Market Overview

| Study Period | 2020 - 2031 |

|---|---|

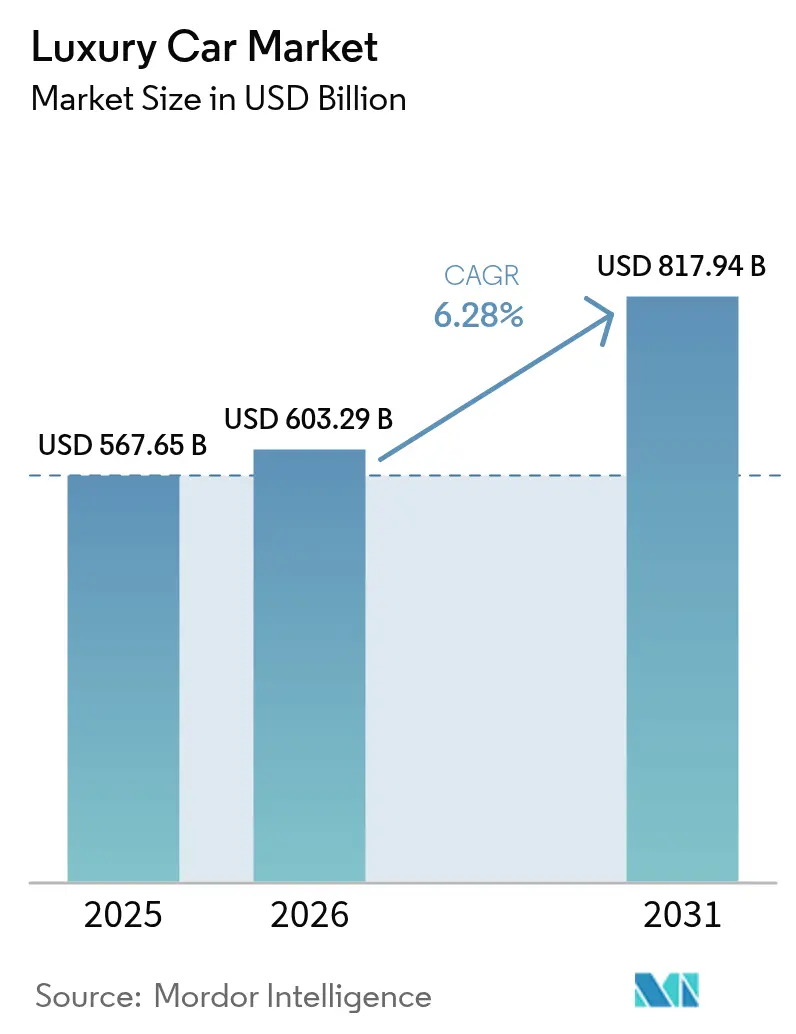

| Market Size (2026) | USD 603.29 Billion |

| Market Size (2031) | USD 817.94 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

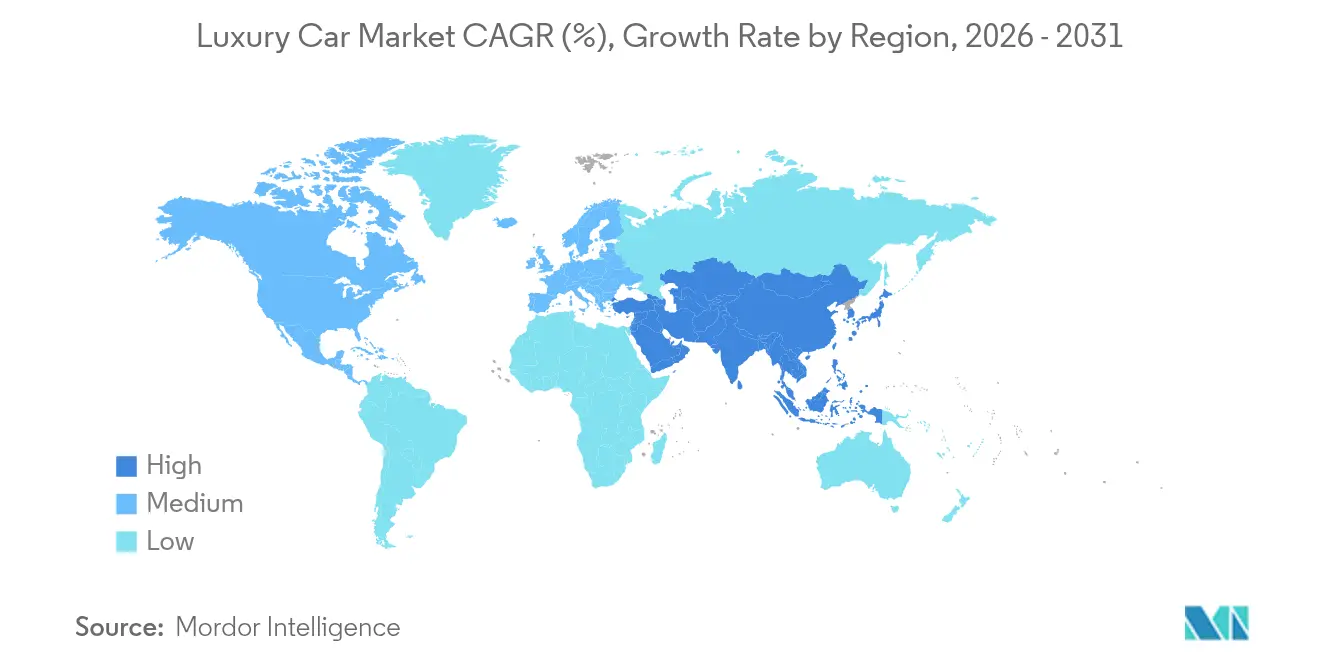

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Car Market Analysis by Mordor Intelligence

The luxury car market size is expected to grow from USD 567.65 billion in 2025 to USD 603.29 billion in 2026 and is forecast to reach USD 817.94 billion by 2031 at 6.28% CAGR over 2026-2031. Rapid wealth creation in Asia-Pacific, the accelerating rollout of battery-electric flagships, and a widening emphasis on personalized, eco-conscious mobility are the core growth engines. Despite ownership-cost inflation and lingering supply-chain kinks, the luxury car market continues to outpace the broader auto sector as premium makers monetize software, customization, and direct sales channels. Competitive pressure is intensifying as Chinese up-market brands and Tesla’s pure-play EV strategy push established European and U.S. marques toward faster electrification, richer digital services, and leaner retail footprints.

Key Report Takeaways

- By vehicle type, sports utility vehicles led with 55.78% of luxury car market share in 2025; sedans are projected to grow at a 7.78% CAGR through 2031.

- By drive type, internal-combustion models retained 68.35% of the luxury car market size in 2025, while battery-electric vehicles are set to expand at a 8.79% CAGR.

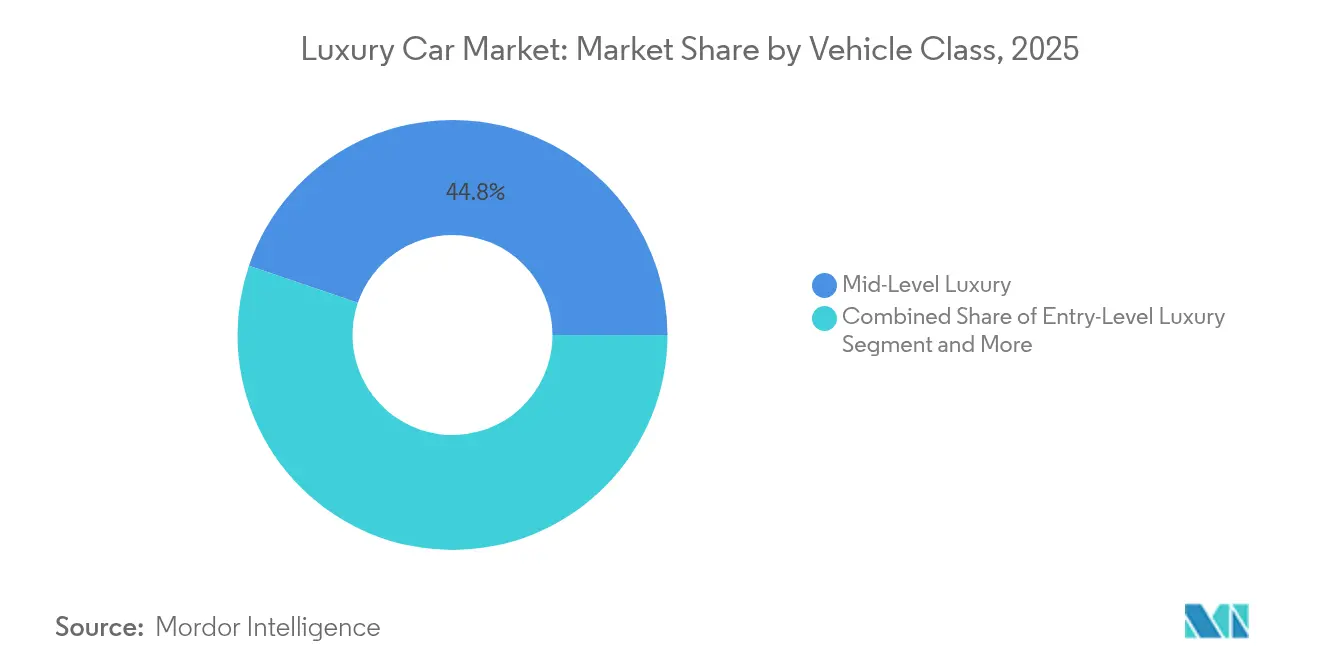

- By vehicle class, mid-level luxury captured 44.78% of the luxury car market size in 2025; ultra-luxury is advancing at an 7.92% CAGR to 2031.

- By sales channel, authorized dealerships held 89.62% share of the luxury car market size in 2025, but direct-to-consumer platforms are climbing at a 8.86% CAGR.

- By geography, Asia-Pacific accounted for a 42.75% luxury car market share in 2025; the Middle East & Africa region is forecast to post the fastest 7.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury SUV Demand | +1.8% | Global (Asia-Pacific, North America strongest) | Medium term (2–4 years) |

| Premium Electrification | +1.5% | Europe, China leading | Long term (≥ 4 years) |

| Rising HNWI in Asia & Middle East | +1.2% | Asia-Pacific core, Middle East acceleration | Long term (≥ 4 years) |

| ADAS and Safety Expectations | +0.9% | North America and Europe, spreading to Asia-Pacific | Medium term (2–4 years) |

| Direct-to-Consumer Retail | +0.7% | Global | Short term (≤ 2 years) |

| Mass Customization & Bespoke Options | +0.6% | Ultra-luxury focused | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Premium Models

Battery-electric derivatives represent the fastest-growing drivetrain, supported by premium makers that position EVs as halo showcases for quiet torque and cutting-edge tech rather than regulatory compliance plays. In India, Mercedes-Benz’s EV sales grew 94% year-on-year through May 2024, led by the locally-built EQS 580 SUV[1]“Q3 2024 Investor Presentation,”, Mercedes-Benz Group AG, group.mercedes-benz.com. BMW delivered 1,249 pure EVs in India the same year, supporting them with fast chargers in 51 cities. Ultra-luxury brands remain cautious: Aston Martin shifted its first EV launch to 2026 for additional powertrain refinement. Ferrari filed patents for synthetic exhaust acoustics to retain emotional appeal in silent drivetrains[2]“Synthetic Exhaust Sound System Patent,”, European Patent Office, european-patents.office. The luxury car market will increasingly judge electrification success on how well brands preserve identity traits such as sound, ride, and craftsmanship.

Rising HNWI Population in Asia and Middle East

Asia-Pacific's luxury vehicle market is surging, driven by an expanding base of affluent consumers. As wealth levels rise, especially among first-time buyers and those seeking upgrades, the demand for premium mobility intensifies. India is a pivotal player, with luxury vehicle sales doubling in recent years. Projections show a continued rise in ultra-high-net-worth individuals, hinting at a shift towards aspirational consumption and a promising long-term market outlook.

In the Gulf region, buoyant oil prices have bolstered disposable incomes, fueling a robust demand for luxury vehicles. Brands such as BMW have grown significantly, underscoring the region's enthusiasm for premium automotive offerings. With a blend of economic resilience and a penchant for high-end mobility, the Gulf solidifies its status as a prime market for luxury OEMs.

Enhanced ADAS and Safety Expectations

The 2025 Cadillac LYRIQ offers Super Cruise with automatic lane-change on compatible roads and includes safety features such as pedestrian detection via Automatic Emergency Braking; availability varies by trim and market. The EU General Safety Regulation (EU) 2019/2144 makes ADAS such as Intelligent Speed Assistance and Automatic Emergency Braking mandatory on new vehicles (phased in from July 2022 and July 2024), while the separate Euro 7 regulation addresses pollutant, brake, and tyre emissions and durability requirements.

Online/Direct-to-Consumer Retail Shift

Tesla’s factory-to-customer model exposed dissatisfaction with dealership haggling and spurred luxury incumbents to invest in digital showrooms, fixed pricing, and concierge-style delivery. Mercedes-Benz now sells the EQE and EQS families online in multiple EU markets, capturing richer data and reducing inventory carrying costs. Regulatory franchising rules are slowly being adopted in parts of the U.S., yet the luxury car market’s e-commerce share is still expected to double by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Ownership Cost | -1.4% | Global (emerging markets acute) | Short term (≤ 2 years) |

| Semiconductor Shortages | -0.9% | Global supply chain impact | Short term (≤ 2 years) |

| Demand Volatility | -0.8% | Developed markets sensitivity | Medium term (2–4 years) |

| SUV Climate Regulation Pressure | -0.5% | Europe & California leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor and Component Shortages

Even with new wafer fabrication facilities launching post the 2022 chip shortage, there's still a tight supply of specialty automotive microcontrollers. This is especially true for those integral to infotainment and comfort systems. As a result, premium OEMs face tough choices: they deliver vehicles missing certain features or push back customer handovers.

Take Mercedes-Benz, for instance. The luxury automaker recently had to delay allocations of its flagship S-Class, underscoring that even elite models aren't shielded from these chip shortages. Such disruptions hit hardest in low-volume, high-content luxury vehicles. These models, dependent on specialized components, have limited leeway in production adjustments.

Anti-SUV Climate Regulation Pressure

Euro 7 and California ACC II tighten CO₂ ceilings and will impose escalating penalties on heavy SUVs unless they shift to zero-emission platforms. Porsche offsets extra fleet emissions by bundling carbon-credit purchases into vehicle price tags via its Impact program. While electric luxury SUVs such as the Mercedes-Maybach EQS mitigate regulatory risk, compliance costs still erode margins, shaving an estimated 0.5 percentage points from the luxury car market’s headline CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Drive Premium Segment Transformation

SUVs controlled 55.78% of the luxury car market size in 2025 and are predicted to post an 7.84% CAGR to 2031. Mercedes-Benz’s SUV roster secured record revenue and over 120 early orders for the AMG G 63 on its first retail day. Sedans keep cultural cachet in chauffeur-driven contexts and certain ultra-luxury niches; however, their relative share diminishes as younger owners prioritize the multi-utility profile of SUVs. Entry-luxury hatchbacks and MPVs remain minor, geography-specific plays, while supercars anchor brand desirability despite negligible volume. Ferocious SUV momentum cements the body style as the luxury car market’s leading profit contributor for the foreseeable horizon.

SUV-centric product roadmaps now dominate R&D prioritization. Audi moved flagship PPE EV development resources toward its Q6 e-tron to pre-empt BMW iX and Mercedes EQS SUV launches. Land Rover is extending its SV Bespoke studio to cater to Range Rover clients seeking one-off materials and colorways, reinforcing the mass-customization uptick discussed earlier. As emission targets tighten, electrified SUV variants will become the default compliance strategy rather than a niche derivative, keeping the luxury car market on an SUV-led growth trajectory.

By Drive Type: Electric Acceleration Reshapes Powertrains

Internal-combustion models still represented 68.35% of the luxury car market size in 2025, but battery-electric entries are sprinting ahead at a 8.79% CAGR. Mercedes-Benz and BMW have already mainstreamed 400-volt architectures into core models, and Porsche has frozen new ICE platform investment beyond 2027. Hybrids offer a transitional buffer in regions lacking fast-charging density; Lexus saw a hybrid uptake for its LM minivan launch in China. Ultra-luxury marques favor a staggered roll-in; Aston Martin rescheduled its debut EV to 2026, arguing for additional refinement of ride and cabin sound characteristics. Powertrain diversification remains a balancing act between regulatory compulsion, infrastructure readiness, and brand heritage yet the long arc points toward electrified dominance within the luxury car market.

Electric-only skateboards also facilitate software-defined interiors. Tesla commands premium-EV mindshare via in-house chipsets and full-self-driving updates, nudging rivals toward deeper vertical integration. Mercedes’ MB.OS will roll out across all EQ models after 2025, enabling paid feature over-the-air upgrades that could lift revenue per vehicle by USD 1,200 over a four-year cycle. Such digital monetization strengthens the rationale for accelerated BEV share gains.

By Vehicle Class: Ultra-Luxury Defies Economic Headwinds

Mid-level luxury held 44.78% of the luxury car market size in 2025, but ultra-luxury is the fastest-expanding band at an 7.92% CAGR. India's luxury vehicle market is growing rapidly, driven by rising affluence and an expanding millionaire demographic. High-end models like the Mercedes-Benz Top-End Vehicle range and BMW's X7 are seeing strong demand, reflecting a preference for premium, feature-rich vehicles. Entry-level luxury models face increasing competition from tech-savvy mass-market crossovers, which offer similar features at lower price points, pressuring the lower end of the luxury market. The ultra-luxury segment thrives on exclusivity and personalization. Brands like Ferrari leverage bespoke offerings, with personalization revenue cushioning margins against economic challenges. This segment benefits from wealth concentration and focusing on unique, prestige-driven consumer experiences.

By Sales Channel: Digital Disruption Accelerates

Authorized dealers still captured 89.62% of luxury car market share in 2025; however, direct-to-consumer storefronts are scaling at a 8.86% CAGR. Tesla sold every U.S. Model S and Model X online, demonstrating that premium buyers accept no-haggle digital journeys. Mercedes-Benz now executes fixed-price e-commerce in Germany and the U.K. across its EQ lineup, supplementing dealerships with boutique experience centers. Franchise laws constrain full rollout in select U.S. states, prompting hybrid click-and-collect models. As OEMs aim for lifetime software and service revenues, control of end-customer data becomes a strategic imperative, making further share migration toward online channels inevitable for the luxury car market.

Geography Analysis

Asia-Pacific commanded 42.75% of the luxury car market share in 2025, underpinned by China’s scale and India’s meteoric rise to 50,000 premium units sold, equal to six vehicles every hour. Nevertheless, Mercedes-Benz warned of softer Q1 2025 deliveries amid equity volatility, validating the region’s sensitivity to capital-market swings. China’s domestic marques erode German share as NEV penetration tops 40.9%, pressuring incumbents to localize tech partnerships and brand messaging.

The Middle East shows the steepest 7.96% CAGR through 2031, buoyed by oil-linked disposable income and infrastructure expansion. BMW tallied a 15.4% volume uplift across Gulf Cooperation Council states 2024, led by X7 and 7 Series demand. UAE total automotive sales advanced 15.7%, confirming robust macro tailwinds. South Africa and Türkiye add incremental gains but are subject to currency gyrations that can delay purchase decisions; premium makers mitigate risk with regional production hubs and U.S.-dollar invoicing options.

North America remains a mature but steady pillar for the luxury car market, with affluent demographics offsetting interest-rate-driven payment inflation. Canada’s resource windfall aids luxury penetration, while Mexico is graduating toward premium vehicles as rising middle-class wealth intersects with improved credit access. Europe faces the heaviest regulatory drag via Euro 7 and fleet CO₂ fines, yet maintains entrenched brand loyalty. OEMs are converging on high-margin electric SUVs to absorb compliance costs, leveraging in-house battery plants and renewable-energy credits to defend profitability.

Regulatory Landscape

Luxury-car programs are increasingly shaped by fleet CO2, pollutant, and safety mandates, which raise compliance content per vehicle and accelerate electrification and ADAS packaging. In the European Union, Regulation (EU) 2019/631 sets a fleet-wide average CO2 reduction requirement of 15% for 2025-2029 versus a 2021 baseline, reinforcing the shift toward battery-electric flagships and lower-emission powertrains across premium portfolios. The EU General Safety Regulation (EU) 2019/2144 also phases in mandatory safety and ADAS features (with milestones in July 2022 and July 2024), making functions such as Automatic Emergency Braking and Intelligent Speed Assistance standard-fit considerations for luxury trims.

Policy updates in 2025-2026 add both clarity and near-term execution complexity for global OEMs. The EU presented an Automotive Package on 16 December 2025, including revisions to CO2 performance standards and an omnibus-style simplification effort, signaling parallel focus on decarbonization and industrial competitiveness. In the United States, NHTSA postponed major New Car Assessment Program (NCAP) roadmap changes from the 2026 to the 2027 model year (announced in September 2025), while continuing to credit manufacturer attestations for some ADAS performance in MY2026. In May 2026, NHTSA also sought comment on adding Rear Automatic Braking with pedestrian avoidance capability into NCAP, pushing luxury brands to validate sensing, braking, and software performance beyond current feature availability claims.

Value Chain Analysis

The luxury-car value chain spans premium materials and engineered components (aluminum, high-grade leather, advanced glazing), powertrain systems (ICE, hybrid modules, e-axles), and a fast-expanding electronics and software stack (ADAS sensors, infotainment domains, connectivity, and OTA update infrastructure). Upstream supply remains exposed to bottlenecks in specialized automotive semiconductors and critical raw materials for electric motors, with suppliers and OEMs pursuing design substitutions and sourcing diversification to reduce dependence on constrained inputs. Traceability and compliance demands are also strengthening cross-company data exchange, including through ecosystems such as Catena-X to improve supply-chain transparency and support regulatory reporting needs.

Manufacturing and assembly are becoming more regionally anchored, with luxury OEMs investing in dedicated BEV and high-end production footprints while retaining craftsmanship-oriented finishing for top trims and hypercars. Facility actions reflect this dual-track structure, combining electrified capacity expansions with purpose-built low-volume exclusivity sites. Examples include BMW completing a USD 1.7 billion investment in Spartanburg, South Carolina (supporting fully electric BMW output), Mercedes-Benz commencing all-electric C-Class production at the expanded Kecskemét plant in Hungary after a EUR 1 billion investment, and Bugatti inaugurating La Manufacture in Molsheim, France, to support Tourbillon production. On the distribution side, authorized dealer networks still dominate luxury retail, but OEM-controlled digital storefronts and fixed-price models are increasingly integrated into the go-to-market flow to capture customer data and software-service revenue post-sale.

Competitive Landscape

Key players such as Mercedes-Benz Group AG, BMW AG, Volkswagen Group, and Tesla Inc. dominate the luxury car market. The key players are engaged in continuous product launches and R&D investments, highly driven by advanced technology, more comfort, growing investment in EV technology, and improved living standards worldwide.

Strategic M&A is also reshaping the field. Volkswagen and Rivian signed a USD 5.8 billion JV to co-develop next-generation premium EV platforms, giving Audi and Bentley direct access to Rivian's skateboard tech. McLaren’s acquisition of Forseven expands its battery IP pipeline, illustrating how niche supercar brands secure future relevance. Meanwhile, Cerence’s AI voice pact with Jaguar Land Rover indicates rising cross-industry alliances as tech suppliers court luxury OEMs for early-adopter margins.

Incumbent strengths include expansive service footprints and generational brand equity, yet Chinese upstarts leverage local supply chains and agile direct-sales models to undercut European pricing. Tesla continues to erode traditional share by offering Level 2+ autonomy as a subscription. Consequently, incumbents are redoubling investments in bespoke programs, experiential marketing, and lifetime digital services to protect their luxury car market franchises.

Luxury Car Industry Leaders

Volkswagen Group

Tesla Inc.

Mercedes-Benz Group AG

BMW AG

Toyota Motor Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrified luxury platforms and localized manufacturing footprints are creating room for premium OEMs and key suppliers to reposition capacity, reduce supply risk, and scale high-margin software-enabled features. In North America, BMWs completed USD 1.7 billion investment around Plant Spartanburg and a supporting supply network underscores continued capex directed at EV-capable luxury production. Mercedes-Benz announced a USD 4 billion investment plan for its Tuscaloosa, Alabama facility (to be deployed by 2030) supporting electric and SUV manufacturing. These moves pair with supplier-side localization, including Bosch starting sample production of silicon carbide chips at its Roseville, California site following a USD 225 million federal subsidy, reinforcing a pathway for more secure access to high-voltage power electronics used in premium BEVs.

Opportunities also sit in ultra-luxury personalization, low-volume precision manufacturing, and new premium body styles that combine EV architectures with SUV-led demand. Bugattis opening of La Manufacture in Molsheim (capacity cited at 200 cars per year) highlights ongoing investment into dedicated, high-control facilities for hypercars and bespoke builds, where craftsmanship, materials sourcing, and brand-specific engineering remain differentiators. On the product and retail side, luxury OEMs expanding direct-to-consumer capabilities, including Mercedes-Benz online sales for EQ families in multiple EU markets and Teslas factory-to-customer model, create whitespace for integrated digital purchasing, concierge delivery, and post-sale software monetization, provided brands align feature availability with evolving safety-assessment roadmaps such as NHTSAs NCAP updates and the EUs ADAS mandates.

Recent Industry Developments

- June 2026: BMW Group completed a USD 1.7 billion investment in South Carolina to expand Plant Spartanburg and add supporting capacity for fully electric BMW models. The upgrade strengthens regional EV manufacturing resilience and shortens logistics for high-content luxury components, which helps stabilize output amid electronics and critical-material supply volatility.

- May 2026: NHTSA issued a request for comment to inform the NCAP roadmap, including the potential addition of Rear Automatic Braking with pedestrian avoidance capability. The step raises the bar for validated ADAS performance in premium vehicles, pushing luxury OEMs and suppliers to prioritize sensing, software calibration, and test evidence that aligns with future safety-rating criteria.

- April 2024: Li Auto introduced the Li L6, a mid-to-large-size luxury 5-seater family SUV featuring a 1.5T range extender, a 36.8 kWh LFP battery, and a dual-motor intelligent 4WD system. The launch reinforces the competitive intensity from Chinese brands in electrified luxury SUVs, expanding choice in a segment that already leads global luxury-car volume.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of luxury passenger cars sold. Vehicles are considered luxury when they are positioned and priced above mass-market cars, typically supported by higher comfort, performance, technology, and brand positioning. Coverage is tracked across major automotive regions.

Scope exclusions: This sizing does not count mass-market passenger cars, commercial vehicles, and two-wheelers, even when they have premium trims or high-end features.

Segmentation Overview

- By Vehicle Type

- Hatchbacks

- Sedans

- Sports Utility Vehicles (SUVs)

- Multi-purpose Vehicles (MPVs)

- Sports / Exotic

- By Drive Type

- Internal Combustion Engine (ICE)

- Hybrid Electric

- Battery Electric

- By Vehicle Class

- Entry-level Luxury

- Mid-level Luxury

- Ultra-luxury / Exotic

- By Sales Channel

- Authorized Dealership

- Direct-to-Consumer / Online

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle-East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle-East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we start by building a clean fact base around luxury passenger vehicle sales and value signals, then align it with how the auto industry reports registrations, deliveries, and trade flows. Public sources such as national vehicle registration agencies, customs and trade statistics portals, central bank FX and inflation series, and road transport ministries are used to anchor basic market direction by geography. We also review International Organization of Motor Vehicle Manufacturers (OICA) updates, International Energy Agency (IEA) notes on electrification, and peer-reviewed transport and mobility journals to understand how the powertrain mix and policy shifts are changing demand.

To translate this fact base into a workable model, broader secondary materials such as annual reports, SEC-style filings where available, investor decks, and automaker press releases are reviewed for delivery trends, pricing commentary, and product cycle timing. In selected cases, paid subscriptions are used to speed up checks on company financials and intelligence, news and financials coverage, and patent databases, which helps validate directionally what is changing in powertrain features and software-led upgrades. These desk sources are illustrative and not exhaustive, and additional public references are used during data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that cannot be fully read from public datasets, especially the split between entry-level luxury and ultra-luxury positioning, discounting behavior, and the adoption pace for electrified luxury models. We spoke with stakeholders across OEM and dealer networks, component and technology ecosystems, and fleet and leasing touchpoints, plus industry specialists. Coverage was balanced across APAC, EMEA, and the Americas, so regional differences in pricing and mix could be captured rather than assumed from one geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 19% | APAC: 45% |

| Mid tier: 44% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 20% | Managers: 45% | Americas: 19% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where passenger vehicle sales and registrations by country are filtered into a luxury-addressable pool using brand and model positioning cues. Then, value is reconstructed using region-specific average selling price ranges and mix weights. To keep the totals from drifting, we run selective bottom-up checks using sampled model line-ups, perform channel checks on transaction pricing, and use supplier-side commentary on high-value content per vehicle. The model is adjusted when gaps appear.

Key inputs in the model include luxury vehicle unit sales by region, the SUV share shift within luxury sales, the powertrain mix trend (ICE versus hybrid and battery-electric), typical price band movement by region in nominal terms, and FX conversion timing for multi-country rollups. For forecasting, scenario analysis is used as the core technique, since demand is sensitive to interest rates, consumer confidence, and policy support for electrification, and these drivers were also discussed repeatedly in interviews. Where direct data is thin for smaller countries, we use proxy indicators such as premium import shares and registration growth, then reconcile implied volumes with realistic pricing bands before the value is finalized.

Data Validation & Update Cycle

Validation is done by checking the modeled value against independent signals such as luxury passenger vehicle registrations, reported delivery trends, and region-level price movement, which helps flag outliers early. When a variance is seen, assumptions are reviewed step by step, and follow-up calls are triggered with relevant respondents to confirm whether the change is real or a modeling artifact. Before sign-off, the work goes through internal analyst reviews to keep logic, math, and scope alignment consistent across regions.

The report is refreshed annually, with interim updates when material events occur, such as major policy changes on emissions, sharp FX moves, or meaningful shifts in luxury EV launches. Right before delivery, a final pass is completed so clients receive the latest market view using the most current public releases and validated assumptions.

Mordor Intelligence's Luxury Car Market Size Compared With Other Published Estimates

Published luxury car market values can vary a lot because each publisher draws the line differently on what counts as luxury, how they treat ultra-luxury and sports models, and whether they rely on list prices or transaction-level pricing logic. Timing also matters, since FX conversion, inflation adjustments, and the chosen base year can push the value up or down even when unit trends are similar.

In practice, the biggest gaps usually come from scope expansion into broader premium categories, aggressive assumptions on electrified luxury pricing uplift, and limited cross-checking of unit volume signals against registration and delivery metrics. The spread is also widened when a single global ASP is applied without reflecting that APAC and Europe can have very different mix and discount patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 603.29 B (2026) | |

| Global Consultancy A | USD 1570.00 B (2026) | This figure appears to use a wider definition that can fold premium and super luxury categories together, and it is often paired with a higher assumed SUV-led pricing uplift across regions. |

| Industry Publisher B | USD 749.00 B (2025) | This estimate is anchored to a different base year and can rely on broad regional averages, which may not fully reflect mix changes between SUVs, sedans, and electrified luxury models. |

The table indicates that the gap is mostly explained by what gets counted as luxury and how pricing is translated from units into value, rather than by disagreement on demand direction. By keeping the scope tied to luxury passenger cars and using region-sensitive mix and FX timing checks, a more traceable number is produced, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the global luxury car market in 2026?

The luxury car market size stands at USD 603.29 billion in 2026.

Which vehicle type dominates premium sales?

SUVs lead, capturing 55.78% of 2025 volume and growing at an 7.84% CAGR.

What is driving rapid luxury EV adoption?

Performance, sustainability branding, and stricter Euro 7 and China mandates are propelling a 8.79% CAGR for battery-electric models.

Which region is growing fastest through 2031?

The Middle East & Africa region is forecast to expand at an 7.96% CAGR.

Are dealer networks losing relevance in premium segments?

Direct-to-consumer channels still hold only 10.38% share but are expanding rapidly as Tesla and Mercedes-Benz prove the model’s appeal.

Page last updated on: