| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 7.61 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

MENA Architectural Services Market Analysis

The MENA Architectural Services Market is expected to register a CAGR of 7.61% during the forecast period.

The MENA architectural services landscape is experiencing an unprecedented transformation driven by ambitious infrastructure development initiatives and economic diversification programs. Saudi Arabia has emerged as a dominant force in the regional architectural services sector, demonstrated by its significant market presence and extensive development pipeline. The construction sector has witnessed remarkable growth, with Saudi Arabia alone recording USD 51.3 billion worth of awarded contracts in 2022, representing a 35% increase compared to the previous year. This surge in construction activities has created substantial opportunities for architectural firms, particularly in developing innovative urban spaces and integrated communities.

The industry is witnessing a paradigm shift in architectural planning through the integration of advanced digital technologies and software solutions. Building Information Modeling (BIM) has become increasingly prevalent, offering advantages over traditional paper-based design and CAD systems. The emergence of 4D BIM software, virtual reality (VR), and augmented reality (AR) technologies has revolutionized how architects communicate designs to clients and stakeholders. These technological advancements have enabled more precise geometric modeling, improved project visualization, and enhanced collaboration among project stakeholders.

Urban development across the MENA region is increasingly focused on creating sustainable, smart cities that integrate advanced technologies with traditional architectural elements. In July 2023, a landmark agreement between the United States and the United Arab Emirates committed USD 100 billion toward sustainable energy projects, aiming to install 100 gigawatts globally by 2035. This initiative reflects the region's broader commitment to sustainable architecture and demonstrates the growing emphasis on incorporating environmental considerations into architectural design and urban planning processes.

The market is experiencing significant transformation through increased international collaboration and investment. The Ministry of Investment of Saudi Arabia reported the issuance of over 3,300 new foreign investment licenses, marking a substantial annual increase. This surge in foreign investment has been particularly pronounced in the architectural design sector, driven by major development projects such as NEOM city and other urban transformation initiatives. These investments have not only attracted international architectural expertise but have also fostered innovation in design approaches and construction methodologies, contributing to the region's architectural technology evolution and economic diversification goals.

MENA Architectural Services Market Trends

Increasing Demand for Green Building

The growing emphasis on green building design services has become a fundamental driver in the MENA architectural services market, driven by increasing environmental consciousness and regulatory support. Green construction materials are gaining prominence for their ability to consume less water, require minimal maintenance, and significantly reduce carbon emissions compared to traditional materials. According to ESCWA projections, the Arab building sector is expected to achieve a reduction of 8.8 million tons in carbon emissions annually by 2030 through improved lighting technology alone. This transformation is particularly evident in major infrastructure developments across the region, where sustainable architecture practices are being integrated into both residential and non-residential structures.

The demand for green building design is further amplified by multiple tangible benefits, including improved building efficiency, reduced operational costs, and enhanced occupant well-being. Major developments like the ROSHN projects in Riyadh and Jeddah exemplify this trend, incorporating sustainable design principles while working towards Saudi Arabia's Vision 2030 goal of increasing home ownership to 70%. Other significant projects embracing sustainable architecture practices include the King Abdullah Financial District, Kingdom City, and Jazan Economic City, all of which are encouraging large-scale investments in sustainable construction. These developments are driving architectural firms to innovate in areas such as energy-efficient design, sustainable material selection, and environmental impact reduction strategies.

Understand The Key Trends Shaping This Market

Download PDF

Adoption of 3D Printing

The architectural services market in MENA is experiencing a revolutionary transformation through the increasing adoption of 3D printing technology, which is significantly reducing construction timelines and costs while enabling more complex architectural design. A landmark achievement in this space was demonstrated by Apis Cor in July 2022, with the completion of Dubai Municipality's record-breaking 3D-printed building, featuring a height of 9.5 meters and a surface area of 640 square meters. This two-story structure, built entirely on-site without requiring additional assembly, showcases the practical application and efficiency of 3D printing technology in modern construction.

The integration of 3D printing is being further enhanced through its combination with other advanced technologies such as artificial intelligence, cloud computing, and IoT, particularly in smart city developments. This technological convergence is evident in Saudi Arabia's National Transformation Program (NTP) and the National Industrial Development and Logistics Program (NIDLP), which are actively incorporating Industry 4.0 technologies to improve construction efficiency and building performance. The technology is proving particularly valuable in healthcare architecture, where AI algorithms are being leveraged to create efficient interior and exterior designs, as demonstrated in projects like the 370,000m² Mersin Integrated Health Campus, which optimizes patient-centered care through innovative design approaches. Additionally, 3D architectural visualization is enhancing the precision and creativity of building design services, further driving the adoption of construction design services across the region.

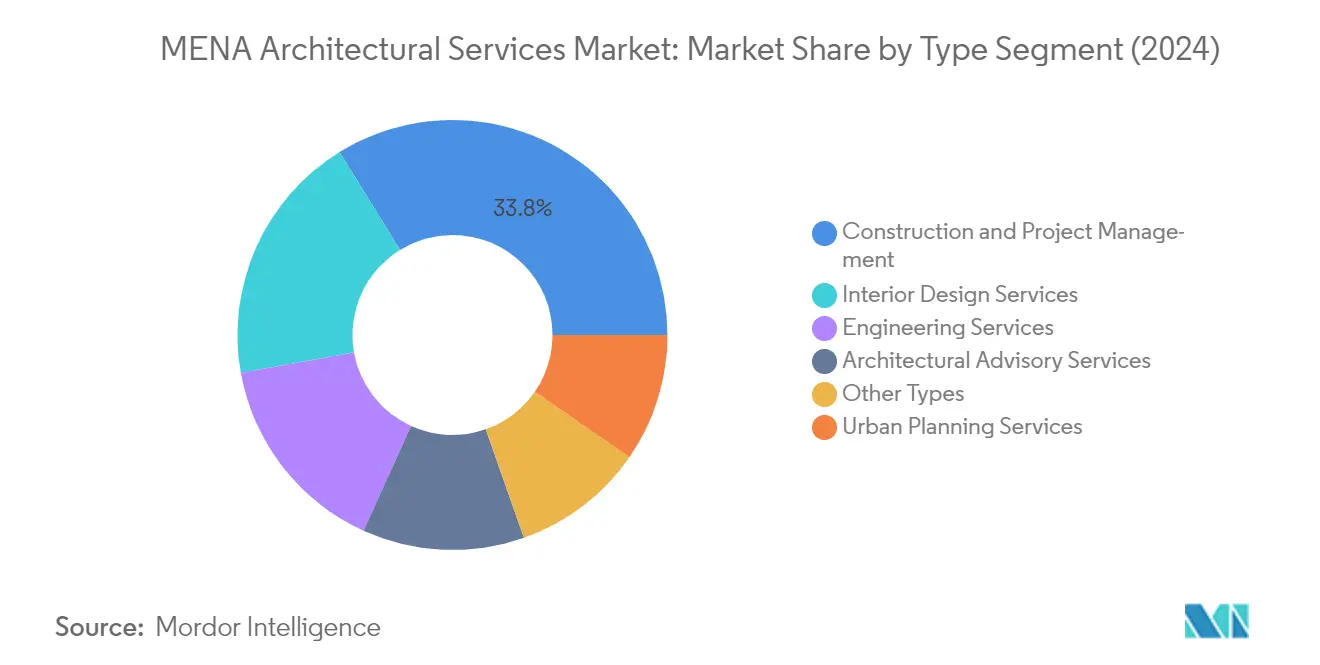

Segment Analysis: By Type

Construction and Project Management Segment in MENA Architectural Services Market

The Construction and Project Management segment dominates the MENA architectural services market, holding approximately 34% market share in 2024. This segment's prominence is driven by massive infrastructure developments across the region, particularly in the UAE, where projects like the Dubai Municipality showcase innovative construction techniques, including 3D printing. The segment's leadership position is reinforced by significant public and private sector investments in smart city initiatives, sustainable building projects, and urban development programs. Architectural project management services have become increasingly critical as projects grow in complexity, requiring sophisticated oversight of procurement processes, contractor relationships, and project lifecycle management.

Interior Design Services Segment in MENA Architectural Services Market

The Interior Design Services segment is emerging as the fastest-growing segment in the MENA architectural services market, with a projected growth rate of approximately 7% from 2024 to 2029. This accelerated growth is primarily driven by increasing demand for sustainable and smart interior architecture solutions, particularly in commercial and residential sectors. The segment is witnessing significant innovation through the integration of IoT technologies, smart home systems, and sustainable materials. The growth is further supported by the rising focus on creating unique, culturally informed spaces that blend contemporary design with traditional Arabic elements, especially in luxury developments and commercial spaces across the region.

Remaining Segments in MENA Architectural Services Market

The other significant segments in the MENA architectural services market include Engineering Services, Urban Planning Services, and Architectural Advisory Services, each playing vital roles in shaping the region's architectural landscape. Engineering Services contribute technical expertise in structural and systems design, while Urban Planning Services focus on creating sustainable and efficient city layouts. Architectural Advisory Services provide strategic consultation for project development and sustainability compliance. These segments collectively support the market's comprehensive service offering, with each bringing specialized expertise in areas such as sustainable design, technological integration, and cultural preservation.

Segment Analysis: By End User

Institutional and Public Segment in MENA Architectural Services Market

The Institutional and Public segment dominates the MENA architectural services market, commanding approximately 65% market share in 2024, while also maintaining the highest growth trajectory. This segment's prominence is driven by massive infrastructure developments and smart city initiatives across the region, particularly in the UAE and Saudi Arabia. The segment encompasses various projects, including government buildings, educational institutions, and urban development initiatives. The development of smart cities remains a key focus area, especially in countries like Saudi Arabia, where projects such as NEOM demonstrate the region's commitment to innovative urban solutions. The integration of digital technologies such as cloud computing, big data, Internet of Things (IoT), and AI in institutional projects has further strengthened this segment's position. Public-private partnerships and government funding continue to fuel growth, with significant investments in transportation infrastructure, public facilities, and smart city developments.

Retail Segment in MENA Architectural Services Market

The retail segment represents a significant opportunity in the MENA architectural services market, particularly with the evolution of retail spaces from traditional malls to lifestyle-led developments. The segment is witnessing a transformation in design approaches, with increasing focus on creating experiential spaces that combine shopping with entertainment and leisure activities. Modern retail architectural projects are incorporating advanced technologies for enhanced customer experiences, including smart lighting, digital wayfinding systems, and interactive displays. The trend towards sustainable retail spaces has gained momentum, with architects integrating green building practices and energy-efficient designs. The rise of mixed-use developments and the integration of retail spaces within residential communities has created new opportunities for innovative architectural solutions. Additionally, the post-pandemic shift in consumer behavior has led to the redesign of retail spaces to accommodate both physical and digital retail experiences.

Remaining Segments in MENA Architectural Services Market

The Healthcare and Other End Users segments continue to play vital roles in shaping the MENA architectural services market. The healthcare segment is experiencing significant transformation with the integration of advanced technologies and sustainable design principles in medical facilities. Healthcare projects are increasingly focusing on patient-centric designs, incorporating healing environments and efficient space utilization. The Other End Users segment, which includes residential and industrial projects, contributes to market diversity through specialized architectural requirements. This segment has seen growing demand for sustainable residential developments and state-of-the-art industrial facilities. Both segments are characterized by increasing adoption of smart technologies, sustainable practices, and innovative design solutions that cater to specific end-user requirements.

MENA Architectural Services Market Geography Segment Analysis

MENA Architectural Services Market in Saudi Arabia

Saudi Arabia dominates the MENA architectural services landscape, commanding approximately 48% of the market share in 2024 and demonstrating remarkable growth potential with a projected CAGR of nearly 9% from 2024 to 2029. The kingdom's architectural services sector is experiencing unprecedented transformation driven by ambitious initiatives like NEOM city and the Red Sea Project. The country's commitment to sustainable urban development and smart city initiatives has created extensive opportunities for architectural design firms specializing in innovative and environmentally conscious designs. The integration of advanced technologies, including 3D printing and artificial intelligence in architectural design, reflects Saudi Arabia's forward-thinking approach. The government's focus on developing tourism infrastructure, healthcare facilities, and educational institutions has further diversified the demand for architectural services, while the emphasis on affordable housing through various government programs continues to drive residential architecture projects.

MENA Architectural Services Market in UAE

The United Arab Emirates stands as a pioneering force in architectural services innovation across the MENA region, with Dubai and Abu Dhabi leading transformative urban development initiatives. The country's architectural services sector is characterized by its embrace of sustainable design principles and smart building technologies. The UAE's commitment to green building practices has become a cornerstone of its architectural development, with numerous projects incorporating energy-efficient designs and sustainable materials. The integration of biophilic design elements in commercial architecture and residential projects reflects the growing emphasis on creating harmonious connections between built environments and nature. The country's architectural landscape continues to evolve with the implementation of advanced construction technologies and innovative design approaches, supported by robust government initiatives promoting sustainable urban development and smart city solutions.

MENA Architectural Services Market in Egypt

Egypt's architectural services market is undergoing significant transformation, driven by extensive infrastructure development and urban renewal initiatives. The country's architectural landscape is witnessing a unique blend of modern design principles while preserving its rich cultural heritage. The development of new administrative capitals and smart cities has created substantial opportunities for urban planning services firms specializing in large-scale urban planning. Egypt's focus on sustainable development has led to increased demand for green building designs and energy-efficient solutions. The country's architectural firms are increasingly adopting digital technologies and innovative design approaches to meet the evolving needs of both public and private sector projects. The healthcare and education sectors have emerged as significant drivers of architectural services, with numerous projects focusing on developing state-of-the-art facilities across the country.

MENA Architectural Services Market in Other Countries

The architectural services market in other MENA countries, particularly Jordan, continues to evolve with unique regional characteristics and development priorities. These markets are characterized by a growing emphasis on sustainable design practices and the integration of cultural elements in modern architecture. The focus on developing tourism infrastructure and public facilities has created diverse opportunities for architectural firms. These countries are increasingly adopting international best practices while maintaining their distinct architectural identity. The trend towards smart city development and sustainable urban planning is gaining momentum across these markets. Regional cooperation and knowledge sharing among architectural firms have fostered innovation and the adoption of new technologies. The emphasis on developing affordable housing solutions and community-centric designs reflects the region's commitment to sustainable urban development.

Get Analysis on Important Geographic Markets

Download PDF

MENA Architectural Services Industry Overview

Top Companies in MENA Architectural Services Market

The MENA architectural services market features prominent players like AECOM, DSA Architects International, HKS Inc., RMJM Inc., Omrania, and Khatib & Alami leading innovation and market development. Companies are increasingly focusing on sustainable design practices and green building solutions, incorporating advanced technologies like Building Information Modeling (BIM) and digital visualization tools to enhance project delivery efficiency. Strategic partnerships with local firms and expansion into emerging market segments have become key growth drivers, while investments in smart city projects and urban development initiatives demonstrate operational agility. Firms are diversifying their service portfolios to include specialized offerings such as healthcare facility design, retail space planning, and sustainable urban development, while simultaneously strengthening their digital capabilities through investments in artificial intelligence, virtual reality, and automated design tools. The market is witnessing a shift towards integrated service delivery models, where firms combine architectural expertise with project management and sustainability consulting to provide comprehensive solutions to clients.

Market Structure Shows Dynamic Regional Evolution

The MENA architectural services market exhibits a fragmented structure with a mix of global architectural firms and regional specialists competing for market share. International conglomerates leverage their extensive experience and technological capabilities to secure large-scale projects, while local firms capitalize on their deep understanding of regional preferences and regulatory requirements. The market is characterized by increasing consolidation through strategic partnerships and acquisitions, as evidenced by significant moves such as Omrania joining the Egis Group and Engineering Consultants Group partnering with the Dorsch Group. These consolidations are driven by the need to enhance service capabilities, expand geographical presence, and strengthen competitive positions in key market segments.

The competitive dynamics are further shaped by the presence of specialized boutique firms focusing on niche segments such as sustainable design, cultural preservation, and smart city development. Market participants are increasingly pursuing joint ventures and collaborative arrangements to combine complementary strengths and address the growing complexity of architectural projects in the region. The trend towards consolidation is particularly pronounced in markets like Saudi Arabia and the UAE, where large-scale development projects and government initiatives are driving demand for comprehensive architectural services. This evolution is accompanied by increasing investment in talent development, technological infrastructure, and service innovation to meet evolving client requirements and maintain competitive advantages.

Innovation and Sustainability Drive Future Success

Success in the MENA architectural services market increasingly depends on firms' ability to integrate sustainable design practices, technological innovation, and local cultural considerations into their service offerings. Incumbent firms are strengthening their market positions by investing in digital transformation initiatives, developing specialized expertise in emerging sectors like healthcare and smart cities, and building strong relationships with key stakeholders including government entities and private developers. The ability to deliver integrated solutions that combine architectural excellence with environmental sustainability and cultural sensitivity has become a critical differentiator, while firms are also focusing on developing robust project management capabilities and expanding their service portfolios to capture new growth opportunities.

Market contenders are gaining ground by focusing on niche specializations, leveraging technological innovations, and building strategic partnerships with established players. The increasing emphasis on sustainable development and green building practices presents opportunities for firms to differentiate themselves through specialized expertise and innovative solutions. Regulatory requirements related to environmental sustainability and building safety are becoming more stringent, creating opportunities for firms with strong compliance capabilities and sustainable design expertise. The concentration of end-users in government and large-scale private sector projects necessitates strong relationship management capabilities and the ability to deliver complex, integrated solutions. While substitution risk remains relatively low due to the specialized nature of architectural consulting, firms must continuously innovate and adapt to changing market requirements to maintain their competitive positions.

MENA Architectural Services Market Leaders

-

DSA Architects Intl

-

HKS Inc.

-

U+A

-

AECOM

-

RMJM Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

MENA Architectural Services Market News

- September 2023: Henning Larsen announced that it is working on creating a home specially designed for climate-resilient moss. The moss has the ability to create naturally resilient cities. It has one of the finest air cleaning and oxygenating competencies of any other plant. It can also absorb and digest fine dust, transforming particles into harmless and natural biomass. Such innovations are anticipated to help developing cities combat pollution.

- March 2023: Omrania will join the Egis Group, a leading global engineering, consulting, and operations firm. The acquisition marks a considerable step forward for both firms in forming an opportunity to leverage their collective footprint and client base to reach a significant scale in Saudi Arabia and strengthen their merged position to help achieve the country's Vision 2030 goals. Omrania and Egis marked a definitive agreement at the Ministry of Investment in Riyadh on March 8, 2023. Omrania's management and operations will continue uninterrupted. The group will continue to serve clients in the same dedicated manner as always, building on its record of excellence. With the addition of almost 700 professionals from Omrania, Egis is anticipated to grow to over 3,000 people in the Middle East.

Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Key Market Drivers

- 4.2.1 Increasing Demand for Green Buildings

- 4.2.2 Adoption of 3D Printing

-

4.3 Market Challenges

- 4.3.1 Lack of New Skills and Knowledge in Designing

- 4.4 Analysis of the Construction Industry in the MENA Region

- 4.5 Market Opportunity Analysis for Architectural Services

5. MARKET SEGMENTATION - UAE ARCHITECTURAL SERVICES

-

5.1 By Type

- 5.1.1 Interior Design Services

- 5.1.2 Engineering Services

- 5.1.3 Construction and Project Management

- 5.1.4 Urban Planning Services

- 5.1.5 Architectural Advisory Services

- 5.1.6 Other Types

-

5.2 By End User

- 5.2.1 Institutional and Public

- 5.2.2 Retail

- 5.2.3 Healthcare

- 5.2.4 Other End Users

6. MARKET SEGMENTATION - SAUDI ARABIA ARCHITECTURAL SERVICES

-

6.1 By Type

- 6.1.1 Interior Design Services

- 6.1.2 Engineering Services

- 6.1.3 Construction and Project Management

- 6.1.4 Urban Planning Services

- 6.1.5 Architectural Advisory Services

- 6.1.6 Other Types (Residential (Multi-House), Industrial, etc.)

-

6.2 By End User

- 6.2.1 Institutional and Public (includes Smart Cities and Urban Planning)

- 6.2.2 Retail

- 6.2.3 Healthcare

- 6.2.4 Other End Users

7. MARKET SEGMENTATION - EGYPT ARCHITECTURAL SERVICES

-

7.1 By Type

- 7.1.1 Interior Design Services

- 7.1.2 Engineering Services

- 7.1.3 Construction and Project Management

- 7.1.4 Urban Planning Services

- 7.1.5 Architectural Advisory Services

- 7.1.6 Other Types (Residential (Multi-House), Industrial, etc.)

-

7.2 By End User

- 7.2.1 Institutional and Public (includes Smart Cities and Urban Planning)

- 7.2.2 Retail

- 7.2.3 Healthcare

- 7.2.4 Other End Users

8. MARKET SEGMENTATION - JORDAN ARCHITECTURAL SERVICES

- 8.1 Market Overview

- 8.2 Key Trend Analysis

- 8.3 Future Outlook

9. COMPETITIVE LANDSCAPE

-

9.1 Company Profiles

- 9.1.1 DSA Architects Intl

- 9.1.2 HKS Inc.

- 9.1.3 U+A

- 9.1.4 AECOM

- 9.1.5 RMJM Inc.

- 9.1.6 Lacasa Architects & Engineering Consultants

- 9.1.7 Henning Larsen

- 9.1.8 Saudi Architects

- 9.1.9 Naga Architects

- 9.1.10 SaudConsult

- 9.1.11 Omrania

- 9.1.12 Keo International Consultants

- 9.1.13 Engineering Consultants Group

- 9.1.14 Sabbour Consulting

- 9.1.15 Khatib & Alami

- 9.1.16 EHAF Consulting Engineers

- 9.1.17 M T Architects

- 9.1.18 Modern Architectural Design

- 9.1.19 Mounir Hajjiri & Associates (Hajjiri Group)

- 9.1.20 Tahhan and Bushnaq

- 9.1.21 Farris & Farris Architects

- 9.1.22 DARB Architects & Engineers

- *List Not Exhaustive

10. INVESTMENT ANALYSIS

**Subject to Availability

Competitive Landscape is segmented into architectural firms operating in UAE, Saudi Arabia, Egypt, and Jordan, respectively, in the Final Study.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

MENA Architectural Services Industry Segmentation

Architectural services include feasibility studies, architectural programming, and project management with the help of design, preparation of construction documents, and construction administration.

The MENA architectural services market is segmented by country into UAE (by type (interior design services, engineering services, construction and project management, urban planning services, architectural advisory services, and other types) and by end user (institutional and public, retail, healthcare, and other end users)), Saudi Arabia (by type (interior design services, engineering services, construction and project management, urban planning services, architectural advisory services, and other types) and by end user (institutional and public (includes smart cities and urban planning), retail, healthcare, and other end users)), Egypt (by type (interior design services, engineering services, construction and project management, urban planning services, architectural advisory services, and other types) and by end user (institutional and public (includes smart cities and urban planning), retail, healthcare, and other end users)), and Jordan. The market sizes and forecasts are provided in terms of value in USD for all the above segments.

Need A Different Region or Segment?

Customize Now

Frequently Asked Questions

What is the current undefined size?

The undefined is projected to register a CAGR of 7.61% during the forecast period (2025-2030)

Who are the key players in undefined?

DSA Architects Intl, HKS Inc., U+A, AECOM and RMJM Inc. are the major companies operating in the undefined.

What years does this undefined cover?

The report covers the undefined historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the undefined size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

MENA Architectural Services Market Research

Mordor Intelligence provides a comprehensive analysis of the architectural services industry. We leverage our expertise in the architectural design and architectural engineering sectors. Our extensive research covers areas such as landscape architecture, interior architecture, and emerging trends in sustainable architecture. The report, available as an easy-to-download PDF, offers detailed insights into building information modeling (BIM) implementation, architectural planning strategies, and advancements in architectural technology across the MENA region.

Stakeholders gain valuable insights into developments in residential architecture and commercial architecture. This is supported by an analysis of expert design consultation services. The report examines building architecture trends, architectural rendering techniques, and building consultation practices. It also highlights innovations in green building design and 3D architectural visualization. Our research encompasses architectural documentation, architectural project management, building design services, and architectural drafting services. Additionally, it provides comprehensive coverage of architectural consulting, urban planning services, construction design services, and building planning services across the MENA region.