Market Overview

| Study Period | 2020 - 2031 |

|---|---|

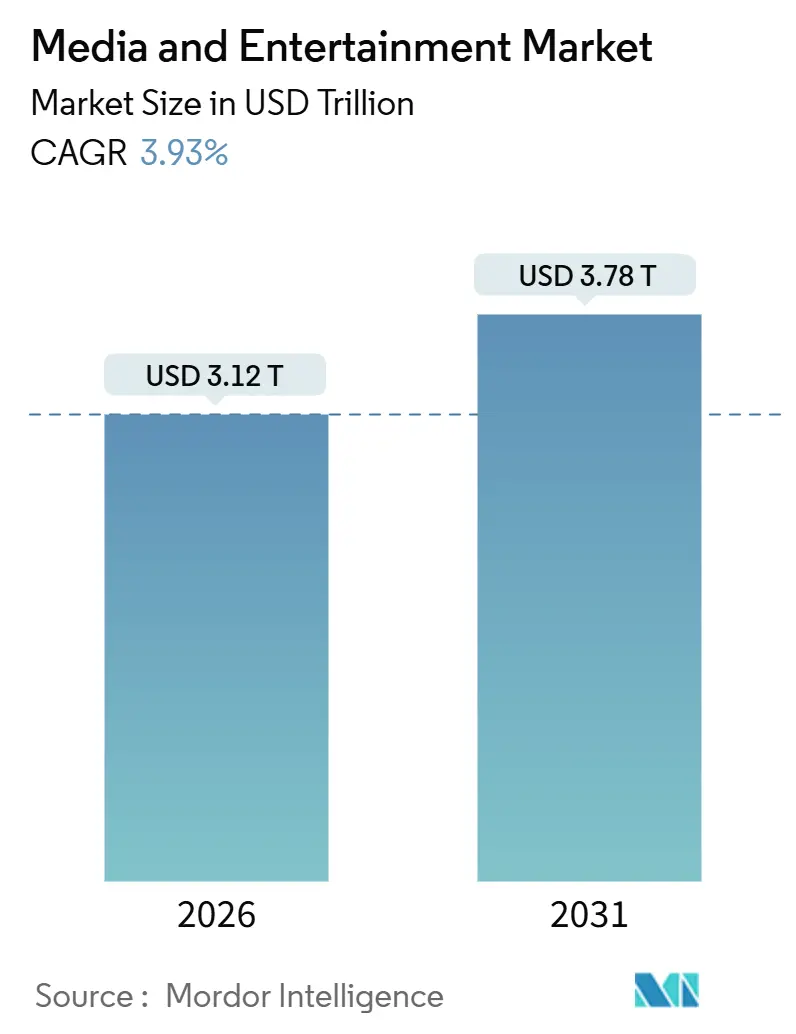

| Market Size (2026) | USD 3.12 Trillion |

| Market Size (2031) | USD 3.78 Trillion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

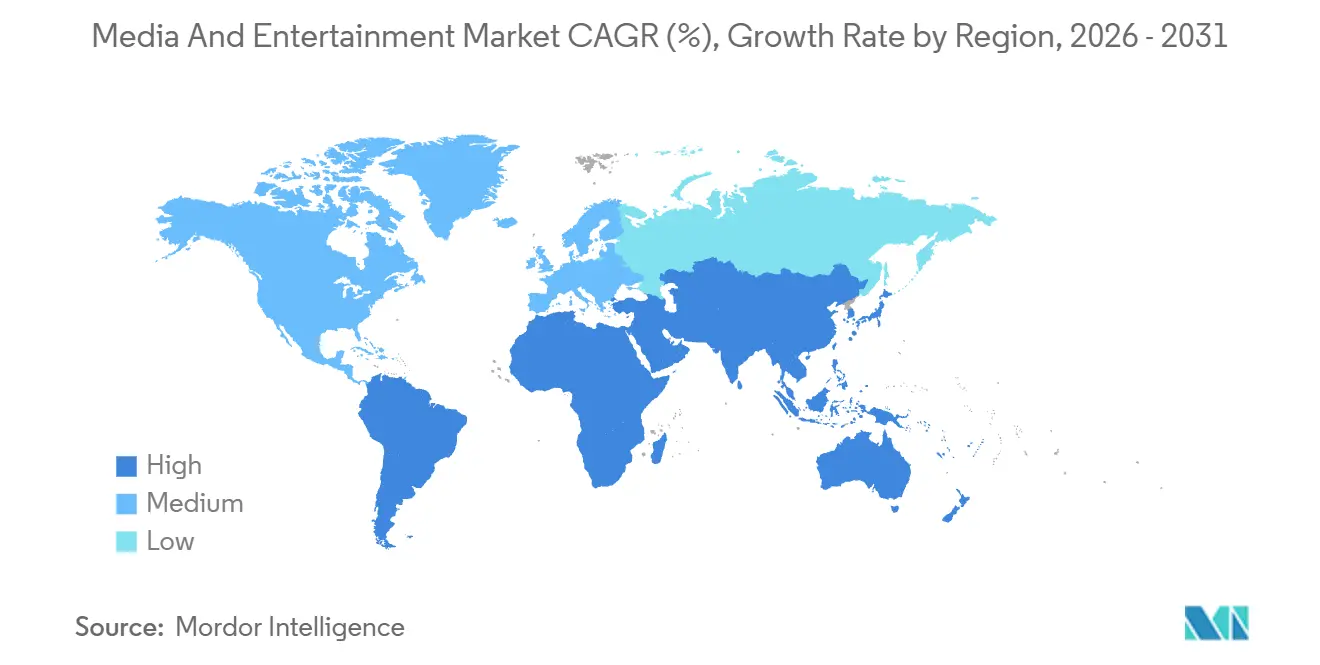

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

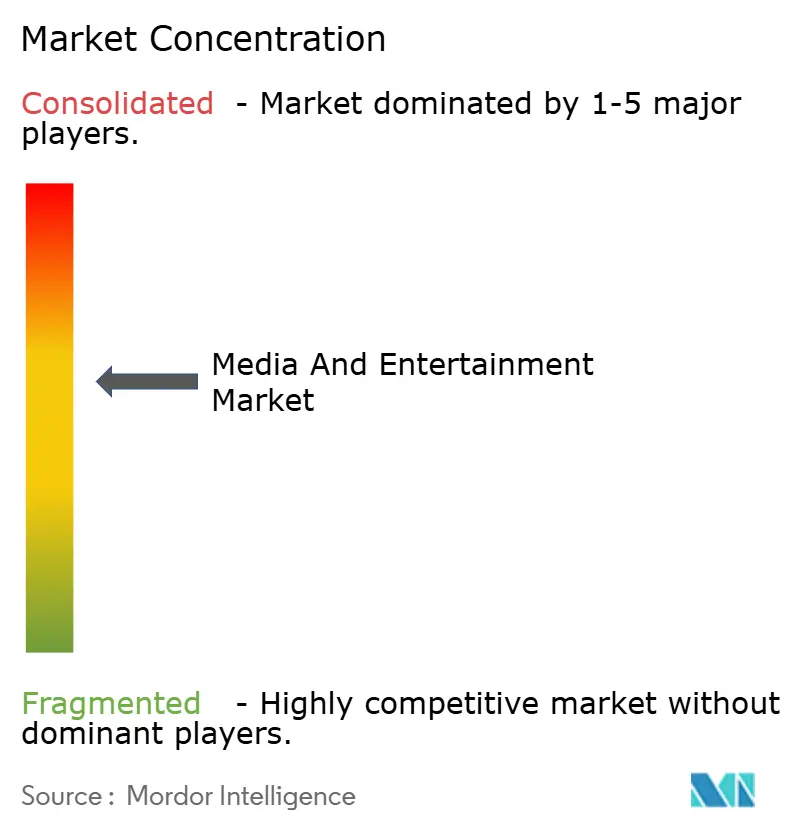

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Media And Entertainment Market Analysis by Mordor Intelligence

The media and entertainment market size stood at USD 3.12 trillion in 2026 and is projected to reach USD 3.78 trillion by 2031, reflecting a 3.93% CAGR over the forecast period. Growth rests on the pivot from legacy print and linear broadcast to streaming, connected-TV advertising, and AI-driven personalization. Large advertisers are shifting budgets toward addressable video as smartphone saturation, 5G speeds, and smart-TV penetration expand audiences. Digital fatigue in North America is encouraging hybrid ad-supported tiers, while India, China, and Brazil add new users at a faster clip than mature regions. Meanwhile, software-defined production, reduced localization costs, and virtual sets allow smaller studios to match incumbent production values, intensifying competition across the value chain.

Key Report Takeaways

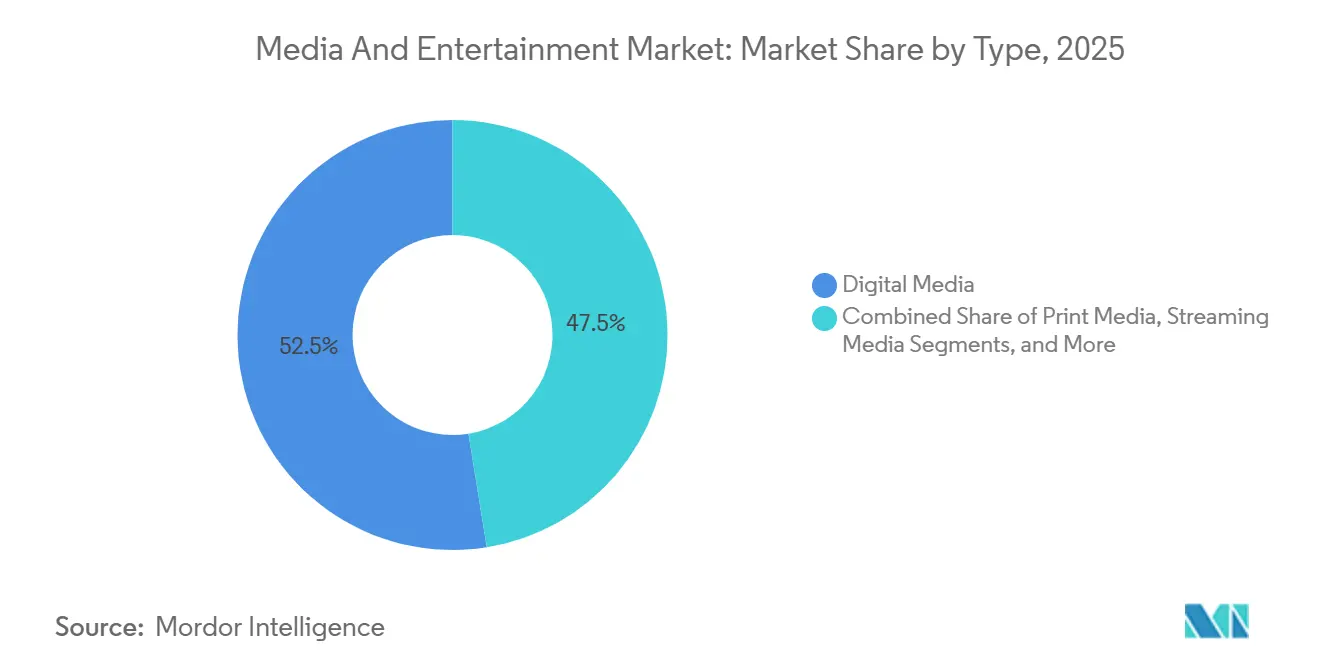

- By content type, digital media led with 52.54% revenue share in 2025, whereas streaming platforms are advancing at a 4.77% CAGR through 2031.

- By revenue model, advertising held 47.82% of 2025 turnover, yet subscriptions are posting the quickest rise at 4.81% CAGR to 2031.

- By device platform, smartphones and tablets commanded 51.43% of 2025 revenue, but smart TVs and set-top boxes are growing at a 4.69% CAGR.

- By geography, North America held 39.87% media and entertainment market share in 2025, while Asia-Pacific is set to log the fastest 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Media And Entertainment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G-enabled mobile video consumption in Asia | +0.8% | Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| Surging connected-TV ad spend by U.S. retail and CPG brands | +0.7% | North America, early adoption in Europe | Short term (≤ 2 years) |

| Rapid uptake of FAST channels in Europe | +0.6% | Europe, expanding to South America | Medium term (2-4 years) |

| Generative AI-based local-language dubbing expanding OTT reach in Middle East | +0.5% | Middle East and Africa, Asia-Pacific secondary | Long term (≥ 4 years) |

| Emergence of virtual production studios reducing content creation costs | +0.4% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| In-game advertising monetization in mobile esports titles | +0.3% | Asia-Pacific dominant, North America secondary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of 5G-Enabled Mobile Video Consumption In Asia

Asia-Pacific crossed 1.7 billion 5G connections in 2025, lowering latency below 20 milliseconds and turning mobile into the primary screen for video. Indian operators bundled unlimited streaming in low-cost data plans, lifting regional-language short-video apps to 40% of daily active users. Hyper-localized creators bypassed traditional gatekeepers, while programmatic mobile video ad spend reached USD 28 billion in 2025, a 35% jump year over year. Affordable 5G devices priced under USD 200 opened tier-2 and tier-3 cities where fixed broadband penetration lags, providing new runways for the media and entertainment market.

Surging Connected-TV Ad Spend By U.S. Retail And CPG Brands

United States connected-TV outlays hit USD 26.6 billion in 2025, with retail and CPG supplying 38% of incremental dollars as first-party purchase data drove conversion rates three to five times above linear TV.[1]“U.S. Podcast Advertising Revenue Surpasses USD 2.5 Billion,” Interactive Advertising Bureau, iab.com Netflix, Disney+, and Amazon launched ad tiers, adding 60% more premium inventory and letting brands reach cord-cutters at household level. Cross-platform measurement standards from the Joint Industry Committee calmed attribution concerns, shifting budgets structurally toward connected-TV.

Rapid Uptake Of FAST Channels In Europe

FAST channels claimed 35% of streaming hours in Spain by late 2025 as viewers battled subscription fatigue. Samsung TV Plus, Rakuten TV, and Pluto TV launched over 400 localized channels across Germany, France, and the United Kingdom, pushing European FAST ad revenue to EUR 1.8 billion (USD 2.0 billion) in 2025. Lighter EU content-quota rules and smart-TV household penetration above 60% enable FAST to keep siphoning spend from shrinking linear inventory.

Generative-AI Based Local-Language Dubbing Expanding OTT Reach In Middle East

Neural voice synthesis cut dubbing costs by 60–70% in 2025, letting Amazon Prime Video add Arabic tracks to 200 titles and see engagement equal to human dubs. In markets where English proficiency is below 40%, willingness to pay rises 25–30% when native audio is available. By scaling AI dubbing, platforms unlock growth in regions where content availability outweighs price sensitivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened EU regulatory scrutiny on targeted digital ads | -0.5% | Europe, spillover effects in North America | Short term (≤ 2 years) |

| Piracy and illegal restreaming curtailing premium OTT ARPUs in Asia-Pacific | -0.4% | Asia-Pacific dominant, emerging in Africa | Medium term (2-4 years) |

| Supply-chain shortages of next-gen graphics chips for immersive media | -0.3% | Global, acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising content acquisition costs eroding streaming profitability | -0.4% | Global, concentrated among subscription platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened EU Regulatory Scrutiny On Targeted Digital Ads

The Digital Services Act forced explicit opt-in consent, cutting addressable video audiences 15–20% and driving compliance costs such as Meta’s EUR 500 million (USD 565 million) annual spend. Lower consent rates in Germany and France dampen conversion efficiency, pushing advertisers toward contextual targeting that delivers weaker returns and slowing media and entertainment market revenue expansion in Europe.

Piracy And Illegal Restreaming Curtailing Premium OTT ARPUs In Asia-Pacific

Unauthorized streams robbed legitimate platforms of USD 9 billion in potential 2025 revenue, with 40–50% of consumers in India, Indonesia, and the Philippines accessing illicit content every month. Low ARPUs of USD 2–4 constrain content investment, and site-blocking orders are routinely bypassed via VPNs, trapping platforms in a low-margin equilibrium and restraining the media and entertainment market’s monetization upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Streaming Platforms Overtake Legacy Digital

Streaming posted the fastest 4.77% CAGR, while digital media retained 52.54% of revenue share in 2025. Print continued its slide as mobile-first news apps ate into circulation, while video games and esports delivered double-digit mobile revenue in Asia-Pacific. Virtual reality accounted for less than 2% of the media and entertainment market despite USD 15 billion in investments from Meta, Apple, and Sony. Podcast ad revenue exceeded USD 2.5 billion in 2025, underscoring advertiser appetite for high-engagement audio.

The media and entertainment market for streaming is poised to expand as on-demand formats align with younger audiences, while legacy television grapples with an aging audience. Subscription fatigue is steering cost-conscious households toward ad-supported tiers, and high-end franchises migrate from pay-per-view to bundled offerings, pressuring transactional models but bolstering stickiness for hybrid platforms.

By Revenue Model: Hybrid Tiers Balance Growth And Risk

Advertising accounted for 47.82% of revenue in 2025, yet subscriptions are expanding fastest at a 4.81% CAGR. The media and entertainment market size linked to hybrid tiers is swelling as Netflix’s ad plan reached 40 million monthly users. Giants are packaging gaming, merchandise, and live events around marquee IP. Disney earned USD 5 billion in 2025 licensing fees.

Ad-only players face cyclical risk when macro conditions soften, whereas subscription-only services battle churn when content pipelines thin. A balanced portfolio shields cash flows, with advertising subsidizing entry-level tiers and IP extensions deepening monetization. Future regulation on algorithmic transparency, especially in Europe, could tilt the scales again by limiting ad yield optimization. [2]Disney Licensing Revenue Fiscal 2025,” The Walt Disney Company, thewaltdisneycompany.com

By Device Platform: Smart TVs Climb As Mobile Levels Off

Smartphones and tablets backed 51.43% of 2025 revenue, yet smart TVs and set-top boxes are rising at a 4.69% CAGR as connected-TV ad demand accelerates and 4K sets become affordable. Smart-TV household penetration exceeded 60% in North America, [3]Smart TV Household Penetration Exceeds 60% in North America,” Consumer Technology Association, cta.tech cementing the large screen as a prime ad canvas. The media and entertainment market share shifting toward smart TVs also raises average CPMs for premium video.

PC relevance is sliding for pure entertainment, though esports viewing and e-learning sustain niche demand. Gaming consoles serve double duty as content hubs, with over half of owners streaming video weekly. VR and AR hardware shipped 5 million units in 2025, hinting at gradual mainstreaming, yet the installed base is still too small to redirect significant wallet share from established devices.

Geography Analysis

North America retained 39.87% media and entertainment market share in 2025, buoyed by USD 26.6 billion connected-TV ads and subscription penetration exceeding three-quarters of broadband homes. However, saturation is constraining net additions, and regulators are scrutinizing data-privacy practices. Mexico is a bright spot as 5G expands, while password-sharing crackdowns lifted U.S. paid subscriber counts.

Asia-Pacific is on a 5.03% CAGR path, driven by India’s 300 million 5G users, China’s USD 45 billion mobile-gaming haul, and Southeast Asia’s rising middle class. Domestic Chinese platforms dominate via localized content and social integration, whereas foreign entrants face ownership caps. Japan and South Korea boast high per-capita spend, and Australia mirrors U.S. dynamics but on a smaller scale.

Europe posts steady progress powered by FAST channel uptake, yet the Digital Services Act and Digital Markets Act weigh on targeted ad returns. The United Kingdom, Germany, and France top revenue ranks, though Poland and Romania deliver faster growth from lower bases. South America, led by Brazil’s 80 million OTT subscribers, benefits from telco bundles and local originals. The Middle East and Africa lag in payment infrastructure, yet AI dubbing and mobile money are lowering barriers, with Saudi Arabia’s Vision 2030 accelerating digital entertainment investment.

Regulatory Landscape

Regulation is tightening across streaming, advertising, and platform accountability, with Europe standing out for stricter rules on targeted ads and consent under the Digital Services Act. These changes have reduced addressable video audiences and increased compliance costs for large platforms. In the United Kingdom, implementation steps tied to the Media Act 2024 are bringing larger video-on-demand services (over 500,000 UK users) under enhanced Ofcom oversight, including new content standards and accessibility-related codes. This raises the compliance bar for OTT operators that historically operated under lighter on-demand frameworks.

In North America, policy is also moving on market structure and local content funding. In July 2026, the US Federal Communications Commission announced a planned August 6, 2026 vote to repeal the 39% national broadcast ownership cap, shifting from a hard reach limit to case-by-case review and reopening consolidation discussions among broadcast groups. In Canada, the CRTC set a May 2026 framework requiring online streaming services with more than CAD 100 million in annual Canadian revenue to contribute 25% of those revenues to support Canadian and Indigenous content. That requirement directly affects the unit economics of global streamers and their local commissioning and licensing strategies.

Value Chain Analysis

The value chain runs from ideation and rights acquisition through production and post-production (including VFX and localization), packaging, and distribution across streaming, linear broadcast, social video, and gaming platforms. Monetization follows via advertising, subscription, transactional models, and licensing and merchandising.

Delivery is increasingly managed through two linked pipelines: the movement of large media files (commonly via cloud storage and accelerated transfer tools) and the handling of metadata and rights management. Together, these functions shape discoverability, recommendations, and accurate ad and royalty reporting across territories. Bottlenecks show up most in cross-border delivery operations and fragmented tooling, where disconnected systems still struggle to track complex versioning, clearances, and partner deliveries. This leads to backlogs and rework when volumes spike. Platform intermediaries also influence economics, especially for subscription flows routed through third-party billing, where mobile app stores can take 15-30% of subscription revenue. As a result, streamers and publishers increasingly steer users toward direct billing, bundles, or operator partnerships. Competitive differentiation is shifting toward software-defined production, AI-enabled localization and dubbing, and dynamic ad insertion, which can shorten time-to-market and improve yield on connected-TV and FAST inventory.

Competitive Landscape

Roughly 45% of 2025 global revenue was held by the top 10 firms, pointing to moderate concentration. Technology giants weaponize cloud scale and AI recommendations to erode studio moats, while regional specialists thrive on language and cultural proximity. ByteDance’s TikTok surpassed 1 billion daily users, monetizing via in-feed ads and commerce.

Virtual production, AI dubbing, and dynamic ad insertion are key differentiators, driving double-digit increases in engagement and retention. Regulatory complexity, especially in Europe, favors larger incumbents able to absorb compliance overheads, while smaller entrants navigate fragmented rules at a higher relative cost.

Business-model agility now sets resilient leaders apart from scale-focused peers. Netflix's FIFA Women's World Cup deal highlights its shift to premium live sports, driving ad and subscription growth. Amazon's ad-supported Prime Video tier uses first-party commerce data to attract brand budgets. Disney's Hulu integration reduces marketing costs and churn, demonstrating the benefits of bundling. Paramount's Skydance merger and Sony's Crunchyroll consolidation emphasize vertical integration to monetize intellectual property and highlight the importance of balance-sheet scale in funding blockbuster content.

Media And Entertainment Industry Leaders

News Corporation

Comcast Corporation

Walt Disney Company

Warner Bros. Discovery, Inc.

Paramount Global

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are clustering around approaches that can lower content supply-chain costs while improving monetization quality, particularly in ad-supported video (connected TV and FAST) and localization at scale. Europe offers a visible whitespace for FAST growth backed by observed usage, with FAST channels reaching 35% of streaming hours in Spain by late 2025 and platforms such as Samsung TV Plus, Rakuten TV, and Pluto TV expanding localized channel lineups across major markets. That expansion supports additional advertiser inventory at a time when tighter targeted-ad rules are raising the value of reach and contextual placement.

In the Middle East and Africa, AI-driven dubbing and localization is an actionable lever tied to cost and availability. Neural voice synthesis cuts dubbing costs by 60-70% in 2025, and Amazon Prime Video is expanding Arabic availability across hundreds of titles, improving engagement where native audio changes willingness to pay. Investment in infrastructure and production capacity is also creating room for new formats and operating models. In July 2026, ByteDance began construction of a large data center complex in Ceara, Brazil, and Meta detailed a major expansion of its Richland Parish, Louisiana data center campus, reinforcing a move toward heavier compute for recommendation, personalization, and generative AI workflows that sit behind streaming, social video, and advertising products. On the production side, Netflix reached a construction milestone in June 2026 at the Fort Monmouth production hub in New Jersey, signaling continued studio build-out that can support higher throughput and shorter production cycles. At the same time, piracy and illegal restreaming continues to constrain monetization in Asia-Pacific, with meaningful revenue leakage in 2025 creating demand for stronger anti-piracy enforcement, watermarking, and more compelling low-price hybrid tiers to convert viewers into legitimate subscriptions or ad-supported users.

Recent Industry Developments

- July 2026: The US Federal Communications Commission announced a planned August 6, 2026 vote to repeal the 39% national TV ownership cap, replacing a hard reach limit with a case-by-case review approach. A rule change of this kind alters consolidation constraints for broadcast groups and can reshape bargaining power for content, sports rights, and national ad inventory.

- June 2026: Comcast announced plans to separate into two independent, publicly traded companies via a tax-free spin-off of NBCUniversal and Sky from its connectivity-focused operations. The move creates a more focused global media entity for content, advertising, and distribution partnerships, while the remaining business centers on broadband and wireless economics and investment priorities.

- May 2026: The CRTC established a new framework requiring online streaming services with more than CAD 100 million in annual Canadian revenue to contribute 25% of revenues toward Canadian and Indigenous content. This increases the effective cost of operating in Canada for large global platforms and influences decisions around local commissioning, licensing, and pricing for ad-supported and subscription tiers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the value of media and entertainment content and services that reach end users through advertising-funded, subscription, and transactional revenue models, across major formats such as video, audio, games, publishing, and live entertainment.

Scope exclusions: Hardware/device sales, telecom carriage fees, and pure infrastructure revenues are not counted in this market sizing.

Segmentation Overview

- By Type

- Print Media

- Newspaper

- Magazines

- Billboards

- Banners, Leaflets and Flyers

- Other Print Media

- Digital Media

- Television

- Music and Radio

- Electronic Signage

- Mobile Advertising

- Podcasts

- Other Digital Media

- Streaming Media

- OTT Streaming

- Live Streaming

- Video Games and eSports

- Virtual / Augmented Reality Content

- Print Media

- By Revenue Model

- Advertising

- Subscription

- Pay-Per-View / Transactional

- Licensing and Merchandising

- By Device Platform

- Smartphones and Tablets

- Smart TVs and Set-top Boxes

- PCs and Laptops

- Gaming Consoles

- VR / AR Headsets

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of what gets counted as media and entertainment revenues and what does not, then mapping those revenue pools across regions. For that, we refer to public datasets and explainers such as national statistics offices, the US Bureau of Economic Analysis for selected media spending lines, UNESCO Institute for Statistics for cultural indicators, the International Telecommunication Union for connectivity context, and the World Bank for macro and population series.

We also review company annual reports, investor presentations, and earnings transcripts to understand revenue mix and pricing direction in areas like subscriptions, advertising, and transaction-based purchases. Where available, patent databases are checked to sanity-test adoption direction for immersive formats and XR experiences. For market hygiene, a paid subscription for company financials and intelligence, plus news and financials, is used to spot corporate actions and reporting changes that can distort year over year comparability. These examples are illustrative, and many other public and proprietary sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test revenue logic, pricing movement, and how content is monetized across advertising, subscription, and transactional routes. We spoke with a mix of content owners, distributors, platform operators, and adjacent service providers, then validated assumptions across APAC, EMEA, and the Americas so regional skews do not slip into the global totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 21% | APAC: 44% |

| Mid tier: 53% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 21% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where published revenue lines and proxy indicators are used to reconstruct the demand pool by monetization route and region, and then reconciled into a single market number. To keep the outputs practical, we corroborate the result with selective bottom-up approximations such as sampled average revenue per user for subscriptions, ad load and CPM direction checks for ad-funded content, and volume times average price for transactional categories where credible public signals exist.

Inputs are chosen because they can be tracked every year without relying on internal platform data. Examples include advertising spend direction across major channels, subscription penetration and churn cues, pricing and bundling trends (including annual price resets), content release cadence and live event attendance momentum, and broad consumer spending capacity tied to GDP and population. Forecasts use scenario analysis supported by interview feedback, where the base case is shaped by the expected pace of price increases, ad demand recovery, and engagement shifts across screens, then downside and upside cases are applied when those drivers move faster or slower than expected. When a bottom-up cross-check is thin for a niche area, the gap is handled through conservative penetration assumptions and then re-tested in validation before final sign-off.

Data Validation & Update Cycle

Validation is done through a set of cross-checks that look for logical fit between the modeled market value and independent signals, including macro spend capacity, regional ad intensity, and subscription price moves. Outliers are investigated by reviewing definition fit, currency timing, and one-off events, then the assumptions are adjusted only when they can be defended with at least two supporting data points.

Before numbers are finalized, the model is reviewed in steps by another analyst to catch formula drift and category overlap, and experts are re-contacted if a major variance appears versus expected industry direction. Reports are refreshed annually, and interim updates are triggered when material events occur, such as policy changes, major mergers, or sharp pricing resets. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Media and Entertainment Market Landscape Market Estimate Compared With Other Published Estimates

Published market values for the media and entertainment landscape often do not match, even when the time period looks similar. Differences typically come from what revenue streams are included, how advertising and subscription value are treated across formats, and how currency timing and inflation are handled.

Some published figures expand the scope by blending in adjacent spend lines like connectivity, device hardware, or broad consumer technology outlays, which can push totals upward even if media usage is the real focus. In Mordor Intelligence, the count is limited to content and service revenues across advertising-funded, subscription, and transactional models, with hardware sales, telecom carriage fees, and pure infrastructure revenues excluded so the number stays tied to monetized media and entertainment activity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.12 T (2026) | |

| Global Consultancy A | USD 2.90 T (2024) | Uses a revenue snapshot anchored two years earlier, and the public summary does not clarify category-level inclusions or how pricing resets and currency conversion timing are normalized across regions. |

| Industry Research House B | USD 2.87 T (2025) | Often presented as a broad entertainment and media revenue pool, with limited disclosure in the public view on whether adjacent tech, distribution pass-throughs, or resales are netted out consistently across segments. |

Across the three figures, the spread is mainly explained by year alignment and by how much adjacent spend is allowed into the total. By keeping the scope tied to monetized content and services and then stress-testing key drivers like advertising intensity, subscription pricing, and transactional demand, our estimate stays easier to trace and repeat when the market shifts.

Key Questions Answered in the Report

What is the current value of the media and entertainment market?

The market was valued at USD 3.12 trillion in 2026 and is forecast to reach USD 3.78 trillion by 2031.

How fast is streaming revenue growing compared with legacy digital channels?

Streaming platforms are projected to grow at a 4.77% CAGR through 2031, outpacing the broader market’s 3.93% CAGR.

Which region offers the fastest growth opportunities?

Asia-Pacific is set to record a 5.03% CAGR as 5G adoption, mobile gaming, and localized content expand the addressable base.

Why are hybrid ad-supported subscription tiers gaining traction?

Hybrid tiers combine lower entry prices with advertising, balancing revenue diversification and reducing churn, especially in mature markets.

What technologies are shaping future competition?

AI-driven dubbing, virtual production studios, and dynamic ad insertion are lowering production costs and raising engagement, helping new entrants challenge incumbents.

Page last updated on: