Marine Anti-fouling Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 2.60 Billion |

| Growth Rate (2026 - 2032) | 4.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Anti-fouling Coatings Market Analysis by Mordor Intelligence

The Marine Anti-fouling Coatings Market size is estimated at USD 2.13 billion in 2026, and is expected to reach USD 2.60 billion by 2031, at a CAGR of 4.08% during the forecast period (2026-2031). The headline expansion reflects strong demand from newbuild ship deliveries in Asia-Pacific, rising repair work on a 22.4-year-old merchant fleet, and premium pricing for nano-hybrid chemistries that cut fuel burn by keeping hulls smoother for longer periods. Red Sea reroutings in 2024–2025 raised average ton-miles and exposed vessels to warmer biomes, shortening effective coating life and lifting replacement volumes despite only modest growth in seaborne trade. Copper-based self-polishing copolymers still anchor the marine antifouling coatings market because shipowners trust their efficacy, yet regulatory caps on copper leaching and volatile cuprous-oxide prices are accelerating migration toward foul-release silicones, graphene hybrids, and self-healing systems. Competitive intensity has risen as incumbents forward-integrate into resin synthesis to secure feedstocks, while niche formulators chase offshore wind foundations and aquaculture nets where non-toxic solutions command premiums.

Key Report Takeaways

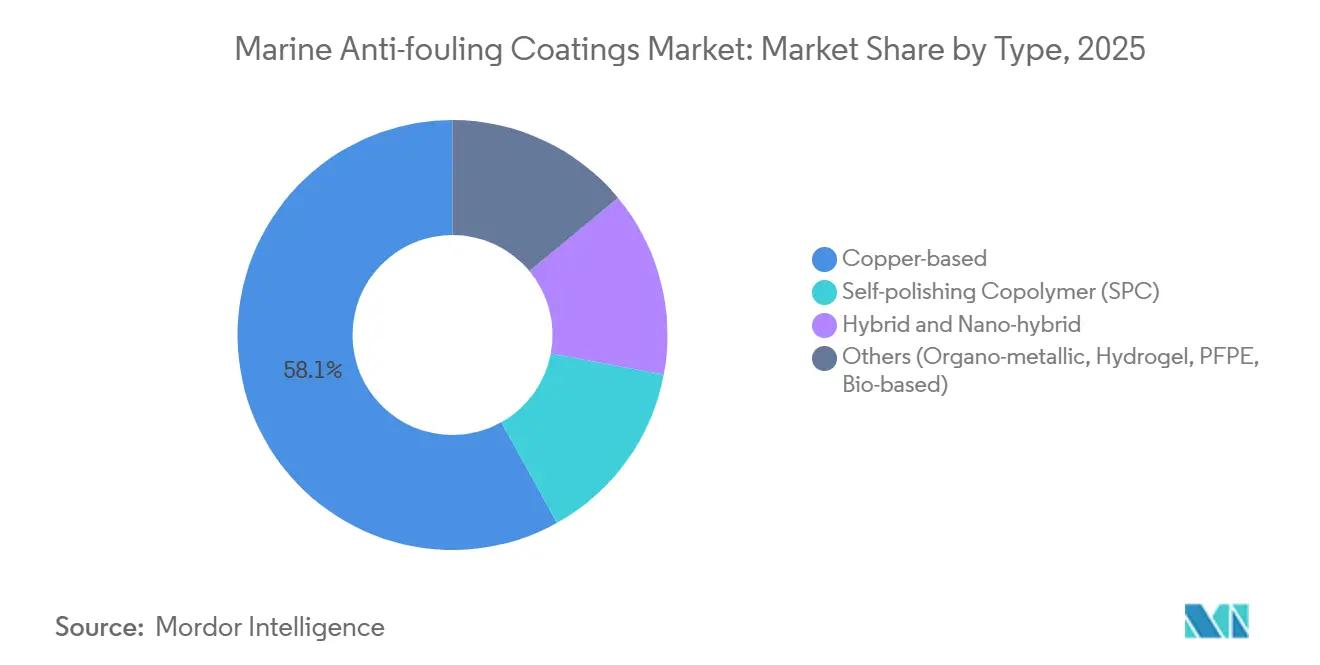

- By type, copper-based led with 58.08% of marine antifouling coatings market share in 2025, while hybrid and nano-hybrid variants posted the fastest 4.76% CAGR through 2031.

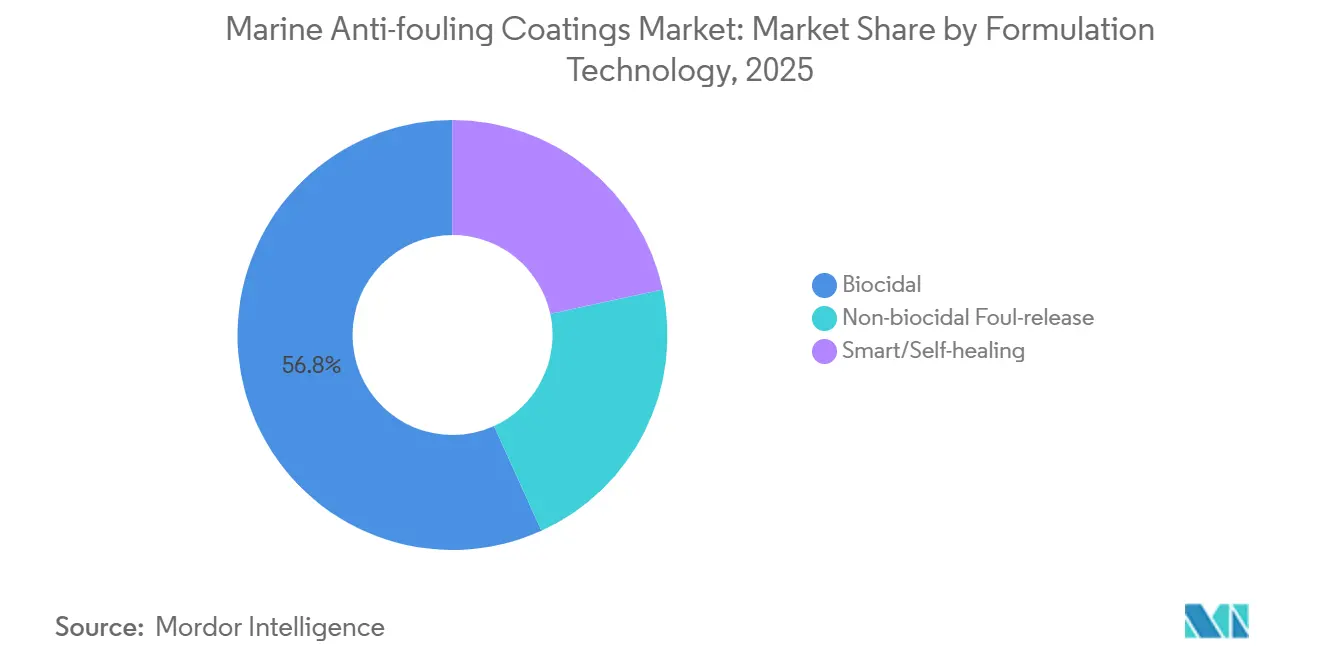

- By formulation technology, biocidal accounted for 56.78% share of the marine antifouling coatings market size in 2025; smart and self-healing coatings register the highest forecast CAGR at 5.02% to 2031.

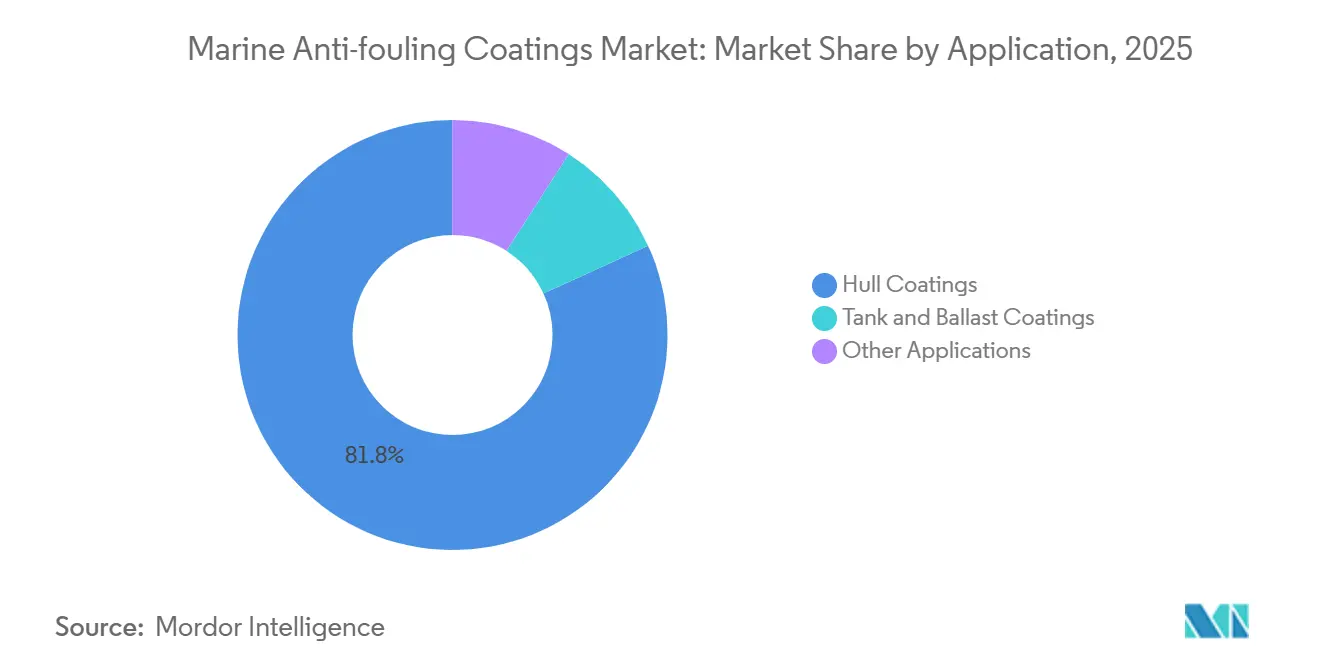

- By application, hull coatings captured 81.82% of the marine antifouling coatings market size in 2025 and are advancing at a 4.91% CAGR to 2031.

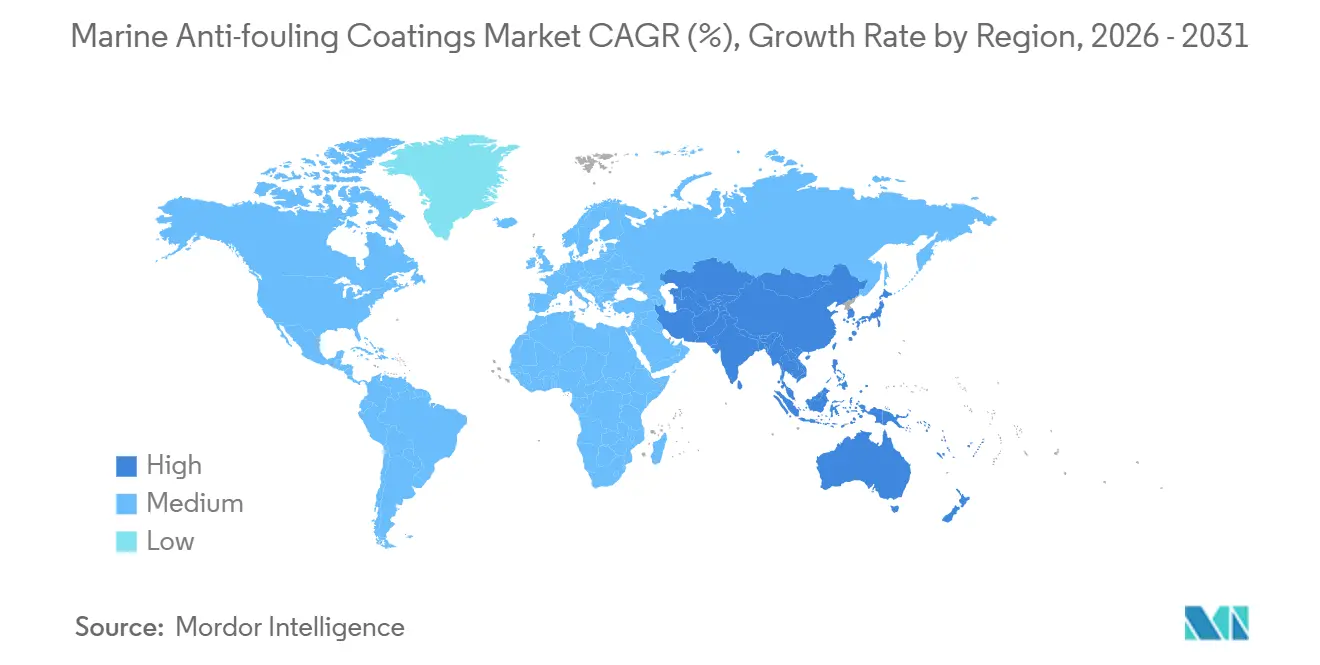

- By geography, Asia-Pacific commanded 68.90% revenue in 2025 and is projected to expand at a 4.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine Anti-fouling Coatings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth in Global Seaborne Trade | +1.2% | Global, with concentration in Asia-Pacific and Middle East trade lanes | Medium term (2-4 years) |

| Increasing Ship Repairs and Maintenance Activities | +0.9% | Global, particularly North America and Europe due to aging fleets | Long term (≥ 4 years) |

| Expansion of Asian Shipbuilding Capacity | +1.1% | Asia-Pacific core (China, South Korea, Japan), spill-over to Southeast Asia | Medium term (2-4 years) |

| Increasing Production of Leisure Boats and Cruise Ships | +0.4% | North America and Europe, emerging demand in Middle East | Short term (≤ 2 years) |

| Military Sonar-Friendly Stealth Coatings Demand | +0.3% | North America, Europe, Asia-Pacific (naval modernization programs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Global Seaborne Trade

Container reroutings around the Cape of Good Hope in 2025 lengthened Asia–Europe voyages by 3,500 nautical miles and lifted ton-miles 6% even though cargo volumes grew only 0.5%. Longer exposure to warmer waters accelerates barnacle settlement, cutting the service life of self-polishing copolymers from 60 months to 48 months and prompting unscheduled dry-dockings. Operators responded with a two-tier coating strategy that loads copper heavily for the first 18 months then overlays foul-release topcoats, lifting spend per hull 15%–20% but avoiding the 40% fuel penalty of severe fouling. The shift toward 24,000 TEU ultra-large container ships expands coated surface faster than cargo capacity, sustaining volume growth in the marine antifouling coatings market[1]United Nations Conference on Trade and Development, “Container Shipping Outlook 2025,” unctad.org. Diversifying trade lanes, notably intra-Asian routes, is distributing repair demand to hubs in Singapore, Dubai, and Santos, increasing just-in-time blending opportunities for suppliers.

Increasing Ship Repairs and Maintenance Activities

Average fleet age reached 22.4 years in 2024, the highest in two decades, after owners deferred scrapping amid high newbuild prices. Older hulls suffer micro-crack formation that forces touch-ups at 30–36 months, effectively doubling addressable demand for repair-grade coatings. Chinese and Southeast Asian yards captured 60% of global repair work in 2024-2025, enabling formulators to pre-position inventory and offer copper-content adjustments matched to future trading regions. Higher-sulfur fuels burned in legacy engines accelerate corrosion in ballast tanks, extending antifouling needs beyond exterior hulls. These dynamics support sustained replacement cycles that underpin the marine antifouling coatings market even as newbuild deliveries climb.

Expansion of Asian Shipbuilding Capacity

China delivered 54.6% of global tonnage in 2024 and South Korea’s USD 120 billion orderbook stretches to 2035, underpinning regional dominance. Newbuild contracts bundle coatings, and yards sign multi-year supply pacts with two or three majors to secure pricing and technical service. Eco-design vessels meeting IMO Energy Efficiency Design Index Phase 3 favor nano-hybrid coatings that reduce hull roughness 5% and fuel use 3%–4%, justifying premiums of 25%–30%. Emerging yards in Vietnam and Indonesia focus on mid-size vessels where delivery speed matters, opening share for regional formulators. Collectively, Asian capacity keeps the marine antifouling coatings market anchored in Asia-Pacific for the next decade.

Increasing Production of Leisure Boats and Cruise Ships

U.S. and European leisure-boat output accounted for 70% of global units in 2025, powered by coastal tourism and private ownership. Cruise-ship orderbooks climbed to 60 vessels with deliveries clustered in 2026-2027, each specifying coatings that combine aesthetics with fouling resistance. Marinas in California and the Mediterranean cap copper runoff, steering leisure craft toward silicone foul-release systems despite shorter maintenance intervals. Sonar-transparent coatings for naval sonar domes line up with frigate and corvette procurements, growing this niche at 8%-10% per year. Though smaller in volume, the leisure and defense segments raise average selling prices across the marine antifouling coatings market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Biocide Bans | -0.6% | Europe, North America, with gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Volatility in Cuprous-Oxide Pricing | -0.4% | Global, with acute impact in Asia-Pacific due to supply-chain concentration | Short term (≤ 2 years) |

| Accelerated Uptake of Non-Coating Hull-Clean Robots | -0.3% | Europe and North America initially, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Biocide Bans

The AFS Convention now ratified by 95 states restricts copper release, while the EU cut leaching limits from 200 μg cm² day⁻¹ to 150 μg in 2024, forcing reformulation or exit for high-copper paints. California imposes even tighter caps, effectively banning high-loading coatings in leisure harbors. Non-biocidal foul-release alternatives cost 40%-60% more and add two or three days to dry-dock schedules, squeezing budgets[2]European Chemicals Agency, “Copper Active Substance Renewal 2024,” echa.europa.eu . Owners operating globally must specify to the strictest rules or manage regional inventories, both raising complexity. The regulatory trajectory accelerates hybrid layering where a thin biocidal primer sits under a silicone topcoat, but multi-year sea trials slow mass adoption.

Volatility in Cuprous-Oxide Pricing

Cuprous-oxide prices swung 30% between Q1 2024 and Q3 2025 after Chilean mine disruptions and Indonesian smelter delays. Majors hedge half their needs but still adjust list prices quarterly, while smaller firms saw margins shrink 200-300 basis points in 2025, prompting consolidation. High copper costs push buyers toward bio-based alternatives, yet current bio-polymer yields remain far from commercial scale.

Segment Analysis

By Type: Copper Endures as Hybrids Gain

Copper-based held 58.08% of marine antifouling coatings market share in 2025 and still dominate newbuild specifications because their USD 8–12 per liter cost undercuts nano-hybrids and provides proven five-year protection. Hybrid and nano-hybrid coatings are posting 4.76% CAGR to 2031 as yards seek to defer first recoating by two or three years and regulators ratchet down copper leaching. The marine antifouling coatings market size for hybrids is therefore expanding faster than for legacy copper products, supported by graphene or silica nanoparticles that cut friction 20%–30% and trim fuel bills.

Advanced chemistries—zwitterionic, hydrogel, PFPE, and bio-based matrices—occupy small yet strategic niches such as polar research vessels and offshore wind monopiles where zero toxicity is paramount. PFPE faces potential PFAS restrictions from 2028, while bio-based paints cost 50%-70% more and last 24-36 months, limiting near-term uptake. Nonetheless, patent filings for these alternatives grew 40% in 2024-2025, signaling R&D commitment among leading suppliers.

By Formulation Technology: Biocidal Incumbency Versus Smart Innovation

Biocidal paints held 56.78% of marine antifouling coatings market share in 2025, anchored by cost advantages and owner familiarity. Non-biocidal foul-release systems are growing in regions that limit copper or on vessels sailing above 15 knots where hydrodynamic flow shears off organisms, yet application demands pristine surfaces, restricting use to newbuilds and full blast refits.

Smart and self-healing expand at 5.02% CAGR on the back of embedded microcapsules that release healing agents upon damage, extending life to 72 months and cutting unscheduled dry-dockings 30% in 2025 trials. Digital twins from Wärtsilä now integrate sensor readings with coating performance data, letting owners schedule maintenance only when drag rises beyond thresholds, a service that boosts value realization across the marine antifouling coatings market.

By Application: Hull Dominance Reflects Fouling Risk

Hull coatings represented 81.82% of marine antifouling coatings market size in 2025 and are forecast to grow at 4.91% CAGR to 2031 owing to drag penalties that can lift fuel burn 15% over a five-year cycle. Owners are shifting to thinner 200-250 micron layers every 36 months rather than heavier films every 60 months, reinforcing annual volume demand even as service intervals tighten.

Tank and ballast coatings trail because owners defer interior work until 15-year special surveys, favoring epoxy anticorrosives over antifouling unless vessels trade in brackish waters. Offshore wind foundations and aquaculture nets form the fastest sub-segment, leveraging nano-hybrids that extend inspection cycles from three to five years and comply with discharge caps in fjords and coastal zones.

Geography Analysis

Asia-Pacific controlled 68.90% of marine antifouling coatings market share in 2025 and will post a 4.66% CAGR to 2031, anchored by Chinese and South Korean yard activity and by repair hubs in Singapore, Busan, and Shanghai. South Korea’s LNG-carrier backlog and Japan’s specialty builds demand premium nano-hybrid coatings that meet Energy Efficiency Design Index targets. India’s USD 3 billion incentive program to boost shipbuilding will add incremental volumes from 2028.

North America shows bifurcated trends: copper-free rules in California push leisure boats toward silicone foul-release, while deep-sea vessels still employ biocidal SPCs. The U.S. Navy’s stealth coatings create a high-value but classified niche. Europe enforces the world’s strictest copper limits in the Baltic and Mediterranean, spurring demand for hybrid layering and robotic hull-clean systems that extend coating life.

South America and the Middle East and Africa grow from offshore oil and gas, container-port expansion, and intra-regional shipping. Brazil’s pre-salt FPSOs use dual-function coatings that withstand hydrocarbon and fouling exposure at 50%-70% premiums. Dry-dock hubs in Dubai and Fujairah attract global repair work on cost and turnaround advantages, while nascent African shipyards blend imported raw materials locally for river barges and fishing fleets.

Competitive Landscape

The marine antifouling coatings market is moderately concentrated. The top five suppliers—Akzo Nobel, Hempel, Jotun, PPG Industries, and Chugoku Marine Paints—command 50%-55% of global revenue, leaving room for regional challengers. Majors co-develop copper compounds with miners, operate hull-monitoring platforms, and navigate 50-plus regulatory regimes, erecting barriers for new entrants. Patent filings for graphene, zwitterionic, and bio-inspired matrices rose 40% during 2024-2025, underscoring a race to commercialize non-toxic alternatives before the next IMO biocide review in 2028.

Regional specialists target inland vessels, aquaculture nets, and leisure boats where customization trumps scale. Digital-twin alliances—Jotun’s HullSkater with Wärtsilä’s Fleet Operations Solution—offer predictive cleaning that extends coating life 20%-30% and justifies higher selling prices. Consolidation is expected as copper price volatility and multimillion-dollar regulatory testing favor vertically integrated players with global distribution.

Marine Anti-fouling Coatings Industry Leaders

PPG Industries Inc.

Hempel A/S

Akzo Nobel N.V.

Jotun A/S

Chugoku Marine Paints, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The Swedish biotechnology company I-Tech AB signed a Memorandum of Understanding (MoU) with Guangdong Havey Advanced Materials Technology Co., Ltd. (Havey) to collaborate on the development of next-generation high-performance antifouling materials for marine coatings. The partnership aimed to combine I-Tech’s Selektope bio-repellent ingredient with Havey’s advanced biodegradable resin binders.

- March 2024: PPG Industries Inc. launched the PPG NEXEON 810, a copper-free antifouling marine coating. It was designed to enhance ship performance, reduce emissions, and support sustainability initiatives.

Global Marine Anti-fouling Coatings Market Report Scope

Antifouling coatings are a type of coating that is put on the outer (outboard) layer of a ship or boat's hull to stop the growth of subaquatic organisms that stick to the hull and can hurt the performance and durability of the vessel and make it harder to move. It also acts as a barrier against corrosion on metal hulls that may degrade and weaken the metal or improve the flow of water past the hull of a fishing vessel.

The marine antifouling coatings market is segmented by type, formulation technology, application and geography. By type, the market is segmented into copper-based, self-polishing copolymer, hybrid and nano-hybrid, and others (organo-metallic, hydrogel, PFPE, bio-based). By formulation technology, the market is segmented into biocidal, non-biocidal foul-release, and smart/self-healing. By application, the market is segmented into hull coatings, tank and ballast coatings, and other applications (offshore structures, aquaculture, and inland waterways assets). The report also covers the market size and forecasts for marine antifouling coatings in 23 countries across major regions. For each segment, market sizing and forecasts were made on the basis of value (USD).

| Copper-based |

| Self-polishing Copolymer (SPC) |

| Hybrid and Nano-hybrid |

| Others (Organo-metallic, Hydrogel, PFPE, Bio-based) |

| Biocidal |

| Non-biocidal Foul-release |

| Smart/Self-healing |

| Hull Coatings |

| Tank and Ballast Coatings |

| Other Applications (Offshore Structures, Aquaculture and Inland Waterways Assets) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| Vietnam | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Qatar | |

| Nigeria | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Copper-based | |

| Self-polishing Copolymer (SPC) | ||

| Hybrid and Nano-hybrid | ||

| Others (Organo-metallic, Hydrogel, PFPE, Bio-based) | ||

| By Formulation Technology | Biocidal | |

| Non-biocidal Foul-release | ||

| Smart/Self-healing | ||

| By Application | Hull Coatings | |

| Tank and Ballast Coatings | ||

| Other Applications (Offshore Structures, Aquaculture and Inland Waterways Assets) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| Vietnam | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Qatar | ||

| Nigeria | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the marine antifouling coatings market?

The marine antifouling coatings market size stands at USD 2.13 billion in 2026 and is projected to advance at a 4.08% CAGR, lifting value to USD 2.60 billion by 2031.

Which region leads demand for antifouling coatings?

Asia-Pacific accounts for 68.90% of 2025 revenue and will remain the largest consumer through 2031.

Which product type holds the highest market share?

Copper-based formulations retain the largest share at 58.08% of 2025 revenue.

What technology is growing the quickest?

Smart and self-healing coatings exhibit the fastest forecast CAGR of 5.02% as owners adopt digital-twin maintenance strategies.