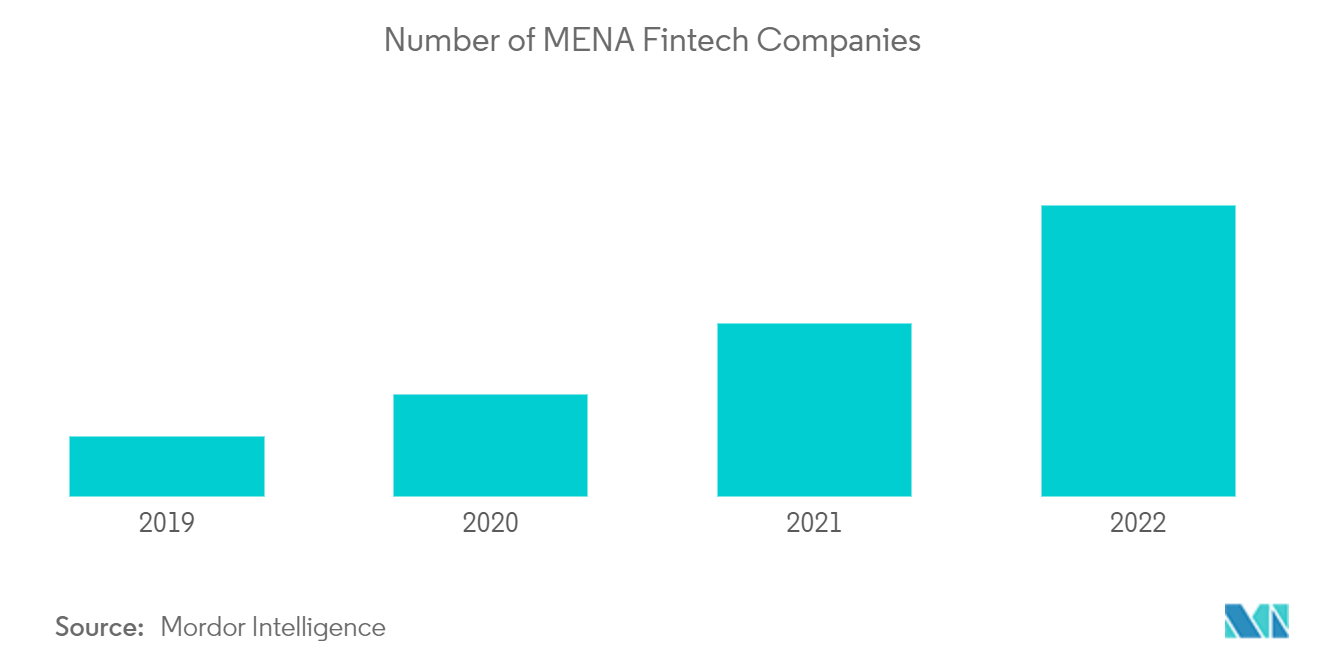

Growing Fintech in MENA Boosted MENA Wealth Management Market

Wealth managers are investing in technologies such as artificial intelligence (AI) and robotic process automation. This is done to better cater to the clients and increase customer experience. FinTechs have created a new trend in the wealth management market. The number of companies in the Middle East and North Africa region. The growth has seen an exponential rise in 2022 due to the pandemic and other factors, such as increasing requirements and needs for digitalization.

MENA Wealth Management Industry Overview

The MENA Wealth Management Market is growing and becoming competitive across the different countries of the UAE. Saudi Arabia is offering many competitive players dominating the market, recently grabbing the market more powerfully through mergers and acquisitions. Major market players include NCB Capital, Orange Asset Management, Waha Capital, Emirates NBD Asset Management, and Riyad Capital.

MENA Wealth Management Market Leaders

-

NCB Capital

-

Orange Asset Management

-

Waha Capital

-

Emirates NBD Asset Management

-

Riyad Capital

*Disclaimer: Major Players sorted in no particular order

MENA Wealth Management Market News

- January 2023: Emirates NBD Securities, a leading brokerage firm in the UAE, partnered with Abu Dhabi Securities Exchange (ADX) to provide traders with instant access to the exchange's listed companies, enabling it to offer instant trading account opening and digital onboarding to another UAE stock exchange.

- January 2023: Emirates NBD, one of the leading banks in the MENAT region, announced the successful pricing of its inaugural AED 1 billion dirham-denominated bonds, the first such issue by a UAE bank.

MENA Wealth Management Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of Study

2. RESEARCH METHODOLOGY

3. EXCEUTIVE SUMMARY

4. MARKET INSIGHTS AND DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Adoption of New Age Digital Platforms by Millenials

4.2.2 Increasing HNWI in MENA Region

4.3 Market Restraints

4.3.1 Increased Cyber-Security Risks

4.4 Technological Advancement Shaping the Wealth Management Landscape in the Region

4.4.1 Insights on Digital Platform and New Age Fintechs Adoption Levels across the Value Chain Wealth Management in the Region

4.4.2 Insights on Robo Advisors and the other applications of Artificial Intelligence techniques in Wealth Management Industry

4.5 Porter's Five Forces Analysis

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Power of Buyers/ Consumers

4.5.3 Threat of New Entrants

4.5.4 Threat of Substitute Product

4.5.5 Intensity of Competitive Rivalry

4.6 Government Policies and Regulations Impacting the Wealth Management Industry of MENA Region

4.7 Insights into Alternative Assets Considered for Financial Planning By Wealth Managers in the Region

4.8 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

5.1 By Client Type

5.1.1 HNWIs

5.1.2 Retail/ Individuals

5.1.3 Mass Affluents

5.1.4 Other Client Types

5.2 By Provider Type

5.2.1 Private Bankers

5.2.2 Fintech Advisors

5.2.3 Family Offices

5.2.4 Other Provider Types

5.3 By Geography

5.3.1 Saudi Arabia

5.3.2 Algeria

5.3.3 Egypt

5.3.4 United Arab Emirates

5.3.5 Rest of MENA Region

6. COMPETITIVE LANDSCAPE

6.1 Market Competition Overview and Integration/ Competition with Traditional Financial Services Companies

6.2 Company Profiles

6.2.1 NCB Capital

6.2.2 Investcorp

6.2.3 Riyad Capital

6.2.4 Lazard Asset Management

6.2.5 Arab National Investment Company

6.2.6 Aljazira Capital

6.2.7 Emirates NBD Asset Management

6.2.8 Waha Capital

6.2.9 Fippar Holdings

6.2.10 Orange Asset Management*

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. DISCLAIMER & ABOUT US

MENA Wealth Management Industry Segmentation

Wealth management is a type of financial Advisory service. A wealth advisor often works with wealthy people to develop a personalized investment plan to assist them in managing their assets. Additionally, thorough financial counseling, tax advice, estate planning, and even legal support are typically included in wealth management. A complete background analysis of the MENA Wealth Management Market, including the assessment of the economy, market overview, market size estimation for critical segments and emerging trends in the market, market dynamics, and key company profiles, are covered in the report. The MENA Wealth Management Market is segmented by client type (HNWI, Retail/ Individuals, Mass Affluent, and others), by provider (Private Bankers, Fintech Advisors, Family Offices, and others), and by geography (Saudi Arabia, Algeria, Egypt, United Arab Emirates, and Other Countries).

| By Client Type | |

| HNWIs | |

| Retail/ Individuals | |

| Mass Affluents | |

| Other Client Types |

| By Provider Type | |

| Private Bankers | |

| Fintech Advisors | |

| Family Offices | |

| Other Provider Types |

| By Geography | |

| Saudi Arabia | |

| Algeria | |

| Egypt | |

| United Arab Emirates | |

| Rest of MENA Region |

MENA Wealth Management Market Research FAQs

How big is the MENA Wealth Management Market?

The MENA Wealth Management Market size is expected to reach USD 1.25 trillion in 2024 and grow at a CAGR of 7.49% to reach USD 1.78 trillion by 2029.

What is the current MENA Wealth Management Market size?

In 2024, the MENA Wealth Management Market size is expected to reach USD 1.25 trillion.

Who are the key players in MENA Wealth Management Market?

NCB Capital, Orange Asset Management, Waha Capital, Emirates NBD Asset Management and Riyad Capital are the major companies operating in the MENA Wealth Management Market.

What years does this MENA Wealth Management Market cover, and what was the market size in 2023?

In 2023, the MENA Wealth Management Market size was estimated at USD 1.16 trillion. The report covers the MENA Wealth Management Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the MENA Wealth Management Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the key obstacles faced by the MENA Wealth Management Market?

The key obstacles faced by the MENA Wealth Management Market are a) Regulatory complexities across different countries b) Geopolitical uncertainties impacting investment decisions c) Lack of skilled professionals in wealth management

MENA Wealth Management Industry Report

The MENA wealth management market is experiencing robust growth, driven by an increasing number of high-net-worth and ultra-high-net-worth individuals, economic diversification, and supportive government policies, particularly in Saudi Arabia where wealth management companies are thriving. The market is intensely competitive, featuring a mix of domestic and international banks, asset management firms, and independent advisory firms. These entities are increasingly adopting hybrid and digital platforms to cater to tech-savvy clients. Key market segments include traditional advisory services, discretionary portfolio management, private banking, and family office services. There is a growing demand for digital transformation, sustainable investing, and comprehensive family office services. Additionally, the popularity of Sharia-compliant products and a rising interest in environmental, social, and governance (ESG) investing are shaping the region's wealth management landscape. Despite regulatory complexities and geopolitical uncertainties, the market presents significant opportunities for wealth management industry growth and market expansion, leveraging innovative technologies and a customer-centric approach. For detailed statistics on the MENA Wealth Management market share, size, and revenue growth rate, refer to industry reports by Mordor Intelligence™, which include market forecasts, outlooks, and historical overviews available as free report PDF downloads.

MENA Wealth Management Market Report Snapshots