Medical Connectors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

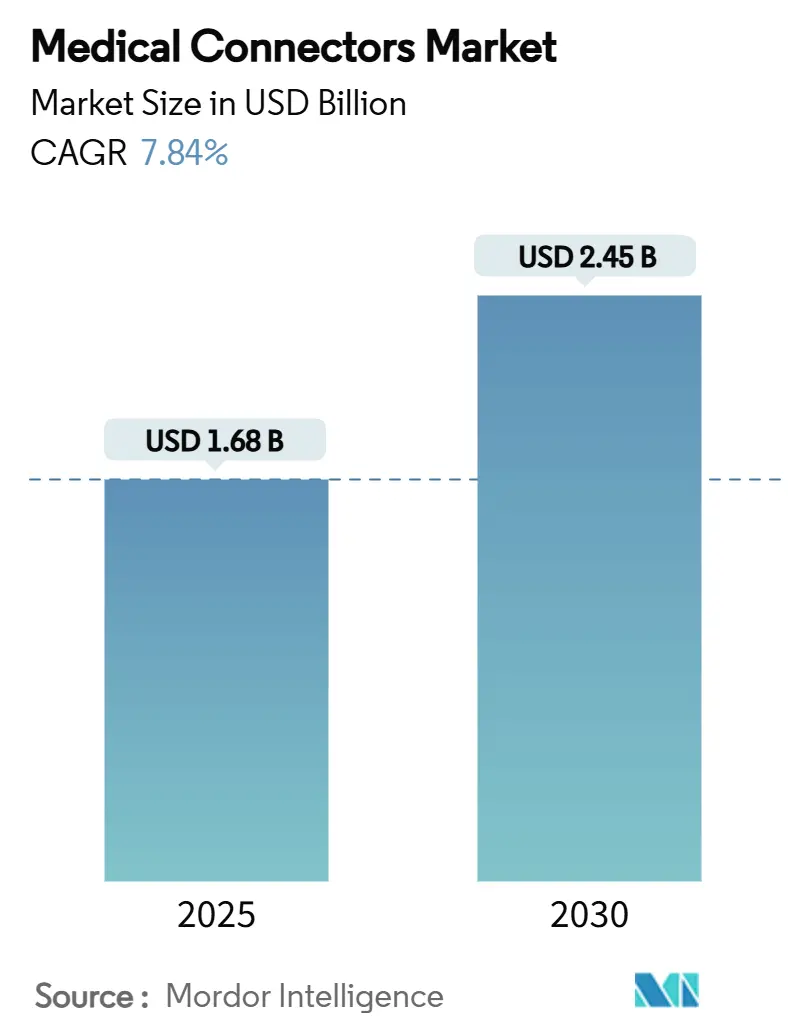

| Market Size (2025) | USD 1.68 Billion |

| Market Size (2030) | USD 2.45 Billion |

| Growth Rate (2025 - 2030) | 7.84% CAGR |

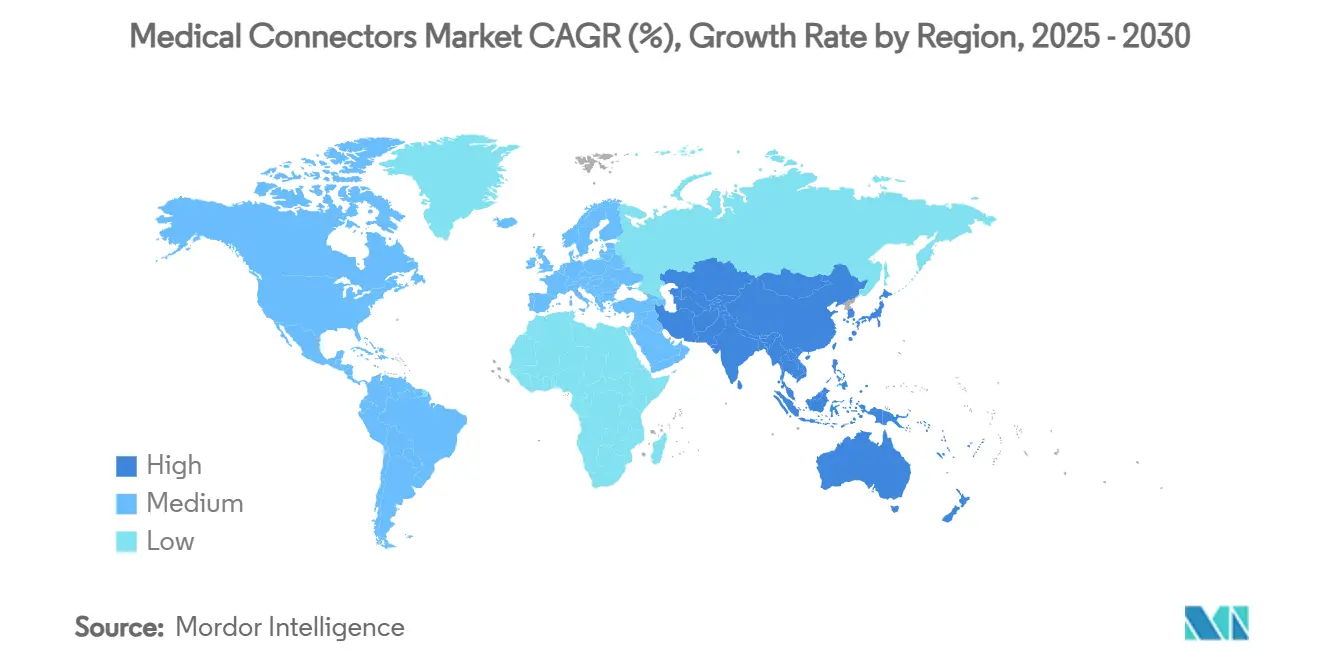

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Connectors Market Analysis by Mordor Intelligence

The medical connectors market size stands at USD 1.68 billion in 2025 and is forecast to reach USD 2.45 billion by 2030, reflecting a 7.84% CAGR through the period. Demand expansion arises from the steady shift toward digitally networked care, the proliferation of wearable monitors, and the growing adoption of single-use device platforms that rely on compact, sterilizable interfaces. Manufacturers are investing in magnetic quick-connect designs that eliminate mechanical wear and accelerate device turnaround times in intensive care units. Interoperability initiatives within hospital information systems reinforce the need for standardized pin configurations, while home-care adoption places equal emphasis on intuitive, patient-safe connection methods. Regional opportunity dispersion is pronounced: North America remains technology-centric, whereas Asia-Pacific benefits from capacity build-out in public hospital networks that prefer modular, multi-purpose connector families. Material science breakthroughs, particularly in silicone shielding and copper-alloy anti-corrosion treatments, further enhance lifespan and performance.

Key Report Takeaways

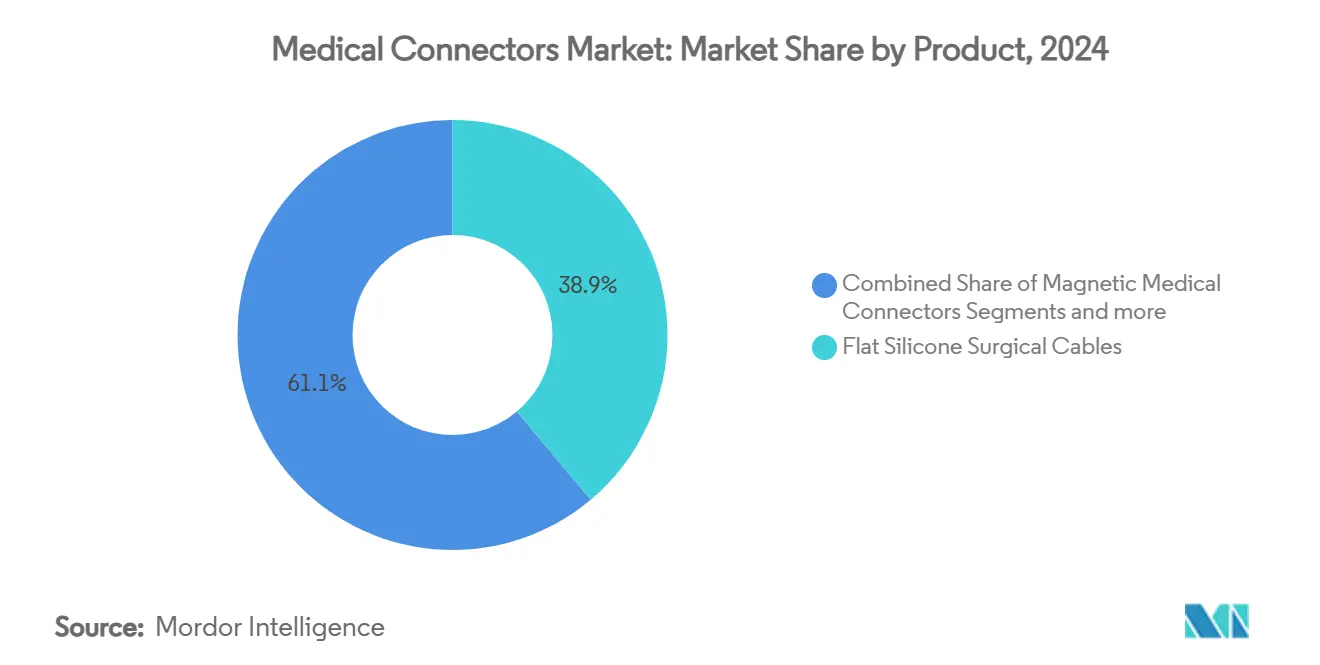

- By product category, flat silicone surgical cables captured 38.89% of the medical connectors market share in 2024. Magnetic medical connectors are projected to advance at an 8.65% CAGR through 2030, the highest growth among product segments.

- By application, patient monitoring devices held 32.23% of the medical connectors market size in 2024. Cardiology devices are forecast to grow at an 8.67% CAGR to 2030, the fastest within the application spectrum.

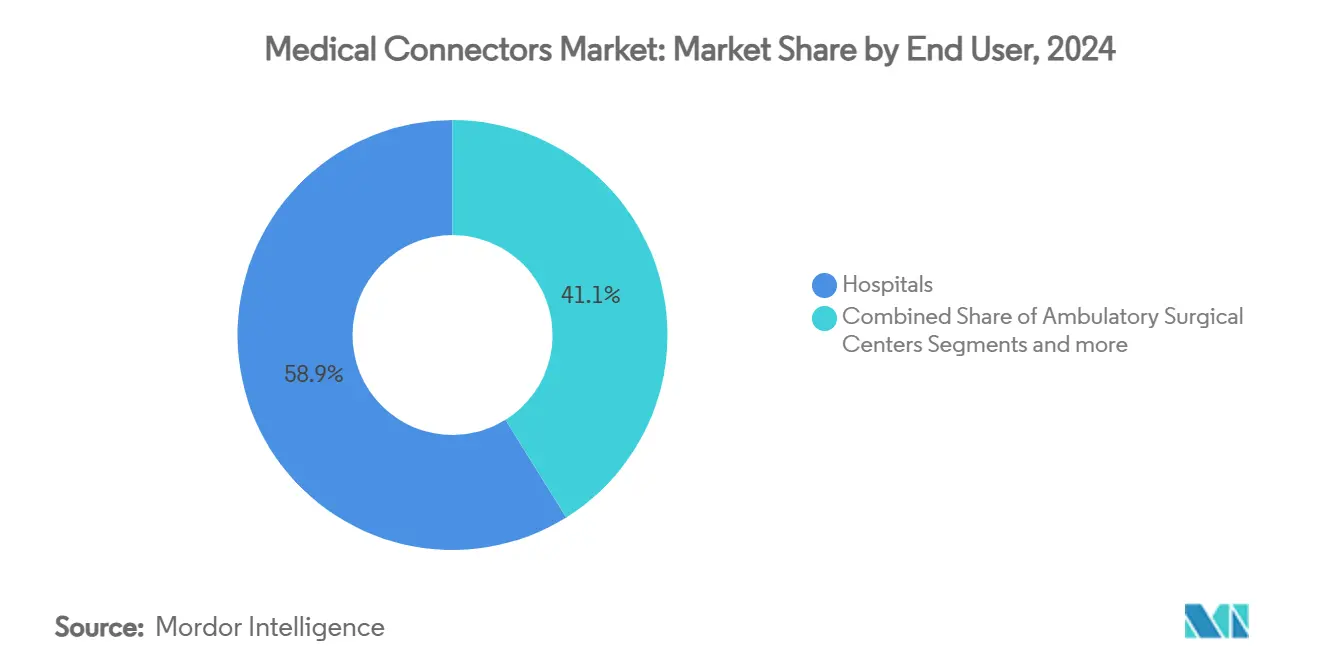

- By end user, hospitals accounted for 58.87% of the medical connectors market in 2024. Ambulatory surgical centers are expected to post an 8.77% CAGR through 2030, outpacing all other user groups.

- By geography, North America led with 41.03% revenue share in 2024. Asia-Pacific is projected to record the quickest regional expansion at an 8.89% CAGR through 2030.

Global Medical Connectors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic diseases | +2.1% | North America and Europe | Medium term (2-4 years) |

| Expansion of the medical device installed base | +1.8% | Asia-Pacific, spill-over to Middle East & Africa | Long term (≥4 years) |

| Shift toward home-care and remote monitoring | +1.5% | North America and Europe, expanding to APAC | Short term (≤2 years) |

| Miniaturization and high-density designs | +1.2% | Global, led by APAC manufacturing hubs | Medium term (2-4 years) |

| Hospital-grade magnetic quick-connect uptake | +0.8% | North America and Europe premium segments | Long term (≥4 years) |

| Disposable fluid-path connectors in single-use kits | +0.4% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Diseases

Elevated cardiovascular and diabetes prevalence has intensified real-time monitoring requirements that depend on robust, low-profile electrical interfaces. Implantable loop recorders and insulin infusion pumps increasingly specify moisture-resistant contact plating that supports uninterrupted telemetry during extended wear periods. Health systems pursuing predictive analytics mandate connectors that sustain high sampling frequencies without electromagnetic interference. As hospital workloads migrate toward proactive disease management, magnetic quick-connect solutions gain traction because they avoid arcing and reduce connector fatigue. Continuous data capture also amplifies cybersecurity scrutiny, prompting OEMs to specify shielded connector housings that integrate physical keying with encryption-ready wiring architectures.

Expansion of the Medical Device Installed Base

Asia-Pacific hospital expansions and robotics investments enlarge the cumulative equipment fleet, driving preference for interoperable connector footprints that streamline spare-parts logistics. Device miniaturization, illustrated by capsule endoscopes and micro-pumps, compresses available board space, compelling manufacturers to develop sub-millimeter pitch headers with solder-reflowable silicone over-molds. Retrofit programs targeting legacy infusion pumps open retrofit revenue streams for vendors able to certify updated connector blocks under revised electrical and biocompatibility norms. Surgical robotics adopters request high-cycle connectors capable of surviving 3,000 autoclave passes without plating delamination. Suppliers that offer end-to-end qualification data shorten OEM design cycles and gain an edge in the medical connectors market.

Shift Toward Home-Care and Remote Monitoring Solutions

Payers incentivize early discharge, channeling capital into remote vital-sign platforms that patients manage unaided. This trend pushes connector ergonomics toward one-handed, color-coded latching mechanisms that mitigate mis-mating risk. Wearable ECG patches require ultra-flexible leads that accommodate repetitive torso movement while preserving impedance stability [1]Molex, LLC, "Smart Skin Patches and Noninvasive Medical Sensing," molex.com. Disposable connector tips limit cross-contamination risk and lower reprocessing costs for home infusion therapies. Telecommunications upgrades, notably 5G rollouts, necessitate connectors with superior signal shielding to prevent packet loss during high-resolution biosignal streaming. These design imperatives are strengthening demand visibility across the medical connectors market.

Miniaturization and High-Density Multi-Contact Designs

High-definition imaging catheters and neuro-stimulation probes require contact counts exceeding 100 in footprints once dedicated to single-channel connectors. Nanocrystalline copper alloys improve conductivity at reduced diameters, while liquid-crystal polymer housings provide thermal stability during vapor-phase sterilization. Smaller contacts raise insertion-force challenges; therefore, vendors are adopting stepped, gold-plated geometries that maintain tactile feedback. High-density layouts amplify crosstalk risk, so differential-pair routing and integrated shielding rings become standard. The innovation race favors firms with fine-pitch stamping presses and laser microwelding expertise, strengthening competitive barriers within the medical connectors market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global and regional compliance | -1.4% | Global | Long term (≥4 years) |

| Sterilization-induced material degradation | -0.9% | High-volume surgical centers worldwide | Medium term (2-4 years) |

| Connector mis-mating hazards | -0.7% | North America and Europe | Short term (≤2 years) |

| Supply shortages of medical-grade resins | -0.6% | Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global and Regional Regulatory Compliance

The FDA’s transition to the Quality Management System Regulation that aligns with ISO 13485:2016 compels manufacturers to overhaul documentation architectures and audit procedures. Europe’s MDR regime imposes unique device identifier obligations, adding traceability costs to every connector batch. Markets in Latin America increasingly demand certified biocompatibility reports, elongating approval cycles for polymer revisions. Smaller suppliers struggle to finance concurrent submissions across multiple jurisdictions, accelerating consolidation within the medical connectors market. Cybersecurity clauses now extend to connectors that transmit patient identifiers, introducing encryption-testing steps that lengthen product validation timelines.

Sterilization-Induced Material Degradation Risk

Ethylene oxide capacity constraints drive hospitals toward vaporized hydrogen peroxide and gamma irradiation, yet both alternatives can embrittle polycarbonate housings or oxidize tin-lead solder joints. Failures manifest as micro-cracks that compromise insulation resistance on defibrillator cables. OEMs must run accelerated-aging studies for every sterilization permutation, stretching time-to-market. Material engineers are experimenting with cyclic olefin polymers that tolerate 55 kGy doses without mechanical drift, though cost premiums hinder rapid substitution. Until proven solutions scale, durability anxieties continue to temper adoption rates in the medical connectors market.

Segment Analysis

By Product: Surgical Cables Anchor the Portfolio

Flat silicone surgical cables retained a 38.89% stake in the medical connectors market share during 2024, underlining their continued primacy in electrosurgical handpieces and laparoscopic energy platforms. The segment benefits from silicone’s flexibility, dielectric stability, and compatibility with autoclave cycles, characteristics that shorten maintenance intervals and uphold electrical integrity. Advancements in layered extrusion now integrate two-tone insulation that provides instant visual damage detection, reinforcing hospital risk-management protocols. Magnetic medical connectors, though presently smaller in installed base, are forecast to log an 8.65% CAGR due to their contactless coupling that minimizes arc formation during high-current transfers. Disposable plastic connectors expand reception in single-use irrigation wands, where eliminating cleaning overhead aligns with infection-control mandates. Push-pull formats continue to address general ward monitoring, delivering a familiar tactile cue that nursing staff trust. Hybrid circular systems enable combined power, fiber, and pneumatic routing within robotic end-effectors, enhancing design freedom for surgical automation specialists. This plurality of formats ensures that the medical connectors market retains healthy product-mix dynamism.

Magnetic alternatives are reshaping purchasing criteria by prioritizing zero-wear longevity over upfront capital cost. Novel alloys such as gold-cobalt pellets enhance magnetic saturation limits, allowing downsizing without compromising retention force. Rapid detachment supports fall-prevention programs, as yanking leads from physiotherapy equipment no longer stresses device ports. Vendors integrating on-board EEPROM chips into connector shells create plug-and-play traceability, which helps technicians schedule predictive maintenance. Electrosurgical cable suppliers are exploring thermochromic jackets that visually indicate overheating, pre-empting insulation failure. The drive toward multi-contact density has spurred sub-assembly modularization, with OEMs outsourcing over-molding processes to connector specialists that hold ISO 14644-1 cleanroom certifications. These initiatives collectively sustain momentum for product innovation within the medical connectors market [2]TE Connectivity, "IoMT Sensors," te.com.

Note: Segment shares of all individual segments available upon report purchase

By Application: Monitoring Dominates, Cardiology Accelerates

Patient monitoring devices generated 32.23% of the medical connectors market size in 2024, supported by mandatory vital-sign capture in perioperative pathways. Multi-parameter monitors utilize color-coded snap connectors that permit rapid cable swaps without shut-downs. Integrated ECG and SpO₂ lead sets reduce bedside clutter, driving hospital preference for consolidated connector hubs. Cardiology equipment is poised for the quickest expansion at an 8.67% CAGR as implantable cardioverter defibrillators and left-ventricular assist devices multiply, each requiring hermetic feed-throughs that survive body-fluid exposure. Electrosurgical units increase current density demands that only silver-plated contacts can handle, boosting average selling prices in high-power connector niches. Diagnostic imaging modalities, especially portable ultrasound, incorporate high-speed coax arrays that deliver loss-less echo data. Respiratory care grows steadily with home ventilation adoption, prioritizing low-force coupling to minimize tracheostomy site stress. Collectively, diverse clinical use-cases reinforce sustained revenue visibility for stakeholders in the medical connectors market.

The cardiology segment’s pace benefits from value-based procurement that recognizes the downstream cost savings of accurate rhythm diagnostics. MRI-conditional pacemakers enforce non-ferromagnetic connector material selection, prompting suppliers to develop titanium-ceramic hybrids. Hemodynamic monitoring in cath labs integrates fiber-optic pressure sensors that require optical-electrical hybrid connectors with ingress-protection ratings above IP68. Ventilator manufacturers raise expectations by specifying 20,000 mating-cycle durability benchmarks, influencing polymer blend choices. Emerging AI-driven monitoring platforms retrieve four times more data packets per minute, necessitating connectors engineered for minimal contact resistance drift over prolonged use. Such application-level demands translate into steady product redesign cycles, ensuring recurring opportunities across the medical connectors market.

By End User: Hospitals Lead, ASCs Surge

Hospitals held 58.87% command of the medical connectors market in 2024 as their capital budgets underpin high-acuity device purchases that demand premium connector specifications. Group purchasing organizations negotiate volume rebates, incentivizing suppliers to maintain broad catalog coverage and rapid field-service capabilities. Hospital engineering teams increasingly favor connectors with integrated RFID tags that streamline asset tracking. Ambulatory surgical centers, though smaller in individual order size, are projected to outpace hospitals with an 8.77% CAGR, propelled by procedural migration from inpatient settings to lower-cost outpatient facilities. ASCs favour modular cabling kits that minimize set-up time and support fast room turnover. Home-care providers enter procurement matrices by scaling remote monitoring fleets, prompting demand for consumer-grade connectors verified for clinical accuracy.

In hospitals, the drive toward enterprise interoperability leads biomedical departments to standardize connector SKUs across multi-vendor fleets, simplifying maintenance training and reducing spare-part inventory. ASCs, operating on thinner margins, lean toward cost-optimized connector lines that still pass IEC 60601-1 leakage current tests. Vendor service models adapt by offering subscription-based connector replacement programs that align with ASC cash-flow profiles. Diagnostic laboratories, another modest yet steady customer cluster, require hermetically sealed connectors that endure corrosive reagent exposure [3]Ambulatory Surgery Center Association, "Sg2 2024 Annual Report Projects High Growth in ASC Volume," ascfocus.org. The heterogeneous end-user base necessitates flexible pricing architectures and multi-tier technical support, reinforcing competitive differentiation within the medical connectors market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 41.03% revenue leadership in 2024, reflecting mature capital equipment cycles and well-established compliance frameworks that reward early adoption of high-specification connectors. Value-based care metrics push hospitals to embed predictive maintenance sensors within connector housings, thereby reducing unplanned downtime. The region champions ISO 80369-7 implementation ahead of other geographies, accelerating replacement demand. Start-up ecosystems in Minneapolis and Boston foster next-generation neurostimulation devices, further lifting local connector design activity. Policy incentives for domestic semiconductor packaging benefit suppliers integrating miniaturized electrode arrays, maintaining technological headship for the medical connectors market.

Asia-Pacific will post the fastest regional trajectory at an 8.89% CAGR through 2030 as public health insurers in China and India commit to broadening access to chronic disease management technologies. Local OEMs are scaling infusion pump output, thereby enlarging baseline connector consumption. Regulatory agencies in Singapore and South Korea harmonize documentation with the US FDA, lowering duplication for global suppliers and hastening product launches. Government subsidies for indigenous medical electronics manufacturing reduce import dependency, prompting multinationals to establish connector assembly plants in Malaysia and Vietnam. Urbanization intensifies demand for patient monitoring systems in secondary cities, spreading volume beyond Tier 1 healthcare hubs and diversifying opportunity within the medical connectors market.

Europe maintains steady expansion driven by stringent environmental policies that prioritize recyclable connector materials. National health services renew aging device fleets, enforcing RoHS and REACH compliance that favors halogen-free insulation compounds. Collaborative purchasing platforms across the Nordics compress unit margins but guarantee multi-year volume commitments. Germany’s precision-engineering base continues to pioneer hybrid circular connectors for surgical robotics, with EU-funded research propelling material science improvements. Eastern Europe emerges as a cost-competitive manufacturing locus, providing a near-shore alternative for Western suppliers concerned about Asia-Pacific freight volatility. Consequently, the region balances performance leadership with sustainability interventions, sustaining its strategic relevance in the medical connectors market.

Competitive Landscape

The market exhibits moderate consolidation. TE Connectivity and Amphenol leverage vertically integrated stamping, plating, and over-molding operations across three continents, enabling dual-sourcing assurances prized by multinational device OEMs. Molex capitalizes on high-density fine-pitch board-to-board connectors derived from its telecom portfolio, adapting these designs for diagnostic imaging consoles. Smiths Interconnect exploits ceramic-to-metal sealing know-how to address implantable defibrillator feed-through demand, thereby defending profitable niches. Fischer Connectors focuses on sealed push-pull couplers for harsh sterile field conditions, differentiating through rapid-clean exterior geometries.

Strategic alliances feature prominently: TE Connectivity partners with sterilization service providers to co-validate material compatibility, reducing OEM test cycles. Amphenol’s medical division deploys digital twin simulations to forecast contact resistance drift over lifecycle extremes, a tactic that shortens prototype iterations. Emerging entrants target smart connector add-ons, embedding EEPROM or NFC chips that log mating cycles and flag impending service needs. Price competition remains contained in high-reliability applications where qualification costs deter low-price challengers, though commodity disposables face margin erosion from Asian contract manufacturers. Patent portfolios covering magnetic alignment and keyed housing geometry underpin litigation defenses, sustaining entry barriers within the medical connectors market.

Sustinability is an evolving battleground. Leading players pilot closed-loop silicone recycling programs that reclaim insulation scrap from cable production. Bio-based polymer experimentation continues, although biocompatibility certification hurdles prolong commercialization. Suppliers that transparently publish life-cycle assessments gain an edge with European healthcare chains that embed carbon-footprint clauses in tender documents. Digital service layering is another frontier; connectors that stream real-time temperature and insertion cycle data integrate seamlessly with hospital asset-management software, creating aftermarket revenue streams that diversify beyond hardware. These competitive vectors collectively shape trajectory and value capture across the medical connectors market.

Medical Connectors Industry Leaders

-

Amphenol Corporation

-

Smiths Interconnect

-

TE Connectivity

-

Fischer Connectors SA

-

Molex LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed acquisition of BIOTRONIK’s vascular intervention business for EUR 760 million (USD 827 million), broadening its portfolio of drug-coated balloons and stents that rely on high-pressure vascular connectors.

- June 2025: Phillips-Medisize introduced TheraVolt medical connectors engineered to handle mixed signal and high-voltage lines in compact device architectures.

- November 2024: Chi Feng launched QuikLock bladder perfusion and Gen2Zero needle-free connectors aimed at lowering infection risk in urology and infusion therapy.

- October 2024: Binder unveiled the PBC15 connector system that transmits elevated currents within restricted spaces for miniaturized surgical tools.

Global Medical Connectors Market Report Scope

Medical connectors are the component of devices that connect to other medical devices such as syringes, tubing, and catheters. Every medical device that has its links can also be used on a single patient with several types of medical devices at the same time. In medical facilities, patients may use such devices over their entire lives for long-term care.

The market is segmented by product (flat silicone surgical cables, embedded electronics connectors, radio-frequency connectors, disposable plastic connectors, hybrid circular connectors, and receptacle systems, power cords with retention systems, lighted hospital-grade cords, magnetic medical connectors, and push-pull connectors), application (patient monitoring devices, electrosurgical devices, diagnostic imaging devices, cardiology devices, analyzers and processing equipment, respiratory devices, dental instruments, endoscopy devices, neurology devices, enteral devices, other applications), end user (hospitals, ambulatory surgical centers, and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across significant regions globally. The report offers the value (in USD million) for the above segments.

| Flat Silicone Surgical Cables |

| Embedded Electronics Connectors |

| Radio-Frequency Connectors |

| Disposable Plastic Connectors |

| Hybrid Circular Connector & Receptacle Systems |

| Power Cords with Retention Systems |

| Lighted Hospital-Grade Cords |

| Magnetic Medical Connectors |

| Push-Pull Connectors |

| Patient Monitoring Devices |

| Electrosurgical Devices |

| Diagnostic Imaging Devices |

| Cardiology Devices |

| Analysers & Processing Equipment |

| Respiratory Devices |

| Dental Instruments |

| Endoscopy Devices |

| Neurology Devices |

| Enteral Devices |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Flat Silicone Surgical Cables | |

| Embedded Electronics Connectors | ||

| Radio-Frequency Connectors | ||

| Disposable Plastic Connectors | ||

| Hybrid Circular Connector & Receptacle Systems | ||

| Power Cords with Retention Systems | ||

| Lighted Hospital-Grade Cords | ||

| Magnetic Medical Connectors | ||

| Push-Pull Connectors | ||

| By Application | Patient Monitoring Devices | |

| Electrosurgical Devices | ||

| Diagnostic Imaging Devices | ||

| Cardiology Devices | ||

| Analysers & Processing Equipment | ||

| Respiratory Devices | ||

| Dental Instruments | ||

| Endoscopy Devices | ||

| Neurology Devices | ||

| Enteral Devices | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical connectors market and its growth outlook?

The medical connectors market size is USD 1.68 billion in 2025 and is projected to reach USD 2.45 billion by 2030, advancing at a 7.84% CAGR.

Which product type holds the largest share of the medical connectors market?

Flat silicone surgical cables led with 38.89% market share in 2024, reflecting their widespread use in electrosurgical applications.

Which application segment is expanding the fastest?

Cardiology devices are expected to grow at an 8.67% CAGR through 2030 due to rising investment in cardiac rhythm management technologies.

What region is forecast to record the highest growth rate?

Asia-Pacific is projected to register an 8.89% CAGR through 2030, supported by healthcare infrastructure expansion in China and India.

How concentrated is the competitive landscape?

The top five suppliers control roughly 55% of global revenue, giving the market a moderate concentration score of 5.

What key trend is reshaping connector design for home-care equipment?

The shift toward remote monitoring accelerates demand for low-profile, patient-friendly connectors that can maintain signal integrity over wireless networks.

Page last updated on: