MENA Information And Communications Technology (ICT) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 177.10 Billion |

| Market Size (2030) | USD 280.60 Billion |

| Growth Rate (2025 - 2030) | 9.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Information And Communications Technology (ICT) Market Analysis by Mordor Intelligence

The Middle East and North Africa ICT market size stands at USD 177.1 billion in 2025 and is forecast to reach USD 280.6 billion by 2030, reflecting a 9.64% CAGR. This growth is propelled by sovereign wealth-fund capital directed toward artificial intelligence and semiconductor projects, hyperscale cloud buildouts that satisfy emerging data-residency mandates, and 5G network rollouts that raise bandwidth demand across consumer and enterprise segments. Saudi Arabia and the UAE alone account for more than two-thirds of announced greenfield digital-infrastructure spending, reinforcing their roles as regional technology hubs. Government digital-transformation agendas amplify private-sector adoption of cloud, cybersecurity, and advanced analytics, while energy-subsidy reforms accelerate the shift toward renewable-powered data centers. Intensifying competition between global hyperscalers and regional telecom groups is reshaping pricing, service portfolios, and partnership models.

Key Report Takeaways

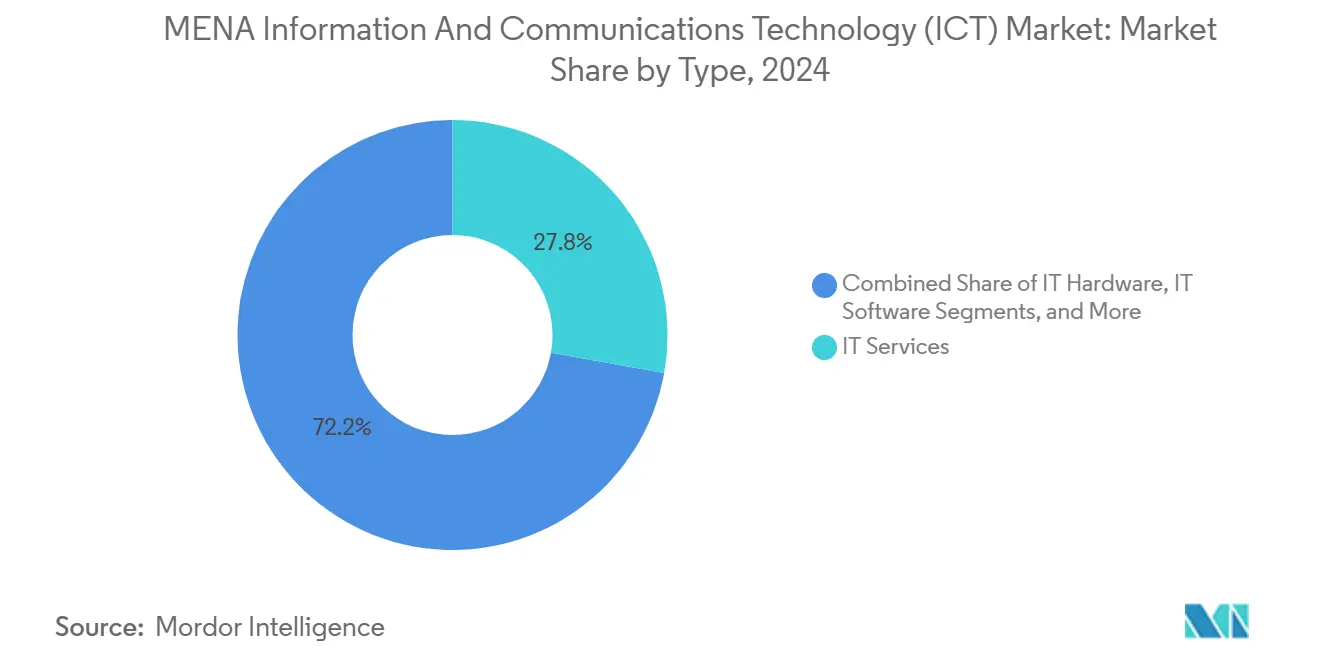

- IT Services led with 27.82% of the Middle East and North Africa ICT market share in 2024.

- Cloud Services are projected to expand at a 9.98% CAGR between 2025 and 2030, the fastest among all type segments.

- Large enterprises commanded 61.83% spending in 2024, while small and medium enterprises are advancing at a 10.12% CAGR through 2030.

- Cloud deployment held 45.76% share in 2024, yet hybrid architectures are forecast to grow at 11.06% CAGR to 2030.

- Government and public administration captured 16.79% revenue in 2024; gaming and esports are poised for a 12.34% CAGR, the highest among verticals.

- Saudi Arabia attracted more than USD 8.9 billion in committed hyperscale cloud investment during 2024 alone, the largest national inflow in the region.

MENA Information And Communications Technology (ICT) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led smart city mega-projects | +2.1% | Saudi Arabia, UAE, Qatar, Egypt | Medium term (2-4 years) |

| National digital-transformation agendas | +1.8% | GCC states, North Africa spillover | Long term (≥ 4 years) |

| Hyperscale cloud and data-center investments | +2.3% | Saudi Arabia, UAE, Egypt, Jordan | Short term (≤ 2 years) |

| 5G-driven mobile data-traffic explosion | +1.6% | GCC core, North Africa expansion | Medium term (2-4 years) |

| Sovereign-wealth AI and semiconductor funding | +1.4% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Data-residency mandates boosting local IaaS | +1.2% | GCC and Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-led Smart City Mega-projects

Saudi Arabia’s NEOM allocates USD 5 billion for technology platforms that integrate traffic, energy, and citizen-service systems; UAE’s Dubai 2040 Urban Master Plan targets AI delivery of 25% of government services by 2025. [1]Smart Dubai Government, “Digital Transactions Dashboard,” smartdubai.ae These initiatives generate recurring demand for cloud capacity, IoT sensors, and cybersecurity solutions well beyond initial construction cycles. Municipalities require interoperable platforms that aggregate data across transport, utilities, and public-safety domains, accelerating procurement of edge computing and analytics capabilities. GCC-level policy coordination enables vendor standardization, reducing integration costs for regional suppliers. Successful pilots, such as the 2.4 billion digital transactions processed under Smart Dubai, showcase scale economics that entice additional sovereign wealth-fund backing.

Hyperscale Cloud and Data-center Investments

Microsoft’s USD 2.1 billion Saudi data-center complex, Oracle’s USD 1.5 billion Riyadh region, and AWS’s USD 5.3 billion multi-year expansion validate the Middle East and North Africa ICT market as a priority for global providers. Local presence satisfies data-sovereignty regulations while cutting latency for enterprise workloads, spurring secondary demand for networking gear, managed services, and colocation space. The UAE’s AED 13 billion (USD 3.54 billion) sovereign-cloud partnership with Core42 extends the model to public-sector workloads, creating a blueprint other governments are adopting. Edge nodes are proliferating near population centers to support gaming, autonomous vehicles, and real-time analytics, further widening the infrastructure footprint.

5G-driven Mobile Data-traffic Explosion

Regional operators report 40-60% annual growth in data traffic as 5G services enable cloud gaming and AR applications. Saudi Telecom Company’s 5G network covers 65% of populated areas and generated USD 20.24 billion revenue in 2024. Average revenue per user in the UAE climbed 15-20% after unlimited 5G plans launched, reinforcing operator investment in small-cell densification and fiber backhaul. Private 5G networks for manufacturing and logistics amplify enterprise spending on mobile edge computing. Satellite partnerships with Starlink and Kuiper extend connectivity to remote locations, supporting agritech and oil-field monitoring use cases that were previously unserved.

National Digital-transformation Agendas

Saudi Arabia’s Vision 2030 mandates 80% digital delivery of public services, driving modernization across health, education, and municipal platforms. Egypt’s Digital Egypt 2030 program similarly prioritizes local content development and cloud adoption, stimulating demand for API management, identity federation, and cybersecurity tools. Compliance frameworks such as Saudi Arabia’s Personal Data Protection Law and the UAE Data Protection Law impose strict data-processing guidelines, creating a sustained market for encryption, audit, and privacy-enhancing technologies. As public-sector procurement often requires local data storage, multinational vendors partner with regional integrators to tailor solutions that meet sovereign criteria.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-skill shortages | -1.7% | Saudi Arabia, UAE, wider MENA | Short term (≤ 2 years) |

| Energy-subsidy reforms raising DC OPEX | -1.2% | Saudi Arabia, Egypt | Medium term (2-4 years) |

| Water-power nexus limiting North Africa DCs | -0.8% | Egypt, Morocco, Tunisia | Long term (≥ 4 years) |

| Political risk in Levant fiber corridors | -0.6% | Lebanon, Syria, Jordan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-skill Shortages

Unfilled cybersecurity positions grew 26.8% in Saudi Arabia and 9.7% in the UAE during 2024, despite double-digit workforce expansion, widening a regional talent gap that forces enterprises to delay cloud migrations or rely on costly consultants. [2]ISC2, “Cybersecurity Workforce Study 2024,” isc2.org Public-sector networks endure about 50,000 daily cyberattack attempts, yet 51% of security leaders cite under-funding as their main obstacle. University programs cannot keep pace with 3:1 demand-supply ratios for cloud-security architects and incident-response analysts. Government initiatives, including Saudi Arabia’s National Cybersecurity Authority scholarships, aim to close the gap within five years, but near-term shortages persist. This limits the speed at which enterprises adopt advanced, security-sensitive workloads such as multicloud analytics.

Energy-subsidy Reforms Raising DC OPEX

Saudi Arabia’s industrial power-tariff increase of 260% and Egypt’s phased subsidy removal have lifted electricity costs, which represent 60-70% of data-center operating expenses. Operators are accelerating adoption of solar PPAs, liquid-immersion cooling, and AI-powered workload scheduling to offset rising costs. Facilities with access to renewable energy secure competitive pricing advantages and capture colocation demand from price-sensitive hyperscalers. Smaller operators without scale or renewable options face margin compression, spurring consolidation. Energy reforms also catalyze green-energy investment, creating ancillary opportunities for EPC firms and battery-storage suppliers.

Segment Analysis

By Type: Services Integration Drives Cloud Migration

The IT Services segment accounted for 27.82% of the Middle East and North Africa ICT market in 2024, underscoring the need for integration expertise during complex cloud migrations. Accelerating demand for data-sovereignty compliant architectures positions system integrators and managed service providers as strategic partners to both hyperscalers and enterprises. The segment benefits from recurring revenue models tied to multiyear transformation programs, cybersecurity audits, and application modernization contracts. Rising adoption of platform-as-a-service solutions further expands advisory opportunities as organizations re-platform legacy workloads. Local providers differentiate through Arabic language support and familiarity with regional regulatory frameworks, creating barriers to entry for purely international consultancies.

Cloud Services recorded the highest growth trajectory at a 9.98% CAGR and are expected to narrow the revenue gap with IT Services by 2030. Establishment of sovereign cloud regions by Microsoft, Oracle, and AWS reduces latency and compliance hurdles, accelerating workload migration. Enterprises increasingly adopt multicloud strategies to avoid vendor lock-in, driving demand for orchestration tools and cost-optimization services. The surge in data-intensive applications such as AI model training and real-time analytics amplifies infrastructure-as-a-service consumption. Meanwhile, IT Hardware remains essential for 5G backhaul and edge-computing nodes, although its growth lags service-centric categories due to virtualization trends.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SME Cloud Adoption Accelerates

Large enterprises generated 61.83% of spending in 2024, leveraging scale to pursue end-to-end digital initiatives spanning ERP modernization, cybersecurity consolidation, and AI experimentation. This cohort secures preferential pricing from hyperscalers and telecom operators, reinforcing its procurement influence. Multinational corporations in the energy, aviation, and finance sectors anchor multi-region cloud deployments that uplift ancillary segments such as data-governance software and SD-WAN solutions.

Small and medium enterprises are set to outpace overall market growth with a 10.12% CAGR, underpinned by cloud-first policies that lower entry barriers to sophisticated software suites. UAE’s Mohammed Bin Rashid Innovation Fund and Saudi Arabia’s Kafalah program funnel capital toward technology upgrades that enable SMEs to fulfill electronic procurement mandates MBRF.AE. Software-as-a-service adoption among SMEs tripled since 2022, particularly in CRM, accounting, and endpoint-security tools. As supply-chain digitization deepens, large enterprises increasingly rely on SME tech vendors for niche AI, blockchain, and IoT capabilities, weaving smaller firms into regional ecosystems.

By Deployment Model: Hybrid Architectures Balance Control and Scalability

Cloud deployment captured 45.76% revenue in 2024 as enterprises prioritized operational agility over capital-intensive on-premises infrastructure. Data-residency mandates in Saudi Arabia, UAE, and Egypt compelled hyperscalers to launch local regions, reducing compliance friction and accelerating adoption. Cost optimization, elastic scaling, and global service catalogs remain the top cloud drivers across verticals.

Hybrid models are forecast to grow at 11.06% CAGR through 2030, reflecting the need to retain sensitive workloads on premises while leveraging cloud scalability for less regulated applications. Oracle’s sovereign cloud partnerships exemplify this approach by offering public-cloud services within local data centers that remain under government jurisdiction. [3]Oracle Newsroom, “Oracle Launches Sovereign Cloud Regions,” oracle.com Edge computing intensifies hybrid requirements, distributing compute near devices for latency-critical tasks such as autonomous-vehicle control and industrial automation. On-premises deployments persist for legacy systems and ultra-low-latency use cases, though spending shifts toward modernization rather than net-new capacity.

By End-user Industry Vertical: Gaming Disrupts Traditional Sectors

Government and public administration retained 16.79% share in 2024, driven by digital-service mandates across GCC countries. Projects span citizen portals, digital identity, and e-procurement platforms, anchoring demand for cybersecurity and sovereign cloud capacity. Budget allocations remain resilient, owing to fiscal surpluses from hydrocarbon revenues that finance diversification strategies.

Gaming and esports headline future growth with a 12.34% CAGR, fueled by Saudi Arabia’s USD 37.8 billion Savvy Games Group investment and a regional mobile-gaming revenue surge to USD 1.78 billion in the first half of 2024. [4]Savvy Games Group, “Investment Portfolio,” savvygames.com Low-latency cloud regions and 5G coverage catalyze mobile gaming adoption, while public-sector funding lowers entry barriers for local studios and tournament organizers. BFSI continues to modernize core banking and digital-wallet platforms amid stricter data-protection laws, while energy, manufacturing, healthcare, and retail increasingly embed IoT, AI, and analytics into operational workflows, diversifying vendor opportunities across the Middle East and North Africa ICT market.

Geography Analysis

Saudi Arabia leads the Middle East and North Africa ICT market through Vision 2030 programs that attracted Microsoft, Oracle, and AWS commitments exceeding USD 8.9 billion. These projects establish localized cloud availability zones, incentivize domestic chipset manufacturing, and finance talent-development academies. Telecom operator STC posted USD 20.24 billion revenue and 85.7% profit growth in 2024, reflecting robust demand for 5G and enterprise-connectivity solutions.

The UAE maintains gateway status by coupling foreign-investment openness with sovereign data-protection laws that reassure multinationals. The USD 3.54 billion Core42-Microsoft sovereign cloud guides federal workloads, while the USD 1.5 billion Microsoft-G42 AI partnership drives semiconductor research. Qatar, Oman, and Bahrain replicate this mix of cloud incentives and digital-government targets, though on smaller scales.

North African markets are anchored by Egypt, whose Digital Egypt 2030 plan stimulates local software development and data-center builds that serve Pan-African connectivity corridors. Political risk and water-power constraints temper Morocco and Tunisia’s data-center attractiveness, yet their proximity to Europe sustains BPO and nearshore service growth. Levantine fiber routes face geopolitical disruptions that elevate redundancy costs, steering hyperscalers toward submarine-cable paths through the Red Sea and Arabian Gulf.

Competitive Landscape

Hybrid dynamics characterize competition as hyperscale cloud providers vie with incumbent telecom operators and emerging local specialists. Microsoft Azure, AWS, and Oracle advance regional footprints via multibillion-dollar data-center builds, capturing enterprise cloud spend while enabling compliance with data-residency rules. Telecom groups STC, Etisalat, and Ooredoo leverage extensive customer bases and spectrum assets to bundle connectivity, edge computing, and managed security, preserving their role in value chains.

Partnership strategies dominate over direct confrontation. Microsoft aligned with UAE-based G42 on AI infrastructure, while Oracle’s sovereign-cloud agreements embed regional governments into its go-to-market model. Such alliances distribute regulatory risk and accelerate client acquisition. Cybersecurity, edge solutions, and industry-specific SaaS remain fragmented, offering entry points for regional scale-ups and specialized consultancies.

Gaming and esports introduce a new axis of competition. Saudi Arabia’s Savvy Games Group finances publishing, infrastructure, and event ecosystems that attract global studios seeking local reach. Telecom operators monetize low-latency 5G networks through cloud-gaming platforms, while hyperscalers provide scalable backend services, creating multi-layered rivalries. Across segments, firms that master compliance, localization, and renewable-energy sourcing secure enduring advantages within the Middle East and North Africa ICT market.

MENA Information And Communications Technology (ICT) Industry Leaders

Google LLC (Alphabet Inc.)

IBM Corporation

Microsoft Corporation

HP Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Saudi Arabia’s Crown Prince met AWS, Scale AI, IBM, Sony, and OpenAI at the World Economic Forum, reinforcing state support for AI projects.

- December 2024: Microsoft finished construction of its USD 2.1 billion Saudi data-center complex, with operations slated for 2026.

- November 2024: Oracle quintupled its Abu Dhabi investment to expand cloud capacity and partner network.

- October 2024: Abu Dhabi’s sovereign-cloud initiative with Microsoft and Core42 secured AED 13 billion (USD 3.54 billion) funding through 2027.

MENA Information And Communications Technology (ICT) Market Report Scope

The MENA ICT market includes the amalgamation and adoption of different Information and Communications Technologies (ICT), such as big data, mobility, storage, outsourcing, and cloud computing in MENA for the purpose of digitization and digital transformation. It tracks the revenue accrued through the sale of technology-related solutions.

The MENA ICT market is segmented by technology (big data analytics, mobility and telecom, cloud computing, storage, business process, and outsourcing), component (hardware/devices, software and services, and communication and connectivity), end-user industry (oil, gas and utilities, travel and hospitality, healthcare, financial services, and manufacturing and construction), and country (Saudi Arabia, United Arab Emirates, Qatar, Oman, Egypt, and Rest of MENA). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Egypt |

| Rest of MENA |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Egypt | ||

| Rest of MENA | ||

Key Questions Answered in the Report

How large is the Middle East and North Africa ICT market in 2025?

The Middle East and North Africa ICT market size is USD 177.1 billion in 2025 and is projected to reach USD 280.6 billion by 2030.

Which segment is growing fastest within regional ICT spending?

Cloud Services post the fastest trajectory with a 9.98% CAGR through 2030, supported by sovereign data-center launches.

Why are hybrid deployment models gaining traction?

Enterprises balance regulatory data-locality rules with cloud scalability, pushing hybrid architectures to an 11.06% CAGR forecast.

What is the primary restraint on digital-infrastructure expansion?

A widening cybersecurity talent shortage is delaying sensitive cloud projects despite strong government upskilling programs.

Which country attracts the most hyperscale investment?

Saudi Arabia leads with more than USD 8.9 billion in announced cloud-region capital commitments from Microsoft, Oracle, and AWS.

How fast is gaming revenue expanding across MENA?

Gaming and esports are expected to grow at a 12.34% CAGR through 2030, driven by sovereign investment and widespread 5G access.