Managed IT Infrastructure Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

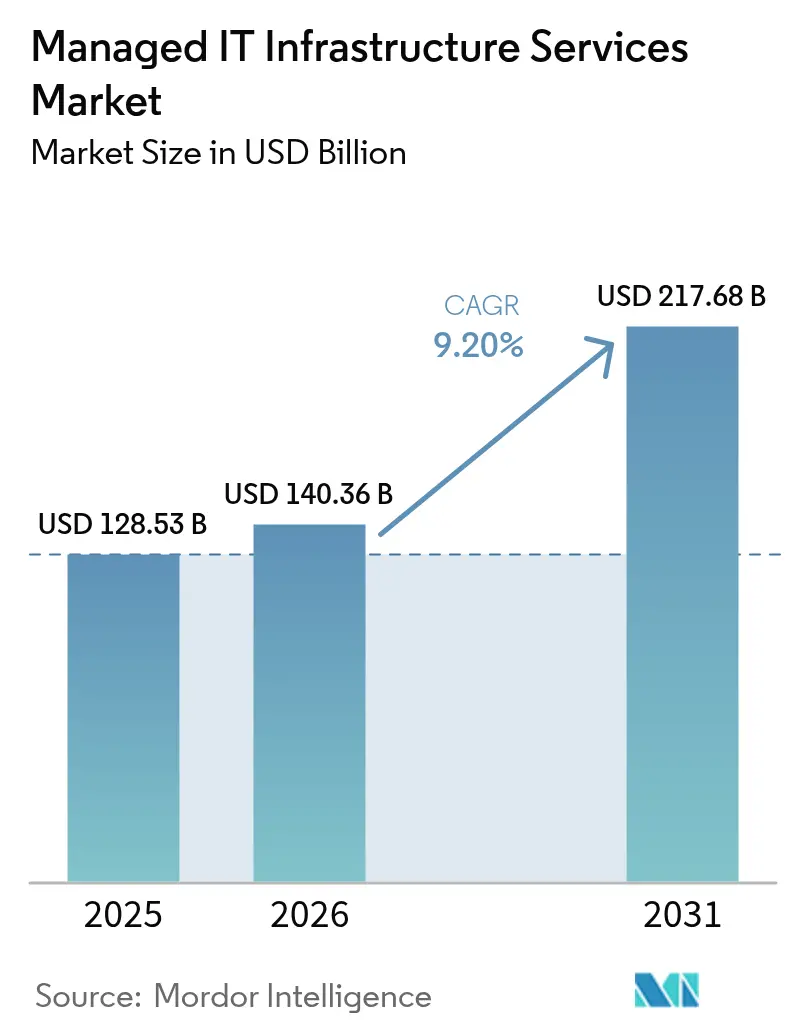

| Market Size (2026) | USD 140.36 Billion |

| Market Size (2031) | USD 217.68 Billion |

| Growth Rate (2026 - 2031) | 9.20% CAGR |

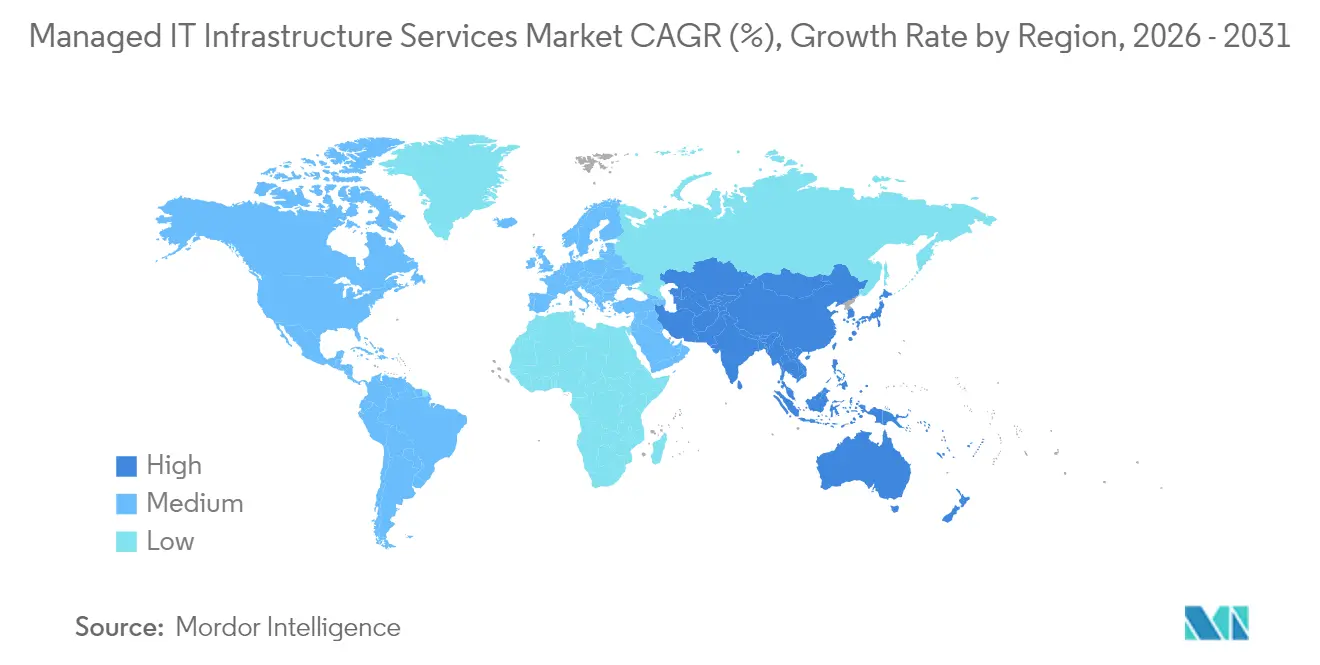

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed IT Infrastructure Services Market Analysis by Mordor Intelligence

The managed IT infrastructure services market size was valued at USD 128.53 billion in 2025 and estimated to grow from USD 140.36 billion in 2026 to reach USD 217.68 billion by 2031, at a CAGR of 9.20% during the forecast period (2026-2031). Growing demand is closely tied to cloud-first mandates, AI-driven automation that lowers operating overhead, and an acute shortage of advanced infrastructure talent. Enterprises use managed partners to modernize networks and data centers, accelerate edge deployments for Industry 4.0, and adopt green-data-center practices that satisfy emerging ESG scorecards. The managed IT infrastructure services market now functions as a strategic enabler of digital transformation, shifting relationships from cost-arbitrage toward business-outcome contracts. Competition is intensifying as global system integrators, telecom carriers, and cloud-native specialists converge on platform-based, automation-rich offerings.

Key Report Takeaways

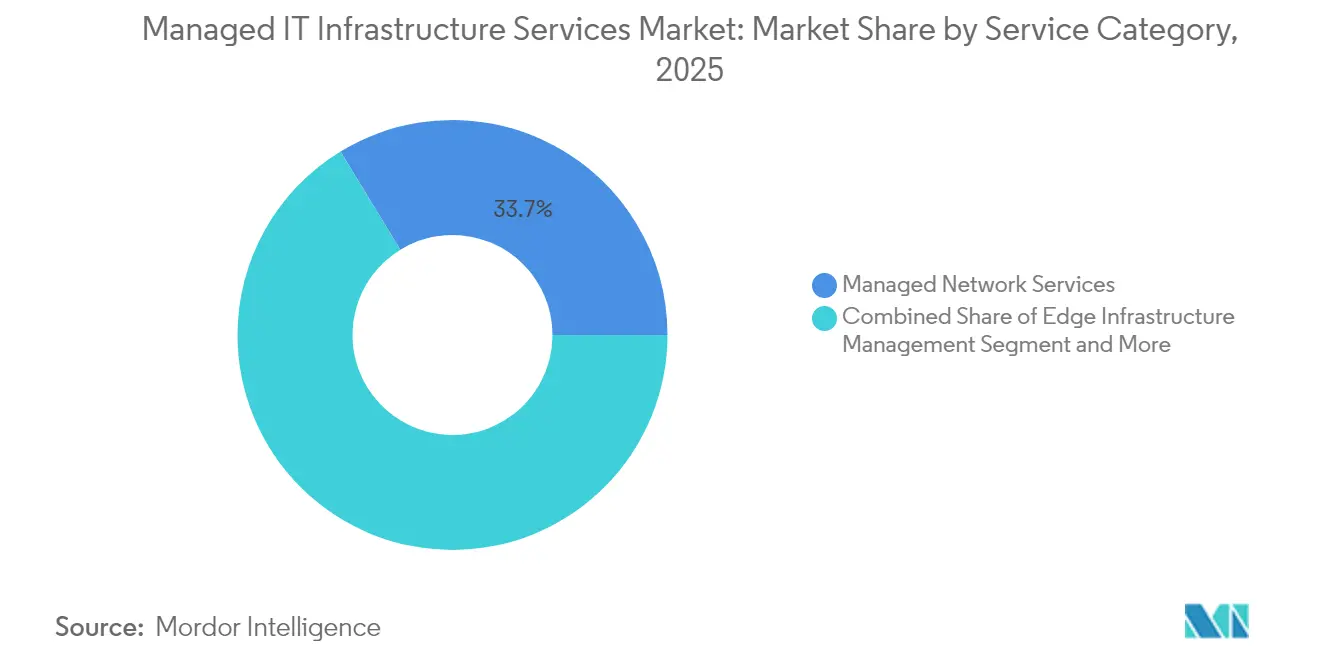

- By service category, managed network services held 33.72% of the managed IT infrastructure services market share in 2025, while edge infrastructure management is advancing at an 11.33% CAGR through 2031.

- By enterprise size, large enterprises accounted for 60.55% of the managed IT infrastructure services market size in 2025, whereas small and medium enterprises are projected to expand at a 9.28% CAGR to 2031.

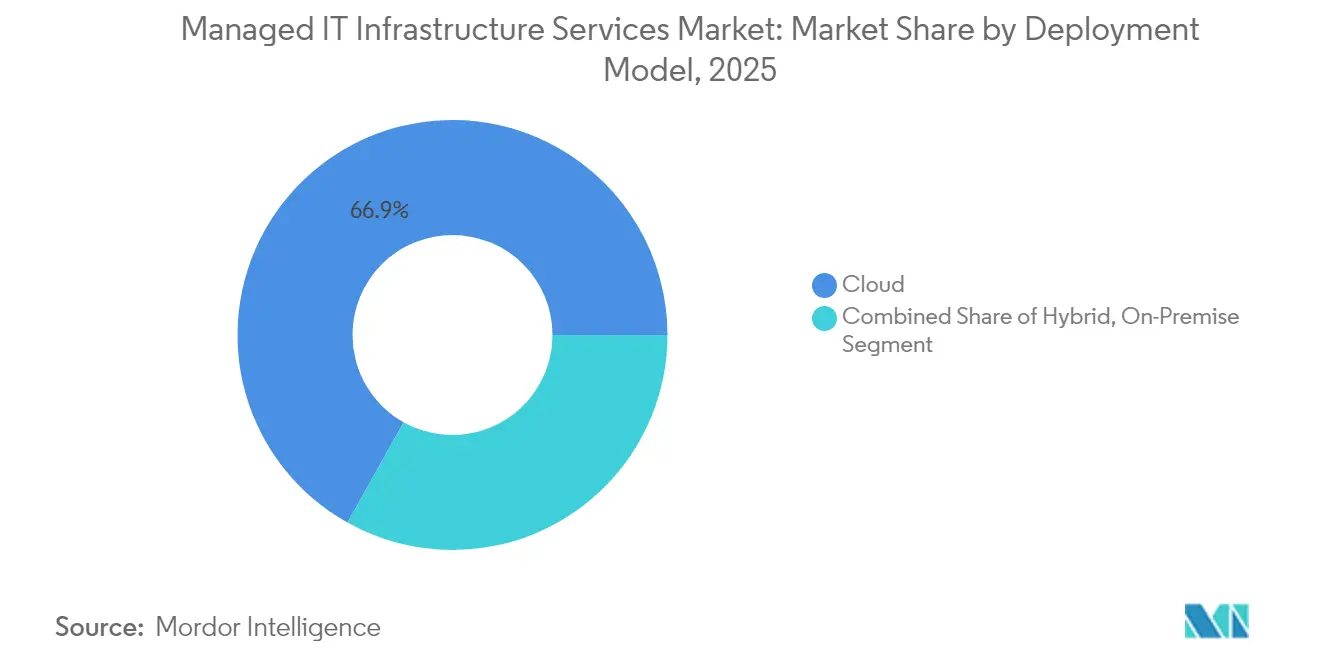

- By deployment model, cloud deployments commanded 66.88% of the managed IT infrastructure services market size in 2025, but hybrid approaches are forecast to grow at a 10.52% CAGR between 2026-2031.

- By end-user industry, IT and Telecommunication led with 25.75% revenue share in 2025; healthcare is set to post the fastest 9.54% CAGR through 2031.

- By geography, North America dominated with 34.12% market share in 2025, while Asia Pacific is projected to deliver the highest 10.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Managed IT Infrastructure Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost optimisation through outsourcing | +2.1% | North America, Europe, global scope | Medium term (2-4 years) |

| Cloud and hybrid-first transformation wave | +2.8% | Global, led by North America, strong in Asia-Pacific | Long term (≥ 4 years) |

| IT-skills shortage in advanced infrastructure ops | +1.9% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| AI-driven hyper-automation lowers MTTR | +1.4% | North America and Europe early, and Asia-Pacific following | Medium term (2-4 years) |

| Edge infrastructure surge in Industry 4.0 | +1.2% | APAC manufacturing hubs, expanding worldwide | Long term (≥ 4 years) |

| Green-datacentre mandates and ESG scorecards | +0.8% | Europe leading, global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Optimisation Through Outsourcing

Enterprises are replacing labour-arbitrage contracts with outcome-based partnerships that funnel savings into innovation programs. Managed vendors provide predictable operating expenses, freeing CIO budgets for AI pilots and product digitization. CFO stewardship now benchmarks partners on uptime, resiliency, and experience scores rather than invoice line items. These dynamics reaffirm the managed IT infrastructure services market as a lever for value creation rather than a cost-cutting commodity.

Cloud and Hybrid-First Transformation Wave

Cloud migration has matured into workload placement optimisation across multicloud estates. Enterprises mix hyperscaler, colocation, and edge footprints to satisfy latency, sovereignty, and TCO goals. The expanded Oracle Database@Azure program—now in 24 additional regions—underscores how joint service catalogs mitigate lock-in and achieve policy compliance.[1]Oracle Corp., “Microsoft and Oracle Expand Partnership to Satisfy Global Demand for Oracle Database@Azure,” oracle.com Providers able to engineer and operate these interwoven fabrics win larger, longer contracts that elevate the managed IT infrastructure services market.

IT-Skills Shortage in Advanced Infrastructure Ops

High demand for Kubernetes platform engineers, site-reliability architects, and observability specialists has widened the talent gap. MSPs offset scarcity with 24×7 command centers, skill academies, and AI copilots that reduce manual toil. Clients increasingly treat MSP benches as an extension of internal teams, driving recurring revenue streams. The shortage therefore directly lifts contract volumes across the managed IT infrastructure services market.[2] Kyndryl Ltd., “Kyndryl to Modernize and Manage Canara Bank’s IT Operations,” kyndryl.com

AI-Driven Hyper-Automation Lowers MTTR

Predictive analytics now pre-empt incidents, while auto-remediation scripts restore services within minutes. A leading Asian bank cut outage minutes by deploying a managed AIOps stack that monitors 111.9 million customer accounts. As hyper-automation becomes table stakes, MSPs differentiate by embedding domain-specific AI and secure data pipelines. Quicker mean-to-recovery cements the managed IT infrastructure services market as an operational risk-mitigation partner.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security and privacy concerns | −1.8% | Regulated industries worldwide | Short term (≤ 2 years) |

| Vendor lock-in and integration complexity | −1.2% | Legacy-heavy enterprises globally | Medium term (2-4 years) |

| Escalating power/cooling OPEX for MSPs | −0.9% | High-energy-cost regions | Long term (≥ 4 years) |

| Data-sovereignty/geopolitical fragmentation | −0.7% | Europe, China, emerging worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security and Privacy Concerns

Financial services and healthcare boards scrutinise managed deals for threat exposure and compliance posture. HIPAA requires robust Business Associate Agreements, layered encryption, and audit trails before workloads leave hospital campuses.[3]Lakeridge IO, “HIPAA for Managed Service Providers,” lakeridge.io Extended due diligence lengthens sales cycles and can delay revenue realisation, tempering near-term growth for the managed IT infrastructure services market.

Vendor Lock-in and Integration Complexity

Proprietary management planes impede portability between providers, raising exit costs. Clients, therefore, demand open APIs and reference architectures that ease migration. The launch of a platform-agnostic service catalog by a global provider illustrates the strategic pivot toward neutrality to assuage lock-in fears. Until standards mature, integration pain will continue to restrain some buyers within the managed IT infrastructure services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Category: Network Services Drive Market Leadership

In 2025, managed network services accounted for 33.72% of total revenue, making connectivity optimisation the biggest contributor to overall demand. Enterprises continue to modernise SD-WAN and zero-trust architectures to support hybrid work and latency-sensitive SaaS. Parallel growth in edge orchestration at an 11.33% CAGR mirrors rising sensor density and real-time analytics across factories. The managed IT infrastructure services market rewards vendors that merge campus, branch, cloud, and edge monitoring into single observability stacks.

Network modernisation also anchors higher-value cross-selling. Once circuits and routers fall under an MSP’s remote management, adjacent services such as SASE gateways, firewall-as-a-service, and AI-based traffic optimisation follow. Virtualisation, storage, and server management maintain steady demand as legacy hardware is rationalised, but margins trend lower due to commoditisation. By contrast, cloud infrastructure management is ascending on the back of multicloud finops, security posture management, and AI workload tuning. Providers that package these layers in integrated blueprints will capture outsized wallet share as the managed IT infrastructure services market matures.

By Enterprise Size: SME Adoption Accelerates Market Expansion

Large enterprises delivered 60.55% of 2025 billings, reflecting complex multiregional estates needing 24×7 oversight. However, SMEs now post a 9.28% CAGR to 2031, benefitting from subscription pricing that obviates data-center buildouts. Cloud marketplaces and self-service portals let a 500-employee retailer spin up managed firewalls, backups, and observability within hours.

The resulting democratization fuels net-new logo growth inside the managed IT infrastructure services market. For MSPs, SME onboarding drives volume efficiency, though ARPU remains lower than with global accounts. Economies of scale thus hinge on automation and AI chatbots that minimise manual ticket handling while preserving SLA adherence. As consumption models evolve, flexible term lengths and modular bundles will remain decisive in winning SME contracts.

By Deployment Model: Hybrid Strategies Reshape Infrastructure Approaches

Cloud-only estates represent 66.88% share today, yet hybrid architectures are scaling fastest at a 10.52% CAGR. Regulatory workloads, low-latency manufacturing apps, and data-sovereignty mandates keep critical systems on-premises or in dedicated colocation cages. MSPs therefore orchestrate policy engines that dynamically route traffic among private clusters, hyperscaler regions, and edge nodes.

This pivot cements the role of unified control planes, identity brokering, and cost-visibility dashboards across clouds. Enterprises value partners who combine certified experts for AWS, Azure, and Oracle with ITIL processes and local compliance expertise. On-premises footprints no longer stagnate; they integrate with managed Kubernetes distributions and NVMe-over-Fabrics to sustain legacy performance needs. The complexity lifts service intensity, expanding the managed IT infrastructure services market size for hybrid management offerings.

By End-User Industry: Healthcare Leads Digital Transformation Acceleration

IT and Telecommunication remained the top revenue contributor at 25.75% in 2025 as carriers outsource network lifecycle operations and OTT players offload CDN optimization. Yet healthcare’s 9.54% CAGR reflects robust investment in telemedicine, AI-assisted imaging, and secure interoperability among electronic health records. Providers seek MSPs possessing HIPAA attestation and real-time ransomware response capabilities.

BFSI, manufacturing, retail, and energy sectors show differentiated yet solid trajectories. Banks replace monolithic cores with cloud-ready microservices, requiring round-the-clock managed observability. Automotive and discrete manufacturing adopt edge orchestration to enable predictive maintenance and digital twins, boosting outsourced demand. Energy utilities modernise grid SCADA through managed private LTE and OT cybersecurity offerings. Such verticalisation strategies further enlarge the managed IT infrastructure services market opportunity set.

Geography Analysis

North America sustained 34.12% revenue share in 2025, reflecting early-mover maturity in workload outsourcing and stringent SLAs that favour outcome-based contracts. United States multinationals execute multi-year renewals covering cloud migration, AI co-development, and zero-trust enablement. Canadian firms prioritise hybrid platforms to ensure data residency, and Mexican manufacturers deploy managed campus networks aligned with Automotive-4.0 production lines. Vendor competition here is intense, driving consolidation among midsized MSPs and telecom-carrier captives.

Asia Pacific is projected to grow at 10.12% CAGR through 2031, the fastest regional pace inside the managed IT infrastructure services market. China’s state-incentivised digitisation funnels managed spend into smart-factory platforms. Japan’s enterprises experiment with private-cloud AI clusters to accelerate product innovation cycles, while India’s domestic startups adopt consumption-based managed Kubernetes clusters straight from the cloud. Australia, South Korea, and ASEAN-5 economies witness leapfrog uptake as businesses bypass legacy data centers and go straight to SaaS and managed edge nodes.

Regulatory Landscape

Managed IT infrastructure service delivery is increasingly shaped by horizontal cybersecurity and operational-resilience rules that raise expectations for third-party risk governance and incident reporting, especially for regulated buyers. In the European Union, the Digital Operational Resilience Act (DORA, Regulation (EU) 2022/2554) entered full application in January 2025, requiring financial entities to implement ICT risk management, resilience testing, incident reporting, and ICT third-party risk controls. DORA also set up an EU Oversight Framework for critical ICT service providers, which can bring managed service providers and cloud operators into supervisory scope.

Standards and policy proposals are also tightening expectations for cyber governance and sovereignty in managed environments. In February 2024, NIST released Cybersecurity Framework 2.0, adding the Govern function and expanding applicability beyond critical infrastructure to broader organizations, reinforcing supply-chain accountability that often lands on MSPs operating customer infrastructure. In June 2026, the European Commission advanced proposals related to EU cloud and AI capacity and assessment frameworks (including the Cloud and AI Development Act concept and the ongoing Cybersecurity Act revision package), which increases emphasis on cybersecurity assurance and sovereignty signaling for cloud, hybrid, and managed infrastructure services used across the EU.

Competitive Landscape

The market now features three competitive strata. First, global system integrators bundle consulting, transformation, and managed run services, often via proprietary platforms that orchestrate multicloud and edge assets. Second, focused managed specialists such as telco-anchored MSPs leverage deep network IP to target connectivity, SASE, and IoT. Third, cloud-native challengers rely on serverless automation and AI to deliver low-touch, high-margin skeleton crews. Acquisition momentum remains brisk, with larger players buying AI-ops startups and regional boutiques to fill portfolio gaps and secure local delivery capacity.

Strategic differentiation tilts toward AI-assisted remediation, carbon-neutral hosting, and industry-specific templates that accelerate time-to-value. A five-year renewal between a global tyre manufacturer and its MSP underscores how clients prize joint-innovation roadmaps over vendor-of-record status. Multicloud alliances such as Oracle-Microsoft tighten competitive fences by embedding sticky co-engineered services deeper into customer estates. Meanwhile, investment consortia spearheaded by Microsoft and BlackRock pour billions into next-gen data-center capacity, reinforcing supply-chain advantages for hyperscale-aligned MSPs. Despite moderate consolidation, more than 200 regional providers hold niche footholds, sustaining healthy price-performance tension across the managed IT infrastructure services market.

Managed IT Infrastructure Services Industry Leaders

Fujitsu Limited

Verizon Communications Inc.

Microsoft Corporation

IBM Corporation

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Outcome-linked, AI-enabled operations are creating near-term whitespace in managed network and hybrid infrastructure management, where enterprises want a managed control plane spanning cloud regions, on-prem estates, and edge nodes while reducing MTTR and operating overhead. In July 2026, Tata Consultancy Services signed a multi-year agreement with ABB to manage global network operations under a network-as-a-service model using AI-driven automation, illustrating how large buyers are moving from ticket-based support to AI-led, platform-driven network operations aligned to enterprise transformation programs.

Regulated-sector modernization and sovereign-by-design delivery are also expanding opportunity for providers that build governance, data residency, and third-party risk controls into standard managed architectures. In July 2026, Accenture announced a contract with NATO focused on resilient and agile digital infrastructure, and World Wide Technology received a U.S. Army GEMSS 2.1 agreement to modernize and centralize enterprise IT support, reinforcing government and defense demand for managed modernization at scale. Alongside this, large multi-year managed workplace and network engagements, including HCLTechs July 2026 USD 1.14 billion, 5.5-year contract in Europe, point to continued buyer willingness to commit when providers can operationalize AI-driven delivery models across infrastructure and network domains, with additional room for verticalized templates in BFSI, healthcare, and public sector environments where compliance and resilience are procurement gating factors.

Recent Industry Developments

- July 2026: Kyndryl expanded sovereignty solutioning with Microsoft by integrating Microsoft Sovereign Cloud capabilities with Kyndryl managed services for regulated enterprise architectures. The integration targets managed infrastructure offerings for data residency and compliance requirements, aligning with buyer demand for sovereign and hybrid deployments.

- April 2025: Kyndryl launched AI Private Cloud services for business, combining consulting with secure hosting and operations for AI workloads across industries such as financial services, healthcare, and manufacturing. This broadened the companys managed infrastructure portfolio toward AI-ready private cloud environments where governance and security controls are central to adoption.

- November 2024: Kyndryl and Microsoft introduced mainframe modernization and generative AI services aimed at helping enterprises transform legacy workloads for Microsoft Cloud. The joint offering paired modernization tooling with managed services, accelerating hybrid-cloud transitions for organizations with mainframe-dependent infrastructure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers third-party, contract-based services that run and optimize an enterprise's IT infrastructure on a day-to-day basis, including monitoring, maintenance, incident handling, and change support across core infrastructure layers.

Scope exclusions: We exclude one-time professional services projects and the sale of standalone hardware or software licenses that are not delivered as part of an ongoing managed service.

Segmentation Overview

- By Service Category

- Virtualization

- Networking

- Storage

- Servers

- Cloud Infrastructure Management

- Edge Infrastructure Management

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Deployment Model

- On-premises

- Cloud

- Hybrid

- By End-User Industry

- IT and Telecommunication

- BFSI

- Manufacturing

- Retail and E-commerce

- Transportation and Logistics

- Healthcare

- Energy and Utilities

- Geographic Analysis

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market frame and keep the numbers tied to real IT spending signals and infrastructure activity. We rely on public, official source types such as US Bureau of Economic Analysis and US Bureau of Labor Statistics data, plus Eurostat, the International Telecommunication Union, and World Bank indicators to understand macro IT demand and regional patterns.

To translate that context into a usable model, we also review company filings and annual reports, investor presentations, contract announcements, and reliable press coverage for managed service revenue cues and client adoption language. Where it helps, we use paid subscriptions for company financials and intelligence, news and financials, and patent databases to verify timelines and service capability shifts. This list is not exhaustive, and we reviewed additional sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys help confirm what buyers actually purchase under managed infrastructure contracts, how bundles are priced, and what drives renewals across industries and regions. We speak with service providers, channel partners, and enterprise IT decision-makers to test assumptions on migration pace, typical contract lengths, and which infrastructure layers are most often outsourced in each geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 51% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 18% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where overall IT services spend and infrastructure operations intensity are reconstructed by region, then filtered using managed adoption rates and outsourcing penetration discussed in interviews. After the demand pool is built, we split it using service-mix weights that reflect how often networking, storage, server management, virtualization, and related infrastructure management are bundled in contracts.

To keep the totals realistic, we cross-check with selective bottom-up approximations using sampled provider revenues, deal sizes observed in public announcements, and simple volume times average contract value logic for large buyer cohorts. Inputs that matter most in this market include cloud migration pace, data center footprint shifts (including edge sites), average contract duration and renewal rates, remote monitoring and automation adoption, labor cost pressure in infrastructure operations, and regional IT spending growth. Forecasting uses scenario analysis, where a base case is adjusted using primary feedback on budget cycles, cloud repatriation or hybrid trends, and changes in outsourcing preferences. When bottom-up signals are missing in smaller countries or niche use cases, we fill gaps with proxy ratios from comparable markets and then re-check them with expert feedback before locking the final curve.

Data Validation & Update Cycle

Validation is done by cross-checking outputs against independent signals such as regional IT services spending growth, hiring and wage trends for infrastructure roles, and large contract flow patterns seen in public reporting. If a regional result moves too far from these signals, the assumptions are revisited and, where needed, respondents are re-contacted to clarify what changed.

Before sign-off, the model goes through multiple review steps, including variance checks across regions and a logic review of service mix and pricing progressions. Reports are refreshed annually, and interim updates are made when material events shift demand or pricing, after which a final pass is completed close to delivery so clients receive the latest updated view.

Mordor Intelligence's Managed IT Infrastructure Services Market Estimate Compared With Other Published Estimates

Published market values for managed IT infrastructure services often do not line up because the scope lines are drawn differently, and the inputs behind pricing and adoption are refreshed at different times. The year used, the mix of cloud versus on-premise delivery counted, and whether adjacent services are bundled can all change the final number.

One-time professional services and standalone hardware or software license sales sit outside Mordor Intelligence's scope, which can pull some published totals down or up depending on how tightly those items are bundled into managed infrastructure contracts. Gaps also show up when a source applies a single global growth rate, uses aggressive cloud migration assumptions, or converts currencies using a different timing that does not match the measurement year used for revenue capture.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 140.36 B (2026) | |

| Global Consultancy A | USD 146.98 B (2026) | Uses a broader revenue definition that can include related goods bundled into the service and may apply different geographic revenue attribution rules, which tends to lift the total versus a pure managed-service revenue view. |

| Industry Research Group B | USD 131.95 B (2024) | Uses a different base year and may apply a narrower capture of managed infrastructure work, with limited clarity on contract scope and service-bundle treatment, making cross-year comparison sensitive to assumed pricing and migration pace. |

The spread across sources mainly comes from what gets counted as managed infrastructure service revenue, the year chosen for the starting value, and how bundled items are treated. By keeping the model traceable to clear demand indicators, contract behavior, and region-wise checks, our estimate stays easier to explain and replicate when users test the assumptions.

Key Questions Answered in the Report

What is the current value of the managed IT infrastructure services market?

The market is valued at USD 140.36 billion in 2026 and is set to grow to USD 217.68 billion by 2031.

Which region is growing fastest?

Asia Pacific shows the highest growth with a projected 10.12% CAGR through 2031, driven by large-scale digital-transformation programs.

Which service category leads revenue?

Managed network services hold the top position with 33.72% share in 2025, reflecting their foundational role in connectivity modernisation.

What industry vertical is expanding quickest?

Healthcare leads with a 9.54% CAGR as hospitals adopt telemedicine platforms, AI diagnostics, and secure cloud records.

Page last updated on: