Medical Vending Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

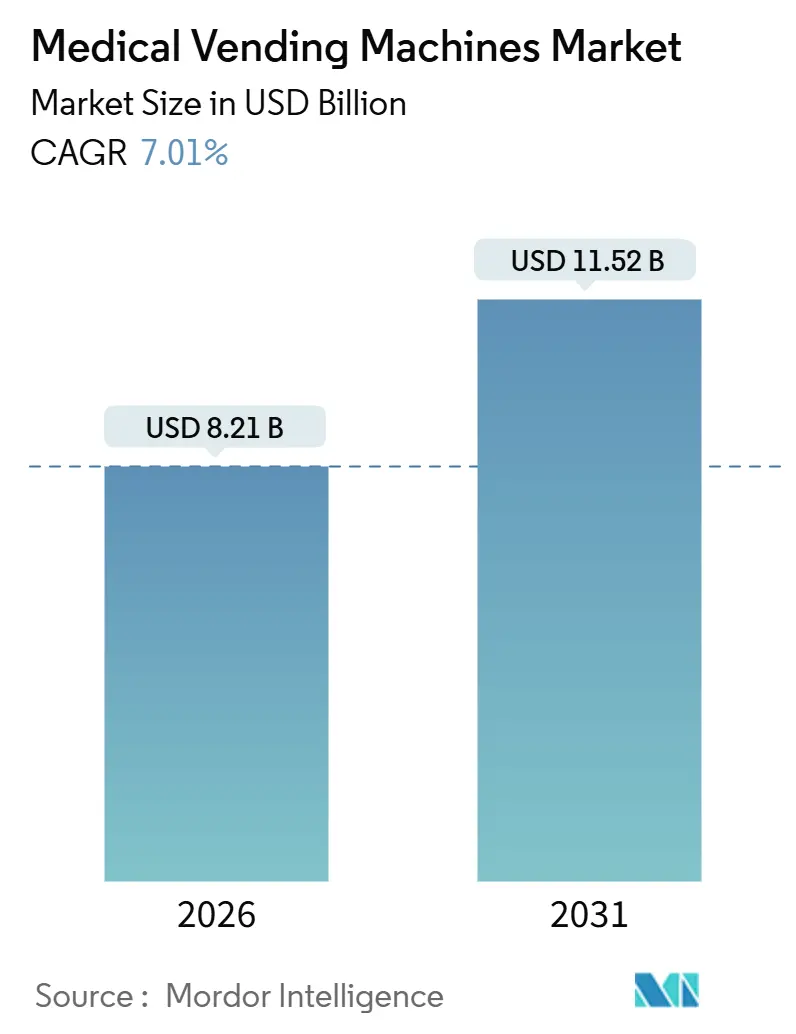

| Market Size (2026) | USD 8.21 Billion |

| Market Size (2031) | USD 11.52 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Vending Machines Market Analysis by Mordor Intelligence

The Medical Vending Machines Market size is estimated at USD 8.21 billion in 2026, and is expected to reach USD 11.52 billion by 2031, at a CAGR of 7.01% during the forecast period (2026-2031).

Across hospitals, clinics, and public venues, automated dispensing is replacing manual pharmacy counters, lowering medication-error rates, shrinking inventory losses, and extending access after traditional hours, thus accelerating the medical vending machines market trajectory. Growing adoption of cloud-connected cabinets that feed real-time data into hospital information systems, coupled with upgrades to temperature-controlled units for vaccines, keeps demand resilient. Competitive activity centers on service contracts and interoperability, while regulatory clarity in the United States and expanding telepharmacy statutes in Asia-Pacific open fresh opportunities. Counterpressure comes from cybersecurity threats and fragmented device approvals that slow cross-border rollouts.

