| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 11.40 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Malaysia Payment Market Analysis

The Malaysia Payments Market is expected to register a CAGR of 11.4% during the forecast period.

Malaysia's payments landscape is undergoing a significant digital transformation, supported by robust technological infrastructure and increasing internet penetration. According to recent data, internet users in Malaysia increased by 365,000 (+1.3%) between 2021 and 2022, while cellular mobile connections reached 42.11 million at the start of 2022. The country's payment systems have evolved from traditional paper-based methods to increasingly cashless and paperless solutions in the digital era. The government has established comprehensive payment infrastructure for smooth operations, with the Bank Negara Malaysia-owned Payments Network Malaysia Sdn Bhd (PayNet) operating the country's extensive value payment system, RENTAS, which enables secure transfer and settlement of high-value interbank financial transactions and securities.

The banking sector is witnessing unprecedented innovation through the introduction of new digital services and strategic partnerships. In 2023, a significant development was the gradual integration of PayNow-DuitNow linking Singapore and Malaysia's real-time payment systems, enabling customers to transfer funds between the two countries using just mobile numbers. The central bank has also approved new digital bank licenses, marking a pivotal shift in the financial services landscape. These digital banks are expected to introduce specialized products and payment services with reduced switching costs, fostering greater competition and innovation in the sector.

The merchant acceptance infrastructure continues to expand, with EFTPOS terminals reaching 804,413 in July 2022, demonstrating the growing adoption of digital payment solutions at physical points of sale. The retail sector has shown remarkable resilience and adaptation to digital payments, with retail sales recording a significant increase of 62.5% year-over-year in the second quarter of 2022. This growth has been particularly notable in fashion and accessories, supermarkets, and department stores, indicating a broad-based adoption of digital payment solutions across various retail segments.

The widespread adoption of digital payments is evident from the Visa 2022 Consumer Payment Attitudes report, which reveals that 96% of Malaysians now use digital payments. Financial institutions and technology providers are continuously innovating to meet this growing demand, introducing new electronic payment solutions such as QR codes, contactless payments, and digital wallets. The payment ecosystem has evolved to include various stakeholders, from traditional banks to fintech companies, creating a competitive environment that drives innovation and improves service delivery. These developments are supported by regulatory frameworks that ensure security while promoting innovation, making Malaysia's payment system more efficient and accessible to all segments of society.

Malaysia Payment Market Trends

Solid E-commerce Growth, Rising Basket Spend, and an Increasingly Digitally Savvy Population

Malaysia's digital economy is experiencing remarkable growth, driven by a tech-savvy population that increasingly embraces online shopping and digital wallet usage. The country has established itself as an attractive market for e-commerce in Southeast Asia, supported by its dynamic economy and well-developed digital infrastructure. According to recent data, about 82.9% of mobile users in Malaysia actively shop online, demonstrating the population's high comfort level with online payments. This trend is further reinforced by the presence of three major annual national shopping events – Malaysia Super Sale (March), Malaysia Mega Sale Carnival (June-August), and Malaysia Year-End Sale (November-December), which have significantly contributed to increased online shopping adoption and digital wallet usage.

The country's digitally savvy population continues to grow, evidenced by the increasing adoption of advanced technologies including social media, cloud computing, and the Internet of Things. As of January 2022, Malaysia recorded 30.25 million social media users, representing an 8% increase from the previous year. This digital transformation is complemented by the country's digital economy blueprint, which focuses on empowering Malaysians with digital literacy, high-value job creation, fintech education, and healthcare improvements. The blueprint, extending until 2030, includes substantial investments in digital framework, telecommunications strengthening, nationwide 5G rollout, and cloud service provider enhancement, with a total investment of USD 15 billion, creating a robust foundation for continued e-commerce and online payments growth.

Understand The Key Trends Shaping This Market

Download PDF

Adoption of Card-based Payments

The growth of card-based payments in Malaysia is primarily supported by the continuous expansion of payment infrastructure and favorable regulatory policies. A significant indicator of this growth is the increasing number of EFTPOS terminals across the country, which reached 804,413 in July 2022, compared to 668,057 in 2019, demonstrating the robust development of card payment acceptance infrastructure. This expansion is further supported by the Central Bank's initiatives, including the Payment Cards Framework, which aims to ensure fair and reasonable card acceptance costs for merchants while addressing various frictions in the payment card market.

The adoption of card-based payments is also driven by the growing preference for contactless payments and the convenience they offer for both in-store and online transactions. According to the Visa Consumer Payment Attitudes report, 96% of Malaysians now use online payments, with card payments being one of the predominant methods. This trend is reinforced by continuous innovations in the payment ecosystem, such as the integration of new payment gateway technologies and the introduction of virtual credit cards (VCCs) by financial institutions. For instance, Alliance Bank Malaysia Bhd launched the country's first VCC for individuals, offering enhanced security features for online transactions and demonstrating the banking sector's commitment to advancing card-based payment solutions.

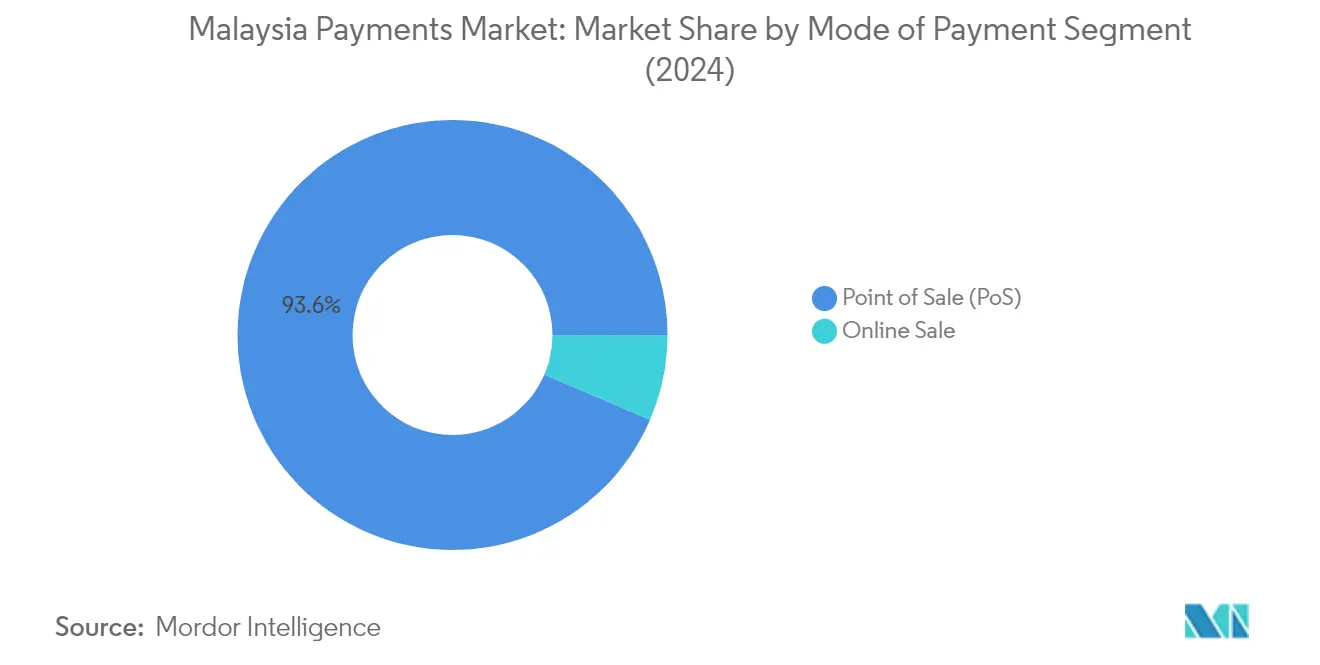

Segment Analysis: By Mode of Payment

Point of Sale (PoS) Segment in Malaysia Payments Market

The Point of Sale (PoS) segment dominates the Malaysia payments market, commanding approximately 94% market share in 2024, demonstrating its crucial role in the country's payment ecosystem. This substantial market position is supported by the widespread adoption of various PoS payment methods at physical stores, including card payments, digital wallets, and cash transactions. The segment's strength is further reinforced by the increasing integration of modern payment processing technologies at retail locations, with merchants actively embracing contactless payments and QR code solutions. Major financial institutions and payment service providers continue to enhance their PoS offerings, focusing on security, convenience, and faster transaction processing to maintain the segment's dominant position in the market.

Online Sale Segment in Malaysia Payments Market

The Online Sale segment is experiencing remarkable growth in the Malaysia payments market, with an expected growth rate of approximately 20% during 2024-2029. This accelerated growth is primarily driven by the rapid expansion of e-commerce, increasing digital literacy, and growing consumer confidence in online transactions. The segment's growth is further supported by the proliferation of innovative digital payment solutions, including digital wallets, card payments, and emerging options like Buy Now Pay Later (BNPL) services. Financial institutions and technology companies are actively developing and implementing advanced security measures and user-friendly interfaces to enhance the online payment experience, contributing to the segment's robust growth trajectory.

Segment Analysis: By End-User Industry

Retail Segment in Malaysia Payments Market

The retail payment segment dominates the Malaysia payments market, commanding approximately 38% market share in 2024, driven by the country's robust retail infrastructure and digital transformation initiatives. The segment's leadership position is strengthened by the widespread adoption of digital payment solutions across both traditional and modern retail channels. Malaysia's retail sector has witnessed significant evolution with over 1,000 shopping centers offering more than 16.42 million square meters of retail space, creating extensive opportunities for merchant payment adoption. The integration of various payment technologies, including mobile wallets, contactless payments, and QR-based solutions, has transformed the retail payment landscape. Major retail chains and merchants are increasingly partnering with payment service providers to offer innovative payment solutions, while regulatory initiatives supporting cashless transactions have further accelerated digital payment adoption in the retail sector.

Remaining Segments in End-User Industry

The healthcare segment maintains a significant presence in the Malaysian payments market, focusing on digitizing payment processes across public and private healthcare facilities. The entertainment segment has evolved significantly with the integration of digital payment solutions across streaming services, gaming platforms, and traditional entertainment venues. The hospitality sector has embraced digital payments to enhance customer experience and streamline operations across hotels, restaurants, and tourism services. Other end-user industries, including transportation, education, and consumer electronics, collectively represent a substantial portion of the market, each contributing to the diverse payment ecosystem through specialized solutions and use cases tailored to their specific needs.

Malaysia Payment Industry Overview

Top Companies in Malaysia Payments Market

The Malaysia payments market features a mix of established financial institutions and emerging fintech players, including Maybank, PayPal Holdings, United Overseas Bank, iPay88, CIMB Group, Samsung Pay, Visa, Bank Islam Malaysia, GrabPay, and Huawei Pay. These companies are driving innovation through cloud-based payment technology platforms, digital wallet solutions, and integrated merchant services. The industry demonstrates strong operational agility through real-time payment solutions and cross-border transaction capabilities. Strategic partnerships between traditional banks and technology providers are reshaping the competitive landscape, while expansion strategies focus on reaching underserved segments and rural areas. Companies are investing heavily in developing comprehensive digital ecosystems that combine payment services with value-added features like loyalty programs, installment options, and merchant analytics tools.

Dynamic Market with Strong Growth Potential

The Malaysian payments landscape is characterized by a balanced mix of global payment networks and local financial institutions, with domestic players holding significant market share due to their deep understanding of local preferences and regulatory requirements. Traditional banks are transforming into digital-first institutions through strategic partnerships with fintech companies, while global payment providers are localizing their offerings to better serve the Malaysian market. The market structure shows moderate consolidation with established players maintaining their positions through continuous innovation and service enhancement.

The market is witnessing increased merger and acquisition activity as companies seek to expand their technological capabilities and market reach. Global payment providers are entering the market through strategic acquisitions of local fintech companies, while domestic banks are forming joint ventures to develop new digital payment solutions. This trend is particularly evident in the e-wallet segment, where companies are combining resources to achieve scale and technological advancement. The competitive dynamics are further influenced by the emergence of new digital banks and payment service providers who are challenging traditional players with innovative solutions.

Innovation and Adaptation Drive Market Success

For incumbent players to maintain and expand their market share, they must focus on developing comprehensive digital payment ecosystems that integrate multiple services and payment channels. Success factors include building robust merchant networks, offering seamless payment experiences, and developing value-added services that address specific market needs. Companies need to invest in advanced payment security measures and compliance frameworks while maintaining competitive pricing structures. The ability to form strategic partnerships and leverage data analytics for personalized services will be crucial for market leadership.

New entrants and challenger brands can gain ground by focusing on underserved market segments and developing specialized solutions for specific industries or user groups. The market presents opportunities for companies that can effectively address pain points in traditional payment systems while offering innovative features that appeal to digitally-savvy consumers. Success will depend on building trust through robust payment security measures, maintaining regulatory compliance, and developing user-friendly interfaces. The regulatory environment continues to evolve in favor of digital payments, though companies must remain vigilant in addressing compliance requirements and maintaining high security standards to protect against emerging threats.

Malaysia Payment Market Leaders

-

Ipay88 (m) Sdn Bhd

-

United overseas bank (Malaysia) Bhd

-

PayPal Holdings Inc.

-

Cimb Group Holdings Berhad

-

Maybank

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Malaysia Payment Market News

- May 2023: Maybank launched its cross-border QR payment service for Maybank customers traveling to Singapore, Indonesia, and Thailand, as they can now make cashless and instant payment transactions via the MAE app. Similarly, incoming tourists from these countries can make cashless payments with Maybank QRPay merchants in Malaysia. The new offering will enable Malaysians visiting the respective countries to enjoy a cheaper, faster, and more convenient payment option through the MAE app.

- January 2023: Xoom, PayPal's international money transfer service, has announced that it has launched a new cross-border money transfer product, debit card deposit, enabling Xoom customers, and the new feature will offer remittance receivers easy, secure, and real-time access to funds, which are sent directly to a recipient's eligible Visa debit card.

Malaysia Payment Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the Payments Landscape in Malaysia

- 4.5 Key Market Trends Pertaining to the Growth of Cashless Transaction in Malaysia

- 4.6 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 E-commerce Growth, Rising Basket Spend, and Rise in Digitally-aware Population

- 5.1.2 Adoption of Card-based Payments

-

5.2 Market Restraints

- 5.2.1 Challenges Faced by Small Retailers and Street Vendors while Adapting to the Cashless Payment Ecosystem

-

5.3 Market Opportunities

- 5.3.1 Digitalization of Payment Services

- 5.3.2 Expansion of E-commerce Businesses

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of Major Case Studies and Use Cases

- 5.6 Analysis of the Key Demographic Trends and Patterns in the Payments Industry in Malaysia

- 5.7 Analysis of the Increasing Emphasis on Customer Satisfaction and Convergence of the Global Trends in Malaysia

- 5.8 Analysis of Cash Displacement and Rise of Contactless Payment Modes in Malaysia

6. MARKET SEGMENTATION

-

6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments

- 6.1.1.2 Digital Wallets

- 6.1.1.3 Cash

- 6.1.1.4 Other Point-of-sale Payments

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments

- 6.1.2.2 Digital Wallets

- 6.1.2.3 Other Online Sale Payments

-

6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Maybank

- 7.1.2 Paypal Holdings Inc.

- 7.1.3 United Overseas Bank (Malaysia) Bhd

- 7.1.4 Ipay88 (m) Sdn Bhd

- 7.1.5 Cimb Group Holdings Berhad

- 7.1.6 Samsung Pay (Samsung Electronics Co. Ltd)

- 7.1.7 Visa Inc.

- 7.1.8 Bank Islam Malaysia Berhad

- 7.1.9 Grab Pay (Grab Holdings Limited)

- 7.1.10 Huawei Pay (Huawei Technologies Co. Ltd)

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Malaysia Payment Industry Segmentation

Payment shall be a voluntary transfer of funds, equivalent, or other valuable items from one person to another in exchange for goods and services received or satisfying an obligation under the law.

The Malaysian Payments Market is segmented by mode of payment (point of sale (card payments, digital wallets (including mobile wallets), cash) and online sale (card payments, digital wallets)) and end-user industry (retail, entertainment, healthcare, and hospitality).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Mode of Payment | Point of Sale | Card Payments | |

| Digital Wallets | |||

| Cash | |||

| Other Point-of-sale Payments | |||

| Online Sale | Card Payments | ||

| Digital Wallets | |||

| Other Online Sale Payments | |||

| By End-user Industry | Retail | ||

| Entertainment | |||

| Healthcare | |||

| Hospitality | |||

| Other End-user Industries | |||

Need A Different Region or Segment?

Customize Now

Malaysia Payment Market Research FAQs

What is the current Malaysia Payments Market size?

The Malaysia Payments Market is projected to register a CAGR of 11.4% during the forecast period (2025-2030)

Who are the key players in Malaysia Payments Market?

Ipay88 (m) Sdn Bhd, United overseas bank (Malaysia) Bhd, PayPal Holdings Inc., Cimb Group Holdings Berhad and Maybank are the major companies operating in the Malaysia Payments Market.

What years does this Malaysia Payments Market cover?

The report covers the Malaysia Payments Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Malaysia Payments Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Malaysia Payments Market Research

Mordor Intelligence provides a comprehensive analysis of the payments industry in Malaysia. We leverage our extensive expertise in financial transactions and payment technology research. Our detailed report examines the evolution of electronic payments and the adoption of digital wallets. It also highlights emerging trends in payment gateway implementation and online payments systems. The analysis covers various segments, including mobile payments, contactless payments, and cryptocurrency payments. This offers stakeholders crucial insights into payment infrastructure development and payment authentication protocols. The report PDF is available for download, offering in-depth coverage of payment processing dynamics and payment security measures.

This comprehensive study benefits industry participants by delivering actionable insights into money transfer innovations and advancements in payment solutions. The report examines the ecosystems of merchant payments, B2B payments, and P2P payments. It also analyzes payment software implementation and payment hardware deployment strategies. Our research thoroughly covers the transformation of digital payments, the adoption of instant payments, and the integration of POS payments. Additionally, it explores developments in the wholesale payments and retail payments sectors. The analysis also delves into C2B payments dynamics and emerging payment services. It provides stakeholders with strategic recommendations for optimizing their market positioning and operational efficiency.