| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 11.34 Billion |

| Market Size (2030) | USD 12.43 Billion |

| CAGR (2025 - 2030) | 1.86 % |

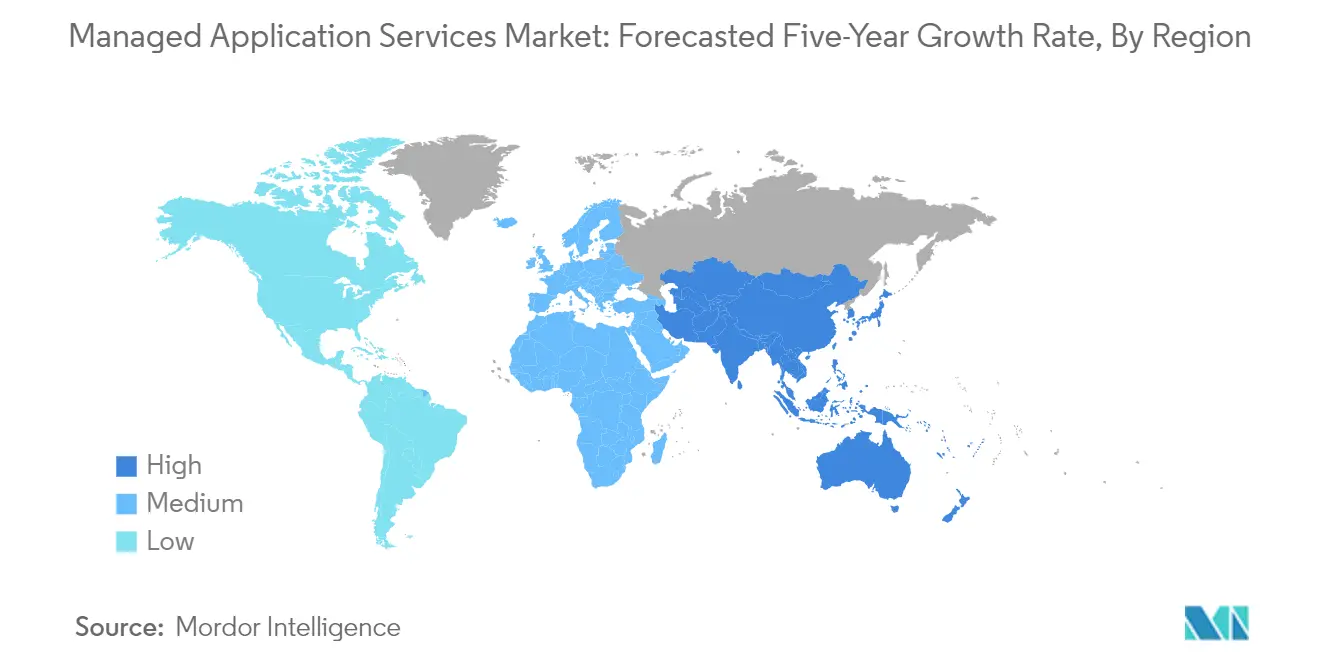

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Managed Application Services Market Analysis

The Managed Application Services Market size is estimated at USD 11.34 billion in 2025, and is expected to reach USD 12.43 billion by 2030, at a CAGR of 1.86% during the forecast period (2025-2030).

The managed application services industry is experiencing a fundamental transformation as enterprises increasingly embrace comprehensive application management services solutions. Studies indicate that the successful deployment of managed services can reduce IT costs by 25-45% while increasing operational efficiency by 45-65%, demonstrating the tangible benefits of these solutions. This shift is particularly pronounced among small and medium enterprises, with industry data showing that approximately 60% of managed service providers' clients have between 1-150 employees. The evolution of service delivery models has led to more flexible and scalable solutions, enabling organizations of all sizes to access enterprise-grade application management capabilities.

The technological landscape continues to evolve with the emergence of cloud-native architectures and microservices-based solutions. Recent developments include VSHN's announcement of Project Syn, representing a next-generation open-source managed services framework for DevOps and application operations. This framework introduces pre-integrated tools for provisioning, updating, backing up, and monitoring production applications on Kubernetes and in the cloud. The integration of DevOps practices through complete self-service and automation has become a cornerstone of modern application lifecycle management strategies, reflecting the industry's movement toward more sophisticated service delivery models.

Infrastructure modernization remains a critical focus area, with organizations increasingly adopting hybrid and multi-cloud environments. According to recent industry analysis, approximately 20% of large enterprises now invest over USD 12 million annually in public cloud infrastructure, highlighting the significant financial commitment to managed cloud services. The launch of Amazon Managed Apache Cassandra Service exemplifies this trend, offering scalable, highly available database services that enable seamless workload management in the cloud without the complexity of infrastructure management.

The proliferation of connected devices and automation technologies is reshaping the managed services landscape. Industry research from Cisco indicates that 46% of network devices are now machine-to-machine or IoT-based, necessitating more sophisticated application performance management approaches. Service providers are responding by developing comprehensive solutions that integrate security, performance monitoring, and automated management capabilities. This evolution is driving the development of more sophisticated service offerings that can handle the complexity of modern application environments while maintaining high levels of security and performance.

Managed Application Services Market Trends

Ongoing Shift to the Cloud Coupled with Growing Demand for Integrated Application Hosting Services

The increasing adoption of cloud computing and integrated application hosting services is fundamentally transforming how enterprises manage their IT infrastructure. According to the Hazelcast Infinity Data report, IT decision-makers identified cloud application performance as a critical opportunity to unlock profits, with financial services (49%), telecommunications (42%), and e-commerce (40%) ranking it as their highest priority. Application hosting services have emerged as essential computing platforms that enable software delivery via the Internet, supporting everything from content management applications to database applications and email management systems, providing organizations with operational flexibility and scalability.

The shift toward cloud-based application hosting services is driven by the need for improved security, enhanced application performance, and simplified management capabilities. Organizations are increasingly adopting subscription-based cloud hosting models, which provide cost-effective solutions while offering benefits such as high availability, disaster recovery, and seamless integration capabilities. Major technology providers are expanding their cloud application hosting capabilities through strategic partnerships and innovative solutions, as evidenced by Microsoft's collaboration with Pivotal to create Azure Spring Cloud, designed to simplify the deployment and management of Spring Cloud applications.

Understand The Key Trends Shaping This Market

Download PDF

Organizations are Increasingly Looking at Outsourcing Non-core Functions to Gain Competitive Advantage

Enterprises are strategically outsourcing their non-core functions to managed service providers, driven by the potential to reduce IT costs by 25-45% while increasing operational efficiency by 45-65%. According to a comprehensive study by NTT Ltd covering inputs from over 1,250 IT and business leaders across 29 countries, nearly half the respondents (45%) indicated their organizations would outsource more than they insource in the coming months, highlighting the growing trend toward managed IT services adoption. This shift enables companies to focus on their core competencies while leveraging external expertise for technical operations.

The application maintenance outsourcing trend is particularly strong among organizations seeking to optimize their resource allocation and improve service delivery. Companies are increasingly splitting their application management duties, outsourcing legacy management tasks while redirecting their in-house teams toward strategic projects. This approach helps organizations control ongoing expenditure, share risks associated with new technology adoption, and achieve economies of scale. Managed service providers are responding by offering comprehensive application management solutions that include consulting, implementation, functional and technical support, and overall IT infrastructure management.

Digitization Efforts and High Adoption of Mobile Solutions to Augment Growth

The rapid digitization of business processes coupled with the increasing adoption of mobile solutions is creating substantial demand for managed software services. According to recent industry data, 64% of surveyed network and IT managers plan to implement SD-WAN managed services, highlighting the growing emphasis on digital transformation initiatives. This trend is particularly evident in sectors such as retail, healthcare, and financial services, where mobile applications have become crucial for delivering enhanced customer experiences and improving operational efficiency.

The proliferation of BYOD (Bring Your Own Device) policies and enterprise mobility solutions is further driving the need for managed software services. Organizations implementing BYOD policies are experiencing significant cost benefits, with enterprises saving an average of USD 350 per year per employee through basic BYOD programs, while more sophisticated reactive programs can boost these savings to as much as USD 1,300 per year per employee. This trend is complemented by the increasing adoption of mobile applications for critical business functions, requiring robust management solutions to ensure security, compliance, and optimal performance across diverse mobile platforms and devices.

Segment Analysis: By Organization Size

Large Enterprises Segment in Managed Application Services Market

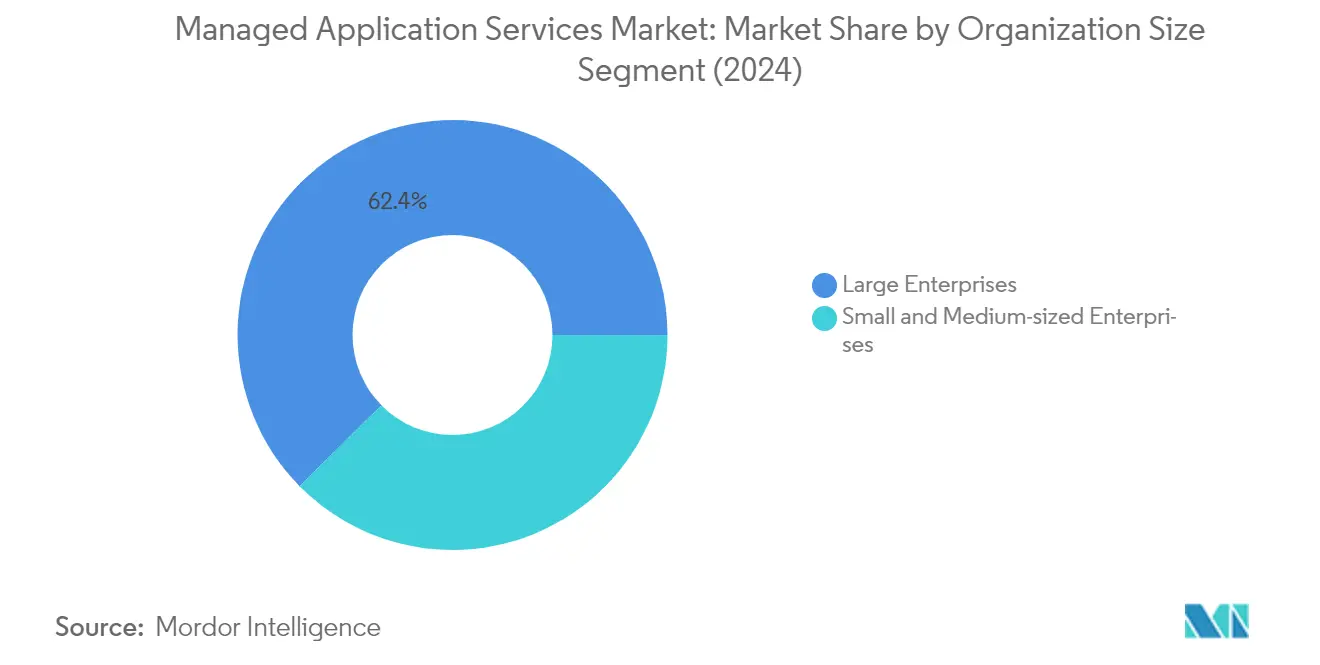

Large enterprises continue to dominate the managed application services market, holding approximately 62% market share in 2024. These organizations, characterized by their extensive IT environments spanning multiple technology types, face significant challenges related to complexity and scale. The segment's dominance is primarily driven by these enterprises' substantial IT budgets, their need for comprehensive end-to-end enterprise software management and application support services, and their increasing focus on digital transformation initiatives. Large enterprises are particularly attracted to managed services due to their ability to handle complex application portfolios, provide specialized expertise, and offer robust security measures. The adoption of cloud computing, mobility solutions, and advanced technologies like AI and machine learning has further strengthened this segment's position, as large organizations seek partners who can manage their sophisticated application landscapes while ensuring business continuity and innovation.

SME Segment in Managed Application Services Market

The Small and Medium-sized Enterprises (SME) segment is emerging as the fastest-growing segment in the managed application services market, with a projected growth rate of approximately 19% during 2024-2029. This accelerated growth is primarily driven by SMEs' increasing recognition of the value proposition offered by managed services in terms of cost reduction and access to advanced technologies. The segment's growth is further fueled by the rising adoption of cloud-based solutions, which enable SMEs to access enterprise-grade applications without significant upfront investments. The increasing complexity of application maintenance services, coupled with limited internal IT resources and expertise, is compelling more SMEs to partner with managed service providers. Additionally, the growing focus on digital transformation and the need to maintain competitiveness in an increasingly digital marketplace are key factors driving SMEs to adopt managed application services.

Segment Analysis: By End-User Vertical

BFSI Segment in Managed Application Services Market

The Banking, Financial Services, and Insurance (BFSI) sector dominates the managed application services market, accounting for approximately 26% of the total market share in 2024. This significant market position is driven by the sector's rapid digital transformation initiatives and increasing need for robust application support services. Financial institutions are increasingly leveraging managed services to handle their complex application portfolios, ensure regulatory compliance, and maintain high security standards. The adoption of cloud-based services, integrated application hosting services, and the growing demand for digital banking solutions have further strengthened the BFSI segment's position. Financial applications performing critical transactions, such as online banking portals and insurance applications, require sophisticated security measures and continuous monitoring, making managed application services essential for maintaining operational efficiency and customer trust.

Healthcare Segment in Managed Application Services Market

The healthcare sector is emerging as the fastest-growing segment in the managed application services market, with an expected growth rate of approximately 20% during 2024-2029. This remarkable growth is primarily driven by the increasing digitalization of healthcare services, the rising adoption of telemedicine platforms, and the growing need for efficient management of electronic health records (EHR). Healthcare organizations are increasingly embracing managed application services to handle their complex IT infrastructure while ensuring compliance with stringent regulations and privacy concerns. The deployment of mobile applications, mobile medical devices, and intelligent wearable devices has significantly improved the quality of healthcare by providing real-time health information to patients and doctors, creating a strong demand for digital application services to support these technological advancements.

Remaining Segments in End-User Vertical

The managed application services market encompasses several other significant segments, including Retail & E-commerce, IT & Telecom, Manufacturing, and Other End-user Verticals. The retail and e-commerce sector is experiencing substantial growth due to the increasing adoption of digital commerce platforms and the need for seamless customer experience management. The IT and Telecom sector continues to be a crucial segment, driven by the high rate of technological adoptions and increased frequency of BYOD policy implementation. The manufacturing sector is leveraging managed services for optimizing production processes and implementing Industry 4.0 initiatives. Other verticals, including energy and utilities, media and entertainment, are also contributing significantly to the market's growth through their digital transformation initiatives and increasing reliance on application outsourcing services.

Managed Application Services Market Geography Segment Analysis

Managed Application Services Market in North America

North America continues to dominate the global managed application services market, holding approximately 35% of the market share in 2024. The region's leadership position is driven by the changing IT infrastructure landscape, particularly among small and medium enterprises that are increasingly focusing on outsourcing various services. The penetration of smartphones and tablets, coupled with strong network connectivity across the region, is encouraging organizations to adopt BYOD policies, further driving market growth. The region's managed services adoption is particularly strong in sectors like healthcare, retail, and financial services, where organizations are leveraging these services to enhance operational efficiency and reduce costs. North American companies are rapidly evolving their IT infrastructure, leading to the adoption of several technologies required to improve productivity and maintain a competitive advantage. The benefits of improved agility, flexibility, and faster application deployment are key factors driving adoption in this region. The market is characterized by a strong presence of major service providers and a mature technological infrastructure, making it a benchmark for global managed cloud services market adoption.

Managed Application Services Market in Europe

The European managed application services market has demonstrated robust growth, recording approximately 12% growth annually from 2019 to 2024. The region's market is characterized by increasing reliance on managed service providers among organizations seeking to maintain a competitive edge, regardless of their size. The migration from private to public cloud is becoming a preferred choice among businesses, driven by lower costs and increased convenience. European organizations are particularly focused on digital transformation initiatives, with many businesses seeking consulting services that bring agile elements into all aspects of their operations. The region's strong regulatory framework, particularly around data protection and privacy, has created unique requirements for managed service providers. The market is seeing increased demand for hybrid cloud solutions, with organizations looking for flexible deployment options that can meet both performance and compliance requirements. The presence of a large number of small and medium enterprises, coupled with their growing focus on digitalization, continues to create new opportunities for managed service providers in the region.

Managed Application Services Market in Asia-Pacific

The Asia-Pacific managed application services market is positioned for exceptional growth, with a projected growth rate of approximately 20% annually from 2024 to 2029. The region's market is characterized by the increasing adoption of mobile applications and a significant presence of SMEs with limited resources, driving them towards managed services adoption. Organizations across the region are increasingly embracing cloud computing and digital transformation initiatives, creating substantial opportunities for managed service providers. The market is witnessing a shift in enterprise mindset, with more businesses recognizing the value of outsourcing non-core functions to gain competitive advantages. The region's diverse economic landscape, ranging from mature markets like Japan and Singapore to emerging economies like India and Indonesia, presents unique opportunities for service providers. The growing emphasis on digital transformation across various sectors, particularly in banking, retail, and manufacturing, is creating new avenues for enterprise application services. The market is also seeing increased demand for security and compliance services, as organizations seek to protect their digital assets while maintaining regulatory compliance.

Managed Application Services Market in Rest of the World

The Rest of the World region, encompassing Latin America and the Middle East & Africa, represents an emerging market for managed application services with significant growth potential. The market in these regions is characterized by increasing adoption of cloud services and digital transformation initiatives across various sectors. Organizations in these regions are increasingly looking for better application performance, enhanced security, and the ability to meet compliance requirements. The underlying benefits of lower costs and simplified application management are driving factors for fintech companies and other start-ups in adopting managed services. Recent developments in information systems, coupled with government initiatives to spur technological advancements, are creating new opportunities for service providers. The market is witnessing increased investment in infrastructure development and growing demand for real-time data monitoring capabilities. The adoption of application management services market is particularly strong in sectors such as banking, telecommunications, and government services, where organizations are seeking to modernize their operations while maintaining cost efficiency.

Get Analysis on Important Geographic Markets

Download PDF

Managed Application Services Industry Overview

Top Companies in Managed Application Services Market

The managed application services industry features prominent players like IBM Corporation, Fujitsu Limited, HCL Technologies, Wipro, Mindtree, and CenturyLink leading the competitive landscape. These companies are heavily investing in cloud-native architectures and microservices development to enhance their service portfolios. Strategic focus areas include artificial intelligence integration, automation capabilities, and DevOps practices to deliver more efficient application management solutions. Companies are expanding their digital transformation capabilities through innovation labs and research centers worldwide, while simultaneously strengthening their cybersecurity offerings to address growing security concerns. The market is characterized by continuous product innovation, particularly in areas like hybrid cloud management, containerization, and application modernization services market. Operational agility is being achieved through platform-based delivery models and integrated service management frameworks, while geographic expansion is primarily driven through strategic partnerships and local market penetration strategies.

Consolidation and Integration Drive Market Growth

The managed application services market exhibits a moderate level of consolidation, with global IT services conglomerates holding significant market share alongside specialized regional players. Large multinational corporations leverage their extensive infrastructure and cross-domain expertise to offer comprehensive enterprise application services, while regional specialists focus on niche markets and industry-specific solutions. The competitive dynamics are shaped by the presence of both pure-play application management providers and diversified IT service companies that offer managed services as part of their broader portfolio. Market participants are increasingly adopting platform-based delivery models and establishing dedicated innovation centers to maintain a competitive advantage.

The market is witnessing substantial merger and acquisition activity, driven by the need to acquire specialized capabilities and expand geographic presence. Companies are pursuing strategic acquisitions to strengthen their technical capabilities, particularly in emerging areas like cloud computing, artificial intelligence, and automation. These consolidation efforts are aimed at creating comprehensive service offerings that can address the evolving needs of enterprise customers. The trend towards vertical integration is evident as service providers seek to control the entire value chain, from infrastructure management to application development and maintenance, enabling them to offer more integrated and efficient solutions to their clients.

Innovation and Customer Focus Drive Success

Success in the managed application services market increasingly depends on providers' ability to deliver innovative solutions while maintaining strong customer relationships. Service providers must focus on developing industry-specific expertise and solutions that address unique vertical requirements, particularly in highly regulated sectors like banking and healthcare. The ability to offer flexible engagement models and demonstrate a clear value proposition through outcome-based pricing is becoming crucial for market success. Companies need to invest in building strong partner ecosystems and maintaining technology vendor relationships to ensure comprehensive service delivery capabilities. Additionally, providers must focus on developing strong automation capabilities and incorporating artificial intelligence to improve service delivery efficiency and reduce costs.

Market participants must address the growing emphasis on security and compliance while maintaining service quality and cost competitiveness. The increasing concentration of end-users in certain industries necessitates specialized domain expertise and industry-specific solutions. While substitution risk from in-house IT teams exists, the complexity of modern application landscapes and the need for specialized skills continue to drive demand for managed services. Regulatory compliance requirements, particularly in data protection and privacy, are becoming increasingly important factors in service provider selection. Success in this market requires a balanced approach to innovation, operational excellence, and customer relationship management, while maintaining the agility to adapt to changing technology landscapes and customer requirements. The application lifecycle management market is also seeing growth as companies seek to optimize their application processes.

Managed Application Services Market Leaders

-

HCL Technologies Limited

-

Fujitsu Ltd.

-

IBM Corporation

-

Virtustream, Inc.

-

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Managed Application Services Market News

- June 2022 - AWS Managed Services (AMS) Accelerate a new cloud operations offering that assists customers in achieving operational excellence regardless of their cloud journey. Accelerate can run any workload on Amazon Web Services (AWS) while giving customers complete access to all AWS services. AWS services such as AWS Systems Manager, Amazon CloudWatch, Amazon GuardDuty, and AWS Config are used by Accelerate for operations and security.

- Moreover, these services are less expensive than other commercial alternatives and can be integrated into existing enterprise processes. Customers can be production-ready in days as a result of this. Customers can get support 24 hours a day, seven days a week from a team of cloud experts who bring AWS best practices, experience, and operational processes at scale.

- February 2022 - "Let's create," IBM's new integrated global platform was launched. "Let's create" reflects IBM's current vision, strategy, and purpose. It reaffirms the company's commitment to innovation and collaboration to create long-term value for clients and partners while assisting them in addressing their most pressing business issues. 'Let's create' is an invitation to IBM's clients and partners to collaborate on data-driven solutions that automate, modernize, secure, and transform organizations worldwide by leveraging IBM's hybrid cloud and artificial intelligence (AI) technology, as well as our consulting expertise.

Managed Application Services Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increased demand for end-to-end application hosting

- 4.2.2 The requirement to improve and secure critical business applications

- 4.2.3 Increase in the level of application infrastructure

-

4.3 Market Restraints

- 4.3.1 Security risks associated with application data

- 4.4 Value Chain / Supply Chain Analysis

-

4.5 Porters 5 Force Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 PESTLE Analysis

5. MARKET SEGMENTATION

-

5.1 Organization Size

- 5.1.1 Small & Medium-scale Enterprises

- 5.1.2 Large Enterprises

-

5.2 End-user Verticals

- 5.2.1 BFSI

- 5.2.2 Retail & E-Commerce

- 5.2.3 IT & Telecom

- 5.2.4 Manufacturing

- 5.2.5 Healthcare

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.5 Middle East

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers & Acquisitions

-

6.3 Company Profiles

- 6.3.1 Fujitsu Limited

- 6.3.2 IBM Corporation

- 6.3.3 HCL Technologies Limited

- 6.3.4 Wipro Limited

- 6.3.5 VIRTUSTREAM INC.

- 6.3.6 RACKSPACE INC.

- 6.3.7 CenturyLink, Inc.

- 6.3.8 DXC Technology Company

- 6.3.9 BMC Software, INC.

- 6.3.10 Mindtree Limited

- 6.3.11 Unisys Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Managed Application Services Industry Segmentation

Managed Application Services (MAS) are defined as a service offering that leverages a managed service provider's expertise to manage an enterprise's critical applications efficiently. Managed application services provide companies and organizations with the necessary tools, resources, and knowledge. It can be used to implement system-to-system integrations, advanced reporting, new user training, business-efficiency customizations, and many other things. The research examines driven application service demand across key end-user segments, deployment type, geography, and the impact of COVID-19 on the overall managed application services market.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Organization Size | Small & Medium-scale Enterprises | ||

| Large Enterprises | |||

| End-user Verticals | BFSI | ||

| Retail & E-Commerce | |||

| IT & Telecom | |||

| Manufacturing | |||

| Healthcare | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | India | ||

| China | |||

| Japan | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Middle East | United Arab Emirates | ||

| Saudi Arabia | |||

| Rest of Middle East | |||

Need A Different Region or Segment?

Customize Now

Managed Application Services Market Research FAQs

How big is the Managed Application Services Market?

The Managed Application Services Market size is expected to reach USD 11.34 billion in 2025 and grow at a CAGR of 1.86% to reach USD 12.43 billion by 2030.

What is the current Managed Application Services Market size?

In 2025, the Managed Application Services Market size is expected to reach USD 11.34 billion.

Who are the key players in Managed Application Services Market?

HCL Technologies Limited, Fujitsu Ltd., IBM Corporation, Virtustream, Inc. and Wipro Limited are the major companies operating in the Managed Application Services Market.

Which is the fastest growing region in Managed Application Services Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Managed Application Services Market?

In 2025, the North America accounts for the largest market share in Managed Application Services Market.

What years does this Managed Application Services Market cover, and what was the market size in 2024?

In 2024, the Managed Application Services Market size was estimated at USD 11.13 billion. The report covers the Managed Application Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Managed Application Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Managed Application Services Market Research

Mordor Intelligence provides a comprehensive analysis of the Managed Application Services (MAS) industry through detailed research and consulting expertise. Our extensive report covers the evolving landscape of application lifecycle management, enterprise software management, and application performance management. The analysis includes key segments such as managed IT services, application modernization services, and managed cloud services. These insights are crucial for stakeholders and are available in an easy-to-download report PDF format.

The report offers valuable intelligence on enterprise application services, application maintenance services, and application support services, enabling businesses to make informed decisions. Our analysis also covers emerging areas like cloud application management, SaaS management services, and digital application services. Additionally, it examines application hosting services and application optimization services. Stakeholders gain access to detailed market size assessments, growth projections, and comprehensive insights into the managed software services ecosystem. This is supported by our proven research methodology and industry expertise.