Key Report Takeaways

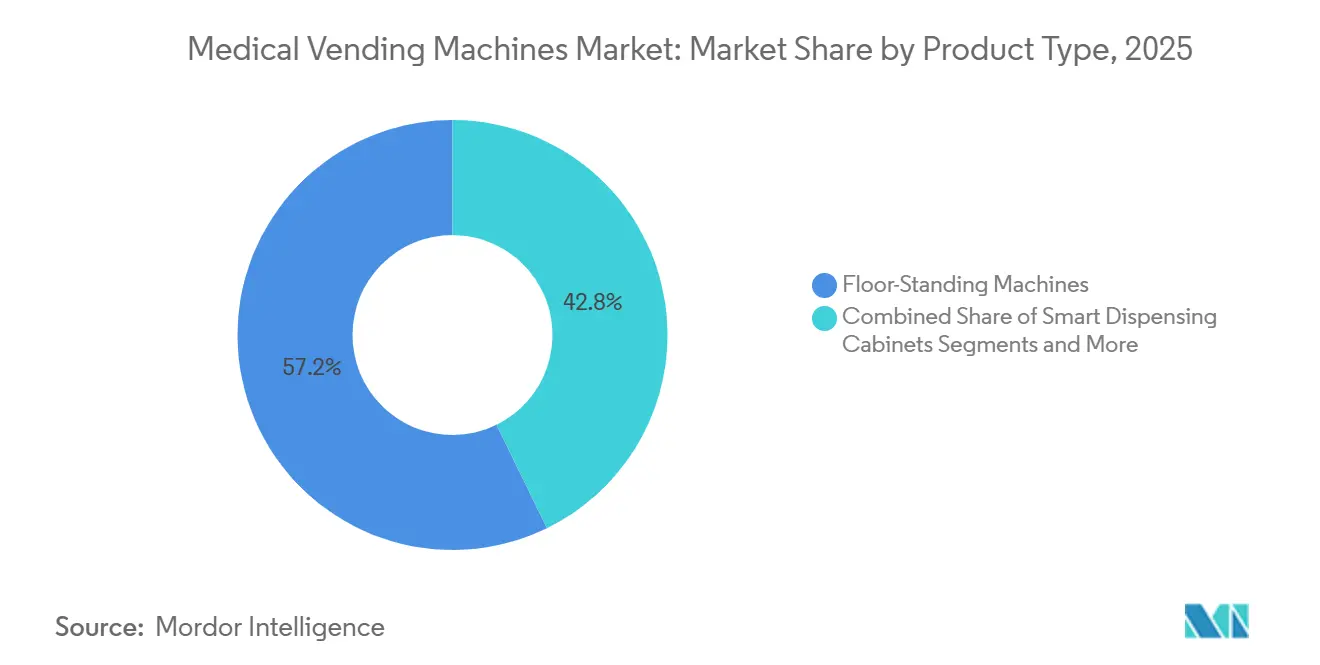

- By product type, floor-standing machines held 57.24% revenue share in 2025, while countertop and benchtop units are projected to grow at an 11.43% CAGR through 2031.

- By medication class, prescription drugs commanded 44.63% of 2025 revenue; vaccines and other cold-chain drugs are expected to advance at a 10.32% CAGR to 2031.

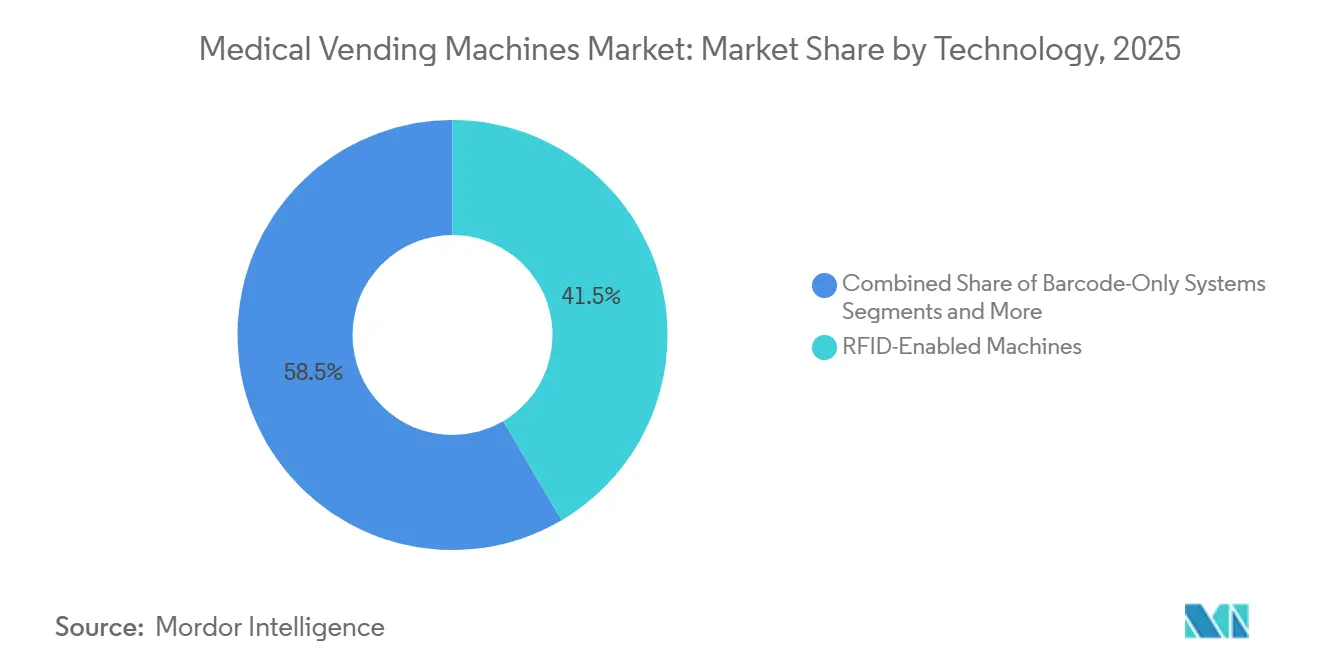

- By technology, RFID-enabled cabinets accounted for 41.52% of the medical vending machines market share in 2025, whereas AI vision-based systems are forecast to register an 11.89% CAGR through 2031.

- By end user, hospitals and specialty clinics contributed 44.61% of 2025 revenue, while workplace and corporate clinics are on track for a 9.63% CAGR through 2031.

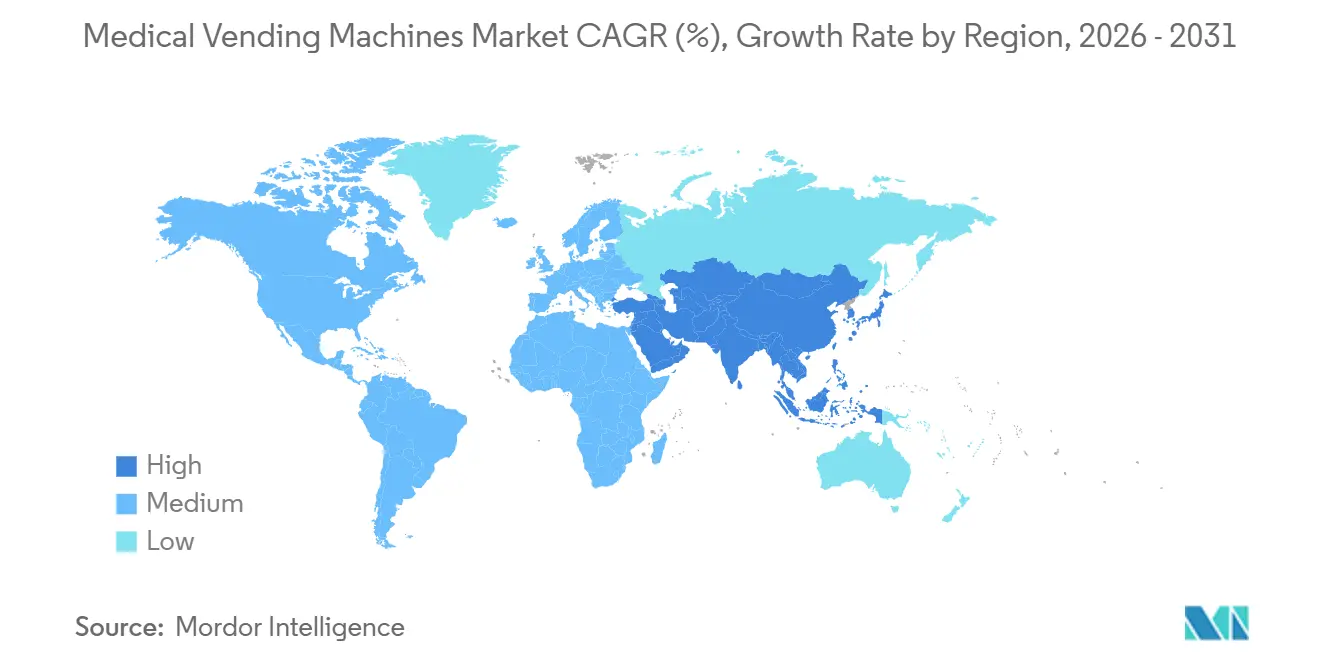

- By geography, North America led with 33.11% global revenue in 2025; Asia-Pacific is poised to expand at a 10.20% CAGR over the same forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Vending Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing dependency on prescription medicines in remote & rural areas | 1.2% | Global, with concentration in rural US, India, sub-Saharan Africa | Medium term (2-4 years) |

| Demand for real-time inventory visibility & shrinkage control | 1.4% | North America & EU, early adoption in urban APAC hospitals | Short term (≤ 2 years) |

| Rising chronic-disease burden driving 24/7 medication access | 1.6% | Global, acute in aging economies (Japan, Germany, US) | Long term (≥ 4 years) |

| Integration with tele-pharmacy & e-prescription platforms | 1.1% | North America, Australia, select EU markets with digital-health mandates | Medium term (2-4 years) |

| Blockchain-enabled anti-counterfeit dispensing authentication | 0.5% | APAC core (China, India), spill-over to MEA | Long term (≥ 4 years) |

| Hospital micro-fulfilment for PPE & consumables | 0.9% | Global, sustained post-pandemic in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Dependency on Prescription Medicines in Remote & Rural Areas

Pharmacy deserts leave patients in rural districts traveling 30 miles or more for refills, a gap that fuels demand in the medical vending machines market. Community centers, fire stations, and convenience stores host 24/7 machines that dispense chronic-disease drugs, lowering travel costs and improving adherence. Los Angeles County’s 2025 rollout of free units stocked with naloxone and COVID-19 tests illustrates how municipalities leverage unattended cabinets to close public-health gaps.[1]Los Angeles County Department of Public Health, “Public Health Introduces Community Health Stations to Provide Lifesaving Products,” Los Angeles County, lacounty.gov In India, solar-powered dispensers piloted under the National Health Mission pair with telemedicine kiosks, helping village clinics avoid over-stocking slow-moving SKUs. Such deployments demonstrate the medical vending machines market potential when infrastructure and remote verification converge.

Demand for Real-Time Inventory Visibility & Shrinkage Control

Unaccounted inventory costs U.S. hospitals USD 4.5 billion annually, a burden magnified by opioid diversion penalties. RFID cabinets with biometric locks have cut unexplained losses by up to 77% in long-term-care settings, according to a 2024 BD study. Cloud dashboards surface anomalies—such as withdrawals outside a clinician’s shift—and trigger compliance reviews before diversion escalates. New York City Health + Hospitals unified cabinet data across 11 facilities in 2024, trimming duplicate purchase orders and freeing working capital. These gains reinforce purchasing decisions, strengthening the medical vending machines market outlook among cost-pressured providers.

Rising Chronic-Disease Burden Driving 24/7 Medication Access

Non-communicable diseases cause 41 million deaths yearly, 74% of the global total. Six in ten U.S. adults have at least one chronic condition, pushing hospitals toward vending solutions that cut after-hours refill delays.[2]Centers for Disease Control and Prevention, “About Chronic Diseases,” Centers for Disease Control and Prevention, cdc.gov Machines placed in lobbies, senior-living centers, and retail pharmacies add off-clock convenience and help reduce readmissions under value-based care contracts. Japan, where 28.6% of residents are 65-plus, installs wall units in train stations so older adults can collect pre-packed medicines without queueing. This continuous-access imperative supports sustained growth across the medical vending machines market.

Integration with Tele-Pharmacy & E-Prescription Platforms

By 2025, 28 U.S. states had legalized telepharmacy models that let remote pharmacists verify orders while the machine dispenses on-site.[3]Michael A. Dowell, “The Evolving Telepharmacy Dispensing Landscape,” U.S. Pharmacist, uspharmacist.com MedAvail’s kiosk embeds high-definition video, satisfying counseling mandates and shrinking wait times. E-prescription uptake is strong; 90% of U.S. ambulatory scripts travel electronically, yet discharge orders still rely on fax in many hospitals, limiting fully unattended dispensing. Australia’s My Health Record links scripts directly to government smart cards, letting machines identify patients and release refills autonomously. Better digital hand-offs will broaden the use cases for medical vending machines in outpatient and rural environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & physical misuse risks | -0.8% | Global, acute in North America & EU with high digitization | Short term (≤ 2 years) |

| Complex multi-country regulatory approvals | -0.6% | Global, most severe in APAC & MEA with fragmented frameworks | Medium term (2-4 years) |

| High service, refill & calibration costs in low-volume sites | -0.5% | Rural North America, sub-Saharan Africa, remote APAC | Long term (≥ 4 years) |

| Consumer trust gap around machine-dispensed medicines | -0.4% | APAC & MEA, legacy markets with pharmacist-centric models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security & Physical Misuse Risks

Healthcare ransomware attacks spiked in 2024; the Change Healthcare breach alone imposed USD 2.3 billion to USD 2.5 billion in remediation costs. Connected cabinets inherit these vulnerabilities, exposing dose settings and access logs to hackers. Ascension Health’s May 2024 cyberattack forced 140 hospitals back to paper workflows, delaying elective surgeries for weeks. Physical tampering—such as stolen fingerprints or crowbar attacks—adds another risk layer. Vendors now promote air-gapped networks, multifactor log-ins, and tamper seals, yet rising threat vectors still temper near-term momentum in the medical vending machines market.

Complex Multi-Country Regulatory Approvals

The U.S. Food and Drug Administration treats automated cabinets as Class II devices that need 510(k) clearance, while Europe delegates oversight to each member state, creating divergent compliance checklists. China’s National Medical Products Administration adds domestic trials and plant inspections that stretch 18–24 months. Emerging markets often lack clear statutes, leaving importers uncertain which ministry to approach. These hurdles extend launch cycles and inflate legal costs, slowing cross-border scale-up within the medical vending machines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Floor-Standing Units Dominate, Countertop Solutions Scale

Floor-standing machines captured 57.24% revenue in 2025, reflecting hospitals’ need for 200-plus SKU capacity and integration with pneumatic tubes that cut nurse walk-time. Their footprint anchors the medical vending machines market size in high-acuity settings. Countertop and benchtop models, forecast to post an 11.43% CAGR to 2031, appeal to ambulatory centers, urgent-care clinics, and workplace health rooms that face tight real-estate budgets. Wall-mounted and compact units address EMS vehicles and offshore rigs where mobility trumps inventory depth. Smart dispensing cabinets, while pricey, deliver rapid payback by reducing shrinkage and labor.

Countertop machines are edging out traditional pharmacy counters in drugstores as remote pharmacists verify scripts while the drawer dispenses, freeing staff for counseling. Wall-mounted units in emergency departments provide immediate naloxone or emergency contraception access during overnight shifts. AI vision sensors identify pill shape and color, flagging errors before they reach patients. These evolutions keep the medical vending machines market vibrant across facility types.

By Medication Class: Prescription Drugs Lead, Vaccines Gain Speed

Prescription drugs held 44.63% value share in 2025, spanning maintenance therapies and controlled substances that demand audit trails. Over-the-counter items grow steadily in transport hubs and campuses. PPE and supplies stabilized at higher baselines post-pandemic as hospitals maintain surge stockpiles. Vaccines and cold-chain drugs, expected to grow 10.32% annually to 2031, require refrigerated cabinets fitted with backup power and continuous logging, expanding the medical vending machines market size in immunization programs.

Cold-chain units cost 40%–60% more than ambient models yet enable rural clinics to administer shots on-site, boosting revenues and coverage. Prescription-drug vending faces stricter oversight; several U.S. states still mandate live pharmacist review before dispensing narcotics. OTC kiosks operate under retail statutes, opening placement in hotels and airports. PPE cabinets in corridors cut manual checks and automate orders, underscoring the medical vending machines market efficiency benefits.

By Technology: RFID Holds Lead, AI Vision Accelerates

RFID machines controlled 41.52% share in 2025, offering touchless package tracking that updates electronic records without barcode scans. Barcode-only systems remain in budget-constrained facilities but slow workflows. IoT connectivity unlocks predictive analytics, spotting seasonal spikes and optimizing par levels. AI vision dispensing, forecast to expand 11.89% per year to 2031, verifies pill imprint codes, catching errors RFID tags miss. However, regulatory guidance on computer vision remains sparse, requiring hybrid RFID-vision workflows for high-risk drugs, a nuance shaping technology decisions in the medical vending machines market.

Cloud platforms let technicians troubleshoot remotely, slashing downtime. Yet vision algorithms struggle with look-alike generics, prompting ongoing refinement. Hospitals weigh capital outlays against long-term safety and labor savings, a dynamic that fuels iterative innovation across the medical vending machines market.

By End User: Hospitals Command Spend, Workplace Clinics Climb

Hospitals and specialty clinics represented 44.61% of demand in 2025, driven by Joint Commission standards and malpractice-avoidance imperatives. Retail pharmacies place kiosks in lobbies for after-hours pickups, blocking mail-order leakage. Workplace clinics are rising at a 9.63% CAGR as employers deploy machines that dispense diabetes and hypertension refills on site, cutting absenteeism. Transport hubs stock OTC units for travelers seeking quick relief, diversifying venue mix in the medical vending machines market.

Rural centers face capital and connectivity hurdles; solar-powered machines with satellite links soften the blow but still incur elevated service costs. Retail chains benefit from extended hours without hiring night staff, yet some states bar unattended controlled-substance dispensing. Workplace clinics serve predictable populations, enabling tight inventory optimization. Cashless and biometric payments in airports and stadiums streamline turnover, keeping the medical vending machines market aligned with consumer convenience trends.

Geography Analysis

North America held 33.11% revenue share in 2025, anchored by 86.1% U.S. hospital penetration of automated cabinets. Mature EHR integration lets machines verify allergies and log doses automatically. NYC Health + Hospitals’ 2024 rollout across 11 facilities underscores public-sector momentum. Regulatory clarity via the FDA’s 510(k) pathway sustains investment, reinforcing the medical vending machines market foothold.

Europe sits second, with Germany, France, and the U.K. leading. Fragmented oversight—some states ban unattended prescription vending—creates uneven uptake. Spain and Italy push telepharmacy to serve aging rural areas, installing compact units in village posts. GDPR compliance adds encryption and consent requirements, influencing vendor design choices in the regional medical vending machines market.

Asia-Pacific is the growth engine, forecast at 10.20% CAGR to 2031. China’s 2026 blockchain traceability mandate drives cabinet upgrades. Japan installs wall units in train stations for elderly convenience, while India pilots solar-powered dispensers tied to telemedicine in Uttar Pradesh and Bihar. Australia links scripts to smart cards via My Health Record, enabling unattended refills. South Korea’s digital infrastructure supports IoT dashboards that optimize par levels across multi-hospital systems, collectively propelling the medical vending machines market forward.

Middle East & Africa and South America remain smaller yet active. GCC smart-hospital projects include automated dispensing as a pillar. Brazil’s 2024 rule change allowed cabinets in pharmacies under pharmacist oversight, opening new lanes for vendors. Argentina’s pilots in Buenos Aires and Córdoba test viability despite patchy broadband and electronics tariffs, signaling incremental room for the medical vending machines market to expand.

Competitive Landscape

The medical vending machines market is moderately concentrated. Becton Dickinson, Omnicell, and Capsa Healthcare together control roughly half global revenue through entrenched service contracts and deep EHR integration. BD’s Pyxis line scored 84.6 in KLAS 2025 rankings, reflecting uptime and workflow fit. Omnicell posted USD 1.14 billion sales in 2024 across 40 countries, pitching cloud cabinets that sync with enterprise resource planning suites.

Niche entrants chase white-space. InstyMeds offers retail kiosks that dispense prescriptions in under a minute. MedAvail, now part of Tabula Rasa HealthCare, embeds video consults for underserved neighborhoods. Disruptors emphasize AI vision and blockchain verification, though regulatory ambiguity slows broad uptake. Patent filings show BD focusing on biometric locks, while Omnicell invests in demand-forecast algorithms.

Service depth is a key differentiator; hospitals favor 24-hour technical support and regional parts depots. Vendors versed in 510(k), CE, and NMPA clearances enjoy multiyear leads. Total cost of ownership, not sticker price, steers decisions—maintenance, software upgrades, and integration complexity weigh heavily. Together, these factors shape competitive dynamics and sustain innovation across the medical vending machines market.

Medical Vending Machines Industry Leaders

Becton, Dickinson and Company

Omnicell Inc.

Capsa Healthcare

InstyMeds Corporation

ScriptPro LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Cal Poly Campus Health & Wellbeing introduced four medical vending machines offering OTC medicines, hygiene items, and reproductive-health products to students and employees.

- October 2025: Amazon launched prescription kiosks at One Medical clinics in Los Angeles, allowing patients to obtain medications minutes after appointments.

- August 2025: Harvest installed its first smart vending machine at IWK Health in Halifax, providing 24-hour access to healthy grab-and-go meals.

- May 2025: Los Angeles County deployed free health vending machines across transit hubs and libraries, dispensing naloxone, COVID-19 tests, and condoms to underserved neighborhoods.

Global Medical Vending Machines Market Report Scope

Medical vending machines are the automated machines used to dispense prescription drugs, medical devices and miscellaneous medical products by paying through an interface. The medical vending machines can be installed at a suitable place depending on the utility of the machine.

Medical vending machines market is segmented by product type, medication class, technology, end user and geography. By Product Type, the market is segmented into Floor-Standing Machines, Countertop/Benchtop Machines, Wall-Mounted/Compact Units, Smart Dispensing Cabinets. By Medication Class, the market is segmented into Prescription Drugs, OTC Medicines, PPE & Medical Supplies, Vaccines & Cold-Chain Drugs. By Technology, market is segmented into RFID-Enabled, Barcode-Only, IoT/Cloud-Connected, AI Vision-Based. By End User, the market is segmented into Hospitals, Retail Pharmacies, Workplace Clinics, Transportation Venues, and Rural Health Centers. By Geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. Market Forecasts are Provided in Terms of Value (USD).

| Floor-Standing Machines |

| Countertop / Benchtop Machines |

| Wall-Mounted / Compact Units |

| Smart Dispensing Cabinets |

| Prescription Drugs |

| Over-the-Counter (OTC) Medicines |

| PPE & Medical Supplies |

| Vaccines & Cold-Chain Drugs |

| RFID-Enabled Machines |

| Barcode-Only Systems |

| IoT / Cloud-Connected Units |

| AI Vision-Based Dispensing |

| Hospitals & Specialty Clinics |

| Retail Pharmacies & Drugstores |

| Workplace & Corporate Clinics |

| Transportation & Public Venues |

| Remote & Rural Health Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Floor-Standing Machines | |

| Countertop / Benchtop Machines | ||

| Wall-Mounted / Compact Units | ||

| Smart Dispensing Cabinets | ||

| By Medication Class | Prescription Drugs | |

| Over-the-Counter (OTC) Medicines | ||

| PPE & Medical Supplies | ||

| Vaccines & Cold-Chain Drugs | ||

| By Technology | RFID-Enabled Machines | |

| Barcode-Only Systems | ||

| IoT / Cloud-Connected Units | ||

| AI Vision-Based Dispensing | ||

| By End User | Hospitals & Specialty Clinics | |

| Retail Pharmacies & Drugstores | ||

| Workplace & Corporate Clinics | ||

| Transportation & Public Venues | ||

| Remote & Rural Health Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast size of the medical vending machines market by 2031?

The market is expected to reach USD 11.52 billion by 2031.

Which product configuration leads current deployments?

Floor-standing cabinets account for 57.24% of 2025 revenue.

Which technology segment is growing fastest?

AI vision-based dispensing is set to expand at an 11.89% CAGR through 2031.

Which region shows the highest growth momentum?

Asia-Pacific is projected to grow at a 10.20% CAGR to 2031.

Page last updated on: