Machinery Rental And Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 136.12 Billion |

| Market Size (2030) | USD 174.81 Billion |

| Growth Rate (2025 - 2030) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

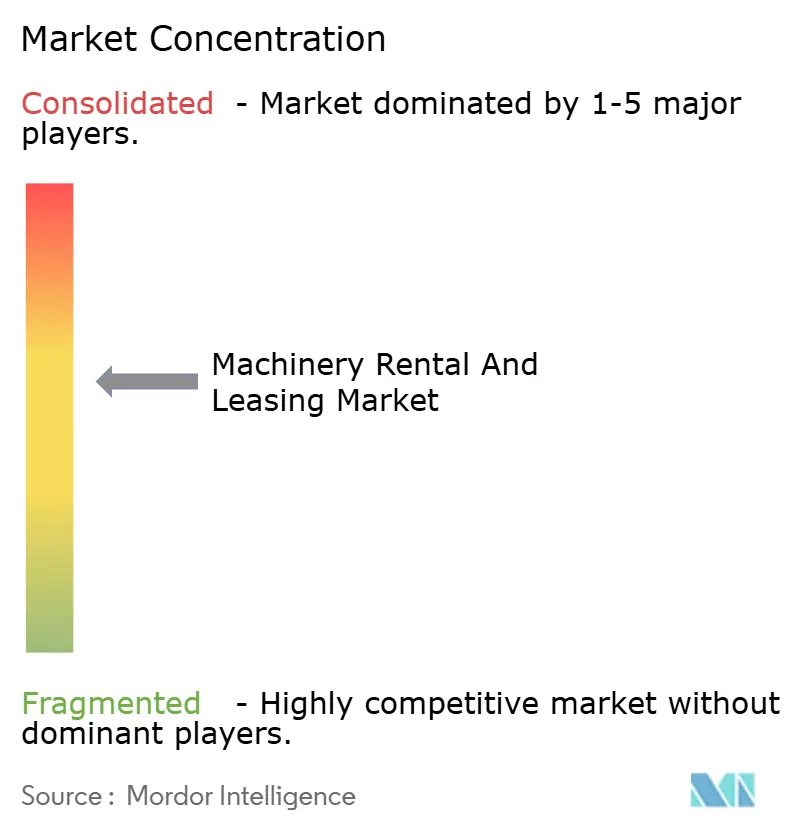

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Machinery Rental And Leasing Market Analysis by Mordor Intelligence

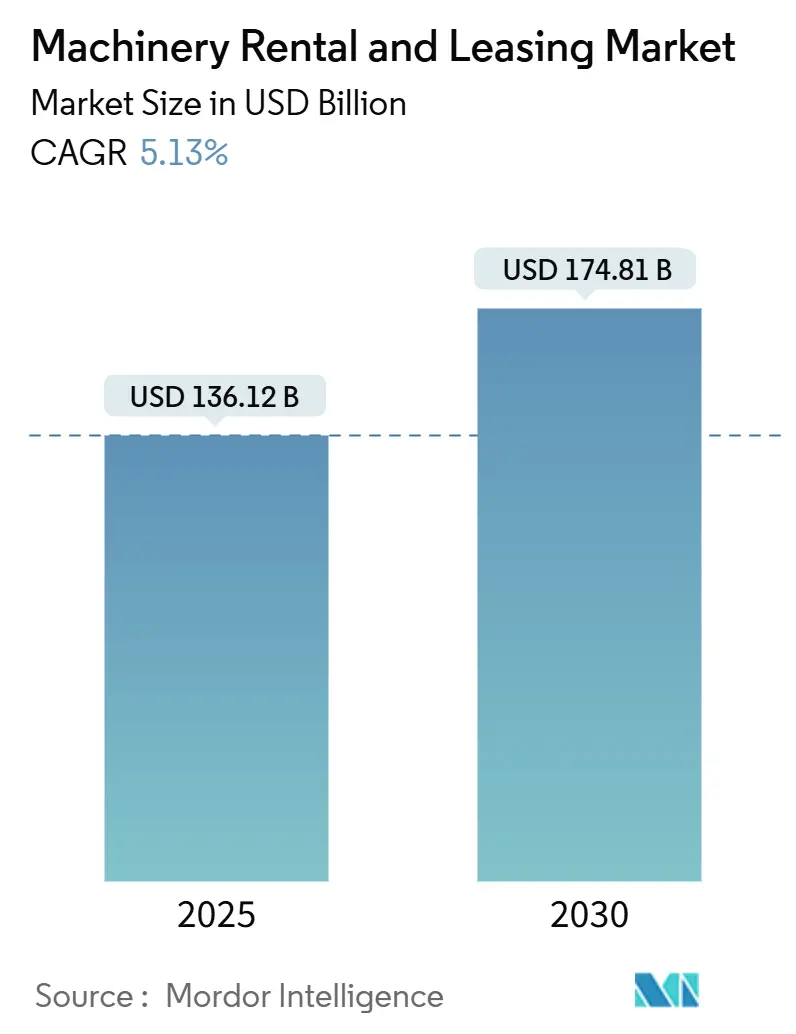

The machinery rental and leasing market size is estimated at USD 136.12 billion in 2025, and is expected to reach USD 174.81 billion by 2030, at a CAGR of 5.13% during the forecast period (2025-2030). Sustained infrastructure spending in the United States, the European Union, and Asia-Pacific underpins demand as enterprises favor flexible equipment access over ownership. High capital costs, accelerating technology cycles, and stringent sustainability mandates to steering corporate and public buyers toward rental or lease options. Digital marketplaces further widen the addressable customer base by shortening procurement lead-times, while telematics enhances fleet visibility, which improves utilization and return on assets. Growth pockets emerge in material-handling applications, government procurement, and hybrid Equipment-as-a-Service contracts that bundle analytics and maintenance.

Key Report Takeaways

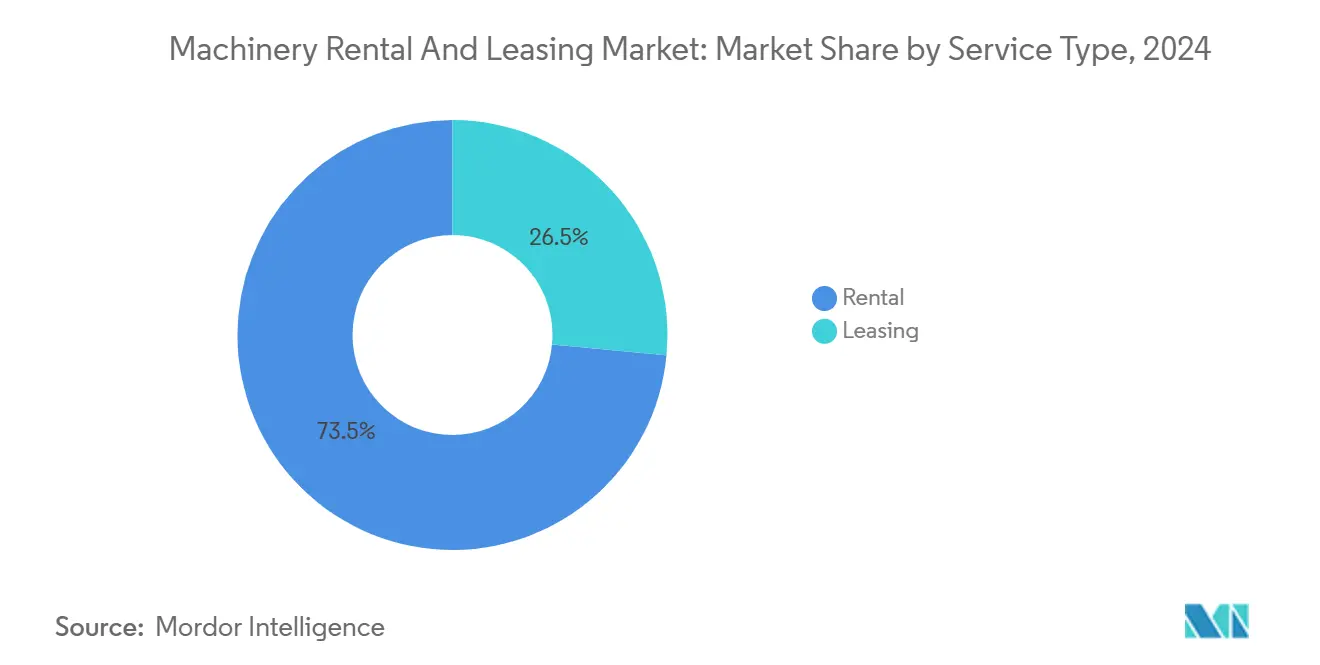

- By service type, rental services accounted for 73.46% revenue share in 2024. Leasing will post the fastest expansion at a 5.18% CAGR through 2030.

- By equipment type, construction equipment held 41.28% of the machinery rental and leasing market share in 2024. Material-handling equipment is forecast to advance at a 5.21% CAGR to 2030.

- By customer type, SMEs contributed 54.73% of transactions in 2024. Government agencies are anticipated to grow at a 5.24% CAGR through 2030.

- By mode of rental, offline distribution retained 87.61% of revenue in 2024, while online channels are set to climb at a 5.15% CAGR to 2030.

- By geography, North America captured 35.53% of global value in 2024. Asia–Pacific is projected to register a 5.17% CAGR between 2025 and 2030.

Global Machinery Rental And Leasing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise Of Infrastructure Megaprojects | +1.2% | Global, concentrated in North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| High Equipment Ownership Cost | +0.8% | Global | Medium term (2-4 years) |

| Surging Demand For Short-Cycle Capex Flexibility | +0.7% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Digital Rental Platforms | +0.6% | Global, led by North America | Medium term (2-4 years) |

| Equipment-As-A-Service (EaaS) | +0.5% | North America and Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| ESG Pressure To Optimise Utilisation | +0.4% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Infrastructure Megaprojects Drives Equipment Demand

A federal investment package in the United States and a climate transition program across the European Union extend equipment orders well into the next decade. China’s Belt and Road Initiative, attracting massive revenue in cumulative capital, deepens rental penetration across Southeast and Central Asia. Rental fleets absorb project-specific demand spikes more efficiently than owner-operators because specialized machinery can be redeployed at the project closeout stage. Contractors in California, Texas, and Florida tap rental agreements to execute in state-level road and bridge projects scheduled for completion by 2028 [1]“Building a Better America Fact Sheet,” The White House, whitehouse.gov . High utilization in megaproject corridors strengthens pricing power for fleet operators and reinforces the equipment-as-a-service narrative that pairs availability with guaranteed uptime.

High Equipment Ownership Cost Accelerates Rent-Versus-Buy Decisions

Since 2022, prices for new earth-moving and lifting machinery have significantly increased. This spike is largely attributed to rising costs in steel, electronics, and freight, which have inflated OEM material bills. Concurrently, parts shortages have driven maintenance expenses higher each year. This trend is eroding the profitability of low utilization rates, a norm in cyclical construction. Rental contracts have become a strategic move, allowing fleet operators to sidestep risks associated with technology obsolescence and capital lock-in. These operators frequently refresh their assets on a large scale. Instead of making substantial investments in single units, contractors are now opting for rentals. This shift grants them immediate access to cutting-edge electric and autonomous models, all integrated with IoT diagnostics. Consequently, there's been a notable increase in rental penetration, especially among midsize builders and specialty trades, who are navigating tight project-cycle milestones.

SME Demand for Short-Cycle Capex Flexibility Intensifies

Small and medium enterprises account for more than half the global customer base. These firms face uneven order books and credit constraints, prompting an operational preference for pay-per-use machinery. Port delays and semiconductor shortages that extend delivery lead-times from the customary three months to a year further push SMEs toward rental. Online marketplaces allow next-day equipment dispatch, compressing project mobilization timelines and letting SMEs preserve working capital for payroll, raw materials, and marketing. The flexibility edge widens because rental contracts embed compliance inspections and insurance, reducing administrative load on lean SME back-office teams [2]“2025 Small Business Economic Profile,” U.S. Small Business Administration, sba.gov .

Digital Platforms Transform Customer Acquisition and Fleet Optimization

Asset-light brokers such as EquipmentShare and BigRentz deploy artificial intelligence that allocates inventory across depots based on real-time demand signals. Telematics data informs predictive maintenance algorithms that cut idle hours, shrink downtime by one-third, and extend service life without compromising safety. Lower idle ratios allow platforms to offer dynamic discounts during low-demand periods while preserving margin through surge pricing in peak seasons. The software layer standardizes contract workflows and electronic payments, accelerating repeat bookings and widening the machinery rental and leasing market beyond traditional contractor segments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Supply-Chain Volatility | -0.9% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Rising Interest Rates Lifting Financing Costs | -0.6% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Secondary Equipment Glut | -0.4% | North America and Europe primarily | Medium term (2-4 years) |

| Data-Security and Cyber-Risk | -0.3% | Global, highest impact in digitally advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Supply-Chain Volatility Inflates Fleet Acquisition Costs

OEM lead times have significantly increased due to shortages in steel, microchips, and hydraulic components. As a result, invoice prices have risen considerably compared to previous levels. Rental companies are delaying fleet refresh cycles, causing machines to age beyond their optimal reliability. While operators are trying to mitigate rising maintenance costs through rate adjustments, the competitive market limits the extent of recovery. Some operators are adopting strategies such as placing bulk orders or diversifying their supplier base in regions like India and Mexico, but freight bottlenecks are reducing the effectiveness of these measures. Despite strong demand indicators, these challenges are putting pressure on profit margins and delaying expansion into new geographic areas.

Rising Interest Rates Increase Fleet Financing Expenses

Benchmark borrowing costs in the United States surged from near zero to more than one-fifth by 2025, forcing equipment financiers to reprice loans at a minimal rate for investment-grade lessees. Smaller regional rental firms pay double-digit rates, which raises hurdle rates for new fleet procurement. Costlier capital slows depot expansion plans and nudges some providers to lengthen replacement intervals, which may erode customer perception of equipment availability and quality. Interest rate inflation thus weighs on the machinery rental and leasing market by tempering supply expansion during a period of elevated demand [3]“Open Market Operations in 2025,” Federal Reserve Board, federalreserve.gov .

Segment Analysis

By Service Type: Rental Dominance Amid Leasing Acceleration

The machinery rental and leasing market size attributed to rental services was fairly high in 2024. Rental keeps leadership because contractors value the short-term alignment of payments with project cash flows, also accounting for 73.46% market share. High churn fleets enable providers to redeploy assets regionally, which sustains high utilization and supports consistent returns even when construction cycles soften.

Leasing gains traction, generating an exponential growth by 2030, with a CAGR of 5.18% through 2030, as manufacturers, energy companies, and logistics operators lock in multi-year equipment access under predictable cost structures. Accounting rule changes that place operating leases on balance sheets no longer sway the rent-versus-lease decision as strongly, shifting selection criteria toward uptime guarantees, technology refresh provisions, and embedded maintenance. Hybrid Equipment-as-a-Service contracts blur legacy boundaries by fusing rental flexibility with the multiyear continuity inherent in leasing.

By Equipment Type: Construction Leadership With Material-Handling Momentum

Construction equipment accounted for 41.28% of global revenue in 2024. Fleet providers stock excavators, aerial work platforms, and tower cranes aligned to public-works timetables in the United States and Europe.

Nevertheless, material-handling equipment revenue is set to grow significantly by 2030 due to e-commerce fulfillment expansion. The segment’s 5.21% CAGR reflects warehouse automation rollouts where robotic pallet movers and telescopic handlers are essential yet episodically utilized, making rental the rational choice. Logistic center saturation across the Midwest United States and coastal China sustains steady month-to-month utilization, smoothing seasonal peaks often seen in construction.

By Customer Type: SME Dominance With Government Acceleration

In 2024, SMEs generated 54.73% of the machinery rental and leasing market. Their preference for variable cost structures and zero depreciation risk keeps rental intensity high.

Government agencies rank as the fastest-growing buyer group with a CAGR of 5.24% through 2030, driven by federally funded highway, bridge, and renewable energy initiatives. Public buyers also lean on fleet operators for Occupational Safety and Health Administration certifications and carbon reporting, duties that strain municipal procurement departments. Large corporations use rental to cover maintenance shutdowns and temporary capacity boosts during major capital upgrades, while individuals tap mobile apps for do-it-yourself landscaping and small renovation projects.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Rental: Digital Transformation Accelerates Online Growth

Offline depots produced 87.61% of 2024 turnover due to entrenched contractor relationships and the hands-on nature of heavy machinery inspections. Even so, online channels are projected to grow exponentially by 2030, reflecting a 5.15% CAGR.

Platforms integrate inventory search, contract e-signature, and logistics scheduling in a single interface that especially suits light equipment and short-duration rentals. Brick-and-mortar dealerships adopt hybrid models where digital storefronts secure reservations and depot staff handle delivery, training, and service calls. This convergence improves visibility into future fleet availability, supporting smarter asset rotations and capex planning.

Geography Analysis

North America contributed significantly to global revenue in 2024, representing 35.53% of the machinery rental and leasing market. Sustained federal infrastructure disbursements and private housing refurbishments underpin robust utilization. United Rentals alone recorded vast rental revenue, anchoring capacity expansion and setting regional rate benchmarks. Canada’s resource extraction rebound adds steady demand for earth-moving equipment, particularly in Alberta oil sands and British Columbia mining operations.

Asia–Pacific will expand exponentially by 2030, with a 5.17% CAGR. China’s domestic rental turnover grew significantly in 2024, propelled by Belt and Road logistics construction and rapid urban redevelopment of tier-two cities. India’s National Infrastructure Pipeline targets roads, airports, and metro rail through 2030, elevating demand for cranes, concrete pumps, and compaction machinery. ASEAN member states also invest in port and renewable projects that lean on rental fleets for specialized lifting and piling equipment [4]“National Infrastructure Pipeline Progress Update,” Ministry of Finance India, nip.gov.in .

Europe generated a massive revenue in 2024 with stable, policy-driven growth. The EU Green Deal funnels funds into offshore wind foundations, grid modernization, and hydrogen pilot plants, each requiring bespoke lifting and on-site power solutions that favor rental over ownership. Stricter carbon disclosure rules encourage fleet operators to adopt electric mini excavators that can be rotated across multiple users, spreading the premium acquisition cost while meeting urban emission caps.

Competitive Landscape

In 2024, the top five companies commanded a significant share of the global revenue, indicating a moderate concentration and leaving space for regional contenders. United Rentals, with a vast network of depots, leverages data analytics to fine-tune its fleet mix and pricing based on zip codes. Ashtead Group, operating as Sunbelt Rentals in the United States, is on a fast track, with numerous new locations added through a mix of greenfield expansions and bolt-on acquisitions. Rounding out the top tier, Loxam, Aggreko, and Herc Rentals are each channeling investments into telematics and predictive maintenance to enhance asset turnover.

New-age players like EquipmentShare and BigRentz are carving a niche, focusing on platform scalability and an asset-light brokerage model. Harnessing artificial intelligence, they adeptly match latent demand with underused third-party assets. This strategy not only boosts revenue for regional owner-operators but also ensures a healthy margin spread. Notably, patent filings have seen a significant increase for telematics, fleet management software, and dynamic pricing algorithms, underscoring a heightened commitment to R&D, even from traditional hardware-centric players.

Industry players are adopting three primary strategies. Those leaning towards scale-driven consolidation benefit from purchasing discounts and a denser network. Digital innovators find value in data monetization and efficient matchmaking. Meanwhile, niche experts target lucrative segments, such as renting HVAC chillers for data centers or providing aerial access for wind turbine upkeep. The machinery rental and leasing sector is thus navigating a path between the advantages of consolidation and the depth of localized expertise, with emerging partnerships aiming to blend these strengths seamlessly.

Machinery Rental And Leasing Industry Leaders

-

United Rentals Inc.

-

Ashtead Group plc (Sunbelt Rentals)

-

Herc Holdings Inc. (Herc Rentals)

-

WillScot Mobile Mini Holdings Corp.

-

H&E Equipment Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tadano Ltd. divested Rabern Rentals to Sunbelt Rentals, sharpening its focus on core crane competencies and reshaping its North American footprint.

- April 2025: CASE introduced compact wheel loaders, a telescopic-boom small articulated loader, and upgraded compact track and skid steer loaders, all targeted at rental fleets.

Global Machinery Rental And Leasing Market Report Scope

The machinery rental and leasing market covers the latest equipment rental and leasing demand trends, technological development, government policies, manufacturer developments, etc. The report covers a complete background analysis of the market. it includes an assessment of the market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles.

Machinery rental and leasing markets are segmented by type, mode, and region. By type, the market is sub-segmented into mining, oil and gas, forestry machinery and equipment rentals, commercial air, rail, and water transportation equipment rentals, heavy construction machinery rentals, office machinery and equipment rentals, and other commercial and industrial machinery and equipment rentals. By mode, the market is sub-segmented into offline and online. By region, the market is sub-segmented into North America, Europe, Asia-pacific, South America, the Middle East, and Africa. The report offers market size and forecasts for the machinery rental and leasing market in value (USD) for all the above segments.

| Rental |

| Leasing |

| Construction Equipment |

| Industrial Equipment |

| Agricultural Equipment |

| Material Handling Equipment |

| Small and Medium Enterprises (SMEs) |

| Large Corporations |

| Government Agencies |

| Individual Users |

| Online |

| Offline |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Service Type | Rental | |

| Leasing | ||

| By Equipment Type | Construction Equipment | |

| Industrial Equipment | ||

| Agricultural Equipment | ||

| Material Handling Equipment | ||

| By Customer Type | Small and Medium Enterprises (SMEs) | |

| Large Corporations | ||

| Government Agencies | ||

| Individual Users | ||

| By Mode of Rental | Online | |

| Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What revenue level does North America contribute to the machinery rental and leasing market in 2024

The region generated USD 48.3 billion, equivalent to 35.53% of global value.

Which equipment category is expanding the fastest

Material-handling equipment is forecast to grow at a 5.21% CAGR through 2030

How quickly are online rental platforms growing

Online channels are set to record a 5.15% CAGR and reach USD 30.0 billion by 2030

Why do SMEs favor rental over ownership?

Rental eliminates high upfront capex, mitigates technology obsolescence, and provides next-day equipment access.

What impact do rising interest rates have on fleet operators

Borrowing costs climb to 7%-9% for investment-grade firms, reducing appetite for rapid fleet expansion

Which company leads global revenue rankings

United Rentals tops the league with USD 11.2 billion in rental revenue and more than 1,400 locations.

Page last updated on: