Market Size of MENA ICT Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

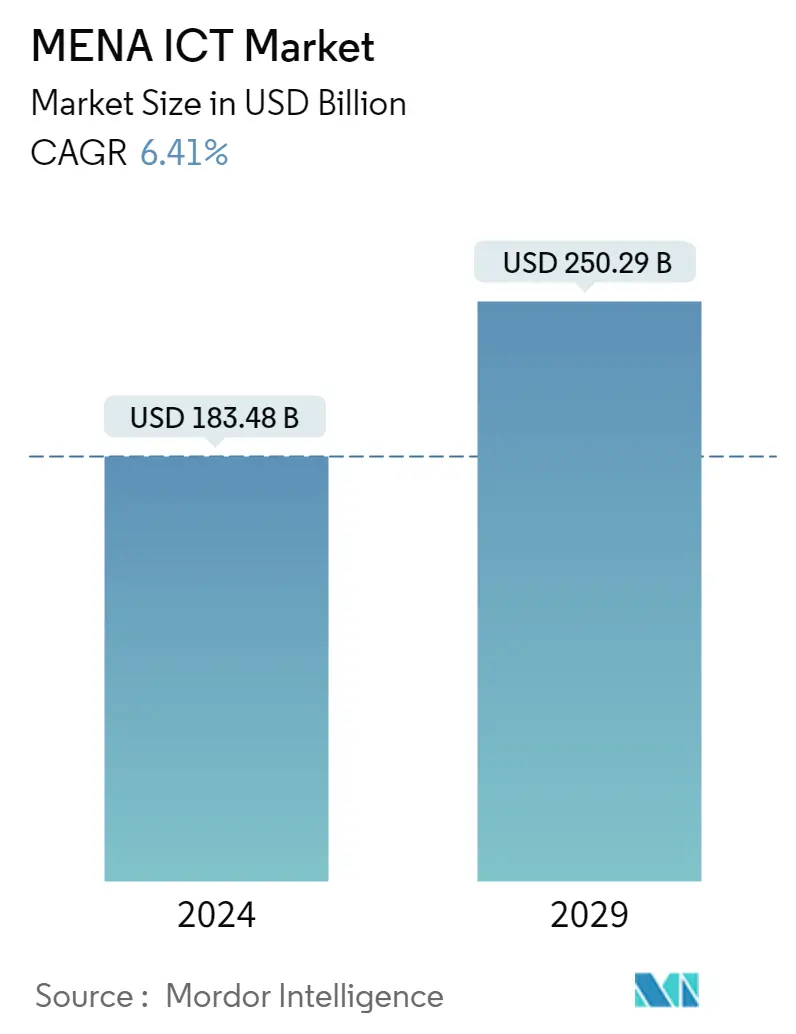

| Market Size (2024) | USD 183.48 Billion |

| Market Size (2029) | USD 250.29 Billion |

| CAGR (2024 - 2029) | 6.41 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

MENA ICT Market Analysis

The MENA ICT Market size is estimated at USD 183.48 billion in 2024, and is expected to reach USD 250.29 billion by 2029, growing at a CAGR of 6.41% during the forecast period (2024-2029).

- Ongoing Events and Tourism Driving Automation: The MENA ICT market is witnessing a surge in automation demand, catalyzed by ongoing events and tourism. In 2022, the UAE's travel and tourism sector contributed AED 167 billion to the GDP, representing 9% of the total. International tourists spent AED 117.6 billion, with hotel capacity expanding to 203,000 rooms across 1,189 establishments. This rise in tourism is driving the adoption of smart technologies:

- Automated check-ins: Self-service kiosks streamline guest experiences in hotels and airports.

- Smart room controls: Enhance comfort while improving energy efficiency through IoT devices.

- Baggage automation: Airports are implementing automated baggage handling systems for operational efficiency.

- Tourist attractions: Automated ticketing and guided tours are becoming standard, improving visitor management.

- Government Policies Fostering Digital Transformation: Government strategies across the MENA region are pivotal in driving digital transformation. These initiatives aim to diversify economies and bolster ICT infrastructure:

- UAE Digital Government Strategy 2025: Promotes governance that is digital-by-design, integrating technology across government functions.

- Egypt Vision 2030 and Digital Egypt: Focus on infrastructure development, innovation, and fostering digital skills to fuel economic growth.

- Oman’s Digital Transformation Program: Targets sustainable knowledge building and enhancing public sector productivity by upgrading digital infrastructure.

- Saudi Arabia’s Vision 2030: Emphasizes 5G deployment, e-government, data governance, and cybersecurity, setting a foundation for nationwide digital progress.

- Rising Digital Transformation Across Industries: The MENA region is experiencing substantial digital transformation across sectors, with industries increasingly integrating cutting-edge technologies:

- Healthcare: Providers like Medeor Hospitals and Mediclinic are adopting unified healthcare information systems to improve patient engagement.

- Financial sector: Fintech solutions, including digital banking and payment systems, are seeing widespread adoption.

- Manufacturing: Industry 4.0 technologies, such as AI-driven predictive maintenance, are being implemented to enhance operational efficiency.

- Retail: Big data analytics is being used to personalize customer experiences and optimize inventory management.

- Regulatory Reforms Shaping the ICT Landscape: Regulatory frameworks are crucial in creating a competitive ICT environment. Key focus areas include:

- Licensing frameworks: Balancing industry growth with regulatory control for sustainable development.

- Spectrum allocation: Ensuring adequate bandwidth for expanding telecommunication needs.

- Data protection laws: The UAE’s 2021 federal law on personal data protection sets new standards for safeguarding user data.

- Cybersecurity regulations: Information Assurance Regulations are in place to protect the region’s critical digital infrastructure.

- Investment and Partnerships Driving Innovation: Significant investments and partnerships are accelerating digital transformation in the MENA ICT sector:

- Mindware and Xebia (Nov 2023): This partnership will enhance digital transformation across the Middle East & Africa by leveraging Xebia’s AI and cloud expertise.

- Saudi investments: Over $9 billion has been allocated to digital transformation projects, reinforcing Saudi Arabia’s commitment to tech infrastructure.

- Memory Technology Middle East and Huawei (Jul 2023): Partnering to boost digital services for UAE-based SMBs.

- KT, Hyundai E&C, and STC Group: A joint initiative to establish digital infrastructure in Saudi Arabia, including internet data centers and smart cities.

- Market Growth and Future Outlook: The MENA ICT market is on a trajectory of substantial growth. Egypt’s ICT market alone, valued at $14.65 billion in 2022, is expected to reach $27.52 billion by 2028, growing at a CAGR of 10.58%. Major drivers include:

- Smartphone penetration: Expected to hit 92% by 2030, bolstering demand for ICT services.

- Government initiatives: Digital transformation efforts across sectors will fuel industry growth.

- 5G and IoT expansion: Increased demand for cloud computing and data center services will underpin ICT market expansion.

MENA ICT Industry Segmentation

The MENA ICT market includes the amalgamation and adoption of different Information and Communications Technologies (ICT), such as big data, mobility, storage, outsourcing, and cloud computing in MENA for the purpose of digitization and digital transformation. It tracks the revenue accrued through the sale of technology-related solutions.

The MENA ICT market is segmented by technology (big data analytics, mobility and telecom, cloud computing, storage, business process, and outsourcing), component (hardware/devices, software and services, and communication and connectivity), end-user industry (oil, gas and utilities, travel and hospitality, healthcare, financial services, and manufacturing and construction), and country (Saudi Arabia, United Arab Emirates, Qatar, Oman, Egypt, and Rest of MENA). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Technology | |

| Big Data Analytics | |

| Mobility and Telecom | |

| Cloud Computing | |

| Storage | |

| Business Process Outsourcing | |

| Other Technologies |

| By Component | |

| Hardware/Devices | |

| Software and Services | |

| Communication and Connectivity |

| By End-user Industry | |

| Oil, Gas and Utilities | |

| Travel and Hospitality | |

| Healthcare | |

| Financial Services | |

| Manufacturing and Construction | |

| Other End-user Industries |

| By Country | |

| Saudi Arabia | |

| United Arab Emirates | |

| Qatar | |

| Oman | |

| Egypt | |

| Rest of MENA |

MENA ICT Market Size Summary

The MENA ICT market is poised for substantial growth, driven by the rapid digital transformation across various sectors. This expansion is fueled by strategic alliances, mergers, and acquisitions as companies strive to maintain a competitive edge in an increasingly digital landscape. The demand for ICT solutions is being propelled by the need for automation, data analytics, and e-commerce, with significant advancements in telehealth and smart tourism technologies. Government initiatives, such as Oman Vision 2040 and the UAE Digital Government Strategy 2025, are further bolstering the market by enhancing digital infrastructure and promoting e-government services. However, challenges such as security and privacy concerns remain prevalent, as the reliance on digital technologies increases the vulnerability to cyber threats.

The UAE stands out as a key player in the MENA ICT sector, with its competitive environment fostering innovation and digital inclusion. The country's focus on artificial intelligence and cloud-based solutions is driving market growth, supported by initiatives like the Personal Data Protection Law and strategic partnerships with global tech giants. The adoption of high-speed internet and mobile communication services is also contributing to the market's expansion, with emerging technologies like AI, IoT, and the metaverse creating new opportunities. The market is characterized by high competitive rivalry, with major players such as Google, IBM, and Microsoft actively seeking to enhance their offerings through strategic collaborations and technological advancements.

MENA ICT Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 An Assessment of the Impact of COVID-19 on the Industry

-

1.4 Analysis of Key Regulatory Reforms

-

-

2. MARKET SEGMENTATION

-

2.1 By Technology

-

2.1.1 Big Data Analytics

-

2.1.2 Mobility and Telecom

-

2.1.3 Cloud Computing

-

2.1.4 Storage

-

2.1.5 Business Process Outsourcing

-

2.1.6 Other Technologies

-

-

2.2 By Component

-

2.2.1 Hardware/Devices

-

2.2.2 Software and Services

-

2.2.3 Communication and Connectivity

-

-

2.3 By End-user Industry

-

2.3.1 Oil, Gas and Utilities

-

2.3.2 Travel and Hospitality

-

2.3.3 Healthcare

-

2.3.4 Financial Services

-

2.3.5 Manufacturing and Construction

-

2.3.6 Other End-user Industries

-

-

2.4 By Country

-

2.4.1 Saudi Arabia

-

2.4.2 United Arab Emirates

-

2.4.3 Qatar

-

2.4.4 Oman

-

2.4.5 Egypt

-

2.4.6 Rest of MENA

-

-

MENA ICT Market Size FAQs

How big is the MENA ICT Market?

The MENA ICT Market size is expected to reach USD 183.48 billion in 2024 and grow at a CAGR of 6.41% to reach USD 250.29 billion by 2029.

What is the current MENA ICT Market size?

In 2024, the MENA ICT Market size is expected to reach USD 183.48 billion.