Medical Transcription Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

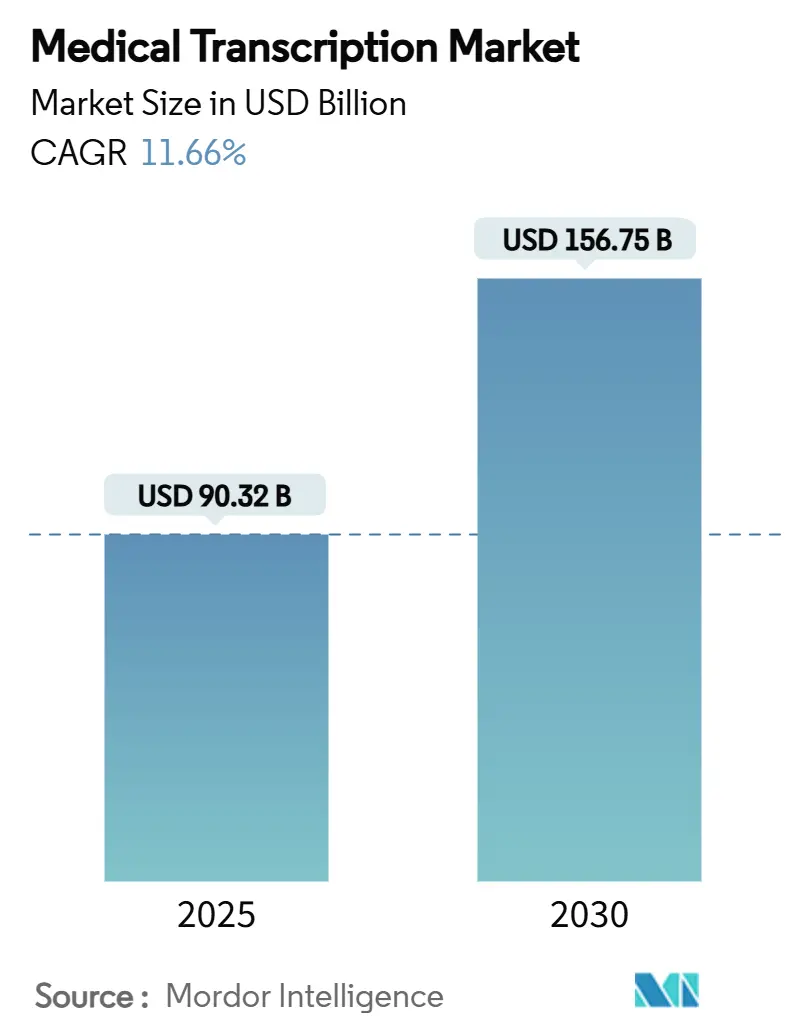

| Market Size (2025) | USD 90.32 Billion |

| Market Size (2030) | USD 156.75 Billion |

| Growth Rate (2025 - 2030) | 11.66% CAGR |

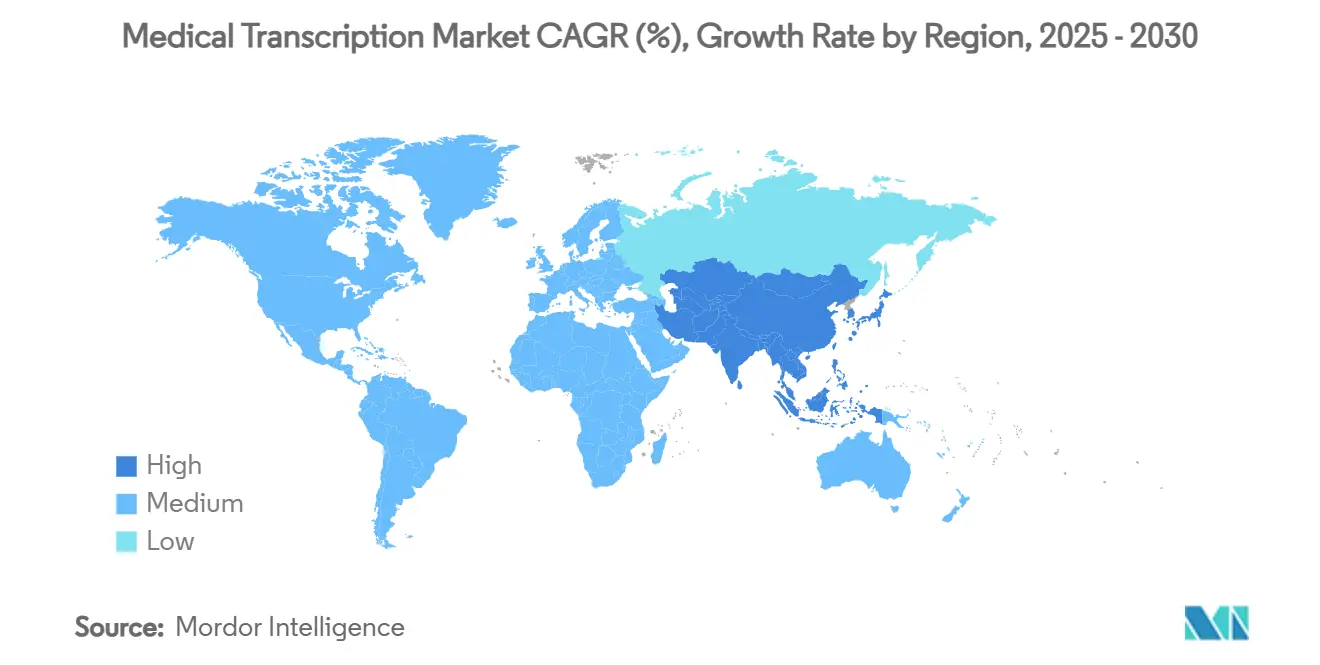

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Transcription Market Analysis by Mordor Intelligence

The medical transcription market is valued at USD 90.32 billion in 2025 and is forecast to reach USD 156.75 billion by 2030, registering an 11.66% CAGR through the period. Continuous investment in AI-powered documentation, stricter data-sharing regulations, and post-pandemic digitization have lifted demand for real-time clinical note creation that fits seamlessly into electronic health records. Providers are prioritizing tools that shorten documentation time, ease physician fatigue, and strengthen reimbursement accuracy, while technology vendors race to embed ambient intelligence inside mainstream EHR platforms. Consolidation is reshaping competitive dynamics as large software firms absorb specialist transcription providers and roll out integrated ambient scribe suites. Growth prospects remain most pronounced in emerging telehealth workflows, multilingual transcription, and hybrid sourcing models that balance cost with tighter data control.

Key Report Takeaways

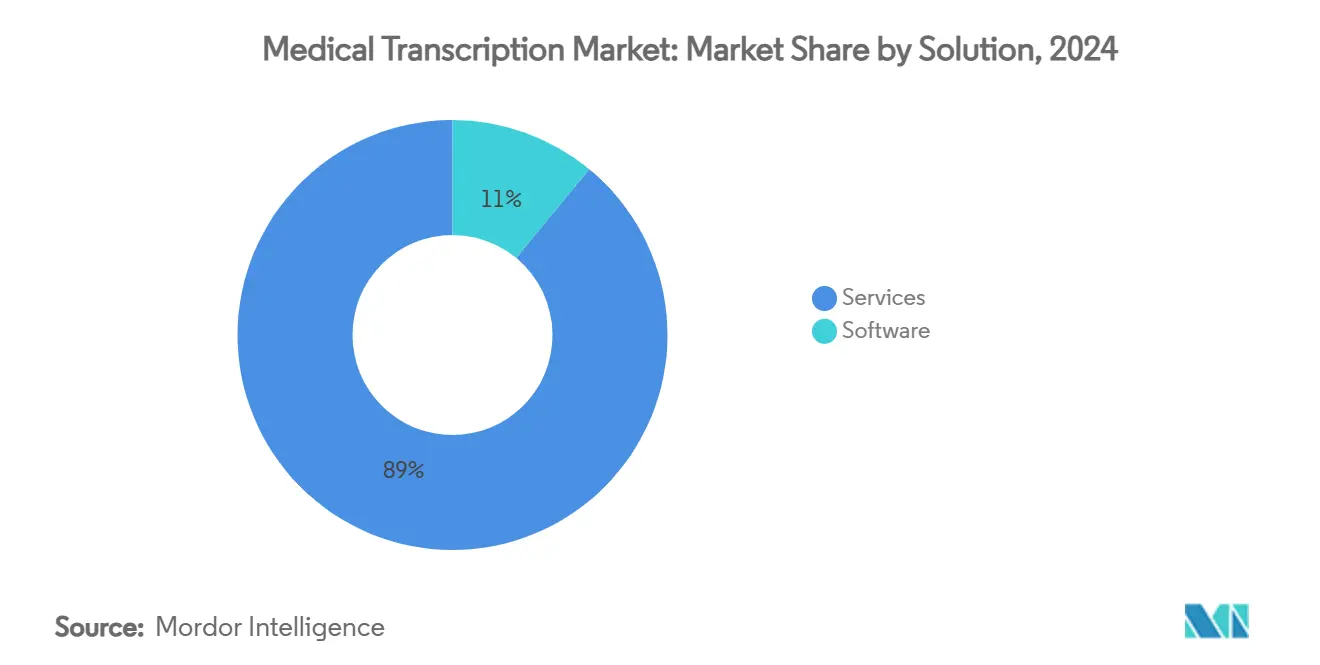

- By solution, services captured 89.02% of the medical transcription market share in 2024, while software is advancing at a 15.47% CAGR toward 2030.

- By technology platform, EHR-integrated speech recognition held 47.56% of the medical transcription market size in 2024; AI ambient scribe systems are growing at 15.02% CAGR to 2030.

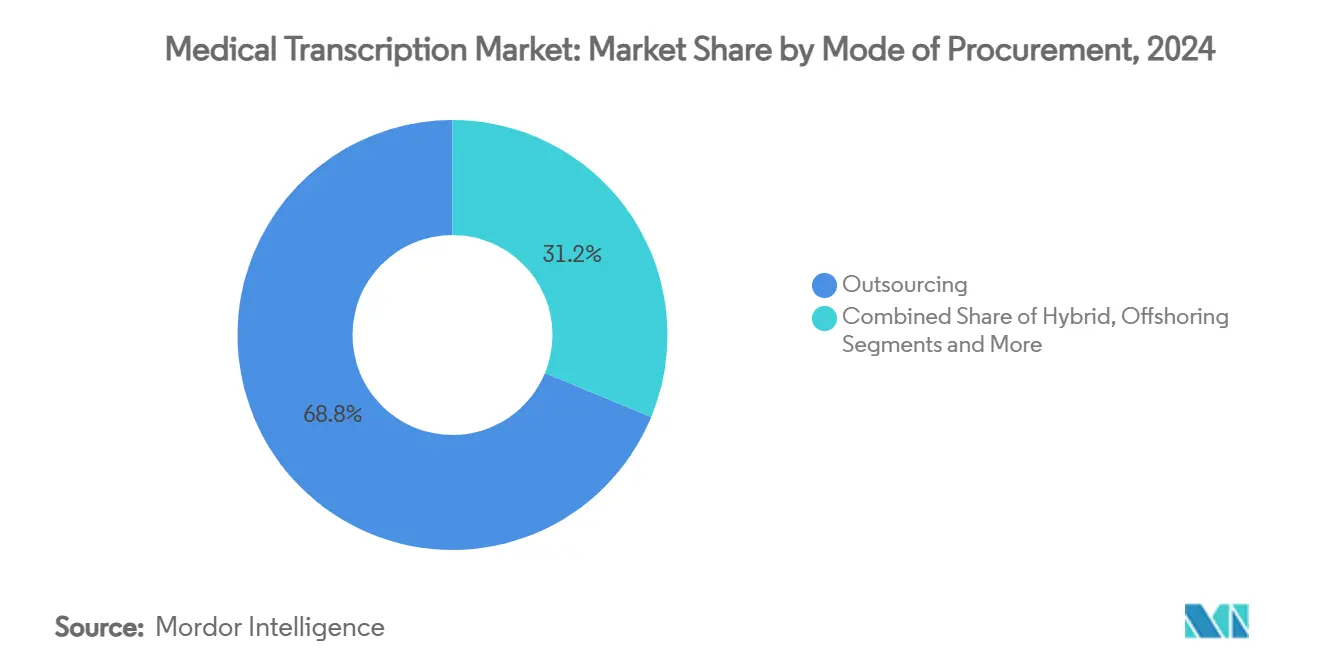

- By mode of procurement, outsourcing accounted for 68.78% share of the medical transcription market in 2024; hybrid captive-outsourced models record the fastest 14.34% CAG.

- By end user, hospitals generated 53.45% demand in 2024, yet telehealth providers post the highest 14.63% CAGR to 2030.

- By geography, North America dominated with 38.74% revenue share in 2024; Asia-Pacific leads growth at 13.56% CAGR through 2030.

Global Medical Transcription Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in adoption of automated speech-to-text solutions | +2.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Expansion of healthcare IT budgets in post-pandemic cycles | +2.1% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Regulatory push for structured clinical documentation | +1.9% | North America primary, EU secondary | Medium term (2-4 years) |

| AI-powered ambient clinical intelligence integrated into EHR workflows | +2.5% | North America and APAC | Short term (≤ 2 years) |

| Value-based reimbursement models demanding granular data capture | +1.4% | North America primary | Long term (≥ 4 years) |

| Explosive growth of video and asynchronous telehealth consultations | +1.9% | Global, with APAC and Latin America acceleration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge In Adoption Of Automated Speech-To-Text Solutions

Real-time speech recognition is replacing legacy dictation in emergency departments and outpatient clinics. Microsoft released Dragon Copilot in March 2025, allowing clinicians to auto-generate encounter notes, referral letters, and orders inside a single workspace. Stanford Health Care reported that 96% of physicians found ambient transcription easy to use after its 2024 DAX Copilot rollout, and 78% said it cut note-taking time. Specialized language datasets created by Gdańsk University of Technology now improve recognition of non-English medical terms, expanding adoption in multilingual regions.[1]Bożena Kostek, “Transforming Health Care with Speech-to-Text Technology,” ScienceDaily, sciencedaily.com Augmedix answered emergency-department needs with a GenAI documenter that operates without manual prompts. Collectively, these advances reposition the medical transcription market toward autonomous, context-aware note creation.

Expansion Of Healthcare IT Budgets In Post-Pandemic Digitization Cycles

Hospitals accelerated cloud documentation projects in 2024 to reduce burnout and standardize data capture. Community Health Network adopted the Dragon Medical platform across its Indiana system as part of a multi-year digital modernization program. Intermountain Health extended DAX Copilot across facilities in seven states to trim administrative complexity and feed analytic engines that support quality reporting. Mid-size providers also invest in AI tools that redirect scarce staff from paperwork to patient care. These capital flows enlarge the medical transcription market and push suppliers to bundle analytics, compliance, and documentation in unified contracts.

Regulatory Push For Structured Clinical Documentation

The 21st Century Cures Act enforces penalties on information blocking, compelling U.S. providers to adopt interoperable note formats. CMS now requires a 180-day EHR reporting window and a minimum 60-point score on electronic prescribing and data exchange objectives. Developers must also reveal algorithm logic under ONC certification updates, increasing transparency for AI-enabled transcription.[2]Office of the National Coordinator, “Certification Program Updates,” federalregister.gov Similar guidance from NHS England is shaping safe adoption of AI scribes in the United Kingdom. The rule environment firmly underpins continued expansion of the medical transcription market.

AI-Powered Ambient Clinical Intelligence Integrated Into EHR Workflows

Hospitals increasingly expect documentation tools to run natively inside core EHRs. Tampa General Hospital logged more than 15,000 ambient-enabled visits that produced real-time structured notes inside its Cerner system, freeing clinicians to focus on patient engagement. Nuance introduced DAX Copilot for MEDITECH users in March 2024, broadening reach across mid-tier hospitals. DeepScribe deepened integration with Epic to serve oncology documentation, illustrating specialty traction for embedded ambient solutions deepscribe.ai. Ambience Healthcare joined the athenahealth marketplace to provide multifeatured AI note creation and coding across 100 specialties. Seamless integration cements user adoption and extends the medical transcription market into decision-support territory.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent dictation quality and accent variation challenges | –1.8% | Global, higher in multilingual markets | Medium term (2-4 years) |

| Heightened cyber-security and HIPAA compliance costs | –2.2% | North America and Europe | Short term (≤ 2 years) |

| Physician push-back over generative-AI hallucinations in draft notes | –1.5% | Global, mainly developed markets | Short term (≤ 2 years) |

| Sustainability concerns over cloud compute carbon footprint | –0.9% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Cyber-Security & HIPAA Compliance Costs

A 2024 breach at Perry Johnson & Associates exposed data belonging to 1.2 million patients and drove urgent investments in encryption, monitoring, and zero-trust architectures. U.S. providers now require 128-bit encryption and continuous risk audits for any outsourced documentation flow, raising barriers for smaller vendors. The White House has also flagged the need for robust governance when AI processes protected health information, further lifting compliance overhead. These expenses temper near-term growth expectations for the medical transcription market.

Physician Push-Back Over Generative-AI "Hallucinations" In Draft Notes

Clinicians report that large language models sometimes fabricate diagnoses or medication lists, undermining trust in automated notes. Med Claims Compliance adopted a human-in-the-loop process that routes AI drafts through trained editors before EHR upload, protecting patient safety but slowing throughput. Academic reviews call for rigorous validation frameworks before fully autonomous scribing becomes standard care.[3]Shilpa Ghatnekar et al., “Digital Scribe Utility and Barriers,” ncbi.nlm.nih.gov Until accuracy rates approach perfect recall, a segment of the medical transcription market will remain labor-intensive.

Segment Analysis

By Solution: Services Dominate Despite Software Acceleration

Services accounted for 89.02% of the medical transcription market share in 2024 owing to deep domain expertise and complex quality-assurance needs that healthcare systems prefer to outsource. Software platforms, though smaller, are expanding at 15.47% CAGR as natural language processing accuracy crosses clinical-grade thresholds. The medical transcription market size tied to software is projected to advance rapidly as provider organizations license cloud-based engines that auto-generate structured notes and route exceptions to human reviewers.

Funding trends reinforce the shift. DeepScribe raised USD 30 million in 2024 to refine ambient capture that flows directly into EHR fields. Service leaders such as iMedX have adopted a “Humanology” model that blends automated drafts with expert editing to maintain 99% accuracy while reducing turnaround time. The medical transcription industry therefore evolves toward hybrid delivery where AI maximizes speed and humans safeguard precision.

By Technology Platform: EHR Integration Leads Ambient AI Surge

EHR-embedded speech recognition held 47.56% of the medical transcription market in 2024 because integrated tools fit clinician workflows without extra log-ins. AI ambient scribe systems post the highest 15.02% CAGR as they capture free-flow dialogue and surface context cues inside patient charts. The medical transcription market size attached to ambient AI is expected to more than double by 2030 if current adoption curves persist.

Vendors target specialty niches for differentiation. Solventum’s Fluency for Imaging ranked first in KLAS for radiology speech reporting in 2024, proving ambient AI can excel in high-acuity domains. Microsoft’s 2025 Dragon Copilot blends ambient listening with rules-based content insertion to cut manual entry even further. These advances confirm that technology variety will persist within the medical transcription market.

By Mode of Procurement: Outsourcing Dominance Faces Hybrid Challenge

Outsourcing controlled 68.78% of the medical transcription market in 2024 as hospitals leveraged vendors for scale, cost, and 24-hour coverage. Hybrid models that combine in-house oversight with external labor grow at 14.34% CAGR, reflecting security concerns and need for rapid custom template updates. The medical transcription market size generated by hybrid procurement will rise further as cloud APIs let providers pull ambient services behind their own firewalls.

Hospitals weigh stigma against savings. A 2024 survey showed 63% still outsource despite community concerns over job loss. Offshoring remains price-competitive, but stricter cyber rules push some work back onshore. Hybrid sourcing offers compromise, keeping sensitive specialties internal while routing routine office notes abroad. The model’s flexibility feeds continuous growth in the medical transcription market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Dominance Challenged by Telehealth Growth

Hospitals produced 53.45% of the overall demand in 2024 thanks to high patient volumes and multi-specialty complexity. Telehealth providers post a 14.63% CAGR as virtual care ubiquity increases, documenting events outside brick-and-mortar settings. The medical transcription market share held by telehealth could double by 2030 as insurers reimburse remote visits at parity.

Emergency services have unique documentation pain points. In 2024, Emergency Services Inc. integrated Augmedix GenAI scribing to alleviate front-line burnout. Ambulatory surgical centers and clinical labs similarly adopt ambient note capture that fits high-throughput environments. Each segment adds layers of diversity and resilience to the medical transcription market.

Geography Analysis

North America retained 38.74% of the medical transcription market in 2024 due to stringent interoperability mandates and mature health IT investment cycles. Providers face monetary disincentives if they impede information exchange under the Cures Act, which accelerates uptake of structured note solutions. Large systems such as Community Health Network and Intermountain Health rolled out ambient AI across multiple states, affirming regional leadership.

Europe ranks second and is shaped by GDPR-aligned privacy protocols that require explicit data-handling controls. NHS England issued 2024 safety guidance on AI scribes, spurring pilot deployments at sites like Great Ormond Street Hospital. Sustainability debates around cloud energy use introduce additional procurement criteria, influencing vendor selection and moderating the regional medical transcription market growth rate.

Asia-Pacific is the fastest-growing segment at 13.56% CAGR as countries expand telemedicine infrastructure and multi-lingual voice recognition. Governments in China, India, and Indonesia fund language resource development to improve clinical speech models, and health systems adopt ambient AI to ease workforce shortages. Localized platforms that address tonal languages and dialects are expected to enlarge the regional medical transcription market size through 2030. South America, the Middle East, and Africa remain nascent but show rising demand as hospitals digitize records and seek outsourced transcription partnerships.

Competitive Landscape

Strategic acquisitions are reshaping competition. Commure agreed to buy Augmedix for USD 139 million in 2024, forming the largest AI software provider focused on healthcare documentation. Microsoft finalized its earlier Nuance purchase to create an integrated voice-activated clinical assistant that embeds inside Office and Azure ecosystems.

Technology differentiation centers on accuracy, specialty content packs, and workflow depth. Solventum holds top radiology speech rankings, while DeepScribe focuses on oncology encounters and Ambience Healthcare covers primary care coding. Smaller innovators explore multilingual or low-bandwidth architecture to serve emerging markets, highlighting white-space opportunities in the medical transcription market.

Hybrid human-AI oversight models grow popular as vendors respond to hallucination concerns. Platforms now embed quality dashboards, confidence scoring, and audit trails to satisfy insurers and regulators. Providers gravitate to suppliers that demonstrate clear data-protection credentials and proven integration APIs, sustaining healthy but competitive growth dynamics within the medical transcription market.

Medical Transcription Industry Leaders

-

iMedX Inc.

-

Nuance Communications Inc.

-

Solventum

-

Global Medical Transcription LLC

-

Acusis LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Corti opened access to a healthcare-specialized Dictation API built on its Solo foundation model, giving developers premium speech-to-text tools.

- March 2025: Deepgram launched Nova 3 Medical, an AI speech-to-text model engineered for clinical environments.

- November 2024: Commure partnered with HCA Healthcare to deploy an ambient AI platform across 188 hospitals and 2,400 care sites.

- July 2024: Commure and Athelas signed a definitive agreement to acquire Augmedix, combining ambient AI assets across 20 health systems.

Global Medical Transcription Market Report Scope

Medical transcription refers to the conversion of the voice-based reports of doctors, physicians, and other healthcare providers into text-based electronic reports. This involves transcribing patient information and reports dictated by doctors into electronic text formats.

The medical transcription market is segmented by type, technology, mode of procurement, and end user. In terms of type, the market is segmented into software and services. By technology, the market is segmented into electronic medical record/electronic health record (EMR/EHR), picture archiving and communication system (PACS), radiology information system (RIS), speech recognition technology (SRT), and other technologies. By mode of procurement, the market is segmented into outsourcing, offshoring, and other modes of procurement. By end user, the market is segmented into hospitals, physician groups, clinics and clinical laboratories, and other end users. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market size and forecasts for the medical transcription market in value (USD) for the above segments.

| Software |

| Services |

| EHR-Integrated Speech Recognition |

| Stand-alone Speech Recognition Engines |

| PACS/RIS Integrated Modules |

| AI Ambient Scribe Systems |

| Other Platforms |

| Outsourcing |

| Offshoring |

| Hybrid (Captive + Outsourced) |

| Captive In-house |

| Hospitals |

| Physician Groups |

| Clinics & Clinical Laboratories |

| Ambulatory Surgical Centers |

| Telehealth Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution | Software | |

| Services | ||

| By Technology Platform | EHR-Integrated Speech Recognition | |

| Stand-alone Speech Recognition Engines | ||

| PACS/RIS Integrated Modules | ||

| AI Ambient Scribe Systems | ||

| Other Platforms | ||

| By Mode of Procurement | Outsourcing | |

| Offshoring | ||

| Hybrid (Captive + Outsourced) | ||

| Captive In-house | ||

| By End User | Hospitals | |

| Physician Groups | ||

| Clinics & Clinical Laboratories | ||

| Ambulatory Surgical Centers | ||

| Telehealth Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the medical transcription market?

The medical transcription market stands at USD 90.32 billion in 2025 and is on pace to reach USD 156.75 billion by 2030.

2. Which segment is growing fastest within the medical transcription market?

AI ambient scribe systems are advancing at a 15.02% CAGR through 2030, outpacing other technology segments.

3. Why is Asia-Pacific the fastest-growing region?

Rapid telehealth expansion, large multilingual populations, and heavy investment in digital health infrastructure lift Asia-Pacific growth to 13.56% CAGR.

4. How are regulations shaping demand for transcription solutions?

The 21st Century Cures Act and similar rules in Europe require structured, shareable records, pushing providers toward automated and auditable documentation platforms.

5. What risks could slow market growth?

Escalating cyber-security costs, physician concerns over AI errors, and sustainability scrutiny of cloud compute resources may restrain adoption momentum.

Page last updated on: