| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 7.18 Billion |

| Market Size (2030) | USD 12.10 Billion |

| CAGR (2025 - 2030) | 11.00 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

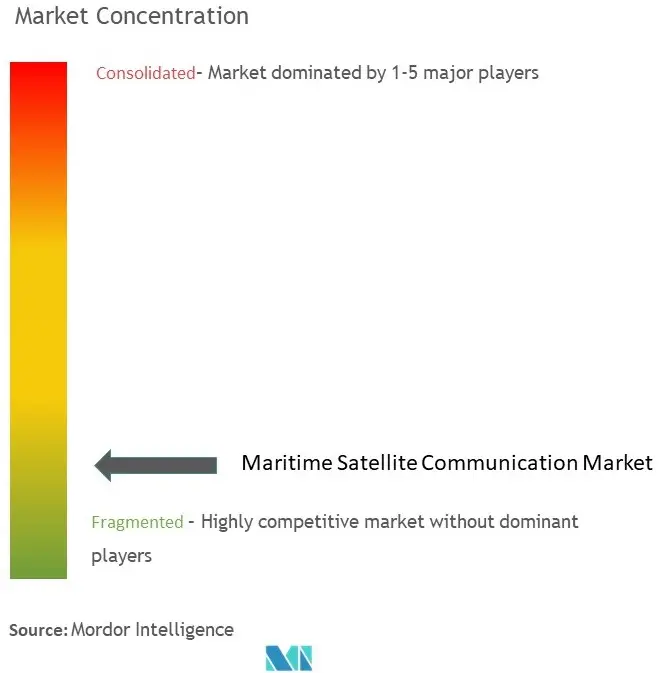

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Maritime Satellite Communication Market Analysis

The Maritime Satellite Communication Market size is estimated at USD 7.18 billion in 2025, and is expected to reach USD 12.10 billion by 2030, at a CAGR of 11% during the forecast period (2025-2030).

The maritime satellite communication industry is experiencing rapid digital transformation driven by increasing internet penetration and connectivity demands across global shipping routes. According to the Department of Telecommunications (India), total internet connections reached approximately 851 million in 2023, highlighting the exponential growth in connectivity requirements. The integration of VSAT terminals has revolutionized maritime communications by enabling comprehensive text, audio, and video data transmission capabilities across Ku, Ka, and C bands. This technological evolution has fundamentally altered how shipping companies manage their operations, from real-time cargo tracking to fleet management and crew communications.

The industry is witnessing significant technological advancement through the integration of cloud computing, IoT applications, and autonomous systems. In a notable development, Chinese authorities successfully deployed the world's first autonomous, electric container feeder ship for retail service in 2023, featuring advanced maritime satellite communication systems for remote operations. This 384-foot vessel, operating between Qingdao Port and Dongjiakou, represents a significant milestone in autonomous shipping technology adoption. The convergence of satellite communication maritime systems with autonomous systems is creating new possibilities for efficient fleet operations and reduced human intervention in routine maritime activities.

Infrastructure development and deployment continue to expand across various maritime regions, with service providers enhancing their network capabilities. The Russian Satellite Communications Company (RSCC) reported a significant milestone in 2022, with its VSAT marine network supporting 400 vessels, including 373 sea-going and river ships and 27 ice-class ships, of which 12 are icebreakers. This robust infrastructure development demonstrates the industry's commitment to providing comprehensive coverage across diverse maritime environments, from busy shipping lanes to remote Arctic routes.

Industry collaboration and service innovation are driving the evolution of maritime satellite communications through cloud-based solutions and integrated communication platforms. In March 2023, Tata Communications launched Jamvee, a cloud-based application offering integrated voice calling and messaging capabilities for enterprises, demonstrating the industry's move toward unified communication solutions. Service providers are increasingly focusing on developing flexible, scalable solutions that can accommodate varying bandwidth requirements and support diverse applications, from basic voice communications to advanced data analytics and remote monitoring systems.

Maritime Satellite Communication Market Trends

Increasing Need for Connectivity for Crew Welfare and Operations

The maritime industry's growing digitalization has made satellite connectivity for maritime essential for both crew welfare and operational efficiency. Modern vessels require constant connectivity to support various critical functions, including real-time weather monitoring, route optimization, equipment maintenance tracking, and emergency communications. The implementation of data-driven decision-making processes has become crucial for vessel operations, with ships increasingly relying on IoT sensors and automated systems that require reliable marine satellite communications infrastructure to transmit data between vessels and shore-based operations centers. This operational necessity is further evidenced by recent developments, such as ONGC's significant investment of INR 400 million to upgrade its in-house Ku-band satellite communication system, aimed at improving connectivity among offshore platforms, drilling rigs, vessels, and onshore locations.

The focus on crew welfare has become particularly prominent as shipping companies recognize the importance of providing reliable communication services to maintain crew morale and retention. This has led to significant investments in advanced maritime satellite communications systems that enable crew members to maintain contact with their families and access entertainment services while at sea. For instance, OneWeb's introduction of its "Try Before You Buy" maritime service in October 2023 demonstrates the industry's commitment to providing high-quality connectivity, offering speeds of over 100 Mbps through its network of 634 satellites. This development reflects the growing recognition that crew welfare is intrinsically linked to operational efficiency and safety, as well-connected crew members are better positioned to perform their duties effectively and maintain high safety standards.

Understand The Key Trends Shaping This Market

Download PDF

Launch of High-Throughput Satellite (HTS) Satellites

The deployment of High-Throughput Satellites (HTS) represents a significant technological advancement in maritime satellite communications, offering substantially increased data capacity and improved service quality. According to the Union of Concerned Scientists, as of April 2022, there were 5,465 active artificial satellites orbiting the Earth, with the United States leading with 3,433 satellites, followed by China with 541 satellites. This growing satellite infrastructure, particularly the deployment of HTS systems, is enabling maritime operators to access higher bandwidth and more reliable connectivity solutions, supporting the increasing data demands of modern vessel operations and crew communications.

The maritime industry is witnessing a transformation in satellite communication capabilities through the continuous launch of HTS satellites, which is evidenced by recent developments in the sector. For instance, the emergence of new maritime satellite communications providers and licensing activities, such as Nelco's application for the Global Mobile Personal Communication by Satellite (GMPCS) license in December 2022, alongside established players like SpaceX and OneWeb, indicates the industry's recognition of HTS technology's potential. These technological advancements are particularly crucial for supporting the growing maritime trade volume, as demonstrated by the significant container throughput at China's coastal ports, which reached approximately 22.3 million TEUs in May 2022. The enhanced capacity and coverage provided by HTS satellites are essential for maintaining efficient communication channels across busy shipping routes and supporting the digitalization of maritime operations.

Segment Analysis: By Type

VSAT Segment in Maritime Satellite Communication Market

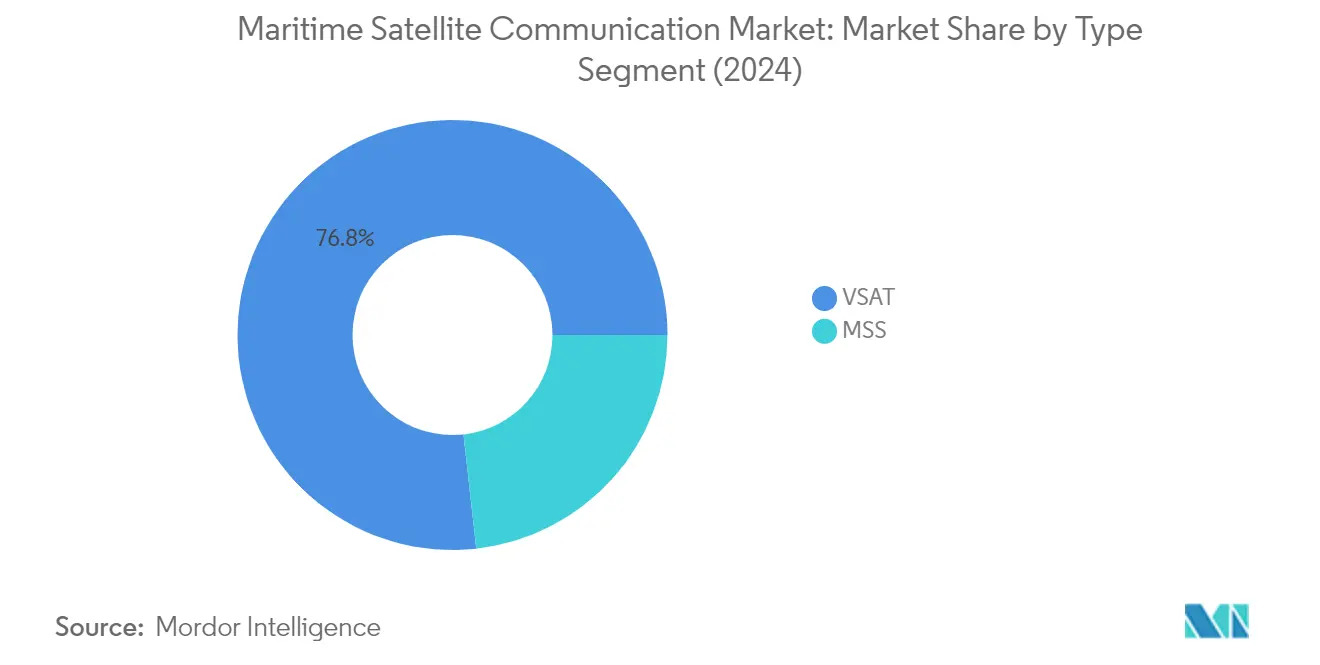

The Very Small Aperture Terminal (VSAT) segment dominates the maritime satellite communication market, holding approximately 77% market share in 2024, demonstrating its crucial role in maritime connectivity solutions. VSAT technology has witnessed significant adoption due to its ability to provide high-speed internet access, phone services, weather pattern monitoring, and business intelligence applications across various maritime operations. The technology enables vessel operators to effectively track fuel usage, vessel speeds, and implement preventative maintenance measures, resulting in improved repair times and real-time navigation capabilities. Maritime corporations increasingly rely on VSAT solutions for critical applications including route planning, ship-to-shore broadband data transfers, and fuel efficiency optimization. The segment's dominance is further strengthened by the comprehensive support offered by VSAT providers, including worldwide technical support for television receive-only (TVRO) antennas and various antenna systems from leading manufacturers like Intellian, KNS, Orbit, and Sea Tel.

MSS Segment in Maritime Satellite Communication Market

The Mobile Satellite Services (MSS) segment is projected to experience the fastest growth in the maritime satellite communications market between 2024 and 2029, with an expected growth rate of approximately 13%. This accelerated growth is driven by the increasing demand for reliable two-way audio and data communications for mobile customers worldwide, particularly in remote locations. MSS operates in the L-band frequency spectrum, which provides superior resistance to rain fade compared to fixed satellite systems in the Ku- and Ka-bands, making it particularly valuable for maritime applications. The segment's growth is further propelled by its versatility in terminal sizes, ranging from portable devices to laptop-sized units, and its ability to be installed in vehicles for continuous communication while in motion. The expansion of MSS capabilities through strategic partnerships and technological advancements continues to enhance its appeal to maritime customers seeking reliable and flexible communication solutions.

Segment Analysis: By Offering

Solution Segment in Maritime Satellite Communication Market

The Solution segment continues to dominate the maritime satellite communication market, holding approximately 67% market share in 2024, driven by the increasing adoption of integrated satellite communication solutions across various maritime applications. This segment encompasses comprehensive offerings including hardware components, network infrastructure, and integrated platforms that enable seamless connectivity at sea. The segment's strong position is reinforced by the growing demand for end-to-end maritime solutions that combine satellite connectivity with advanced features like cybersecurity, crew welfare applications, and fleet management capabilities. Major solution providers are focusing on developing more sophisticated offerings that incorporate AI-driven analytics, IoT integration, and enhanced bandwidth management capabilities to meet the evolving needs of maritime operators. The segment's growth is particularly notable in commercial shipping and offshore operations, where reliable communication infrastructure is crucial for operational efficiency and safety compliance.

Service Segment in Maritime Satellite Communication Market

The Service segment is emerging as the fastest-growing segment in the maritime satellite communication market, with an expected growth rate of approximately 12% during 2024-2029. This accelerated growth is primarily driven by the increasing demand for managed services, maintenance support, and value-added services in the maritime sector. Service providers are expanding their portfolios to include comprehensive support packages, network optimization services, and customized connectivity solutions tailored to specific maritime applications. The segment is witnessing significant innovation in areas such as predictive maintenance services, remote troubleshooting capabilities, and enhanced customer support frameworks. The growth is further fueled by the rising adoption of subscription-based service models, which offer flexibility and scalability to maritime operators while reducing their upfront investment requirements. Maritime organizations are increasingly recognizing the value of professional services in maintaining optimal network performance and ensuring seamless communication capabilities across their fleets.

Segment Analysis: By End-User

Merchants Segment in Maritime Satellite Communication Market

The merchants segment, which includes cargo, tanker, container, and bulk carrier vessels, holds the dominant position in the maritime satellite communication market, commanding approximately 28% market share in 2024. This segment's leadership is driven by the increasing digitalization of merchant vessels, with shipping companies implementing advanced satellite communication in ships for route planning, real-time navigation, and fuel efficiency monitoring. The segment is also experiencing the fastest growth trajectory, projected to grow at nearly 12% during 2024-2029, primarily due to the rising adoption of VSAT connectivity for crew welfare, operational efficiency, and regulatory compliance. The growth is further supported by the increasing global trade volumes and the maritime industry's focus on implementing IoT solutions and digital technologies for better fleet management and operational optimization.

Remaining Segments in Maritime Satellite Communication Market End-User Segmentation

The maritime satellite communication market encompasses several other significant segments including passenger fleet (cruise and ferry), offshore rigs and support vessels, leisure (yachts), and fishing vessels. The passenger fleet segment maintains substantial market presence due to the growing demand for high-speed internet connectivity for both operational requirements and passenger entertainment services. The offshore rigs and support vessels segment demonstrates strong adoption of satellite communication solutions for maintaining operational efficiency and crew safety in remote locations. The leisure segment, particularly the superyacht sector, continues to drive innovation in maritime connectivity solutions with demands for premium communication services. The fishing vessels segment contributes to market growth through the increasing adoption of ship satellite communications for navigation, weather monitoring, and regulatory compliance in commercial fishing operations.

Maritime Satellite Communication Market Geography Segment Analysis

Maritime Satellite Communication Market in North America

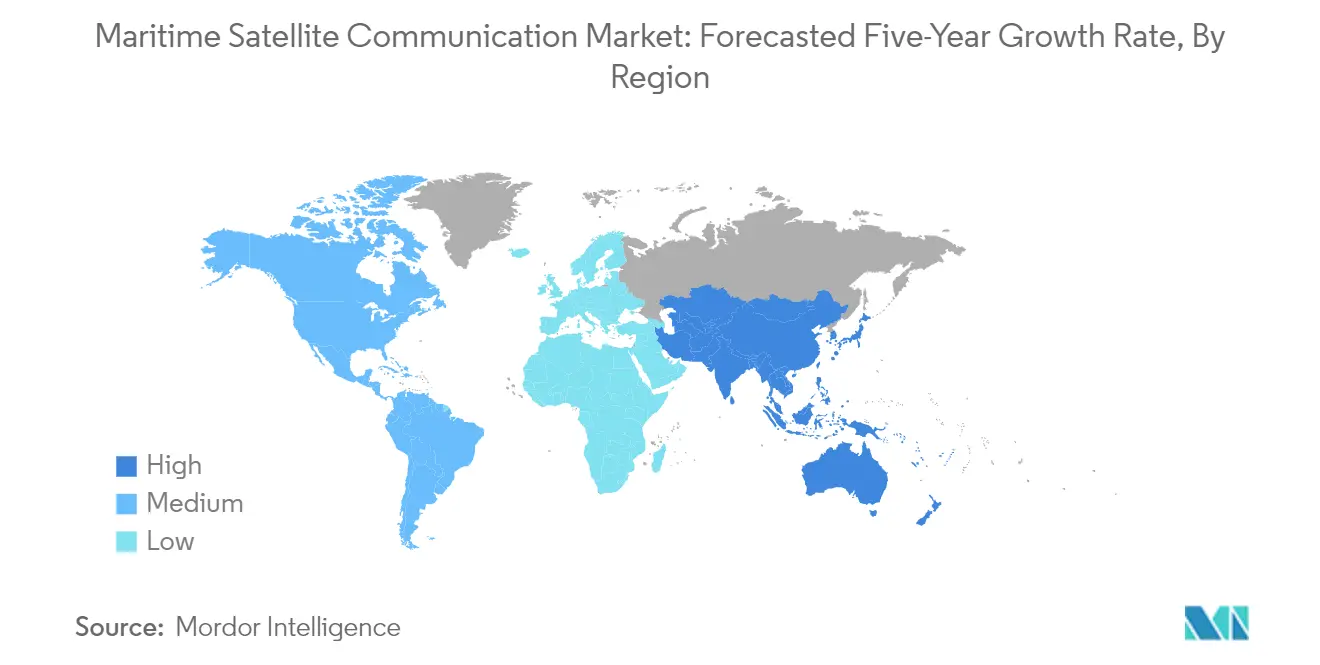

North America continues to dominate the global maritime satellite communication market, holding approximately 32% of the market share in 2024. The region's leadership position is driven by substantial government investments in maritime infrastructure modernization and the widespread adoption of advanced maritime satellite communication technologies across various maritime sectors. The Bipartisan Infrastructure Law has been instrumental in transforming port infrastructure and waterways, focusing on reducing emissions through electrification and implementing low-carbon technologies. The region's strong emphasis on vessel automation, cargo tracking systems, and global navigation has created a robust ecosystem for maritime satellite communications. The presence of major satellite communication providers and their continuous innovation in VSAT and other advanced communication solutions has further strengthened the market. Additionally, the increasing focus on crew welfare, cybersecurity, and operational efficiency has led to higher adoption rates of high-throughput maritime satellite services across commercial and military maritime operations.

Maritime Satellite Communication Market in Europe

Europe has established itself as a crucial hub for the maritime satellite communication market, demonstrating a robust growth rate of approximately 11% during the period 2019-2024. The region's market is characterized by its strong focus on technological innovation and a regulatory framework supporting maritime digitalization. The European Union's commitment to reducing reliance on foreign firms and protecting crucial communications services has led to significant investments in satellite communication infrastructure. The region's extensive coastline and busy shipping routes have necessitated advanced maritime communication services for vessel tracking, crew welfare, and operational efficiency. European maritime operators have shown particular interest in hybrid network solutions that combine multiple communication technologies for enhanced reliability. The presence of major ports, shipping companies, and maritime technology providers has created a sophisticated ecosystem that continues to drive innovation in maritime satellite communications. The region's emphasis on environmental sustainability has also led to increased adoption of smart shipping solutions requiring robust satellite connectivity.

Maritime Satellite Communication Market in Asia-Pacific

The Asia-Pacific maritime satellite communication market is positioned for exceptional growth, with a projected CAGR of approximately 12% during the period 2024-2029. The region's dynamic maritime sector is undergoing rapid digital transformation, particularly in countries like China, Japan, India, and Singapore. The increasing focus on modernizing port infrastructure and implementing smart port solutions has created substantial opportunities for satellite communication providers. The region's vast maritime trade routes and expanding commercial fleet operations have necessitated advanced communication solutions for enhanced operational efficiency and safety. The growing emphasis on crew welfare and connectivity requirements has led to increased adoption of high-throughput satellite services. Additionally, the rise in offshore energy exploration activities and the expansion of fishing fleets have created new demand vectors for maritime satcom. The region's commitment to maritime digitalization, combined with increasing investments in satellite infrastructure, positions it as a key growth driver in the global market.

Maritime Satellite Communication Market in Rest of the World

The Rest of the World region, encompassing Latin America and the Middle East & Africa, represents an emerging market with significant growth potential in marine satcom. These regions have embraced maritime satellite technology to integrate advanced communication networks, particularly for staff working in isolated offshore locations. The increasing focus on digitalization in the maritime sector, especially in oil-rich Gulf countries, has driven the adoption of satellite communication solutions. The region has witnessed growing investments in port modernization and maritime infrastructure development, creating new opportunities for satellite communication providers. The expansion of commercial shipping routes and offshore energy exploration activities has further accelerated the demand for reliable maritime communication solutions. Local partnerships and collaborations between international satellite operators and regional service providers have helped enhance the accessibility and reliability of maritime satellite services in these regions. The growing emphasis on maritime security and operational efficiency continues to drive the adoption of advanced satellite communication solutions across various maritime sectors.

Get Analysis on Important Geographic Markets

Download PDF

Maritime Satellite Communication Industry Overview

Top Companies in Maritime Satellite Communication Market

The maritime satellite communication market features prominent players like Inmarsat, Marlink SAS, KVH Industries, Speedcast International, and Viasat leading the industry through continuous innovation and strategic expansion. These companies are actively investing in next-generation satellite technologies, particularly focusing on high-throughput satellites and hybrid network solutions combining multiple frequency bands, including Ka, Ku, and L-band capabilities. The industry witnesses regular product launches centered around enhanced connectivity solutions, cybersecurity features, and crew welfare applications. Market leaders are increasingly adopting subscription-based business models and forming strategic partnerships to expand their service portfolios. Companies are also prioritizing the development of integrated solutions that combine hardware, software, and value-added services to create comprehensive maritime communication ecosystems.

Dynamic Market Structure Drives Industry Evolution

The maritime satellite communication market exhibits a moderately consolidated structure with global conglomerates maintaining significant market presence through their established infrastructure and technological capabilities. These dominant players leverage their extensive satellite networks, ground infrastructure, and long-standing relationships with maritime customers to maintain their competitive positions. The market has witnessed several strategic acquisitions and mergers, such as the notable Viasat-Inmarsat merger, indicating a trend toward consolidation as companies seek to combine technological expertise and expand their geographical footprint.

The competitive landscape is characterized by a mix of integrated solution providers and specialized service operators, with regional players maintaining strong positions in specific geographical markets or specialized maritime segments. Market participants are increasingly focusing on vertical integration strategies, either through internal development or strategic partnerships, to control key aspects of the value chain from satellite operations to end-user services. The industry also sees regular collaboration between satellite operators and service providers to enhance coverage and service quality while optimizing resource utilization.

Innovation and Adaptability Drive Future Success

Success in the maritime satellite communication market increasingly depends on providers' ability to deliver flexible, scalable solutions that address evolving customer needs while maintaining cost-effectiveness. Companies must focus on developing robust cybersecurity capabilities, implementing advanced network management systems, and offering seamless integration with emerging maritime technologies. The ability to provide reliable connectivity across diverse maritime environments, from coastal waters to remote ocean regions, while maintaining service quality and managing bandwidth efficiently, has become crucial for market success.

Market participants need to consider the growing influence of end-user preferences, particularly regarding digital transformation initiatives in the maritime industry. Companies must navigate potential regulatory changes related to maritime safety, environmental protection, and spectrum allocation while maintaining competitive pricing structures. Success factors also include the ability to develop strong distribution networks, maintain effective customer support infrastructure, and create value-added services that differentiate offerings in an increasingly competitive market. The development of strategic partnerships with technology providers, system integrators, and maritime solution specialists will continue to play a crucial role in maintaining market position and driving growth. Providers of maritime satellite communications are at the forefront of these developments, ensuring that services for maritime satellite meet the high standards required by the industry.

Maritime Satellite Communication Market Leaders

-

Inmarsat Group Limited

-

Marlink SAS (Providence Equity Partners)

-

KVH Industries Inc.

-

Speedcast

-

NSSL Global Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Maritime Satellite Communication Market News

- May 2024: Inmarsat Maritime, a Viasat company, introduced NexusWave, a comprehensive connectivity service. NexusWave utilizes a 'bonded' multi-dimensional network to provide high-speed connectivity, unlimited data, global coverage, and a robust 'secure by design' infrastructure. As a fully managed service from a single provider, NexusWave integrates multiple high-speed networks in real time. These include Global Xpress (GX) Ka-band, low-Earth orbit (LEO) services, and coastal LTE, with an additional L-band layer for enhanced resiliency. This combination ensures fast, always-on connectivity. NexusWave features an enterprise-grade firewall, a security measure trusted by global enterprises and governments.

- April 2023: A collaborative effort between the Satellite Technology and Research Center (STAR) at the National University of Singapore's College of Design and Engineering (NUS CDE) and A*STAR's I2R has resulted in the successful launch of an advanced microsatellite for maritime communications from the Satish Dhawan Space Center in Sriharikotta, India.

Maritime Satellite Communications Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot (Ka, Ku, and C Bands, Size of Terminals, Application Notes, and Penetration)

- 4.4 Impact of Macroeconomic Trends on Maritime VSAT and Allied Markets

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Need for Connectivity for Crew Welfare and Operations

- 5.1.2 Launch of High-Throughput Satellite (HTS) Satellites

-

5.2 Market Restraints

- 5.2.1 Lack of Awareness About the Advanced Satellite Service Market

- 5.2.2 Reliance on High-cost Satellite Equipment

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Mobile Satellite Communication or Mobile Satellite Services (MSS)

- 6.1.2 Very Small Aperture Terminal (VSAT)

-

6.2 By Offering

- 6.2.1 Solution

- 6.2.2 Service

-

6.3 By End-User Vertical

- 6.3.1 Merchant (Cargo, Tanker, Container, Bulk Carrier, etc.)

- 6.3.2 Offshore Rigs and Support Vessels

- 6.3.3 Passenger Fleet (Cruise and Ferry)

- 6.3.4 Leisure (Yachts)

- 6.3.5 Finishing Vessels

-

6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Inmarsat Group Limited

- 7.1.2 Marlink SAS (Providence Equity Partners)

- 7.1.3 KVH Industries Inc.

- 7.1.4 Speedcast International

- 7.1.5 NSSL Global Limited

- 7.1.6 Cobham Satcom

- 7.1.7 Iridium Communications Inc.

- 7.1.8 Thuraya Telecommunications Company

- 7.1.9 Hughes Network Systems LLC

- 7.1.10 Viasat Inc.

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Maritime Satellite Communication Industry Segmentation

Marine communication involves ship-to-ship and ship-to-shore communication. Over the years, how seamen communicate has changed drastically. Previously, semaphores and flags were a primary form of communication for ships out at sea. Maritime satellite communication comprises a range of communication service offerings delivered mainly through Ku-band, L-band, and Ka-band frequency-based satellite communication services, which help communication worldwide.

The market is segmented by types, such as mobile satellite communication or mobile satellite services (MSS) and very small aperture terminal (VSAT), among solution and service offerings. The study also comprises various end-user verticals such as merchant, (cargo, tanker, container, bulk carrier), offshore rigs and support vessels, passenger fleet (cruise and ferry), leisure (yachts), and finishing vessels in multiple geographies such as North America, Europe, Asia-Pacific, and Rest Of The World. The impact of macroeconomic trends on the market is also covered under the scope of the study. The disturbance of the factors affecting the market's evolution in the near future are also covered as drivers and constraints. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | Mobile Satellite Communication or Mobile Satellite Services (MSS) |

| Very Small Aperture Terminal (VSAT) | |

| By Offering | Solution |

| Service | |

| By End-User Vertical | Merchant (Cargo, Tanker, Container, Bulk Carrier, etc.) |

| Offshore Rigs and Support Vessels | |

| Passenger Fleet (Cruise and Ferry) | |

| Leisure (Yachts) | |

| Finishing Vessels | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

Maritime Satellite Communications Market Research FAQs

How big is the Maritime Satellite Communication Market?

The Maritime Satellite Communication Market size is expected to reach USD 7.18 billion in 2025 and grow at a CAGR of 11% to reach USD 12.10 billion by 2030.

What is the current Maritime Satellite Communication Market size?

In 2025, the Maritime Satellite Communication Market size is expected to reach USD 7.18 billion.

Who are the key players in Maritime Satellite Communication Market?

Inmarsat Group Limited, Marlink SAS (Providence Equity Partners), KVH Industries Inc., Speedcast and NSSL Global Limited are the major companies operating in the Maritime Satellite Communication Market.

Which is the fastest growing region in Maritime Satellite Communication Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Maritime Satellite Communication Market?

In 2025, the North America accounts for the largest market share in Maritime Satellite Communication Market.

What years does this Maritime Satellite Communication Market cover, and what was the market size in 2024?

In 2024, the Maritime Satellite Communication Market size was estimated at USD 6.39 billion. The report covers the Maritime Satellite Communication Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Maritime Satellite Communication Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Maritime Satellite Communication Market Research

Mordor Intelligence offers extensive expertise in analyzing the maritime satellite communications industry. We provide comprehensive insights into maritime connectivity via satellite and the maritime telecommunications sectors. Our research thoroughly examines maritime satellite communication systems and their implementation across global maritime operations. This includes insights into satellite communications for offshore connectivity and marine communication systems. The report delivers a detailed analysis of maritime satellite services and maritime communication services. It also covers optimized communication services for maritime sectors, all available in an easy-to-download report PDF format.

Our industry analysis benefits stakeholders by delivering crucial insights into maritime satellite internet trends and maritime VSAT systems. It also explores emerging maritime communications network technologies. The report covers vital aspects of satellite communication in ships and maritime connectivity solutions. Additionally, it examines the evolution of marine satellite communication technologies. Stakeholders gain access to comprehensive data on maritime MSS developments and maritime satellite communications providers. Furthermore, it includes advanced maritime telecom solutions, enabling informed decision-making in this rapidly evolving sector.