Malaysia Adhesives And Sealants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

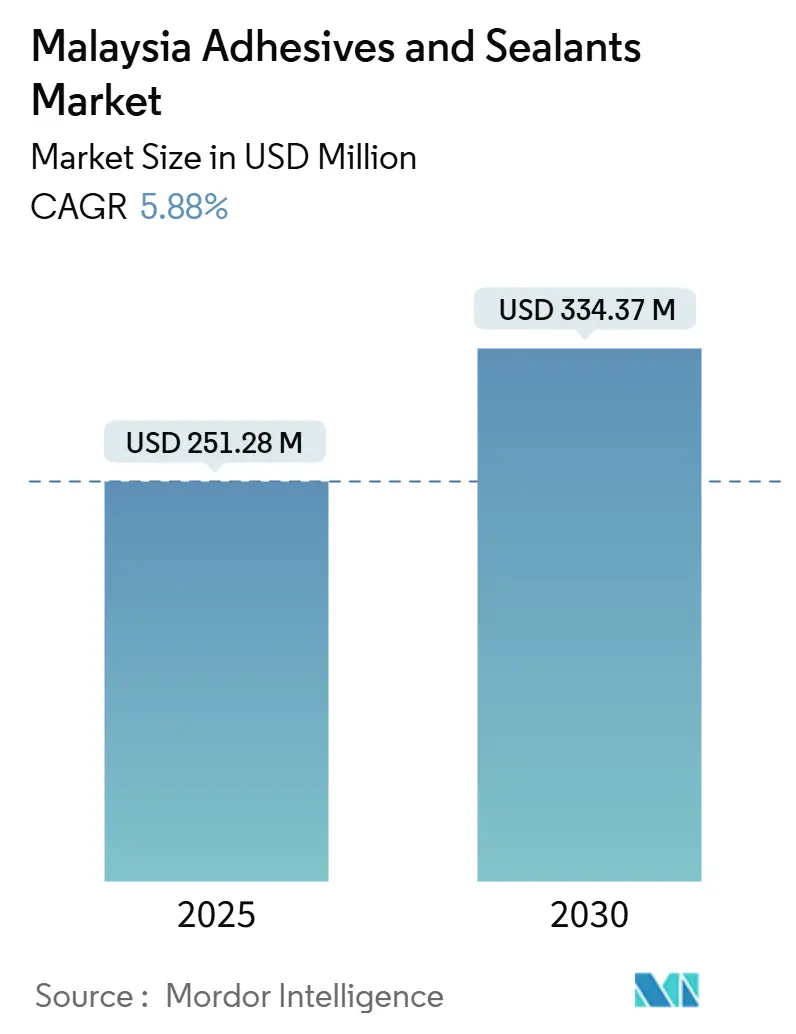

| Market Size (2025) | USD 251.28 Million |

| Market Size (2030) | USD 334.37 Million |

| Growth Rate (2025 - 2030) | 5.88% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malaysia Adhesives And Sealants Market Analysis by Mordor Intelligence

The Malaysia Adhesives and Sealants Market size is estimated at USD 251.28 million in 2025, and is expected to reach USD 334.37 million by 2030, at a CAGR of 5.88% during the forecast period (2025-2030). The trajectory reflects the nation’s role as a regional manufacturing hub where electronics assembly, automotive lightweighting, and large‐scale infrastructure programs converge to lift bonding-material demand. Packaging converters continue to anchor baseline volumes, yet the electric-vehicle build-out, semiconductor back-end investments, and tax-aided green building certifications are widening the application base. Technology adoption is equally dynamic: acrylic resins hold the largest formulation share, though polyurethane chemistries are advancing fastest, while UV-cured systems are gaining ground inside Penang’s high-throughput semiconductor lines. Competitive intensity remains moderate as global majors and regional specialists vie for share, and raw-material price swings coupled with stricter VOC rules shape near-term supply strategies.

Key Report Takeaways

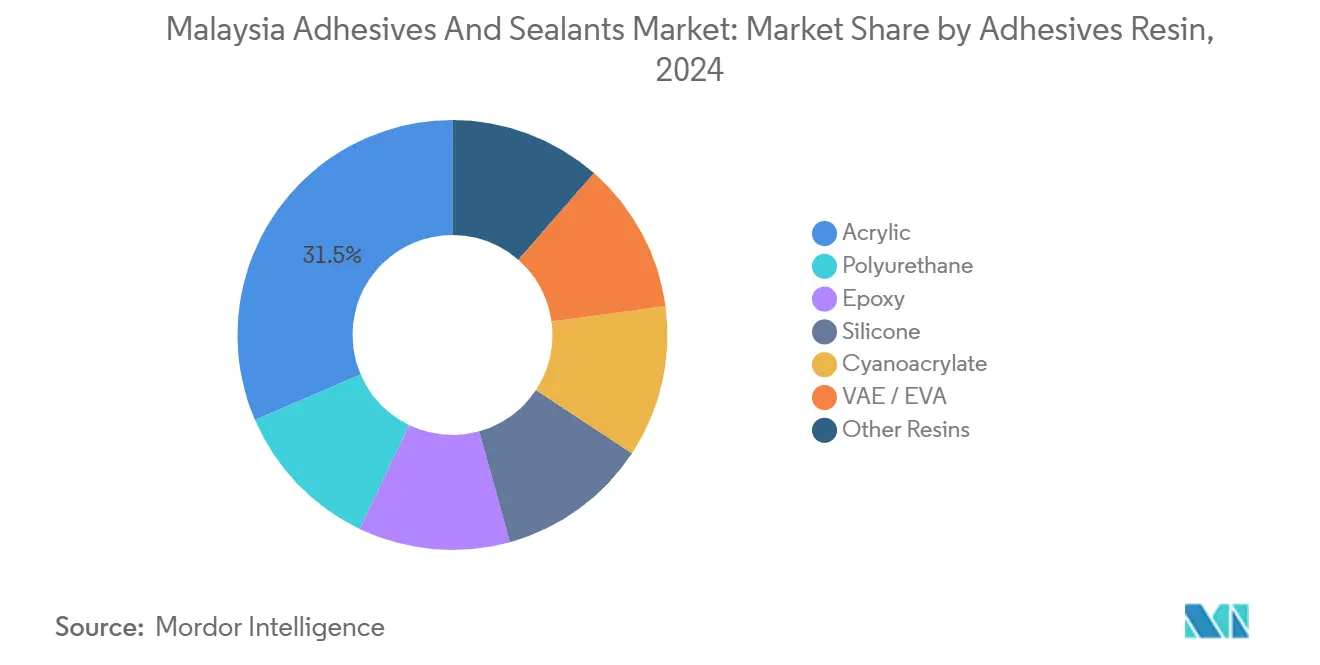

- By adhesives resin, acrylic captured 31.46% of the Malaysia adhesives and sealants market share in 2024, whereas polyurethane recorded the highest 6.47% CAGR projection through 2030.

- By adhesives technology, water-borne systems led with 42.37% of the Malaysia adhesives and sealants market size in 2024, yet UV-cured products are set for a 6.38% CAGR to 2030.

- By sealants resin, silicone held 45.28% revenue share in 2024, while polyurethane sealants will post the quickest 6.68% CAGR during the outlook period.

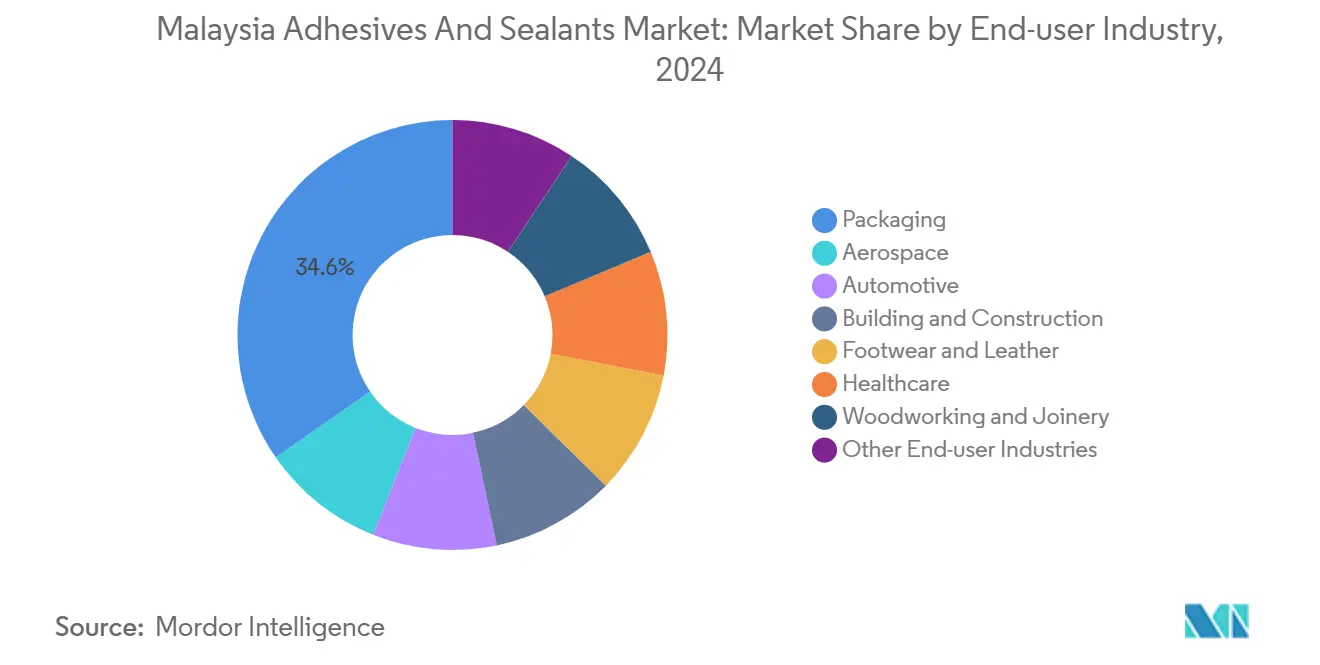

- By end-user industry, packaging accounted for 34.63% consumption in 2024, whereas automotive uses will expand at a 6.19% CAGR through 2030.

Malaysia Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid infrastructure and affordable-housing boom | +1.2% | National, with concentration in Klang Valley, Johor (Iskandar Malaysia), Penang | Medium term (2-4 years) |

| Expansion of FMCG and e-commerce flexible packaging | +1.0% | National, with logistics hubs in Selangor, Johor, Penang | Short term (≤ 2 years) |

| Accelerating electronics-assembly investments | +1.3% | Penang, Kedah (Kulim Hi-Tech Park), Johor (Iskandar Malaysia) | Short term (≤ 2 years) |

| Automotive lightweighting adoption | +0.9% | Perak (Tanjung Malim), Selangor (Shah Alam), Kedah | Medium term (2-4 years) |

| Growth of low-VOC green-building certifications | +0.7% | Urban centers: Kuala Lumpur, Penang, Johor Bahru | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Infrastructure and Affordable-Housing Boom

Malaysia has allocated significant funds for public works through 2025, including the MRT3 line and various highway extensions[1]Ministry of Finance Malaysia, “Budget 2024 Development Allocation,” mof.gov.my. These projects are driving a surge in annual consumption of tile adhesives and construction sealants. Even mid-tier contractors are now opting for epoxy and acrylic-latex blends that pass tropical durability tests. However, with payment cycles stretching to an average of several months in 2024, cash flow remains a challenge. While domestic formulators enjoy the advantage of being close to job sites, the unpredictable nature of projects necessitates inventory buffering, leading to increased warehouse costs. On the supply front, MAPEI's new facility in Johor, set to commence in 2026, will introduce additional adhesive capacity. This development ensures builders have quicker access to locally approved mixes. While the infrastructure drive promises consistent volume growth, it simultaneously underscores the financial challenges faced by smaller converters.

Expansion of FMCG and E-Commerce Flexible Packaging

In 2023, a surge in e-commerce shipments propelled corrugated demand, simultaneously boosting the use of flexible packaging for beverages and personal-care sachets. Nestlé, in a move signaling a shift in industry standards, invested in an expansion featuring solvent-free laminators. These new laminators utilize polyurethane dispersions that adhere to the EU 10/2011 regulations, setting a benchmark for exporters. The industry is increasingly gravitating towards mono-material polyethylene laminates. This transition has been hastened by Malaysia's roadmap to phase out certain plastics, nudging converters to adopt metallocene-catalyzed adhesives that demand more precise rheology control. Arkema's acquisition of Dow's laminating-adhesive division further enhances local access to these advanced chemistries. Collectively, these developments not only sustain high packaging volumes but also shift the focus towards more profitable, regulation-compliant grades.

Accelerating Electronics-Assembly Investments

Siliconware has pledged to establish an advanced packaging plant in Penang's semiconductor ecosystem. This plant will utilize underfill epoxies that cure in under five seconds, leading to a surge in demand for UV curing. TTM Technologies’ PCB line pursues a carbon-footprint cut by switching to UV solder masks, reinforcing low-VOC adoption. Local suppliers benefit from proximity, yet China’s quest for chip self-sufficiency may redirect CAPEX flows, raising competitive urgency in Malaysia. Henkel’s bio-attributed hot-melt wax partnership aligns with ESG targets that electronics OEMs track in supplier scorecards. Speed, reliability, and emissions metrics now collectively underpin adhesive specifications across the peninsula’s electronics corridors.

Automotive Lightweighting Adoption

Proton's new EV plant plans to use structural adhesives and polyurethane foam in each unit. With a target of producing cars annually by the end of 2025, this move is set to boost consumption in the segment. In 2023, national EV registrations increased. With policy aspirations set for significant growth by 2030, this trajectory could spur annual compound growth in vehicle assembly adhesives. Perodua's push for hybrid localization introduces multi-material joints. These joints, when bonded with adhesives, outperform spot welding, leading to reductions in both weight and cycle time. However, the industry faces a challenge: only one battery-cell plant has secured financial closure. As a result, substantial dedicated adhesive lines might see underutilization until local sourcing of cells becomes a reality. Currently, the supply chains are dependent on imported resins, introducing currency-related volatility into their cost structures.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and chemical-import rules | -0.6% | National, with stricter enforcement in Selangor, Penang | Short term (≤ 2 years) |

| Petro-feedstock price volatility | -0.8% | National, linked to global naphtha and ethylene markets | Medium term (2-4 years) |

| Limited local feedstock capacity | -0.5% | National, affecting specialty monomers and resins | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Chemical-Import Rules

Malaysia has set new VOC ceilings for interior coatings and exterior ones, effectively sidelining older solvent-borne formulations[2]Department of Environment Malaysia, “VOC Revision 2024,” doe.gov.my. Under OSHA regulations, SIRIM registration now takes several months and incurs high costs, leading to delayed launches and increased overhead. The upcoming standard for structural-glazing sealants incorporates ASTM protocols, but only a few local producers meet the criteria, pushing architects to favor premium imported silicones. Small and medium-sized enterprises (SMEs) are feeling the pressure: a recent MASA survey revealed that many of them are considering exiting the construction-sealant market instead of investing in re-formulation. In the short term, these compliance challenges are eliminating lower-cost options and stunting growth.

Petro-Feedstock Price Volatility

In 2024, Petronas Chemicals reduced rates at its Kerteh cracker as Asian ethylene prices dipped, leading to significant margin pressures for converters. In the same year, acrylic acid prices fluctuated, necessitating quarterly contract adjustments and complicating demand forecasting. Malaysia continues to rely heavily on imports, sourcing a large portion of its specialty monomers and epoxy bases. Consequently, when freight costs surged—evidenced by Port Klang rates, which increased following disruptions in the Red Sea—many local buyers hesitated to absorb these added expenses. While forthcoming domestic monomer expansions promise some relief, they only partially bridge the gap, leaving resin input risks prominent in the medium-term outlook.

Segment Analysis

By Adhesives Resin: Polyurethane Gains on Flexible-Packaging Shift

Polyurethane advanced at a 6.47% CAGR outlook by winning solvent-free laminating and EV structural slots. Acrylic continued to dominate at a 31.46% Malaysia adhesives and sealants market share in 2024 due to volume pull from pressure-sensitive labels and tile mortars. Epoxies captured a significant share, primarily for electronics and battery packs, while silicones accounted for a portion, focusing on high-temperature seals. VAE/EVA carved out a niche in woodworking, and cyanoacrylates held a modest share. Other minor resins filled in the remaining gaps.

Malaysia's halal ready-meal exporters drive the rapid adoption of polyurethane, drawn by its peel strength and its ability to endure sterility at high temperatures. Local converters, bolstered by tax rebates under NIMP 2030, are upgrading their metering systems to accommodate two-component grades. In a bid to maintain their market share, acrylic producers are enhancing water resistance in their D4-rated dispersions. Looking ahead, while the market size gains for Malaysia's adhesives and sealants are most pronounced in polyurethane, acrylics, with their established presence, continue to lead in total tonnage.

Note: Segment shares of all individual segments available upon report purchase

By Adhesives Technology: UV-Cured Systems Accelerate in Electronics

Water-borne lines led the 2024 ranking through a 42.37% share, a figure underpinned by VOC compliance. Solvent-borne lines captured a significant portion of the market, primarily for fast-track automotive tasks. Reactive epoxies and polyurethanes played pivotal roles in heavy structures. Hot melts, benefiting from bio-attributed wax upgrades that reduce Scope 3 emissions, also held a notable share. UV-cured grades occupied the smallest slice yet carry the steepest 6.38% CAGR.

Siliconware's back-end line in Penang underscores the production edge of five-second cures, steering demand towards photoinitiated chemistries. Although UV's constraints on opaque substrates hinder broader adoption, advancements in PCB masking, display lamination, and optical bonding are pushing boundaries. While UV volumes in Malaysia's adhesives and sealants market are negligible, their strategic significance in the electronics sector is pronounced.

By Sealants Resin: Silicone Leads, Polyurethane Climbs

Silicones answered for 45.28% 2024 volume thanks to unrivaled UV resistance and long-term tensile retention, key for solar-panel edge and curtain-wall joints. Acrylic sealants, favored for cost-sensitive interior applications, held a significant share. Polyurethane is projected to grow at 6.68% through 2030, driven by its demand in windshield bonding and its strong adhesion to both concrete and aluminum in expansion joints. Epoxy and other specialized resins make up the remainder.

With the introduction of the new MS 2753-1 standard, there's a push for quality enhancements. This shift is benefiting high-modulus neutral-cure silicones, especially those backed by documented ASTM data. Meanwhile, vendors of polyurethane are capitalizing on the gap left by non-compliant, lower-grade silicones, particularly in the automotive glass sector. For suppliers, a significant research and development challenge lies in aligning cure profiles to suit tropical humidity conditions.

By End-User Industry: Packaging Leads, Automotive Accelerates

Packaging consumed 34.63% of 2024 tonnage and preserves its pole position by shifting to recyclable mono-material films that continue to use adhesives rather than extrusion lamination. Building and construction held steady in second place. Electronics assembly claimed a significant portion, while woodworking, healthcare, and footwear collectively made up a notable share.

Automotive carries the fastest 6.19% CAGR on EV gluing and multi-material body structures. Once at full capacity, Proton will demand a substantial amount of structural epoxies. Healthcare's stake is set to rise, bolstered by H.B. Fuller's integration of its newly acquired GEM and Medifill assets into Penang's burgeoning medical-device hub. Overall, the growth of Malaysia's adhesives and sealants market is most notable where factors like export compliance, weight savings, and throughput gains align closely with customer economics.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, Penang's semiconductor hub will produce underfills, die-attach, and UV masks, with an expected boost as Siliconware and TTM increase their capacities. Selangor, a key player in FMCG and logistics, is set to drive a consistent demand for packaging adhesives through 2025. Meanwhile, Johor's Iskandar corridor, merging significant construction projects with furniture exports, is on track to capture a significant share of the nation's construction adhesive demand by 2030.

Perak's automotive sector, spurred by Proton's EV initiatives, is expanding, albeit at a modest pace. In 2024, Sabah and Sarawak accounted for a portion of the market, primarily driven by offshore maintenance and timber processing, despite facing higher delivery costs than Peninsular markets. While freight volatility and a reliance on resin imports expose inland states to supply fluctuations, ongoing highway developments promise to bridge the cost divide.

Malaysia's involvement in ASEAN supply chains presents a mixed bag. While NIMP 2030's tax incentives lure specialty-chemical investments, only a few monomer projects have been mechanically completed, underscoring the nation's continued dependence on imports. For Malaysia's adhesives and sealants sector, local integration could mitigate forex risks, but there's still uncertainty regarding the expansion of feedstock sources.

Competitive Landscape

The Malaysia adhesives and sealants market is moderately consolidated. Global producers hold leading positions, each leveraging regional plants to serve Malaysia quickly. Regulation is a competitive wedge. Only three domestic sealant firms meet MS 2753-1:2025. Market consolidation may follow as non-compliant players exit or partner for tech transfer.

Malaysia Adhesives And Sealants Industry Leaders

-

Henkel AG & Co. KGaA

-

Arkema

-

H.B. Fuller Company

-

3M

-

AICA ADTEK SDN. BHD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Henkel Adhesive Technologies introduced Loctite Liofol LA 7837/LA 6265, a solvent-free retort-grade adhesive that removes drying energy and lowers emissions.

- December 2024: Arkema finalized the acquisition of Dow’s flexible-packaging laminating-adhesive unit to reinforce polyurethane dispersion breadth.

Malaysia Adhesives And Sealants Market Report Scope

Adhesives are substances that bond two or more surfaces together to create a strong, lasting connection. Sealants are materials that are used to fill gaps to create a barrier against air, moisture, or other elements.

The Malaysia adhesives and sealants market is segmented by adhesives resin, adhesives technology, sealants resin, and end-user industry. By Adhesives Resin, the market is segmented into polyurethane, epoxy, acrylic, silicone, cyanoacrylate, VAE/EVA, and other resins. By Adhesives Technology, the market is segmented into water-borne, solvent-borne, reactive, hot-melt, and UV-cured. By Sealants Resin, the market is segmented into silicone, polyurethane, acrylic, epoxy, and other resins. By End-user Industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Cyanoacrylate |

| VAE / EVA |

| Other Resins |

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-Melt |

| UV Cured |

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Other Resins |

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

| By Adhesives Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Cyanoacrylate | |

| VAE / EVA | |

| Other Resins | |

| By Adhesives Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot-Melt | |

| UV Cured | |

| By Sealants Resin | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries |

Key Questions Answered in the Report

How fast is the Malaysia adhesives and sealants market expected to grow through 2030?

Value is projected to rise from USD 251.28 million in 2025 to USD 334.37 million by 2030 at a 5.88% CAGR.

Which resin family is gaining the most traction in flexible packaging?

Polyurethane systems are expanding at a 6.47% CAGR due to compliance with food-contact and solvent-free rules.

What drives the uptick in sealant demand inside construction?

Government infrastructure outlays, and Green Building Index incentives are pulling silicone and polyurethane sealants into curtain walls and expansion joints.

How do VOC regulations influence formulation strategies?

Limits of 250–300 g/L force a shift to water-borne, hot-melt, or UV-cured chemistries and raise compliance costs for solvent-borne lines.

Page last updated on: