Medical Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

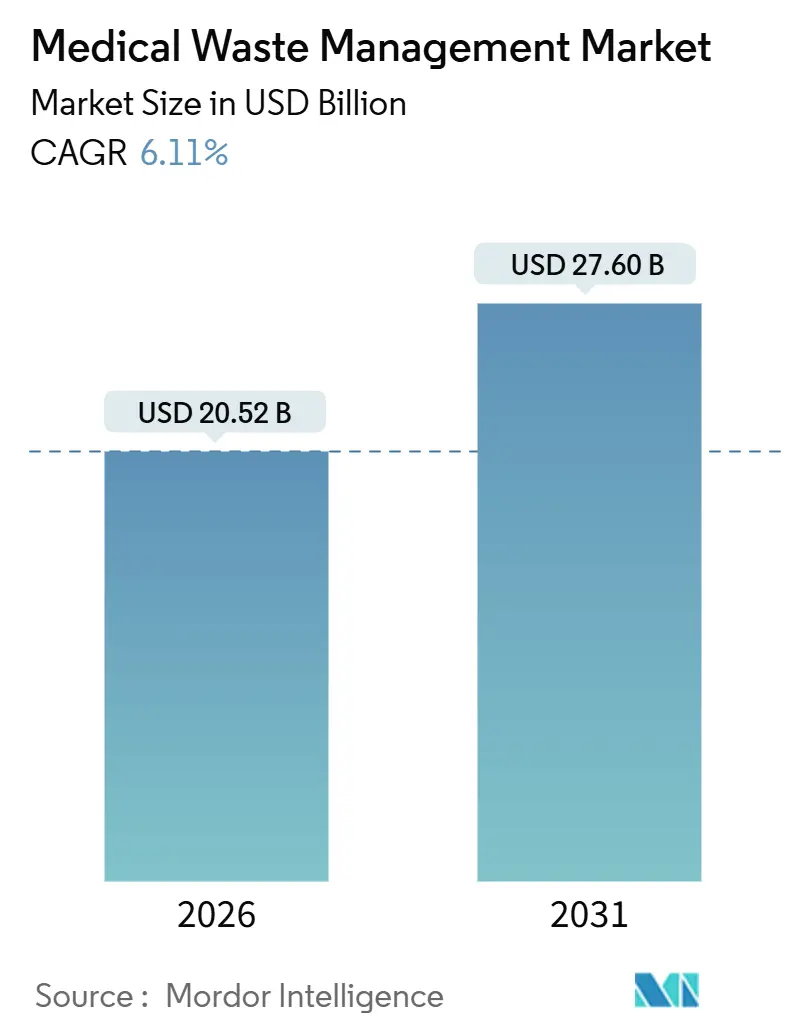

| Market Size (2026) | USD 20.52 Billion |

| Market Size (2031) | USD 27.60 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

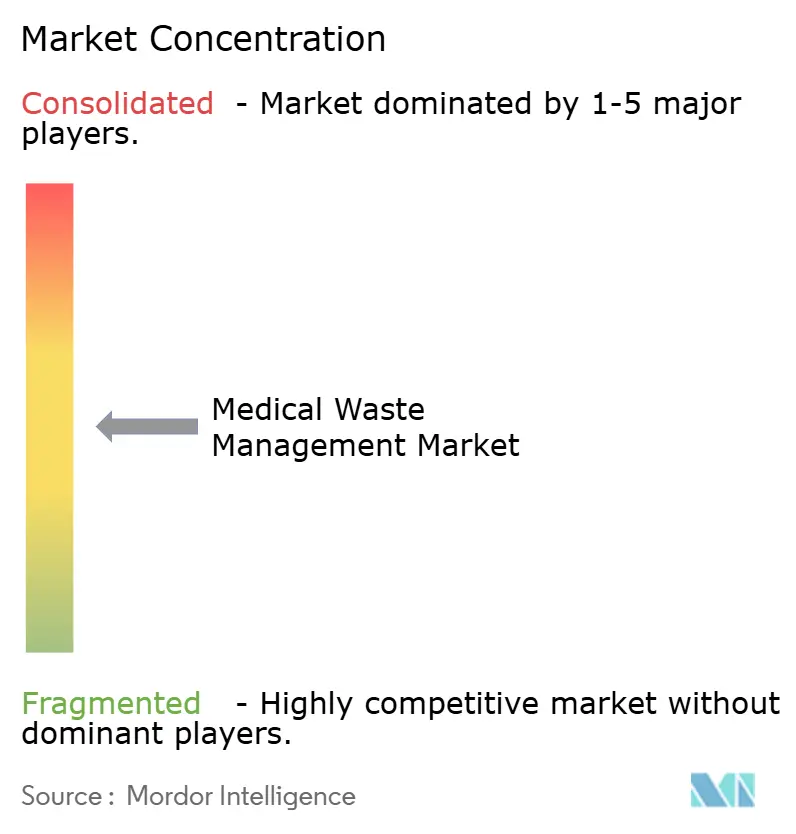

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Waste Management Market Analysis by Mordor Intelligence

The Medical Waste Management Market size is estimated at USD 20.52 billion in 2026, and is expected to reach USD 27.60 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031).

Rising biomedical waste volumes, stricter disposal regulations, and widening outsourcing adoption continue to propel the medical waste management market, while evolving ESG disclosure rules pressure service providers to quantify emissions. Consolidation—highlighted by Waste Management’s USD 7.2 billion purchase of Stericycle—signals a shift toward integrated environmental services, yet margin pressure persists where municipal buyers renegotiate pricing. Europe’s circular-economy mandates and California’s recycled-content laws are pushing recycling penetration, whereas digitized manifests in China and India create demand for IoT-enabled tracking solutions. Competitive differentiation is shifting from sheer route density to data transparency, onsite treatment innovation, and closed-loop recycling programs.

Key Report Takeaways

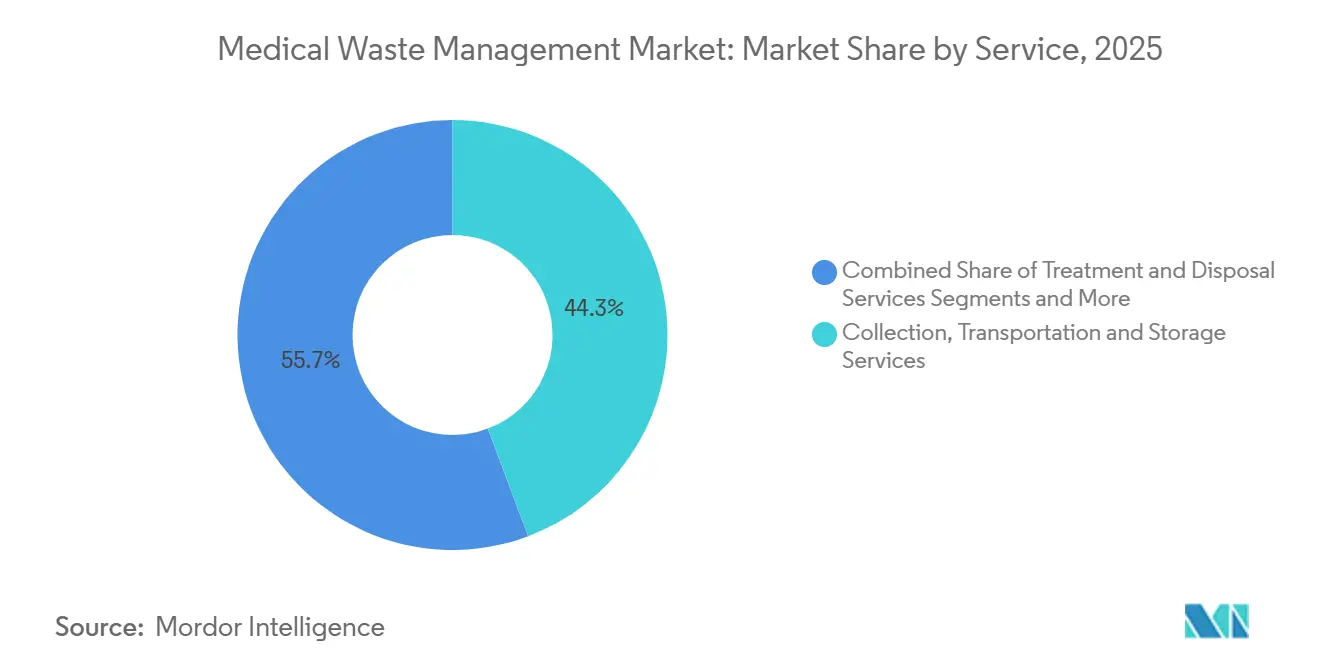

- By service, collection, transportation & storage led with a 44.26% revenue share in 2025; recycling is projected to expand at an 8.64% CAGR through 2031.

- By type of waste, non-hazardous streams accounted for 81.56% of volume in 2025, while infectious & pathological waste is forecast to grow at a 10.06% CAGR through 2031.

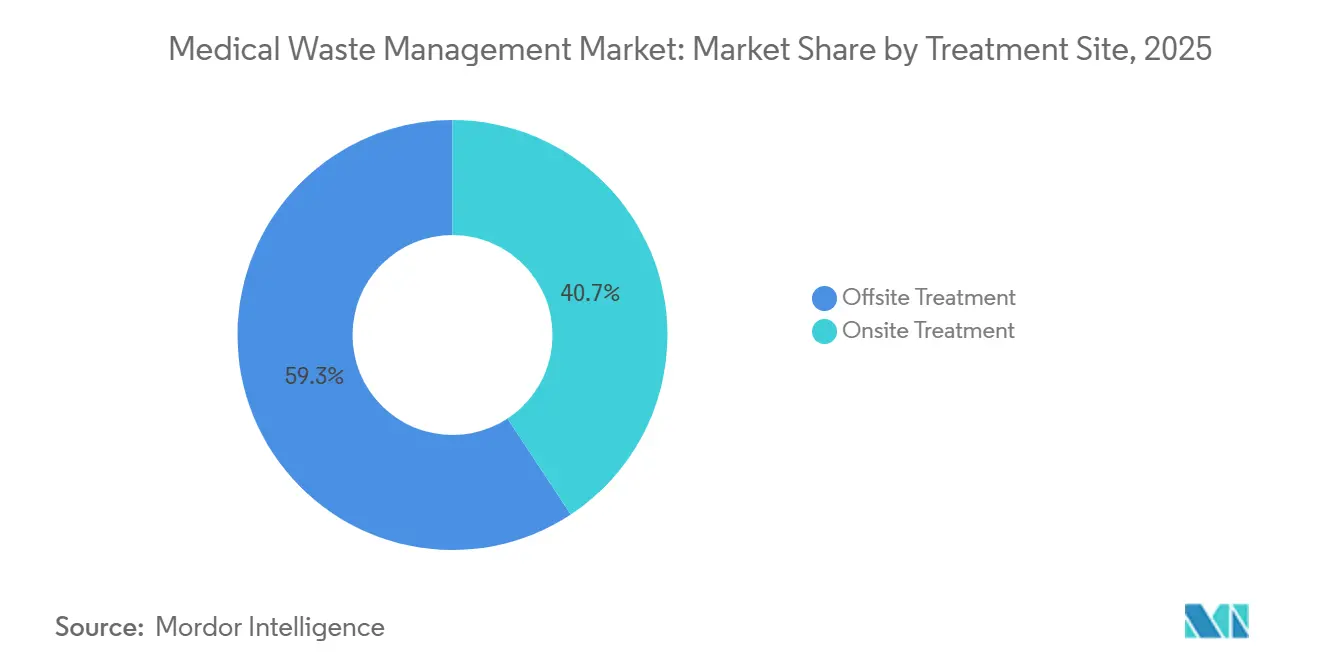

- By treatment site, offsite facilities held 59.27% share in 2025; onsite autoclave & microwave systems are expected to advance at a 9.91% CAGR to 2031.

- By waste generator, hospitals & diagnostic laboratories produced 61.63% of waste in 2025, while pharmaceutical & biotechnology companies are slated for an 8.85% CAGR through 2031.

- By geography, North America captured 31.76% of revenue in 2025, whereas Asia-Pacific is set to accelerate at a 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Waste Management Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume of healthcare and biomedical waste | +1.2% | Global, with acute pressure in APAC and MEA | Medium term (2-4 years) |

| Stringent multi-jurisdictional disposal regulations | +1.0% | North America, EU, China, India | Long term (≥ 4 years) |

| Outsourcing to specialized third-party service providers | +0.9% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Decentralized home-care and point-of-care diagnostics waste surge | +0.7% | North America, EU, Japan, Australia | Short term (≤ 2 years) |

| Biotech and cell-therapy manufacturing contamination-risk waste | +0.6% | North America, EU, Singapore, South Korea | Long term (≥ 4 years) |

| IoT-enabled traceability and ESG-reporting demand | +0.5% | Global, led by EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Healthcare and Biomedical Waste

Global healthcare facilities generated about 2.6 million metric tons of waste in 2025, and the World Health Organization projects a 15% rise by 2030 as emerging-market bed capacity expands.[1]World Health Organization, “Health-Care Waste Fact Sheet,” WHO, who.intIndia alone added 150,000 beds in 2024, adding 82,000 metric tons of new waste streams annually. Tier-1 Chinese hospitals reported a 12% jump in infectious waste in 2025 due to rising chemotherapy and imaging volumes. These surges strain permitted treatment capacity, where new incinerator licensing often exceeds three years. Resulting spot-market price spikes encourage hospitals to explore onsite sterilization to hedge against haulage shortages.

Stringent Multi-Jurisdictional Disposal Regulations

The U.S. EPA’s 2024 revision of 40 CFR Part 60 cut particulate limits to 0.015 gr/dscf, forcing 18 incinerators to invest up to USD 5 million each in scrubbers by 2025.[2]U.S. Environmental Protection Agency, “Hospital/Medical/Infectious Waste Incinerators,” EPA, epa.gov Europe’s Waste Framework Directive requires 55% recycling by 2030, extending responsibility to non-hazardous medical packaging.[3]European Commission, “Waste Framework Directive (2024/825),” European Union, europa.eu India’s 2024 rule amendments add GPS tracking for every waste-haul vehicle, elevating costs 8%–12% for small operators. These overlapping rules reward integrated players able to amortize compliance investments, while regional haulers grapple with shrinking margins.

Outsourcing to Specialized Third-Party Service Providers

By 2025, 68% of U.S. acute-care hospitals outsourced all waste functions, up from 54% in 2020. Clean Harbors reported 11% year-over-year healthcare revenue growth in 2024 as systems bundled sharps, pharma take-back, and hazardous incineration services. The U.K.’s National Health Service awarded Veolia a GBP 1.2 billion contract covering 42 trusts, targeting 20% cost savings by centralized autoclave hubs. Outsourcing transfers liability but introduces cyber risk; Stericycle’s 2024 breach exposed 3.5 million patient records. Still, divestment of captive operations frees hospital capital for clinical upgrades.

Decentralized Home-Care and Point-of-Care Diagnostics Waste Surge

Medicare’s 2024 home-infusion reimbursement expansion drove a 22% rise in at-home intravenous therapies, each session generating up to 300 grams of contaminated tubing. Becton Dickinson shipped 18 million home sharps collectors in 2024, yet polypropylene shortages created back orders that forced hospitals to source uncertified containers. Point-of-care respiratory cartridges added 45,000 metric tons of single-use plastic in 2025, none yet recyclable. Fragmented residential pickup routes raise per-unit collection costs up to 60% versus centralized hospital loads, challenging profitability in the medical waste management market

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating expenditure for advanced treatment technologies | -0.8% | Global, acute in developing APAC and Africa | Long term (≥ 4 years) |

| Tightening incinerator-emission norms and public opposition | -0.6% | North America, EU, urban China | Medium term (2-4 years) |

| Consumables supply-chain disruptions | -0.4% | Global, episodic spikes in North America | Short term (≤ 2 years) |

| Informal and unregulated disposal in developing nations | -0.5% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Expenditure for Advanced Treatment Technologies

A turnkey 10-ton-per-day incinerator with gas scrubbing costs more than USD 8 million, a hurdle for municipal budgets in South Asia and Africa. Natural-gas usage for autoclaves adds USD 18 per ton, while refractory relining hits USD 400,000 every two years. India’s regulator found 38% of common treatment facilities below 60% utilization, driving per-ton costs above informal dumping rates. Microwave systems cut capex but cannot handle chemo vials, narrowing technology applicability.

Tightening Incinerator-Emission Norms and Public Opposition

California’s air district denied permits for three Los Angeles incinerators in 2024, citing particulate breaches in environmental-justice areas. The EU’s Industrial Emissions Directive now requires catalytic NOx reduction by 2028, a EUR 3–6 million outlay per plant. Litigation delayed a Pune, India project by 14 months, sending waste 180 km to the next legal facility. These headwinds favor non-thermal options, but space and labor needs rise.

Segment Analysis

By Service: Logistics Complexity Anchors Collection Dominance

Collection, transportation, and storage generated 44.26% of revenue in 2025, underscoring the logistics intensity that keeps hospitals locked into multi-year contracts. Fuel volatility and driver wage inflation eroded margins, but route density still secures recurring cash flow in the medical waste management market. Treatment and disposal services delivered the remainder, yet commoditization looms as generic autoclave units from Chinese makers reset price floors. The medical waste management market size tied to recycling remains small today, but EU circular-economy directives and California SB 54 are stimulating 8.64% CAGR growth, a bright spot for vendors that can certify contaminant-free resins.

Recycling acceleration will spur service bundling. Republic Services’ 2024 launch of a total-waste package won 140 new ambulatory-surgery clients by integrating biohazard pickup, pharma take-back, and OSHA compliance training. At the same time, Daniels Sharpsmart’s reusable container program shows how innovation can shrink collection frequency by 25%, decoupling revenue from haulage miles while enlarging medical waste management market share among sharps generators. Extended producer responsibility schemes in France create steady funding that should elevate recycling penetration toward 30% by 2030, lifting the segment’s contribution to medical waste management market size.

Note: Segment shares of all individual segments available upon report purchase

By Type of Waste: Non-Hazardous Volume Masks Hazardous Margin

Non-hazardous waste held 81.56% of global volume in 2025, yet low disposal fees restrict its value share to below 40%. Infectious and pathological streams, expected to grow 10.06% annually, remain the primary profit pool for the medical waste management market. Pharmaceutical incineration capacity in the United States is limited to 47 sites, creating regional bottlenecks that push pricing premiums. Sharps waste rose to 420,000 metric tons in 2025, fueled by self-administered biologics, while safety devices increased per-needle plastic mass by 35%.

Audits find misclassification rife; 22% of supposedly non-hazardous U.K. hospital waste contained pharmaceuticals or sharps, triggering re-sorting and penalty fees. Closed-system transfer devices mandated by the FDA boost contaminated syringe counts by 18%, highlighting rising hazardous waste volumes. In turn, vendors that prove exacting segregation protocols can capture incremental medical waste management market share and command premium pricing.

By Treatment Site: Onsite Economics Shift as Technology Costs Fall

Offsite facilities processed 59.27% of waste in 2025, aided by economies of scale in 10- to 50-ton-per-day incinerators. Yet declining autoclave costs and 2024 transport bottlenecks sparked a 9.91% CAGR outlook for onsite systems. A 500-bed hospital installing a USD 600,000 autoclave achieves payback within five years at current offsite fees, reducing risk from haulage disruptions that plagued the 2024 container shortage.

Mobile treatment blurs the onsite-offsite boundary; truck-mounted autoclaves deployed in rural Texas erased 400-mile round trips for clinics. Regulatory disparities, however, complicate adoption—California allows conditional mobile permits, while New York demands fixed-facility licensing. Asia-Pacific hospitals, 73% of which lack a licensed plant within 50 km, stand to become the largest growth arena for onsite systems, expanding medical waste management market size at the local facility level.

By Waste Generator: Pharma and Biotech Complexity Commands Premium Pricing

Hospitals and diagnostic laboratories produced 61.63% of waste in 2025, yet reimbursement compression pushes administrators to renegotiate waste contracts aggressively. Pharma and biotech generators will grow 8.85% through 2031 as CAR-T and mRNA-based therapies enter commercial scale, each batch producing 300–500 kg of vector-laden waste that demands USD per-kilogram fees three to four times higher than standard streams.

Ambulatory surgery centers, tallying 28 million U.S. procedures in 2024, create intense per-procedure waste loads from disposable drapes and trays. Veterinary clinics and tattoo parlors comprise a fragmented tail with outsized compliance lapses. Biotech players such as Amgen are internalizing disposal with onsite systems that cut offsite volumes by 95%, shrinking third-party addressable medical waste management market size yet opening equipment-sales channels.

Geography Analysis

North America commanded 31.76% of the medical waste management market in 2025, but growth moderates to 4.8% CAGR as saturation and higher compliance costs converge. U.S. incinerators spent up to USD 5 million each on scrubber retrofits in 2025, passing through 8%–12% price hikes. Canada earmarked CAD 120 million (USD 89 million) to upgrade waste facilities in Indigenous territories, while Mexico digitized manifest systems, favoring multinational haulers with IT scale.

Europe followed at 27% share. Germany, France, and the U.K. led spending as the Waste Framework Directive’s 55% recycling target for 2030 triggers investments. The U.K. consolidated NHS contracts into a seven-year GBP 1.2 billion deal, spotlighting a procurement trend toward mega-tenders. Germany’s producer-responsibility law compels device makers to fund 70% of take-back costs by 2027, shifting margin pools from haulers to recyclers and increasing medical waste management market size for circular-services providers.

Asia-Pacific is the fastest-growing region at 9.12% CAGR. China’s revised Solid Waste Law imposes CNY 1 million fines for non-digital transfer manifests, accelerating IT adoption. India’s 150,000 new beds exacerbate a capacity gap where only 62% of districts have licensed facilities, creating demand for mobile or onsite treatment. Japan recycles PVC IV bags in a pilot collecting 15,000 tons annually, while South Korea’s Waste Control Act extends producer responsibility to single-use tools. Australia targets 80% resource recovery by 2030 but grapples with dispersed hospital networks, favoring onsite autoclaves.

Middle East & Africa and South America each hold under 10% share, constrained by limited plant availability and informal disposal. Abu Dhabi’s AED 450 million investment in a 25-ton-per-day incinerator shows rising Gulf spending, whereas 41% of hospitals in South Africa’s KwaZulu-Natal still discard sharps as municipal refuse, signaling latent medical waste management market potential.

Competitive Landscape

The top five companies includes Waste Management/Stericycle, Clean Harbors, Veolia, Suez, and Republic Services and others. Waste Management’s 2024 Stericycle acquisition creates the largest U.S. platform but triggered divestiture of 23 routes to satisfy antitrust regulators. Logistical density, IoT-enabled tracking, and recycling integration define competition. Daniels Sharpsmart, with 47 active patents, grew to 18% of the U.S. sharps segment by saving hospitals 22% in disposal costs through reusable containers.

White-space opportunities abound in emerging markets where 58% of facilities lack safe disposal access. Mobile autoclave providers and micro-wave unit vendors price systems below USD 500,000, targeting hospitals without local licensed plants. Triumvirate Environmental processes 1.2 million lb of expired pharmaceuticals annually, while Cyntox markets onsite chemical neutralizers for cytotoxic waste, illustrating niche strategies.

Technology investments accelerate: GFL Environmental’s AI route optimization cut fuel usage 14% in 2024 and delivered same-day pickups for 92% of calls. Regulatory moats persist—FDA 510(k) clearance for onsite devices requires up to USD 500,000 and two years of testing, slowing new entrants but affirming medical waste management market resilience for incumbents like Sterilis.

Medical Waste Management Industry Leaders

Stericycle Inc.

Veolia Environnement SA

Waste Management Inc.

Clean Harbors Inc.

Suez Environmental Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Veolia North America earmarked USD 350 million for three U.S. acquisitions and new hazardous-waste capacity expansions.

- April 2025: Kenya’s Health Ministry and Belgium reviewed progress on a Belgian-backed medical-waste microwave project to cut infection risk

- February 2025: India dedicated “Sṛjanam,” its first indigenously built automated biomedical-waste treatment rig, developed by CSIR-NIIST and installed at AIIMS New Delhi.

Global Medical Waste Management Market Report Scope

As per the scope of the report, medical waste contains infectious materials, and it is the waste generated by healthcare facilities like physician’s offices, hospitals, dental practices, laboratories, medical research facilities, and veterinary clinics. Medical waste can contain bodily fluids like blood or other contaminants. Some examples are culture dishes, glassware, bandages, gloves, discarded sharps like needles or scalpels, swabs, and tissue. The medical waste management market involves the handling, treatment, and disposal of wastes generated by healthcare facilities such as hospitals, clinics, laboratories, and research centers.

The medical waste management market is segmented by service, type of waste, treatment site, waste generator, and geography. By Service, the market is segmented into Collection, transportation and storage; treatment and disposal; and recycling. By Type of Waste, the market is segmented into hazardous and Non-hazardous. Hazardous is further subsegmented into Infectious & Pathological, Pharmaceutical, Sharps, and Other. By Treatment Site, the market is segmented into Offsite and Onsite. By Waste Generator, market is segmented into Hospitals & Diagnostic Laboratories, Clinics & Ambulatory Surgical Centers, Pharmaceutical & Biotechnology Companies, Research Laboratories, Other Generators.By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also offers the market size and forecasts for 17 regional countries globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Collection, Transportation & Storage Services |

| Treatment & Disposal Services |

| Recycling Services |

| Non-hazardous Waste | |

| Hazardous Waste | Infectious & Pathological |

| Pharmaceutical | |

| Sharps | |

| Other Hazardous Waste |

| Offsite Treatment |

| Onsite Treatment |

| Hospitals & Diagnostic Laboratories |

| Clinics & Ambulatory Surgical Centres |

| Pharmaceutical & Biotechnology Companies |

| Research Laboratories |

| Other Generators (Blood Banks, Mortuaries, Veterinary, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Collection, Transportation & Storage Services | |

| Treatment & Disposal Services | ||

| Recycling Services | ||

| By Type of Waste | Non-hazardous Waste | |

| Hazardous Waste | Infectious & Pathological | |

| Pharmaceutical | ||

| Sharps | ||

| Other Hazardous Waste | ||

| By Treatment Site | Offsite Treatment | |

| Onsite Treatment | ||

| By Waste Generator | Hospitals & Diagnostic Laboratories | |

| Clinics & Ambulatory Surgical Centres | ||

| Pharmaceutical & Biotechnology Companies | ||

| Research Laboratories | ||

| Other Generators (Blood Banks, Mortuaries, Veterinary, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the medical waste management market by 2031?

The medical waste management market size is forecast to reach USD 27.60 billion by 2031.

Which service segment is growing fastest?

Recycling services are set to expand at an 8.64% CAGR through 2031 due to circular-economy mandates.

Which region will register the highest growth rate?

Asia-Pacific is anticipated to grow at about 9.12% CAGR as China and India tighten waste regulations.

How will onsite treatment adoption change by 2031?

Onsite autoclave and microwave systems are projected to grow at a 9.91% CAGR, eroding offsite dominance.

What impact does biotech manufacturing have on waste streams?

Each commercial cell-therapy batch generates 300–500 kg of high-risk waste, boosting demand for specialized disposal services.

Why are IoT solutions gaining traction in waste management?

Hospitals need granular carbon and compliance data, and RFID-enabled containers cut collection trips by up to 18%.