Malaysia Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

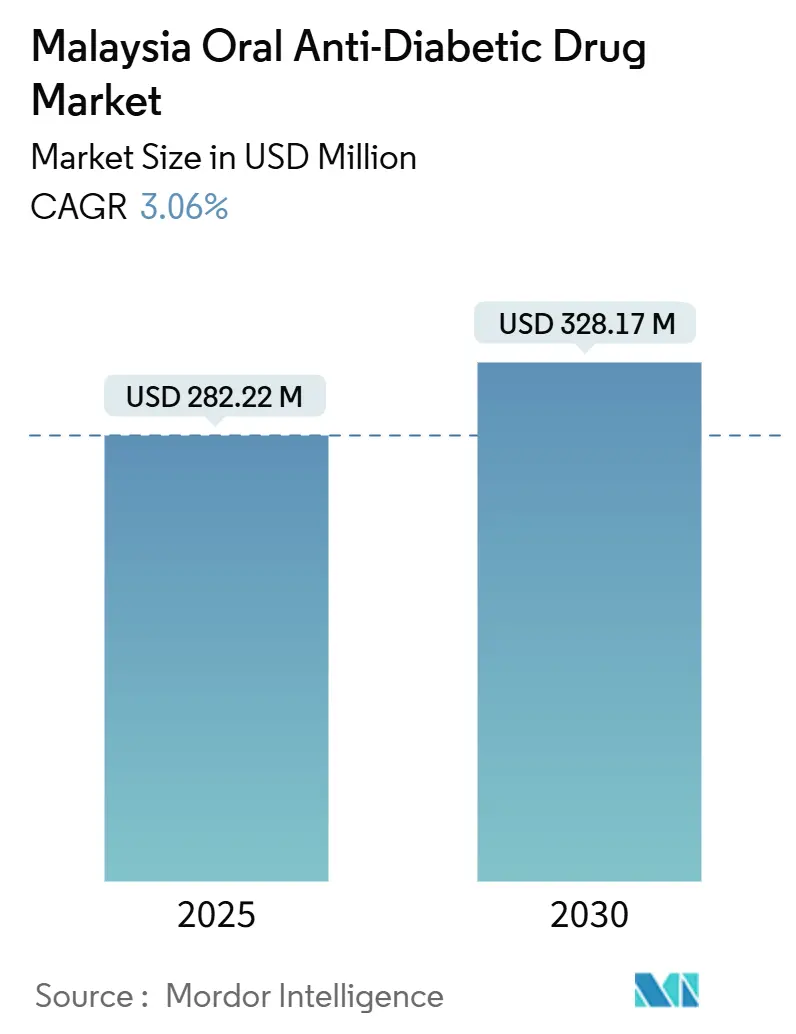

| Market Size (2025) | USD 282.22 Million |

| Market Size (2030) | USD 328.17 Million |

| Growth Rate (2025 - 2030) | 3.06% CAGR |

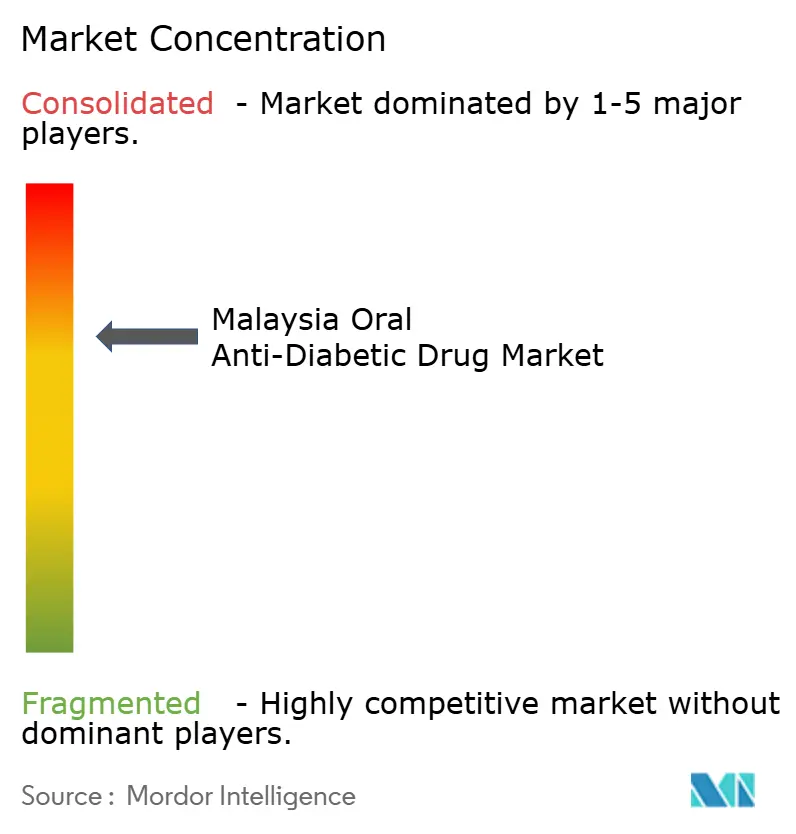

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malaysia Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The Malaysia oral anti-diabetic drug market size stands at USD 282.22 million in 2025 and is projected to reach USD 328.17 million by 2030, advancing at a 3.06% CAGR. The measured pace conceals brisk changes in public health, policy, and channel dynamics. Rapid urbanisation, an ageing population, and tighter screening protocols keep demand for oral therapies on a steady upward slope. Government budgeting supports this trend, with the Ministry of Health raising 2025 allocations by 9.8% to RM45.3 billion, part of which funds non-communicable disease programs [1]Ministry of Health Malaysia, “National Budget 2025 Health Allocation Highlights,” moh.gov.my . Newer therapeutic classes such as SGLT-2 inhibitors are now reimbursed in public facilities, while digital pharmacies widen last-mile reach, especially in East Malaysia. Parallel reforms in procurement, halal certification, and price controls further shape competitive behaviour across the Malaysia oral anti-diabetic drug market.

Key Report Takeaways

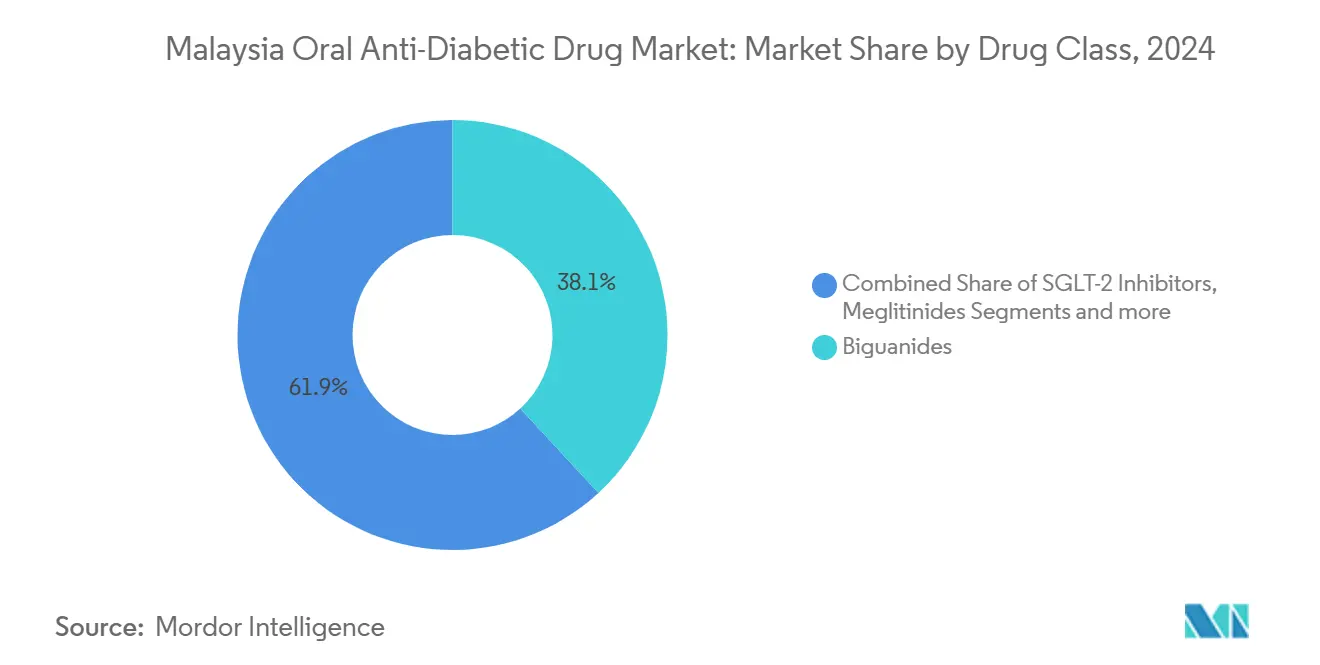

- By drug class, biguanides led with 38.13% revenue share in 2024; SGLT-2 inhibitors are forecast to expand at a 3.64% CAGR through 2030.

- By age group, adults held 67.13% share in 2024; the geriatric segment is set to grow at a 3.98% CAGR to 2030.

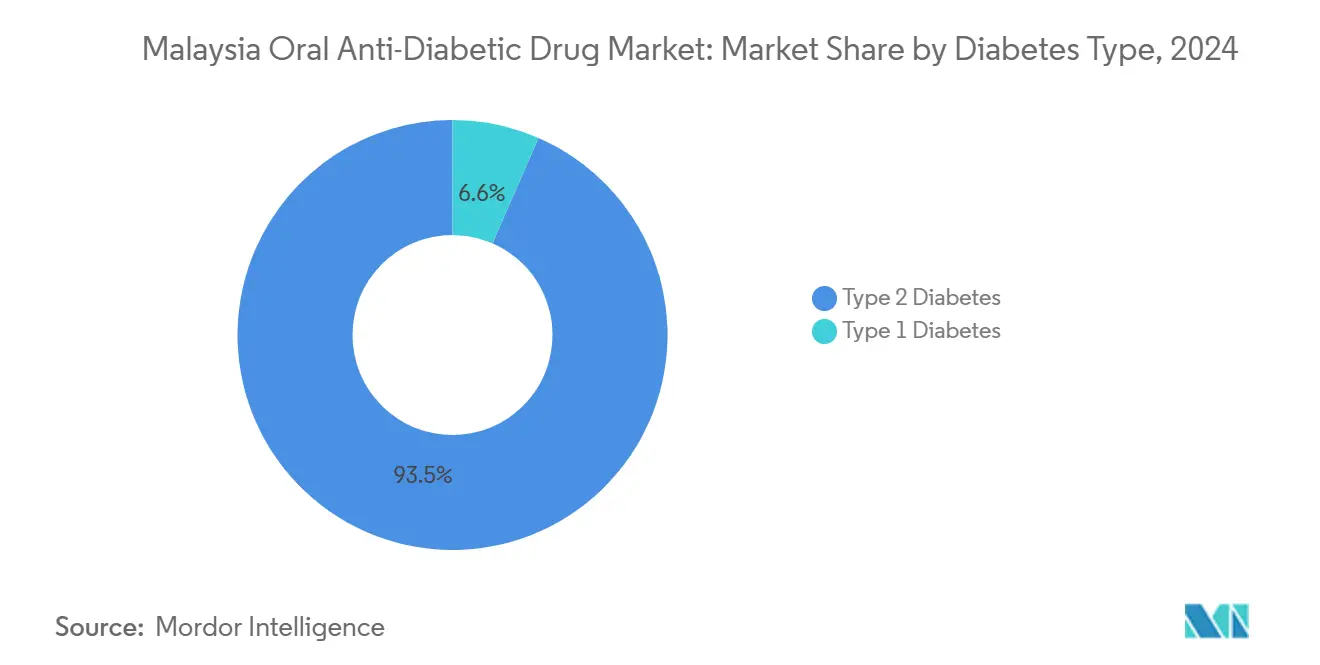

- By diabetes type, type 2 diabetes accounted for 93.45% of the Malaysia oral anti-diabetic drug market share in 2024 and is advancing at a 3.87% CAGR to 2030.

- By distribution channel, hospital pharmacies captured 69.23% share in 2024, while online pharmacies are projected to rise at a 3.88% CAGR through 2030.

Malaysia Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence of type-2 diabetes in urban Malaysia | +1.2% | Peninsular Malaysia urban centres, spillover to East Malaysia | Medium term (2-4 years) |

| Expansion of the private health-insurance pool | +0.8% | National, early gains in Kuala Lumpur, Selangor, Penang | Long term (≥ 4 years) |

| Rapid uptake of SGLT-2 & DPP-4 inhibitors post-NEML 2024 update | +0.9% | Public healthcare facilities nationwide | Short term (≤ 2 years) |

| Government-led “Mysihat” medication-adherence programmes | +0.6% | National, focus on rural and underserved communities | Medium term (2-4 years) |

| Centralised Pharmaniaga tenders squeezing retail prices | +0.4% | National public-sector procurement | Short term (≤ 2 years) |

| Growth of e-pharmacy platforms enhancing last-mile reach | +0.7% | National, notable impact in East Malaysia and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Type-2 Diabetes in Urban Malaysia

Urban centres now post diabetes prevalence of 19.6 deaths per 100,000 population, placing the disease among Malaysia’s top mortality drivers. Registry data spanning a decade lists 288,913 diagnosed patients, and only one-third meet lipid and blood-pressure targets, indicating wide therapeutic gaps [2]World Health Organization, “Non-Communicable Disease Country Profile Malaysia,” who.int . Sedentary lifestyles and nutrition shifts compound genetic predisposition, so pharmacotherapy remains essential even as prevention programs expand. Public hospitals respond by stockpiling metformin and by trialling fixed-dose combinations in primary care. This unmet need anchors baseline growth for the Malaysia oral anti-diabetic drug market.

Expansion of the Private Health-Insurance Pool

Healthcare spending reached 4.38% of GDP in 2025, with private insurance uptake rising among middle-income households. Broader coverage lowers out-of-pocket costs for premium agents such as SGLT-2 and DPP-4 inhibitors. Employer schemes in Kuala Lumpur, Selangor, and Penang now reimburse combination tablets that previously strained household budgets. New policies for foreign workers widen the risk pool and lift unit volumes. Insurers, in turn, negotiate tiered pricing with manufacturers, reinforcing value-based payment models in the Malaysia oral anti-diabetic drug market.

Rapid Uptake of SGLT-2 & DPP-4 Inhibitors Post-NEML 2024 Update

The 2024 National Essential Medicines List removed formulary barriers, allowing public hospitals to dispense SGLT-2 and DPP-4 inhibitors without ad-hoc waivers. Hospital studies report mean 0.9% HbA1c reductions for DPP-4 therapy and improved renal markers under SGLT-2 treatment. Eight SGLT-2 brands are now registered with active NPRA monitoring. Clinicians increasingly prescribe these classes over sulfonylureas, while guideline committees update algorithms accordingly. Early adoption strengthens revenue diversity across the Malaysia oral anti-diabetic drug market.

Government-Led “Mysihat” Medication-Adherence Programmes

The Enhanced Primary Healthcare framework merges telemedicine with community outreach to curb missed doses. Pharmacist-delivered coaching reduced average monthly drug costs to MYR 47.33 for intervention groups versus MYR 236.07 in controls, while tightening HbA1c control [3]Muhammad Zahid Iqbal, "Impact of Pharmacist Educational Intervention on Costs of Medication with Improved Clinical Outcomes for Diabetic Patients in Various Tertiary Care Hospitals in Malaysia: A Randomized Controlled Trial," MDPI, mdpi.com. DoctorOnCall’s virtual clinic expands these services to rural Sabah and Sarawak. The Health White Paper allocates multiyear funding for digital adherence tools, embedding monitoring into routine care. These measures boost treatment persistence and add volume to the Malaysia oral anti-diabetic drug market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying generic competition after key patent expiries | -0.8% | Branded products nationwide | Short term (≤ 2 years) |

| High out-of-pocket cost for latest agents despite reimbursement | -0.6% | Rural and lower-income segments nationally | Medium term (2-4 years) |

| Halal certification gaps limiting acceptance of some branded generics | -0.3% | National, particularly Muslim population segments | Long term (≥ 4 years) |

| Logistics hurdles to East Malaysia causing stock-out risk | -0.4% | East Malaysia (Sabah and Sarawak), affecting rural access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Generic Competition After Key Patent Expiries

Empagliflozin’s patent expiry in March 2025 and scheduled sitagliptin/metformin expiries in 2029 invite generic entries priced 50% lower in line with national policy. Indian firms have publicly targeted off-patent launches, and local manufacturers seek fast-track approvals under the updated NPRA guidebook. Branded incumbents respond with patient-support programs and fixed-dose lifecycle extensions. Volume may rise, yet value erosion weighs on headline growth for the Malaysia oral anti-diabetic drug market.

High Out-of-Pocket Cost for Latest Agents Despite Reimbursement

Fixed-dose combinations consume 44.6% of drug spending while making up only 28.91% of prescriptions, underscoring affordability gaps. Average oral therapy costs stand at USD 68 per patient, climbing to USD 185 when supplements and diagnostics are included. Rural households feel this burden most, leading to treatment deferrals or reliance on older agents such as metformin. Even with expanding insurance, co-payments for SGLT-2 tablets deter uptake. The resulting elasticity tempers the premium tier of the Malaysia oral anti-diabetic drug market.

Segment Analysis

By Drug Class: SGLT-2 Inhibitors Gain Ground on Biguanide Leadership

Biguanides retained 38.13% of the Malaysia oral anti-diabetic drug market share in 2024 owing to metformin’s entrenched role as first-line therapy. SGLT-2 inhibitors contribute small base revenues but grow at 3.64% CAGR, lifted by cardiovascular and renal outcome data. Sulfonylurea sales trend downward because of hypoglycaemia concerns, while DPP-4 inhibitors stabilise as second-line options in elderly cohorts. Alpha-glucosidase inhibitors and thiazolidinediones stay niche after gastrointestinal and safety drawbacks.

Fixed-dose combinations pairing metformin with SGLT-2 or DPP-4 molecules broaden adherence and command premium pricing. Upcoming generic metformin entries cushion price declines within the Malaysia oral anti-diabetic drug market. Meanwhile, exclusivity on newer classes allows innovators to recoup R&D spend. Manufacturers emphasise post-marketing surveillance to reassure prescribers on rare renal adverse events linked to SGLT-2 therapy.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Geriatric Demand Outpaces the Adult Core

Adults aged 20-65 years generated 67.13% of revenue in 2024, reflecting Malaysia’s primary working-age population base. The geriatric cohort, however, is set to expand at a 3.98% CAGR through 2030 as longevity improves and screening intensity rises. Paediatric cases remain minor but escalate with urban childhood obesity.

Geriatric prescribing patterns tilt to DPP-4 inhibitors for low hypoglycaemia risk, while adults receive broader regimens including SGLT-2 tablets. Rural outreach programs in Sarawak now offer quarterly medication reviews for seniors, lifting adherence. As comorbid conditions accumulate, demand shifts toward agents with proven cardiovascular benefit, reinforcing revenue resilience across the Malaysia oral anti-diabetic drug market.

By Diabetes Type: Type 2 Dominance Steers Innovation

Type 2 diabetes accounts for 93.45% of spend and shows a 3.87% CAGR outlook, mirroring global epidemiology. Type 1 remains insulin-centric and occupies a small slice of oral therapy spend, although adjunct trials are ongoing.

Personalised medicine frameworks guide drug choice for type 2 patients, weighing age, BMI, and renal status. Lifestyle programs run concurrently yet pharmacologic escalation remains common as beta-cell function wanes. Pipeline agents focus on weight control and cardiorenal outcomes rather than pure glucose lowering, aligning with unmet needs in the Malaysia oral anti-diabetic drug market.

By Distribution Channel: Online Pharmacies Extend Last-Mile Reach

Hospital pharmacies commanded 69.23% revenue in 2024 under subsidised government supply. Online pharmacies post a 3.88% CAGR forecast thanks to regulatory clarity on telepharmacy and rising consumer trust in e-commerce. Retail chains consolidate to secure purchasing clout and counter online discounting.

Digital platforms now couple medication delivery with teleconsultations and glucometer integrations. In East Malaysia, where terrain restricts physical access, mobile apps cut refill lead times by half. NPRA guidelines on remote counselling ensure safety, further legitimising the channel within the Malaysia oral anti-diabetic drug market.

Geography Analysis

Peninsular Malaysia generated the bulk of 2024 revenue, leveraging dense healthcare infrastructure and higher urban prevalence. Kuala Lumpur, Selangor, and Penang together house most specialist clinics and capture early uptake of SGLT-2 and DPP-4 therapies. Private insurance penetration in these states supports premium prescriptions, while procurement reforms encourage hospital formularies to broaden drug lists.

East Malaysia, covering Sabah and Sarawak, delivers the highest growth outlook to 2030. Federal funding of RM22.1 billion for new hospitals and rural telemedicine hubs narrows the historic service gap. Rural patients now achieve 43% HbA1c goal attainment versus the national average of 23.8% after Enhanced Primary Healthcare pilots. Cross-border trade with West Kalimantan improves supply chain routes, lowering stock-out risk.

Digital solutions hold particular value in remote interiors. DoctorOnCall’s platform schedules video consults with endocrinologists in urban centres, while drones trialled by public hospitals deliver urgent medications to island communities. These initiatives flatten geographic inequities and unlock untapped volumes for the Malaysia oral anti-diabetic drug market.

Competitive Landscape

The Malaysia oral anti-diabetic drug industry displays moderate consolidation. Multinationals dominate innovative classes, whereas local producers excel in generics and halal-certified formulations. Pharmaniaga’s shift away from single-supplier contracts pressures incumbents to compete on value rather than exclusivity. The firm’s Q3 2024 net profit jump to RM49.84 million signals success in diversifying revenue beyond public tenders.

Strategic alliances enhance market penetration. Owen Mumford joined forces with Duopharma Biotech to pair pen-injection devices with oral therapy starter kits, offering bundled solutions for newly diagnosed patients. Insulet’s RM878 million investment in an insulin manufacturing plant underscores confidence in Malaysia’s broader diabetes landscape, complementing oral therapy demand.

Digital capabilities emerge as critical differentiators. Firms deploy artificial-intelligence tools to optimise trial design and to predict adherence risks. Blockchain pilots trace halal-certification status from raw material to blister pack, appealing to Muslim consumers. These innovations strengthen competitive moats and sustain value creation within the Malaysia oral anti-diabetic drug market.

Malaysia Oral Anti-Diabetic Drug Industry Leaders

-

Astrazeneca

-

Astellas

-

Eli Lilly

-

Sanofi

-

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The National Pharmaceutical Regulatory Agency issued the Complete Drug Registration Guidance Document, Third Edition Ninth Revision, shortening approval timelines for diabetes therapies.

- December 2024: The World Health Organization and the Ministry of Health launched the RM30 billion National NCD Strategy, elevating diabetes management across prevention and treatment pillars.

- March 2024: Owen Mumford partnered with Duopharma Biotech to co-develop diabetes management solutions in Malaysia.

Malaysia Oral Anti-Diabetic Drug Market Report Scope

Orally administered antihyperglycemic drugs reduce blood glucose levels. They are often used in Type 2 diabetes care. The Malaysia Oral Anti-Diabetic Drug Market is segmented into drugs. The report offers the value (in USD) and volume (in Units) for the above segments.

| Biguanides |

| Sulfonylureas |

| Meglitinides |

| Thiazolidinediones |

| Alpha-Glucosidase Inhibitors |

| DPP-4 Inhibitors |

| SGLT-2 Inhibitors |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| Type 1 Diabetes |

| Type 2 Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Drug Class | Biguanides |

| Sulfonylureas | |

| Meglitinides | |

| Thiazolidinediones | |

| Alpha-Glucosidase Inhibitors | |

| DPP-4 Inhibitors | |

| SGLT-2 Inhibitors | |

| Others | |

| By Age Group | Adults |

| Pediatric | |

| Geriatric | |

| By Diabetes Type | Type 1 Diabetes |

| Type 2 Diabetes | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies |

Key Questions Answered in the Report

What is the current value of the Malaysia oral anti-diabetic drug market?

The market is valued at USD 282.22 million in 2025 and is projected to hit USD 328.17 million by 2030.

Which drug class is growing the fastest?

SGLT-2 inhibitors lead growth with a 3.64% CAGR following their addition to the 2024 National Essential Medicines List.

Why is the geriatric segment important for future sales?

Malaysia’s ageing population pushes geriatric demand up at a 3.98% CAGR, and elderly patients often require safer agents like DPP-4 inhibitors.

How are online pharmacies affecting distribution?

E-pharmacy channels are projected to grow at 3.88% CAGR, improving rural access and challenging traditional retail models.

What impact will patent expiries have on pricing?

Empagliflozin’s 2025 patent expiry is expected to cut branded prices by 50%, increasing generic competition and pressuring margins.